Note: This is the second blog in a three-part series: Know what you own; Know where you want to go; Know how to get there.

“Occasionally when I’ve high conviction in an idea, . . . I’ll thump the table more widely. I wish to thump it now.”

That was the opening line in an email I received on February 20, 2016. The email came from Gerard Fitzpatrick, our fixed-income CIO at Russell Investments, announcing that he felt the time was right to significantly add high-yield-bond exposure to our fixed-income and multi-asset portfolios. High-yield spreads were over 800 basis points at the time. The market was still shaken by the energy price falls of the previous year and by the perceived potential for widespread defaults, but Gerard saw this as a massive potential opportunity that outweighed the risks. The call turned out to be prescient.

This was no accident. Gerard’s call was not an isolated act, but the product of a process engineered to find the best possible investments. This process is a combination of time-tested investment beliefs, real-time insights and supportive analytics and quantitative models orchestrated by our investment teams—all designed to find the right combination of assets at the right time. Because nothing is more important than this when it comes to delivering desired investment outcomes to our clients.

The preferred position: A process of determination

In my previous blog in this series, I discussed the importance of knowing what you own in your portfolio. As vital as that information is, it is a commentary without a counterpoint, if, as an investor, you don’t know where you would like the portfolio to be. We believe portfolios must constantly adapt to succeed. They must adjust to shifts in fundamentals, market dynamics and macro forces that impact the valuations of assets.

At Russell Investments, clearly knowing where we want to be allows us to take the data on our current portfolio position and match it against our preferred position—a constant testing effort—while keeping in mind everything we know about capital markets. This begs the obvious question: How do we determine our preferred position?

The answer is two-fold.

- For long-term views, we adhere to a time-tested set of strategic beliefs.

- And for more tactical views, we analyze current market conditions through our three lenses of cycle, valuation and sentiment (CVS).

In analogous terms, think of the strategic beliefs as our anchor. Our tactical views shift, but are always tied to that anchor point. Many times our tactical views are right in line with our strategic beliefs. In fact, we operate with a first do no harm approach. If we don’t have a strong tactical view, we stick with our long-term beliefs. You may find that some asset managers may use a benchmark as their anchor. But we believe strategic beliefs work better than a benchmark.

Our strategic beliefs are not designed per se, but are more of the result of natural selection—beliefs that are proven and battle-scarred over decades, resulting in what we believe are superior correlation characteristics and better overall risk/return profiles. These beliefs draw us back to center, so that while we may often tilt in a short-term direction to increase a more tactical return or avoid a short-term risk, we depend on our strategic beliefs to bring us back.

Let’s walk through an example.

When it comes to value, one of our strategic beliefs states that stocks with lower valuation characteristics generate higher returns. This strategic belief gives us a long-term bias toward value stocks and a tendency to overweight that style. But there are certain times when our CVS analysis tells us that value looks less attractive. And that’s when our tactical views kick in.

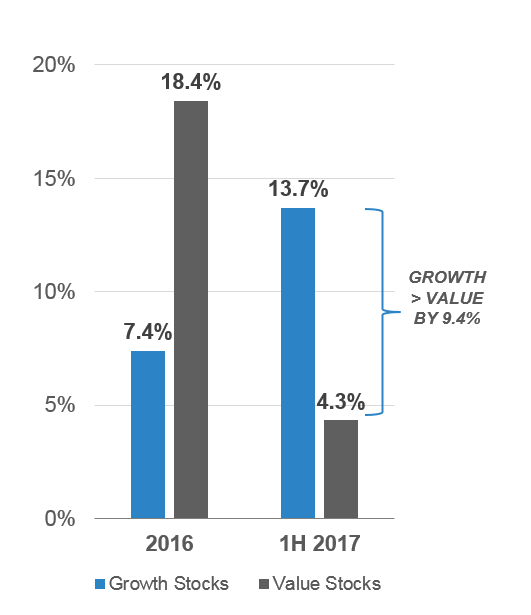

For example, in 2016, we witnessed value outperform growth very strongly, as measured by the Russell 3000® Index. According to our CVS data, it was time to sell high and take profits. That was the short-term view. But because of the balancing force of our strategic beliefs—our long-term view that included a bias toward value—our final actions were significant-but-limited, and did not create a major portfolio upheaval. The result was a slight overweight toward growth in our portfolios.

Chart: Strong quarter for growth managers

Source: Russell 1000® Growth Index, Russell 1000® Value Index Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investments

In the final blog post in this series, we’ll talk about what we believe are the best practice processes for making moves like this happen with the least amount of portfolio inefficiency. But in the meantime, we’ll keep our tactical views anchored to our strategic beliefs, because we feel certain this is the best way to invest. We won’t always get this right, but we believe a structured investment process will create discipline to add incremental value.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

Investing involves risk and principal loss is possible.

Past performance does not guarantee future performance.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

This material is not an offer, solicitation or recommendation to purchase any security. Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Indexes are unmanaged and cannot be invested in directly.

The Russell 3000® Index measures the performance of the largest 3000 U.S. companies representing approximately 98% of the investable U.S. equity market.

The Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and lower expected growth values.

The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments' management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

Copyright © Russell Investments Group LLC 2018. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI-11164