The Advent of a Cynical Bubble

Membership required

Membership is now required to use this feature. To learn more:

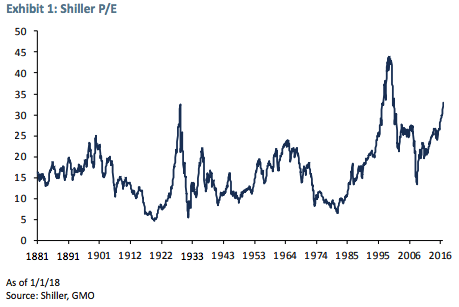

View Membership BenefitsThat the US equity market is obscenely overvalued can hardly be news to anyone. Even a cursory glance at Exhibit 1 reveals that we are now at the second most expensive level of the Shiller P/E ever seen – surpassed only by the TMT bubble of the late 1990s!

Only a handful of what we might call valuation deniers remain. They are dedicated to finding new and inventive ways to make equities look reasonable, and they have never yet met a bull market that they didn’t love.

As we have documented before, the Shiller P/E isn’t perfect,1 but it does a pretty good job of providing a really simple way of checking valuation. Nor is it unique in showing the US equity market to be extremely expensive.2 So for all the hand-wringing over the inclusion of 2009 in the 10-year average, the lack of robustness, shifting payout policy, etc., that haunts discussions based on the Shiller P/E, it is still a very powerful metric.3

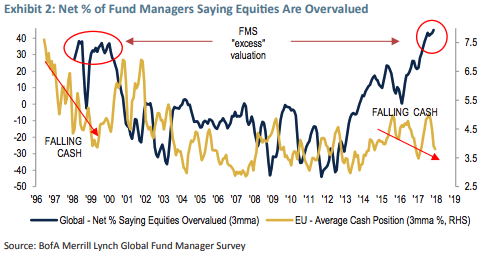

This is not news to most institutional investors. A recent Bank of America ML survey showed the highest level of those citing “excessive valuation” ever (see Exhibit 2).

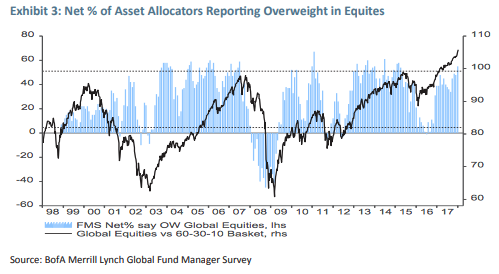

Yet despite this, the same survey showed fund managers to still be overweight in equities (see Exhibit 3). This gives rise to the existence of that strangest of creatures: the fully-invested bear. The most common rationale for such a cognitively dissonant stance is “the fear of missing out on the upside”(aka FOMO – fear of missing out). As I think Seth Klarman pointed out long ago, this isn’t really fear at all, but rather greed.

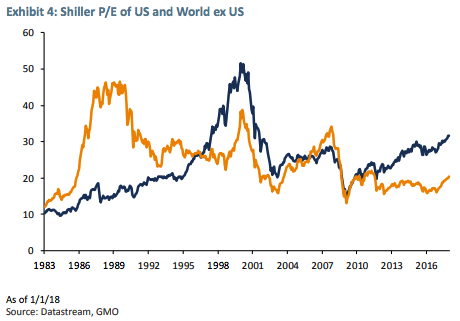

It is possible that the cognitive dissonance of the fully-invested bear might not be as puzzling if the US equity market was the only expensive market. That is to say, if the overweight position in equities held by these investors resulted from owning a lot of cheap non-US markets. Indeed, as Exhibit 4 shows, the rest of the world is certainly cheaper than the US.

But, sadly, saying something is cheaper than the US is not the same thing as its being cheap in absolute terms. Rather, it is akin to standing next to a pigmy and declaring oneself a giant. So whilst we agree that if you must own equities you should own non-US equities, it is hard to argue that they are not expensive in their own right, which makes it hard for us to want to be overweight equities as an asset class.

The fully-invested bear seems to essentially subscribe to Jeremy Grantham’s market melt-up scenario. I certainly can’t rule such an occurrence out. The strongest piece of evidence for it from a personal perspective comes from my own track record of being early in calling bubbles. In 1995 I wrote a piece arguing that Thailand would be the next Mexico (2 years too early); in 1997 I wrote piece arguing we were witnessing the last hurrah in equity markets (3 years too early); and in 2005 I wrote a piece on the bubble in US housing (2 to 3 years too early). This is the curse of those who follow the edicts of value. Valuation is a useful long-term indicator, but not a good short-term indicator. So perhaps the best way to read my research is to put it in a drawer for two years and then take it out and read it!

Jeremy’s case centers around the fact that many of the psychological hallmarks of the classical bubbles are absent. Effectively, we don’t have the euphoria associated with the great bubble peaks. However, I suspect this is an overly narrow definition of a bubble. In the past I have drawn on a taxonomy of bubbles that seeks to separate out four different kinds of bubbles.4 It should be noted that these bubbles are not always mutually exclusive, and many real-world bubbles exhibit characteristics from more than one type of bubble.

