While investors are justifiably focused on what may be the opening crescendo of a long overdue sell-off in stocks, there is not, as of yet, as feverish a discussion of the parallel sell-offs in bonds and the U.S. dollar, which have been underway for at least a year and a half in bonds and 14 months for the dollar. I contend that this should be widely understood as the root causes of the jittery Dow, and are ultimately far more important. A continued decline in the dollar and bonds holds the potential to ignite inflation while increasing mortgage rates, borrowing costs, and federal deficits. These developments would strike at the very heart of the economic foundation that has supported the country since the Financial Crisis of 2008, and threaten to push the economy into a recession that the Fed may be powerless to confront.

Secretary of the Treasury, Steve Mnuchin, stunned markets late last month when he said that a cheaper dollar would be a welcome development for the U.S. economy. The dollar sold off sharply as Mnuchin's words appeared to be taken as proof that the Trump Administration overtly embraced a weaker dollar. To quell the uproar, President Trump himself, freshly arrived in Davos, Switzerland, had to "clarify" the Secretary's comments, explaining, as only 'the Donald' can, that by "weaker" Mnuchin really meant "stronger."

The exchange did provide a fresh twist on our decades-old "strong dollar policy," which traditionally works like this: The President and/or senior Fed officials refer all questions about the health and trajectory of the U.S. dollar to the Secretary of the Treasury, who proclaims loudly and clearly, with no trace of irony, that "a strong dollar is in the national interest." These comments reassure the markets, the dollar rises, and the operation is complete. Although this protocol is one of the simplest Washington has to offer, the Trump Administration managed to get it wrong on its first try.

Despite the fact that Trump's vocal support for a "strong dollar" was not accompanied by any indication that he would actually do anything to support it, his words temporarily reversed the dollar's 24-hour skid. But apart from reacquainting us to the absurdity of a "policy" that is simply based on mouthing a canned phrase, the episode raises a couple of key issues. Trump claimed that the economy is surging and, as a result, the dollar will keep getting stronger and stronger. The problem with these assertions is that neither is true.

Last week's newly released Q4 GDP report from the Bureau of Economic Analysis (BEA) shows that the economy grew at 2.6% in the Fourth Quarter, bringing the entire year's GDP growth rate to 2.4%, only .2% higher than the 2.2% GDP growth that we have averaged over the prior three years (2014-2016). And while 2.4% is marginally higher than the average growth we have had since the end of the 2008 financial crisis, it is still significantly below the average over the past century, and even weaker than two years of Obama's second term.

The news is also surprisingly weak on the trade and employment fronts, another two areas for which Trump has shown particular enthusiasm. Contrary to the supposed "record job creation," average monthly job gains in 2017 were 17% slower than the combined averages in 2015 and 2016, based on data from the Bureau of Labor Statistics. In fact, job growth in 2017 was its slowest pace since 2010. Similar disappointments can be found in America's trade balance, which, according to Trump, has improved dramatically due to his "tough" negotiations and our resurgent manufacturing sector. But according to the U.S. Census Bureau, average monthly 2017 trade deficits (through November) were 11% wider than 2016, and 14% wider than the average over the prior 4 years. What's worse is that these increases come at a time when a falling dollar, in theory, should have narrowed the gap!

Given all this, one would be hard-pressed to find the "boom" Trump describes, especially if one is also claiming that such windfalls were not occurring under Obama. But since when have facts ever mattered in Washington or on Wall Street?

So if Trump is wrong about the economy, jobs, and trade, what should we make of his view that "the dollar will get stronger and stronger?"

While the financial media has been focused on the stock market, most have dismissed the significance of the declining dollar. 2017 saw the first annual; decline in the dollar in five years and its largest decline in 14 years. 2018 is off to an even worse start, with the dollar registering its steepest January decline since 1987. In fact, against the Chinese yuan, January was the weakest month for the dollar since 1994. The current decline in the dollar index that began in December 2016 is now the longest continuous decline in the last 12 years. And while other recent declines have been steeper (see chart below), this one is distinct because it is occurring against a set of economic conditions that should be bullish for the dollar. Economic growth is assumed to be strong, consumer confidence is high, and the Fed is expected to keep raising interest rates and actually shrink its balance sheet (which would diminish the supply of dollars).

Data from Yahoo Finance, BEA, & Bloomberg

Created by Euro Pacific Capital

So if the dollar is falling now, with everything supposedly going in its favor, what should we assume will happen if the dollar's luck runs out? A recession, which typically brings with it a decline in GDP and consumer confidence, and which may cause the Fed to reverse policy, may likely knock out the remaining supports for the dollar and result in deep declines. But given the nearly universal optimism that prevails in financial and political centers, it's unlikely that these concerns are widely shared.

