It’s a country picker’s market. The most synchronized global economy in a decade comes with an unusual counterpart: the most un-synchronized global equity markets in over a decade. Country differentiation will become increasingly important as a mix of country-level risks and macro themes play out. Beneath the rosy global economic surface lies a shifting and nuanced global growth mix. Adopting a country-level focus may help investors better exploit shifting growth dynamics.

We highlight four macro themes to watch:

-

EM early innings: For higher exposure to global growth, look for countries benefiting from robust global trade, such as Japan, Taiwan, Korea, and China, as well as those with improving domestic economies such as Brazil, India, and Indonesia.

-

Growth spillovers: Growth is synchronized, but output gaps are not. Strong DM growth is likely to spillover to trading partners. With the United States and Europe driving growth and China slowing, we favor non-commodity EM exporters, DM countries tied to global CAPEX cycles, while remaining cautious on capital dependent countries, such as Turkey, in case DM economies heat up faster than expected.

-

China’s rebalance: For relative value investors, China’s shifting growth mix – away from the “old” commodity-intensive industries and towards the “new” tech and consumer focused industries – will be heavily felt along commodity vs. non-commodity lines. Investors may consider countries better positioned for China’s new economy, such as northern EM Asia countries and avoiding commodity exporters.

Figure 1: It’s a country picker’s market

Average inter-country correlation

EM early innings

Despite synchronized economic growth, there are meaningfully differences across countries. Developed markets (DM), led by the U.S., are at or near full capacity while most of the emerging markets (EM) excluding China have negative output gaps. The difference in output gaps suggest EM countries can sustain the current above-trend growth for longer than DM. DM growth remains the global driver at the moment, however. U.S. fiscal policy could provide an additional boost, as well as a rebound in the U.S. and European CAPEX cycles and rising import demand. Investors may consider countries, such as Japan and EM Asia, levered to world trade as well as countries with improving domestic economies and accelerating GDP growth, such as Brazil, India, and Indonesia.

Figure 2 illustrates exactly how sensitive companies in different regions and countries are to global economic growth. The higher number indicates that earnings growth in those countries in regions are more sensitive – they have a higher “beta” in other words – to economic growth. U.S. companies tend to be less impacted by global growth than companies in Japan, emerging markets and Europe.

Figure 2: Corporate earnings growth sensitivity to economic growth

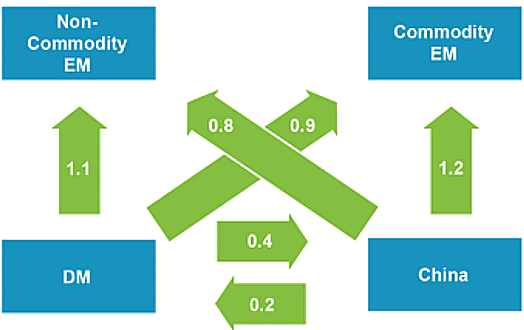

DM output gaps suggest DM countries may risk overheating in coming years at current economic growth rates, yet DM growth spillovers to trading partners could ease domestic inflationary pressures and further underpin the global expansion. Investors may consider European countries with strong growth positions, export-oriented EMs to capture growth spillover, including EM Asia and EM Europe, while being cautious on capital dependent countries, such as Turkey, in case DM economies overheat.

Figure 3: Global spillovers

Impact of hypothetical 1% rise in economic growth over two years

Commodities and China’s rebalance

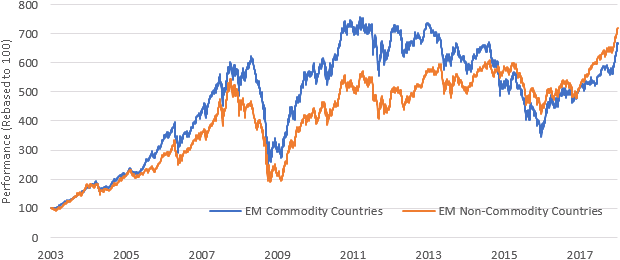

EM assets have rallied over the past year on the back of strong earnings growth and synchronized, above-trend global growth. However, unlike the 2003-2007 bull market, when the global economy was again in sync and EM assets were outperforming DM assets, today’s growth drivers are dramatically different. China’s insatiable commodity demand from the mid 2000s has rapidly declined as China’s growth continues to slow while also pivoting away from commodity-intensive industries and towards tech and consumer focused areas. Despite these secular challenges, robust global growth and tighter oil inventories have provided a lift to commodity prices. However EM commodity countries have failed to rally alongside higher commodity prices.

One explanation: the market believes price increases are temporary. Oil, for example, has seen a 50% rally in the spot prices since June 2017, however longer-dated futures prices are unchanged and remain well below historic levels.1 In contrast to EM commodity countries, EM non-commodity countries are largely driven by advances in technology, such as Korea, Taiwan, and China itself, and by domestic growth stories, such as India and Indonesia.

Figure 4: The new EM: Tech, not commodities

USD returns

Where's my upside?

Commodity prices vs. EM "commodity" alpha

The “reformer” countries offer a set of largely idiosyncratic risk/reward opportunities, where local reform agendas are improving economic and corporate fundamentals. Importantly, each country is working on reforms specifically designed to alleviate bottlenecks in their economies. These reforms have not just the potential for long-term rewards, including better growth, higher profitability, and stronger institutions, but as China’s supply side capacity cuts have shown these reforms may also yield tangible results in the short-run as well.

Summary

The decline in intercountry correlations has made today’s market a “country picker’s market.” Beneath the synchronized global expansion are a number of shifting growth dynamics. With a country-level focus, investors can consider dialing up their EM or DM growth exposure, leverage relative value macro themes, and gain targeted access to idiosyncratic reform stories.

© iShares

Read more commentaries by iShares