A taxonomy of bubbles

The first and canonical type of bubble is the what might be called the “Fad” or the “Mania.” This is truly a bubble of belief. In this type of bubble, people really do believe that this time is different, that a new era has been begun. These are the great bubbles of history: the TMT bubble, the Japanese bubble, the US housing bubble, and the Roaring 20s all stand out as shining examples of delusional new age thinking.

The second type of bubble is described as an intrinsic bubble. In an intrinsic bubble, it is the fundamentals that are the source of the bubble. That is to say, earnings booming at an unsustainable rate, which then often gives rise to extrapolation and overcapitalization by investors. Financials during the US housing bubble were a good example of this kind of bubble. Their earnings were inflated by the economic bubble in the housing market, and this wasn’t recognized by many investors.

The third type of bubble is known in the academic literature as a near rational bubble. I am not a great fan of this nomenclature as it suggests a veneer of respectability that I find undeserved. To me these are really better described as greater fool markets. They are cynical bubbles in that those buying the asset in question don’t really believe they are buying at fair price (or intrinsic value), but rather are buying because they want to sell to someone else at an even higher price before the bubble bursts. Chuck Prince, the former CEO of Citibank, aptly demonstrated the typical cynical bubble mentality when in July of 2007 he uttered those fateful words, “As long as the music is playing, you’ve got to get up and dance. We are still dancing.”

I would suggest that this is exactly the sort of market we are observing at the current juncture. Fund managers for the most part all agree that the US market is expensive but still they choose to own equities – a cynical career-risk-driven position if ever there was one. I have been amazed by the number of meetings I’ve had recently where investors have said they simply “have to own US equities.”

For completeness, the fourth type of bubble is what is known as an informational bubble. I am not going to dwell on this kind of bubble here as I don’t believe it is apposite to the current situation. Suffice to say, this is a situation in which people stop acting on their own private information and start acting on the revealed information of others. You can think of it as an investor saying, “Well I think the US market is expensive, but all these other investors can’t be wrong, so I will override my own view and buy because they must be right.” A touching faith in the wisdom of crowds, if you will.

So, I agree with Jeremy that many of the psychological hallmarks of the Fad or Mania are absent. But to me today’s is a cynical bubble, built not on faith in a new era, but on overoptimism about the ability to get out before everyone else. As Keynes opined,

The actual, private object of most skilled investment today is to ‘beat the gun’… This battle of wits to anticipate the basis of conventional valuation a few months hence, rather than the prospective yield of an investment over the long term, does not even require the public to feed the maws of the professionals; it can be played by professionals amongst themselves.

Experimental Evidence

To help bolster the case that not all bubbles require euphoria, we can turn to the experimental asset market literature, which is based on the premise that most of the elements of the market can be controlled in a way that simply isn’t possible in the real world.

For example, let’s assume that the asset being traded has a known life, with an expected dividend paid in incremental periods during that life. The dividend payout varies depending upon four equally likely states of the world, and the amounts paid under each outcome are known. The asset has zero worth at the end of the game. Thus, the expected value of the assets is the payout of each state of the world multiplied by the probability of each state of the world multiplied by the number of periods left in the game.

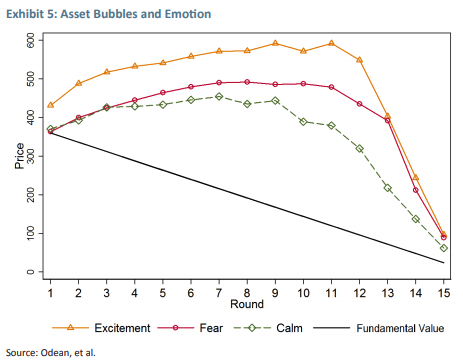

It is well-known that such markets can witness bubbles wherein asset prices are significantly above their intrinsic value. However, in this particular case we are interested in the impact of emotion upon the scale of the bubble. Odean, et al.5 investigated exactly this.

They simulated various emotional states by having participants watch a variety of video clips. To simulate excitement, they were shown car chases; to simulate fear, horror films. A base condition was achieved by showing participants a neutral historical documentary.

Exhibit 5 shows the results of the experiment. Fundamental value slopes downwards from left to right, decreasing by an amount equal to the expected dividend each period. However, each of the emotional states and the neutral condition created bubbles. That is to say, prices traded miles above intrinsic value. For instance, if we look at Round 7, we can see that prices are, at minimum, approximately twice fundamental value.

Now, to get a really monster bubble, the participants needed to be feeling very excited (euphoric). This created a bubble that in Round 9 was three times intrinsic worth. So, to get a true Mania and the associated bubble it would appear that optimism was a necessary condition. But to get run-of-the-mill bubbles, it simply wasn’t required.