Over the past century, the U.S. economy has experienced a recession, on average, every six and a half years. Despite the fact that more than a decade has passed since our last recession began, few forecasters see another one looming. But interest rates are currently creeping up further and faster than nearly anyone had predicted. At 2.85%, the yield on the 10-year Treasury is currently at its highest level in nearly 4 years. Except for a few days in December 2013, yields haven't been higher than 3% since mid-2011. It's very possible that rates on the 10-Year Treasury will relatively soon break through 3%, perhaps lifting mortgage rates and bank loan rates into territory that we haven't seen for well over a decade.

But it's absurd to expect that yields won't go considerably higher than 3%, especially given how the supply of Treasury bonds coming to market will balloon in coming years. As reported last week by the Wall Street Journal, the Treasury Borrowing Advisory Committee - a group of private banks that advises the Treasury - estimated that $955 billion of Treasury debt will come to the market this year (up from $519 billion last year), and that the issuance will surpass $1 trillion in fiscal 2019 and 2020. The Journal reports that the Committee ramped up its estimates due to the recently passed tax cuts. So the issuance of Treasuries may spike just as demand for them may wane due to a possible slowing economy and a falling dollar. Just today, the Associated Press reports that a potential budget deal being discussed in Congress would grant both parties their respective spending priorities, resulting in a $1 trillion deficit as soon as next year. Recall that the only other times that we ran deficits that large were the years 2009-2012, a period in which the Federal Reserve was buying nearly half a trillion per year of Treasury debt through its Quantitative Easing program. But now the Fed has promised to effectively sell bonds to shrink its balance sheet, in a process that could be called "Quantitative Tightening." This is a recipe for an enormous decline in the bond market, which could send yields much higher.

Does anyone really expect that our current economy could absorb rates on the 10-year that might hit 4% or higher without slowing? Perhaps they are just too numbed by success to care at this point. In fact, if rates rise above 4%, what is there to prevent them from surging much higher? It's ironic that as stock market investors ignore the collapse in bond prices, the one thing that might prevent a bond market crash would be for the stock market to crash first, thereby forcing the Fed's hand. Yet the markets seem unconcerned.

Since the Federal Reserve and the U.S. Government began intervening in the markets in the wake of the 2008 financial crisis, there has been almost no downside volatility in stocks. With the exception of a trivial 8% decline in the opening two weeks of 2016, the nearly 300% rally in the Dow since March of 2009 has been achieved with hardly a step backwards. The 10% and 20% corrections that were fairly commonplace throughout much of the 20th Century, now seem to be relics of the past. In fact, despite the recent breakneck speed of ascent (40% gain in just 15 months) and the record level valuations (stocks trading around 27 times trailing earnings), the volatility index, which is commonly viewed as a measure of investor fear, is remarkably, almost historically, low.

It does seem that fear and worry have been thoroughly banished from Wall Street.

