It is often said that time in the market is more important than timing the market. Uncertainty always exists, and now more than ever – as a recent example, the market began last year in a month-long freefall, before reversing itself by the end of the first quarter. Add in a heaping of political risk and a president whose tweets can impact not just individual stock prices but entire sectors, and we have a recipe for more, not less, volatility.

Timing the market only works if you have a crystal ball, yet even in today’s environment many investors continue to believe they’ll be able to anticipate the next broad market move. This conviction is the cousin of the emotional behavior that reliably causes investors to, in fact, buy high and sell low. As described in an April client letter by famed hedge fund manager Seth Klarman, "When share prices are low, as they were in the fall of 2008 into early 2009, actual risk is usually quite muted while perception of risk is very high. By contrast, when securities prices are high, as they are today, the perception of risk is muted, but the risks to investors are quite elevated."

The cost of trend-following, reactive behavior has been estimated to be as high as 4% according to a recent Russell Investments report. The key driver of this “behavioral cost” profile is emotion selling, the tendency of investors to move large amounts of money out of stocks at just the wrong time. Fear is an even stronger motivator than greed - investors generally feel the pain of financial loss much more than any investment gain, and run greater risks to avoid loss than to make a profit. With the days of quarterly hard copy statements long gone, investors can now act on these powerful emotions minute by minute, potentially amplifying losses in a perverse twist on enhanced transparency and technology.

Investors who bought and held an S&P 500 fund in the middle of 1996 made a healthy 8% annually over the next decade, notwithstanding the dramatic bursting of the tech bubble which saw the S&P sink 49% from its high in March 2000 through the bottom in October 2002. Fundamentally, an advisor’s job is to construct diversified, all weather portfolios and then provide the reassurance that helps investors exercise this kind of discipline.

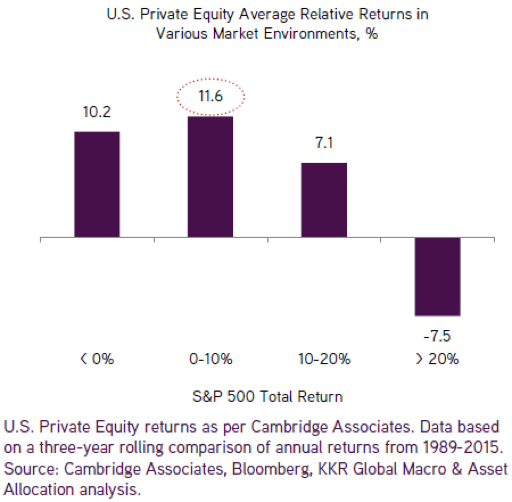

Particularly on the backdrop of today’s markets, private investments can make a meaningful contribution to a balanced portfolio simply by mitigating volatility. Volatility does exist in private markets, but valuations are reported quarterly, not daily, and are based on underlying company performance rather than external factors like investor whims and the emotion of election season. This lower reporting frequency, which has the effect of dampening overall portfolio volatility, can help keep clients from panicking, especially if they are seeing large swings in other parts of the portfolio. It is worth noting that with both stocks and bonds historically expensive, the next downturn could see both asset classes fall simultaneously. In this context, investments that are not going to scare clients with wild swings, that effectively prevent them from selling assets into falling markets, and that are positioned to potentially outperform during periods of public market underperformance become especially valuable.