We are at an interesting point in this economic and capital market adventure we have been through for almost ten years. We hesitate to use the word “cycle” because that implies that economic activity, measured by the output of our country, and in turn the capital markets, would actually turn down. It really is more of an economic experiment, one in which the central banks of the major developed countries in unison have poured money into the global capital markets in an attempt to accelerate economic growth after the desolation of the Financial Crisis nearly ten years ago.

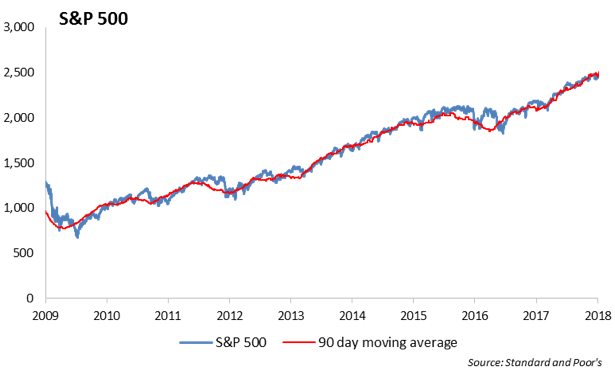

We are at the point where, in the aggregate, the domestic economy is showing real signs of growth. In fact, we are in the midst of a global economic upswing as Japan, Europe and other parts of the world experience rising economic output and asset prices. The S&P 500 increased a solid 22% last year including dividends.

Yet, this growth comes at a price. Our debt burden is growing. Here in the United States, the Tax Bill and its impact on both consumer and business spending will likely increase the budget deficit by $1.5 trillion over the next decade. The budget deficits that we have been incurring will likely grow larger over the next two years as tax collections decline in the hopes that increased economic activity picks up the slack. We estimate this may result in an additional $1.7 trillion in U.S. Treasury issuance over the next two years. We expect our government will continue to grow the debt level to fund the budget deficits and support economic growth. We can only hope that investors and central banks continue to line up to buy our bonds.

The monetary stimulus implemented over the past eight years which was used to jump start this economic growth is unparalleled compared to any period in our economic history. Because of our central bank’s shift in monetary initiatives over this period, we believe we entered a new monetary regime. We shifted from a regime where targeting a level of short term interest rates could, at the margin, have an impact on economic growth to a new regime in which the central bank buys trillions of dollars of bonds in the open market onto its balance sheet in an attempt to lower interest rates across the yield curve. As a result, core tenants of economic measurement including measures of risk and volatility, output, and even expected outcomes appear distorted compared to historical norms. This has a profound impact for investors as asset prices and valuations have been pushed higher.

The surge in asset prices is marked by historically low levels of volatility. We are truly stunned at the resilience of the capital markets to negative news. Wars in Syria, Afghanistan, and the Middle East; the growing nuclear threat in North Korea, imminent default on Venezuelan debt, you name it – there has been no negative news on the geopolitical front that has been able to pull our bond and stock markets lower. With volatility at record lows, investors are showing the wild exuberance that is typically associated with late stage equity bull markets. Feeling like they do not want to miss out, investors ignore risk measures and move with full force into equities believing that they, or their advisor, is sharp enough to get out of the market on time. This doesn’t end well. Markets always correct. The problem is made more complicated during our current economic experiment, because the tools our central bank would normally use to mitigate a downturn have been largely used up. This helps to explain the Fed’s push to raise short term interest rates this year, since the Fed believes they will symbolically be needed to be lowered during the next down turn.

We are cautious on the equity market’s accelerated rally. While we do not see any crisis on the horizon, we are concerned that increased asset valuations have been largely supported by higher debt levels. And, while the banking sector looks to be well capitalized, much of the credit risk which would typically land on bank’s balance sheets has been pushed into the capital markets and is being absorbed by investors. At the same time, American’s have accumulated far more debt than they have assets and income to support. With interest rates and risk premium near all-time lows and debt and asset values near record highs, the seeds are being planted for the next downturn.

The Economy

The pace of growth in the domestic economy increased in the second half of 2017 and will continue to accelerate in 2018. We estimate that the economy grew by 2.9% in the fourth quarter measured by growth in domestic output. Economic growth will be helped by the new Tax Bill which will help consumption, corporate spending and broad sectors of the economy including energy and real estate. In addition, the Administration has indicated its next initiative is an infrastructure spending Bill which should provide more fuel for the economy. With the background of continued accommodative monetary policy in 2018, strong fiscal policy and a pro-business political environment, we believe there is momentum for continued appreciation in equity prices. However, the two critical issues to sustained economic growth remain job growth and private credit expansion.

