Key Points

-

Earnings-driven (and also FOMO-driven) market is breaking records and raising questions.

-

Smart money getting more optimistic.

-

Inflation and tighter monetary policy could be triggers for a bumpier road this year.

U.S. equities have pitched to new all-time highs on the back of a near-commensurate surge in earnings. Fourth quarter earnings per share for the S&P 500 are on track to be up 12% for both last year’s fourth quarter and the full calendar year of 2017. But the real story is about expectations for 2018 earnings. Just over the past three weeks, expectations jumped from 12% to 16% growth for the full year, nearly all due to tax reform.

I don’t want to throw cold water on the improvement to earnings, but do want to note that investors should be careful about wishing for even higher earnings from here. The stock market is a discounting mechanism and as you can see in the table below, the highest zone for year-over-year earnings growth has historically been met with middling market gains. It highlights that once the earnings expectations bar gets set at the highest level, the likelihood of disappointment rises as well.

Source: Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2018 © Ned Davis Research, Inc. All rights reserved.)

The force of the move this year is notable. It’s shaping up to be not just an earnings-led surge, but also a FOMO-driven market. For the less-text lingo savvy among us, that stands for “fear of missing out.” Stocks have been gapping up in the morning nearly every day. During the past 30 trading sessions, more than 85% of them have seen the S&P 500 futures open higher than the prior close. According to SentimenTrader (ST), that is—by far—the most since futures began trading in 1982. In other words, “there has never been a time when traders were so eager to buy stocks that the futures were up almost every single day over such a long time period.”

Big gaps

ST looked at the handful of times historically when stocks were trading at a high and at least 70% of the days gapped up at the open. Like they’ve seen with other recent studies, the momentum often continued a bit in the short-term, but most of the time, those gains were erased during a subsequent pullback (including the only two precedents during the current bull market). Most of the risk over the following year was confined to the first two months, while most of the reward occurred thereafter.

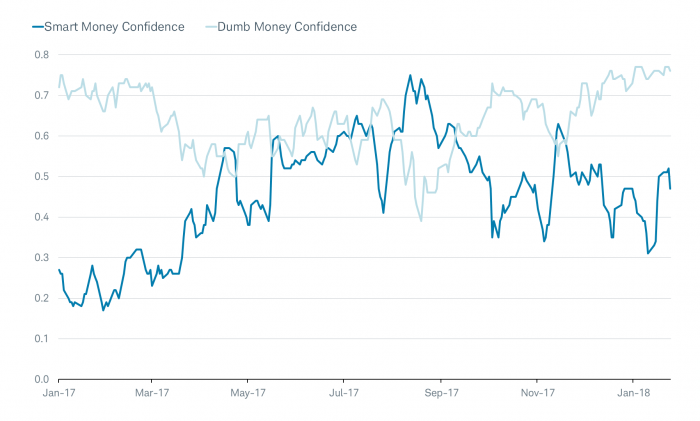

Let me stay with ST data for a moment and highlight their so-called “Smart Money and Dumb Money Confidence” readings. As a refresher, these measures are behavioral in nature as ST is tracking what these cohorts are actually doing with their money (i.e., they are not attitudinal measures of sentiment). Smart money indicators include the OEX put/call and open interest ratios, commercial hedger positions in the equity index futures, and the current relationship between stocks and bonds. Dumb money indicators include the equity-only put/call ratio, the flow into and out of the (bull and bear) Rydex series of index mutual funds, and small speculators in equity index futures contracts.

Smart money getting more bullish

As you can see in the chart below, we recently began seeing a narrowing of the spread between the two confidence measures—but in a manner that is atypical. Smart money confidence (SMC)—typically the non-contrarian indicator—has been catching up to dumb money confidence (DMC), without the latter retreating. There were only three times in the history of this data that SMC jumped 20% or more while DMC was above 70%: early-January 2007, late-April 2010 and mid-January 2014. In each case, the market suffered a pullback shortly thereafter.

Smart money confidence catching up as spread narrows

Source: SentimenTrader, as of January 26, 2018.

This is interesting because it’s in keeping with some notable quotables lately from a few icons in the world of investing:

Warren Buffett, Berkshire Hathaway CEO:

“The game of economic miracles is in its early innings. The world is getting better.”

Ray Dalio, Bridgewater Founder:

“A market surge is ahead. If you’re holding cash, you’re going to feel pretty stupid.”

Jamie Dimon, JP Morgan CEO:

“It’s possible to hit 4% growth this year and 3% long term.”

Lloyd Blankfein, Goldman Sachs CEO:

“Animal spirits are more vital, and I think a 3% economy is doable.”

Jeremy Grantham, GMO Founder

“I recognize that we are currently showing signs of entering the melt-up phase of the bull market.”

