Key points

- The U.S. Treasury yield curve, which flattened for much of 2017, when spreads between long and short maturities recently narrowed to decade lows, has begun to steepen.

- Investors historically have viewed the shape of the yield curve as a signal of future growth. We believe the yield curve is currently suggesting continued economic expansion.

- The ETF Investment Strategy team documents the historical relationship of equities to different yield curve regimes over the last 20 years.

- Against the current backdrop of sustained global expansion, our preferred sectors include cyclicals, specifically financials and technology.

The yield curve: An explanation

The yield curve compares interest rates at different maturities, typically the spread between yields on two- and 10-year bonds. Ten-year yields historically have reflected the market’s growth and inflation outlook, while the short end of the curve is mainly tied to market expectations for Federal Reserve policy rates.

The yield curve flattened for much of 2017, primarily due to a rise in short-term yields. While a flattening yield curve can signal slower growth, rising short-term yields in 2017 showed greater market confidence in the growth and inflation outlook, which also carries expectations the Federal Reserve will continue to normalize policy rates. It would be worrying if the curve had flattened because 10-year yields were falling on concerns that Fed policy tightening might crunch growth and inflation. Instead, low inflation expectations kept rises in 10-year yields in check, while declines in yields on even longer maturities largely reflect strong foreign buying and demand from institutions seeking to hedge risk.

However, in early 2018, the strengthening global economy and U.S. fiscal stimulus are expected to be heralding a turnaround in market sentiment with rise in inflation expectations, reflected in rising long-term bond yields. The yield curve has steepened somewhat in 2018, although we don’t expect long-term yields to rise sharply this year.

What the yield curve can tell us

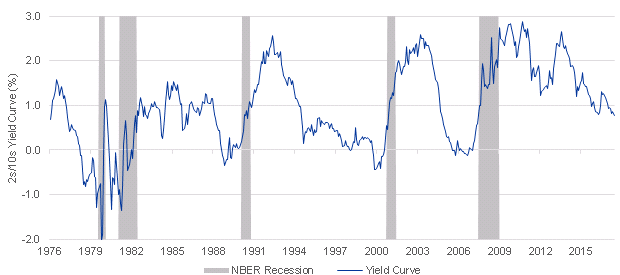

Investors have historically viewed the shape of the yield curve as a signal of future economic growth. It is typically the steepest after recessions, as the Federal Reserve lowers the federal funds rate to stimulate economic activity, and flattens over the course of the business cycle as the Federal Reserve raises the federal funds rate to contain inflation, lifting short-term rates in the process. If a recession looms, the yield curve typically becomes “inverted,” when two-year yields are higher than 10-year yields. In the post WWII era, the yield curve has inverted before every recession.

Figure 1: Yield Curve & Recession

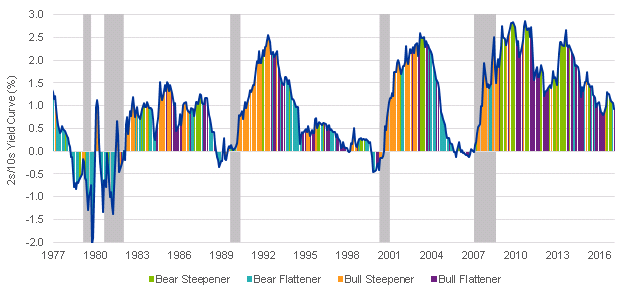

The shape of the yield curve depends on a multitude of factors; for example, it could flatten due to falling long-term yields and/or through rising short-term yields. We believe investors may benefit from a full understanding of both the level of yields and the slope of the yield curve. In general, then, we can decompose the yield curve into four basic regimes:

- Bear steepening – interest rates rising, yield curve steeper

- Bear flattening – interest rates rising, yield curve flat

- Bull steepening – interest rates falling, yield curve steeper

- Bull flattening – interest rates falling, yield curve flat

The chart below illustrates when those four regimes prevailed as the yield curve changed over the last 40 years:

Yield Curve Regimes:

The yield curve and equities

As noted, the yield curve has historically been an effective real-time business cycle indicator. However, we find that incorporating the changing level of interest rates into an analysis of the yield curve yields important insights beyond what just the slope of the yield curve can tell us.

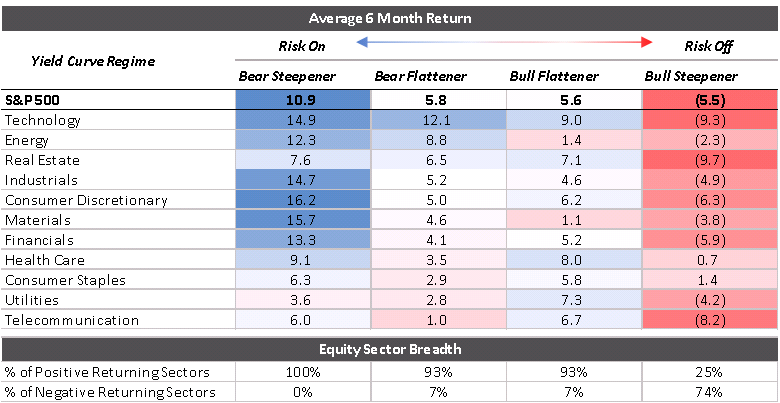

Over the course of the business cycle, equity market leadership often rotates amid changing economic fundamentals. We document the historical relationship over the last 20 years as it relates to the changing level of interest rates and the yield curve shape. Unsurprisingly, there is a significant dispersion across regimes for both the broad market and relative sector returns.

Distribution Across Yield Curve Regimes

As the table shows, equities have performed best during the Bear Steepener regime. It is the best “risk-on” environment, typically capturing increasing bullish sentiment via rising interest rates and stronger conviction around the growth and inflation outlook as long-term rates rise by more than short-term rates.

Meanwhile, the Bull Steepener is the worst risk-on regime. This regime largely reflects the Federal Reserve easing monetary policy in response to a recession. However, our research shows that 25% of the S&P 500 subsectors showed positive six-month average returns during these periods, highlighting the defensive nature of select sectors and the importance of sector rotation over the course of the business cycle.

It is also worth noting that the spread between the steepener regimes is far greater than the spread between the flattener regimes. In other words, broad equity returns are relatively robust to both bull and bear flattening regimes, however there are relative value opportunities at the sector level between bull and bear flattening regimes.

In other words, yield curve regimes matter for overall market returns, or beta, but they also affect relative sector returns.

The market return (S&P 500) has had its best returns in bear steepening periods, which occur in reflationary regimes and are often found early in the business cycle when the economy emerges from recession. In risk on regimes, like the current market environment, cyclical sectors (i.e. consumer discretionary, financials, industrials) historically have performed the best. In risk off regimes, defensive sectors historically have performed the best, e.g., consumer staples, health care.

Conclusion

The yield curve is a valuable real-time business cycle indicator, but it can be improved by incorporating the changing level of interest rates into the analysis. By doing so, investors may be able to identify sectors and sub-sectors that are most likely to outperform the broader market.

We believe the current yield curve is indicating ongoing sustained global economic expansion. Our sector preferences in this environment focus on cyclical sectors, namely technology and financials. Technology appears most insulated from changing yield curve shifts, most likely attributable to their lower reliance on debt financing and secular growth profile. The sector is supported by strong earnings and increasing profitability. As for financials, we believe the sector can benefit from U.S. deregulation, and yield curve steepening could boost lending margins.

© 2018 BlackRock, Inc. All rights reserved.

Read more commentaries by iShares