Should investors worry about the recent rise in US Treasury yields? If they’re high-frequency bond traders—maybe. But for income-oriented investors with a longer investment horizon, our advice is simple: relax.

The 10-year US Treasury yield rose 0.3% in January and hit a four-year high in early February after strong employment and wage data fed concern about inflation. But here’s the good news: rising rates don’t mean disaster for bond portfolios.

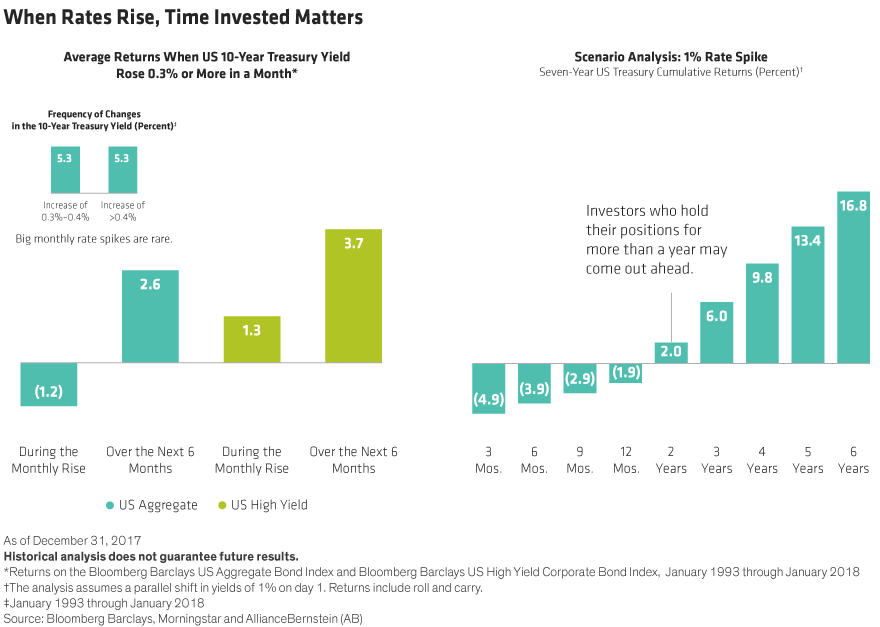

First, it’s important to note that yield spikes of this magnitude don’t happen often—just 11% of the time over the last 25 years. Second, when they do happen, history shows that the longer you hold your bonds, the better you’re likely to do. Since 1993, the Bloomberg Barclays US Aggregate Index, dominated by government and investment-grade corporate bonds, fell 1.2% on average during months when yields increased by at least 0.3%. But it rose 2.6% over the next six months.

US high yield didn’t decline at all, returning 1.3% and 3.7%, respectively.

Would bonds hold up just as well in a bigger sell-off? To find out, we ran an analysis that assumed a sudden 1% rise in yields across the US curve. The results suggested that investors who take the long view can rest easy. A year after the 1% spike, the seven-year US Treasury, whose duration is similar to the US Aggregate’s, would be down almost 2%. But over time, higher yields lead to higher returns. Our analysis suggested that investors who sat tight for three years and reinvested their coupons could have earned a cumulative return of 6%. Six years later, the return in our analysis was nearly 17%.

With bonds, time heals most wounds.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio-management teams.