The retail sector showed marked improvement in the fourth quarter aided by strong holiday shopping sales. The energy sector is benefiting from higher oil prices which recently hit $63 per barrel. Both residential and commercial construction remain strong. However, growth in Commercial & Industrial loans was flat over the past year. In addition, we are seeing some weakness in manufacturing, particularly related to the auto industry. Light vehicle sales dropped 5.85% from their high of 18 million this summer. Economic growth has been fueled in a large part by consumer spending. We are concerned about the sustainability of the consumer sector over the next year given the increase in household debt and the reduced savings rate as a percentage of household income.

There is a divergence between the current economic growth environment and monetary policy. As the economy continues its slow grind toward sustained growth nine years after the Financial Crisis, monetary policy has shifted from Quantitative Easing to Quantitative Tightening. In the absence of fiscal stimulus, the current monetary environment is lined up against economic growth over the next year.

Monetary Policy

We are in a new monetary regime that utilizes the Federal Reserve’s balance sheet as a powerful mechanism to adjust the level of interest rates and the price of risk in the market. In turn, this tool was effective in helping lower borrowing costs which further helped companies to refinance their debt and consumers to reduce their borrowing costs. Lower interest rates helped to spur economic growth.

With this new tool kit, we are now moving from Quantitative Easing into an environment of Quantitative Tightening. But, do not be confused, the monetary policies currently implemented by our Federal Reserve can still be characterized as accommodative. Since 2009, the Fed has accumulated over $4.4 trillion of securities onto its balance sheet through open market purchases of U.S. Treasury and Mortgage-Backed Securities. The Fed has announced its intention to reduce its portfolio holdings over time, however, they are still reinvesting some of the cash flow generated from the holdings in the portfolio. While this is a significant step toward normalization, the Fed is still holding assets it purchased after the Financial Crisis from the capital markets on its balance sheet. And, while we expect the Fed to continue to take steps to reduce its holdings, we don’t believe they will be able to totally exit its QE program. The next economic downturn will make it more difficult to jettison its balance sheet holdings. Every global financial crisis spreads through the banking system. The global banks have successfully emerged from a period of bolstering their capital and improving asset quality. Measured by their capital levels, the banks are fundamentally stronger than any time in the past thirty years. This gives us comfort that the next downturn will be somewhat muted.

As economic growth has gained traction, the Federal Reserve has pushed short term interest rates higher by 1.25% over the past 18 months. At the same time, long term interest rates have not increased and have traded in a tight 30 basis point range. The lack of inflation has provided cover for the Federal Reserve to move consistently to increase short term interest rates. With the current economic strength, the Federal Reserve will continue to talk interest rates higher in 2018; however, we don’t believe that they will push short term interest rates higher than long term rates. This flattening in the yield curve will ultimately choke economic growth which is counter to the Federal Reserve’s initiatives over the past ten years. The question is: will long term rates adjust higher? We expect the answer lies somewhere between a continually weak dollar and the lack of alternatives for foreign central banks to allocate their excess reserves.

Over the past five years, the Federal Reserve has been trying to balance policy between stimulating economic growth and at the same time, pushing the rate of inflation higher. We would favor Fed policy which would allow economic growth to increase and persistently low inflation to err on the high side.

Employment

The domestic labor market continues to be a paradox clouded by the overhang of structural problems. Here is the good news: the economy has produced over 2.0 million jobs during each of the past five years as the unemployment rate declined to 4.1%, its lowest level since 2001. Here’s the problem: a large portion of the jobs that are being created are mostly part-time seasonal positions that have lower wages and no benefits. The structural problem in the labor market following the Financial Crisis is described by the growth in the number of part time workers that are limited to 30 hours a week and unable to obtain benefits including health insurance. The result is that the continued growth in household formation, the sale of single family homes and consumption may be muted.

When people feel good about their job, they spend more money. Consumption represents 70% of the domestic output. Thus, job growth is important to domestic economic growth. At the same time, wage increases also contribute to increased consumption. However, as the rate of unemployment has declined, the pace of wage inflation has not accelerated. This is a conundrum for economists. Normally, as excesses resources are put to work during a period of economic expansion, they become increasingly scarce which results in higher wage pressure later in an economic cycle. Yet, since the unemployment rate is calculated as a percent of those actively seeking work, it does not account for the large body of employable workers sitting on the sidelines. In addition, the labor force participation rate, which measures the number of workers relative to the population of the work force, is near a 40 year low. A material improvement in productivity gains has been slow. While we expect to see the labor market continue to tighten and increased pressure on wages in 2018, we do not expect a sustained increase until we see a higher pace of business formation.