Melt-up indeed

In early December, I wrote about the anatomy of a melt-up in the stock market and it appears we entered that state this year. If you annualize the year-to-date price-only return of the S&P 500 of 7.5%, you get a 155% annualized return. Clearly this is not a realistic pace (unless your year-end target for the S&P is 6800); but what is less clear is what stops the bull’s charge.

We take comfort in the fact that the latest surge has been earnings-driven, and not a function of pure valuation expansion. We take comfort in the likely acceleration of economic growth, aided by a strong pick-up in business capital spending (capex). We take comfort in the fact that although attitudinal measures of investor sentiment show excessive optimism, behavioral measures like fund flows only recently show heightened enthusiasm for U.S. stocks. We take comfort in the fact that the market’s technical strength and breadth indicators remain supportive. And we take comfort in the fact that inflation—often a valuation “killer”—remains low. But on that note, here’s where we find reasons for investors to be on guard.

Inflation/tighter monetary policy coming

Inflation has already accelerated, although core measures are not yet breaching the Fed’s 2% target. But headline measures have been pushed up courtesy of higher oil prices, while the U.S. dollar’s weakness is also inflationary as it raises import prices. And the tight labor market should begin to put more sustained upward pressure on wage growth.

[As an aside, I’ve gotten a lot of questions lately about the dozens of companies that have announced special bonuses in the wake of the tax bill passing; and what it means for coming wage data. As most of the announcements have been for bonuses and not wages, they do not show up in average hourly earnings (AHE), nor likely in median measures like the Atlanta Fed’s Wage Tracker. To date, they also don’t add up to a lot in relative terms. So far $2-3 billion in special bonuses have been announced; but that’s in the context of about $8.5 trillion of total wage and salary income (which includes bonuses) in U.S. personal income.]

Inflation to bite?

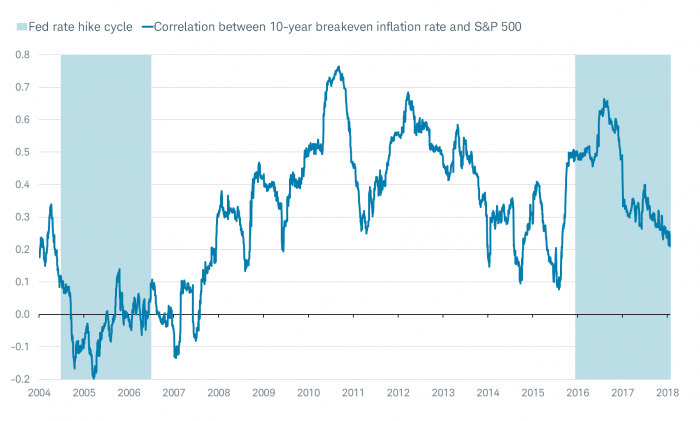

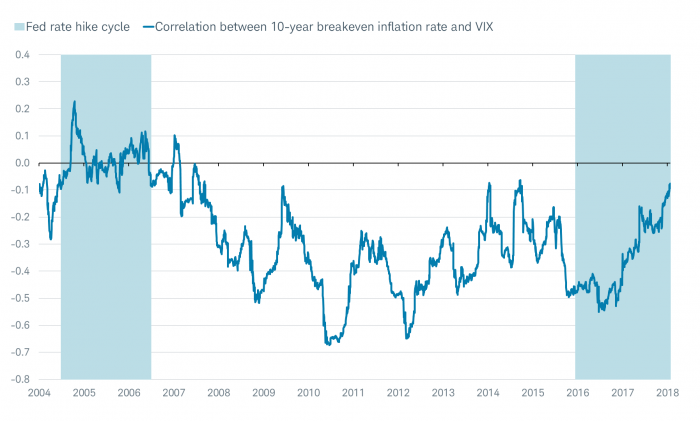

Since the financial crisis, the correlation between inflation and stocks has been positive. It’s in keeping with what has generally been a positive correlation between the 10-year Treasury yield and stocks. This is typical of a deflationary bust (which is what the global financial crisis represented) and the subsequent recovery period. But the Fed is likely to raise rates more aggressively this year; we’ve moved from quantitative easing (QE) to quantitative tightening (QT) with the reduction of the Fed’s balance sheet; the labor market has become quite tight; and the output gap (the spread between actual growth and potential growth) has turned positive for the first time in this cycle.

As you can see in first chart below, we are seeing a descent in the correlation between stocks and inflation (as measured by the 10-year breakeven inflation rate)—typically in a rate hike cycle, the two are inversely correlated, as was the case from 2004 to 2006. And as you can see in the second chart below, we are seeing an ascent in the correlation between volatility (as measured by the VIX) and inflation—typically in a rate hike cycle, the two are positively correlated, as was the case from 2004 to 2006.