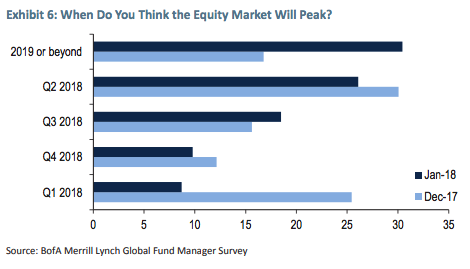

We also have experimental evidence on just how hard it is to be one step ahead of everyone else, which is presumably what the bubble riders are intent upon doing. Indeed, the aforementioned fund manager survey shows that nearly 70% of fund managers expect the equity markets to peak at some point this year.

As Keynes noted,

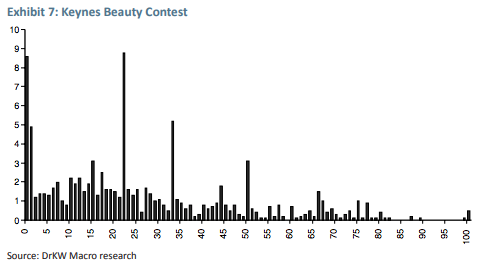

Professional investment may be likened to those newspaper competitions in which the competitors have to pick out the six prettiest faces from a hundred photographs, the prize being awarded to the competitor whose choice most nearly corresponds to the average preferences of the competitors as a whole; so that each competitor has to pick, not those faces which he himself finds prettiest, but those which he thinks likeliest to catch the fancy of the other competitors, all of whom are looking at the problem from the same point of view. It is not a case of choosing those which, to the best of one’s judgment, are really the prettiest, nor even those which average opinion genuinely thinks the prettiest. We have reached the third degree where we devote our intelligences to anticipating what average opinion expects the average opinion to be. And there are some, I believe, who practise the fourth, fifth and higher degrees.

A game based on this idea can be constructed where participants are told to choose a number between 0 and 100. The winner will be the person who picks the number closest to two-thirds of the average number picked.

In one of my previous existences I set up such a game. The players were all professional investors and I had over 1000 participants (making it the fourth or fifth largest game played, and the only played purely by professional investors).

The fact I got a number of answers above 66 is a little disturbing! The highest possible answer is 66, because to pick this one must believe that everyone else has just picked 100. In Exhibit 7, you can see spikes at various levels of induction. The average number picked turned out to be 26 (which is fairly typical of such games), and thus the two-thirds average was 17.4. It proved incredibly hard to be one step ahead of everyone else in this game.

Bursting Cynical Bubbles

I have already confessed a pathetic lack of ability when it comes to timing a bubble’s demise. It is one of the many reasons I regularly extol the concept of patience as a symbiotic to following a valuebased approach.

However, I do know that cynical bubbles are based on a belief that one can get out before everyone else. Obviously, this is simply impossible. Like a game of musical chairs played at a child’s birthday party, when the chairs are increasingly rare, the competition for them gets fiercer. Crowded exits don’t end well – inevitably some are crushed in the stampede.

Now, perhaps you are skilled at picking the managers with great timing ability, and perhaps those managers do have great timing ability, in which case, good luck. As for me, I prefer to leave the party early, in the knowledge that I can walk away with ease.

In closing I can’t do better than repeat the words of caution offered by Keynes:

It is the nature of organized investment markets, under the influence of purchasers largely ignorant of what they are buying and speculators who are more concerned with forecasting the next shift of market sentiment than with a reasonable estimate of future yield of capital - assets, that, when disillusion falls upon an over-optimistic and over-bought market, it should fall with sudden and catastrophic force.

James Montier. Mr. Montier is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2009, he was co-head of Global Strategy at Societe Generale. Mr. Montier is the author of several books including “Behavioural Investing: A Practitioner’s Guide to Applying Behavioural Finance”; “Value Investing: Tools and Techniques for Intelligent Investment”; and “The Little Book of Behavioural Investing.” Mr. Montier is a visiting fellow at the University of Durham and a fellow of the Royal Society of Arts. He holds a B.A. in Economics from Portsmouth University and an M.Sc. in Economics from Warwick University.

Disclaimer: The views expressed are the views of James Montier through the period ending February 2018, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Copyright

© 2018 by GMO LLC. All rights reserved.

1 James Montier, “A CAPE Crusader: A Defense Against the Dark Arts,” February 2014. This GMO white paper is available at www.gmo.com with registration.

2 Matt Kadnar and James Montier, “The S&P 500: Just Say No,” July, 2017; and Rick Friedman and Anna Chetoukhina, “FAANG SCHMAANG: Don’t Blame the Over-valuation of the S&P Solely on Information Technology,” September 2017. Both GMO papers are available at www.gmo.com with registration.

3 Indeed, correcting for these “issues” reveals an almost identical picture to the simple measure shown in Exhibit 1.

4 James Montier, “Behavioural Investing: A Practitioner’s Guide to Applying Behavioural Finance,” Chapter 40, October 1997, Wiley.

5 Andrade, Odean, Lin (2014) Bubbling With Excitement: An experiment available from www.ssrn.com.

© GMO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All