Inflation

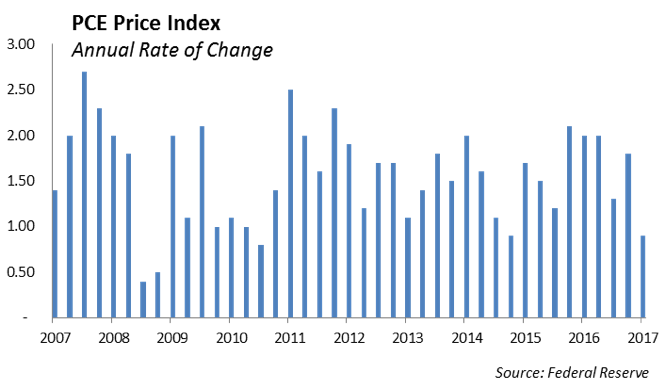

One of the confounding issues for the Federal Reserve is that recorded measures of domestic inflation are not showing a sustained increase approaching their target of 2%. A modest rise in consumer prices in December and strong retail sales has helped to bolster inflation expectations. A small and sustained increase in inflation is important for a growing economy and the lack of inflation has been a concern for economists for the past five years. With the expected increase in near term economic activity, we would expect inflation to increase near 2.2% this coming year.

As central bankers unwind the global stimulus that has helped to produce the rally in asset prices, inflation has been subdued. Near term, we expect that to change. Over the past year, inflation has begun to percolate globally and we are seeing signs across North America, Europe and Japan with increases in producer price indices. With the weakening of the U.S. dollar, domestic imports are no longer suppressing inflation. At the same time, U.S. manufacturers are paying more for raw materials, as reflected in the Institute for Supply Management’s prices-paid index, which is near its highest level in years.

Price increases are gripping industries and we are seeing rising prices in commodities, hospitality, and business services. In addition, we expect to see additional wage pressure over the next year. Typically, a late cycle event, when demand increases for scarce resources in an economic expansion, wages and prices increase. The rate of unemployment is at 4.1%, its lowest level in 17 years. With the labor market tightening and business investment rising, we expect to see near term pressure on wages. In addition, we would expect to see an improvement in the labor force participation rate as more workers re-enter the labor force.

The concern for investors is the expectation that a rise in the rate of inflation will result in a correlated increase in the level of interest rates. While we expect pressure on rising short-term interest rates as the Fed continues to push rates higher, we do not expect an accelerated climb in yields in long-term rates. The U.S. capital markets continue to attract global investors which have helped to suppress the level of interest rates.

The Business Sector is on Solid Footing

The business sector appears to be doing well and prosperity should continue under the Tax Bill with a permanent cut in the corporate tax rate to 21%. As cash is repatriated from overseas banks, we also expect that business investment should increase.

However, business formation remains low. Two reasons are access to capital and heightened business risk. Historically, Small business drives employment growth. However, since the financial crisis, large companies have created more jobs than small companies in the United States. The low pace of business formation is related to the low rate of private credit expansion. It has been difficult for small businesses to obtain a business loan or an increase in credit from traditional lending sources after the financial crisis. Loan growth has been declining over the past three years measured by C&I loans.

The sustained lack of business formation has become more evident in the capital markets as the number of publicly traded companies has declined. While companies have merged and been acquired, the number of new publicly traded companies is significantly smaller and not enough to offset the decline.

So, how does this change? In our view, we will see a tectonic shift in economic activity once bank lending is re-calibrated to the business risk.

Tax Bill Will Provide Near Term Stimulus

Following the financial crisis, our political environment has been toxic and not constructive for business. Upon some reflection over the past few years, we believe that our form of democracy is evolving. The recent election has shined a light on deep divides that exist in our country. The election did not cause the divides, it only revealed them. We believe that our form of democracy is evolving and congress has been unable to exercise much fiscal discipline over the past two decades.

The Tax Bill is a major initiative for economic growth. However, with its passage along partisan lines, it still underscores the divide in Congress. While the Tax Bill will be stimulative to economic growth, it comes at a cost, which we expect will exceed $1.5 trillion over the next decade. Simply put, the amount of revenue lost as a result of the tax cuts will exceed $1.5 trillion if spending goes as planned and the economy grows as expected.

Eurozone Economy is Showing Strong Growth

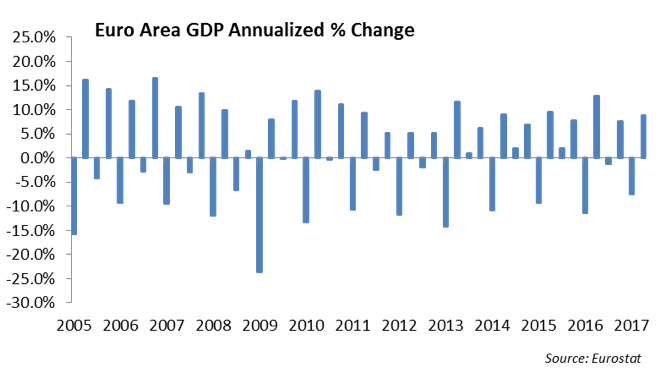

Growth in Europe’s economy has been choppy but is approaching 2.0% over the past year and we expect European economies to grow in 2018. As the labor market tightens, the strengthening in Europe’s economic recovery is reducing the need for the stimulus provided by the European Central Bank’s (ECB) bond purchase program. During the last quarter, the ECB announced that it would reduce its monthly purchases through its quantitative easing program from €60 billion per month to €30 billion per month beginning in 2018. Europe’s economic recovery has been more fragile the United States’ and the ECB cannot afford to take its foot off the pedal just yet.