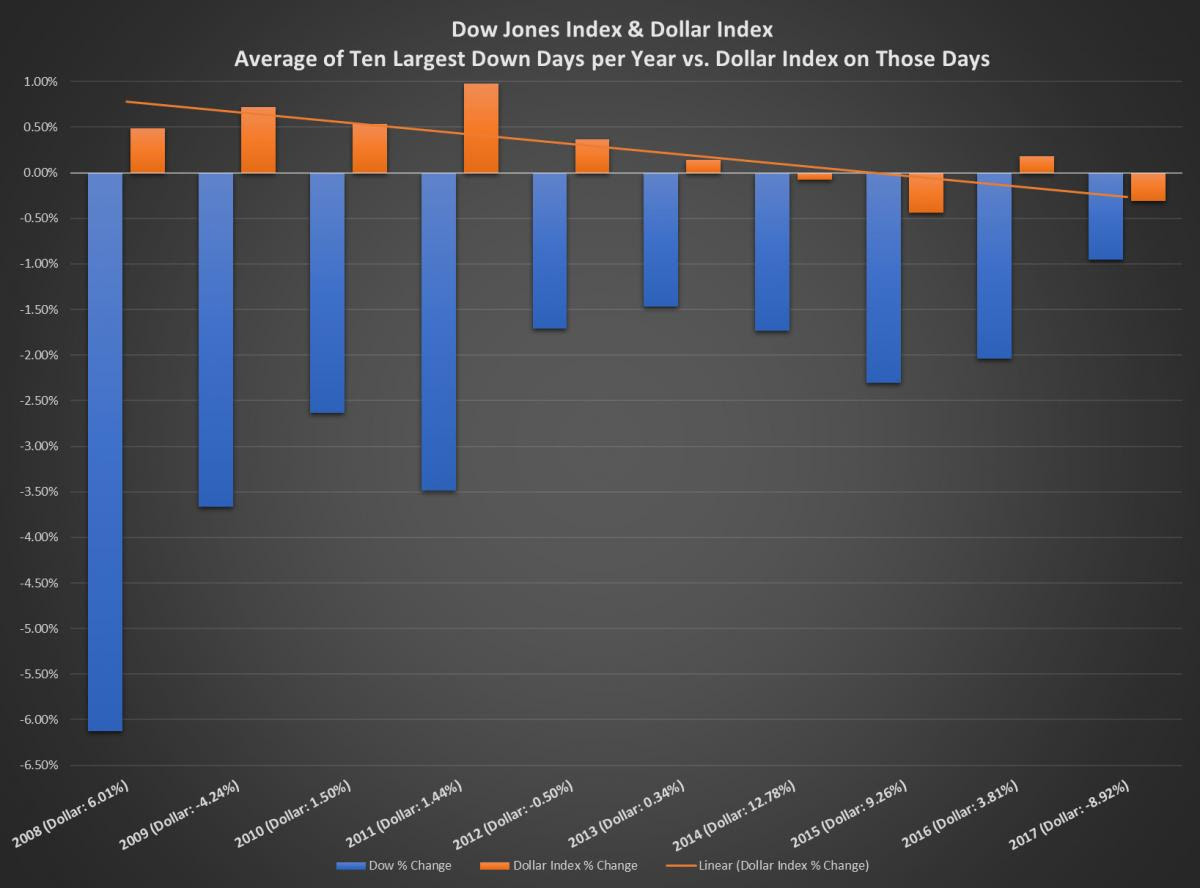

But the dollar itself may be a window into the troubled souls of otherwise carefree investors. Even in the market surge of the past decade, there have been some isolated moments when daily declines are significant. By looking at what "safe haven" choices investors make on the market's worst days, we can potentially see what may happen if the market experiences sustained selling.

If we look at the average of 10 worst market days each year during the five years from 2008 to 2012, 50 days when the Dow dropped by at least 100 points, we can see that the dollar tended to rally in the panic. During those days, the dollar index rallied 80% of the time, and on average rose .6% on the day. This seems to reflect that the dollar maintained its "safe haven" status. But, in more recent years, that has changed considerably. Averaging the 10 worst market days of each year in the market from 2013 to 2017, the dollar fell on those 50 days by approximately .3%, and it only rose 26% of the time.

Data from Yahoo Finance, BEA, & Bloomberg

Created by Euro Pacific Capital

Past performance is not indicative of future results

This shift in sentiment could be extremely significant in the years ahead. This is why a simultaneous collapse in bond prices and the dollar could be so significant. It could show that rising interest rates do not reflect improved growth, as so many stock market bulls conveniently claim, but a loss of confidence in the dollar and the creditworthiness of the United States.

The onset of both of our previous recessions (2000 and 2008) inspired the Fed to cut interest rates by at least 500 basis points. Currently the Fed Funds rate is still under 1.5%. If a recession comes, 150 basis points in cuts before the rate hits zero may not be nearly enough to provide the stimulus that the markets have come to expect. That may mean that the next recession might almost assuredly bring with it another round of quantitative easing from the Fed. But the Fed has already prepared the currency markets for its balance sheet to shrink. Imagine the reaction when the opposite occurs.

A recession that brings on another dose of QE could help to create the perfect conditions to help push the dollar to record lows, continuing its long-term bear market that began in the early 1970s. The low for the dollar Index in 2008, just before the dollar was saved by the financial crisis, was just above 70. It is currently just above 89, having traded above 104 as recently as January of 2017. My guess is the next leg down could take the dollar index to 60. To support the currency, the Fed would have to follow the example of Paul Volcker, who hiked interest rates in the 1980s when the dollar was collapsing. Of course, such moves to prop up the dollar during a recession will be acutely unpopular and may bring on a recession worse than the one seen in 2008. If the Fed lacks the courage to administer such medicine, a dollar index at the 40 level might not be ruled out.

All this adds up to a possibly rough road for investors who maintain 100% exposure to the U.S. dollar.

Read the original article at Euro Pacific Capital

Best Selling author Peter Schiff is the CEO and Chief Global Strategist of Euro Pacific Capital. His podcasts are available on The Peter Schiff Channel on Youtube.

© Euro Pacific Capital

© Euro Pacific Capital

Read more commentaries by Euro Pacific Capital