Descending correlation between inflation and stocks

Source: Bianco Research LLC, Bloomberg, as of January 26, 2018. Chart plots rolling 130-day correlation between U.S. 10-year TIPS breakeven and S&P 500.

Ascending correlation between inflation and volatility

Source: Bianco Research LLC, Bloomberg, as of January 26, 2018. Chart plots rolling 130-day correlation between U.S. 10-year TIPS breakeven and VIX.

Yes, financial conditions remain quite easy—notwithstanding the Fed having been in rate hike mode for more than two years. The St. Louis Fed Financial Stress Index is at an all-time low; while Goldman Sachs’ and the Chicago Fed’s National Financial Conditions indexes are also in or near uncharted territory. But this won’t last in perpetuity, and an eventual tightening of financial conditions could usher in greater market volatility.

Speaking of things that won’t last

Higher inflation and tighter monetary policy represent fundamental reasons to expect that we may have a bit more drama this year—even if it’s in the context of an ongoing bull market (a theory in which I’m a believer). There is also a more simple way to think about this; which is to look at past periods with similar recent performance to see what has unfolded thereafter.

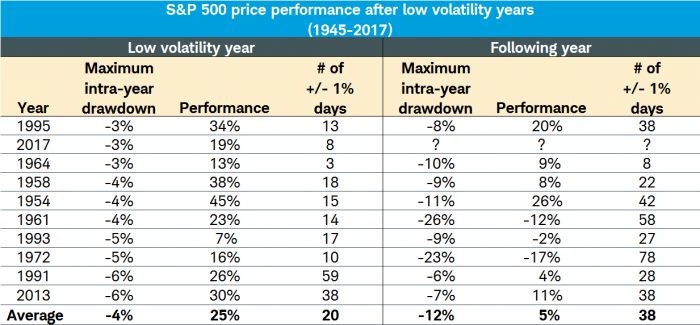

The first table below looks at full year action in stocks. Last year was the second-lowest year of volatility—as measured by maximum intra-year drawdown—since 1945. Only 1995 was a less dramatic year. The right half of the table shows how the market behaved in the subsequent year; with a clear indication of the tendency to suffer larger intra-year drawdowns and a greater frequency of +/- 1% days. The average performance remained in positive territory, but the road to get there had more potholes.

Source: Bloomberg, Strategas Research Partners LLC.

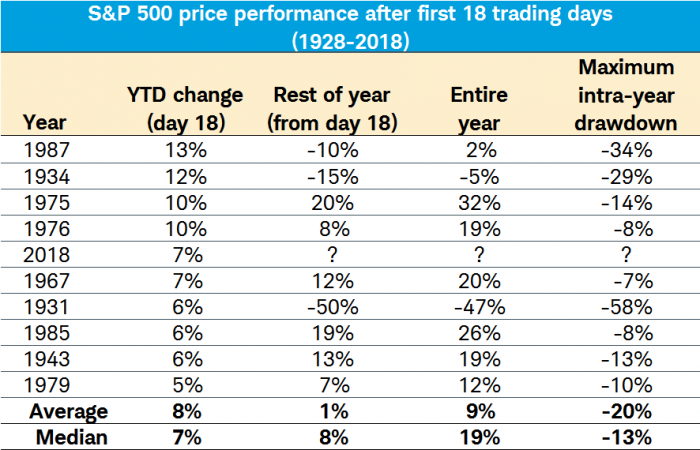

Since 2018 has started in melt-up mode, I thought it would also be instructive to see how similar parabolic starts morphed as the year went on. Looking over the full history of the S&P 500 since 1928, this year ranks in the top-10 in terms of year-to-date change as of the 18th trading day (which was this past Friday). You will see a similar pattern as above, with the rest-of-year and entire year average/median performance still in positive territory; but with a big uptick in maximum intra-year drawdowns.

Source: Bespoke Investment Group, as of January 26, 2018.

Indeed, volatility has begun to pick up. We’ve witnessed a few key reversal days so far this year—with strong opens giving way to weaker closes. And although stocks are trading near all-time highs, from its low on the first trading day of 2018, the VIX is up over 30% (albeit to a still-low absolute level).

There are things investors can do to navigate what could be a choppier year. We continue to recommend investors stay at their long-term strategic allocation to U.S. stocks; but with the surge, there will be more opportunities to rebalance back to that strategic weight. We remain biased toward large capitalization stocks, but also believe investors should have a “value” mindset (that doesn’t mean blindly buying stocks in the value indexes; but to be conscientious of not overpaying for stocks in terms of valuations). In addition, correlations have plunged both across, and within, asset classes, which means diversification reaps more rewards than has been the case for much of this bull market. In a word: discipline.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

©2018 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

Read more commentaries by Charles Schwab