Europe, like the United States, has entered into a new monetary regime with the aggressive use of its asset purchase program. At the end of the day, the process of a central bank printing money over the near term in order to purchase outstanding bonds will help to lower interest rates which, in turn, will help to stimulate economic growth. However, as every central bank in every developed country has leveraged their balance sheet, the downside risks increase during a period of economic slowing.

These risks will likely be challenged first in Italy where GDP growth has improved to 1.5%, its fastest pace in over seven years. Italy has rebounded strongly with the help of the ECB stimulus and the country has taken significant steps to clean up its troubled banks. However, the government has failed to take the hard steps toward austerity measures such as cutting government red tape and reducing labor costs. The low interest rates orchestrated by the ECB helped to reduce mortgage rates to as low as 1% and helped housing prices recover. Corporate interest rates fell to an average of 1.60% this past summer, a decline of roughly 200 basis points in five years. Saddled with higher budget costs and an ever-changing government, and without the tailwinds of monetary stimulus, GDP growth in Italy will decline. Under increased economic stress, they will have more difficulty managing their debt service.

Europe will benefit from increased consumption and the infrastructure buildout that will result from the United Kingdom’s exit from the European Union. Economic growth in the U.K. will slow however, and we expect downward pressure on commercial and residential real estate markets over the next three years.

Investment Strategy

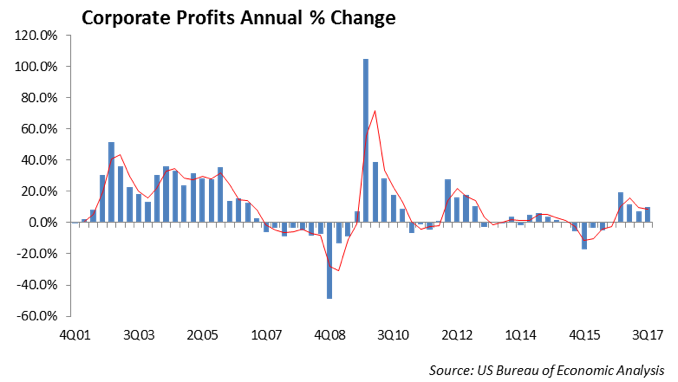

U.S. stocks posted strong gains in 2017 with the total return for the S&P 500 at 22% for the year. Corporate profits continue to be strong as operating margins remain solid and companies are showing increased revenue growth. With the coordinated global central bank stimulus coming together in unison, 2017 experienced a synchronized rally in global stocks as well. The MSCI ACWI ex-USA Index ended 2017 with a gain of 27%, which is the first time in five years that international stock markets outperformed the U.S. We expect sustained low interest rates will be the most significant contributor to supporting current equity valuations in 2018.

Optimistic estimates says that the Tax Bill effectively put $3,000 to $8,000 into the pockets of the middle class households in additional income. This should help consumption and translate into improved corporate earnings. Domestic stocks should have a tail wind over the near term with the passage of the Tax Bill. In addition, any infrastructure package will be further stimulus and will help to support earnings. Less regulation and lower taxes has helped to push valuations in the equity market higher; but, this does not translate into higher long-term growth or sustained returns. We expect equity returns to trend lower from these elevated valuations.

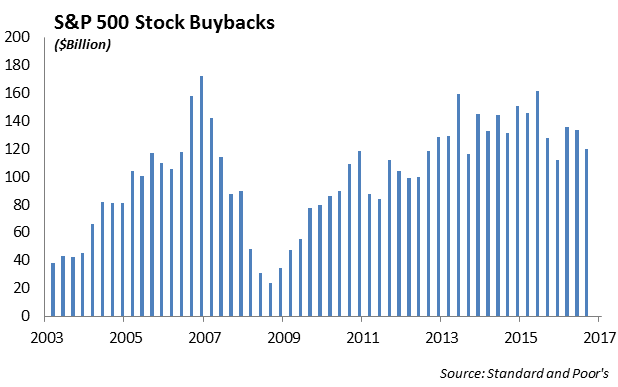

We should expect to see shareholder friendly initiatives from companies that are repatriating their cash from overseas as part of the Tax Bill. In general, we have been critical of the stock repurchase programs perpetuated by corporate management as they repurchase their stock at continually higher valuations. But, with cash in hand, we expect to see a modest acceleration in the pace of stock repurchases as well as increases in dividends from some of the companies bringing cash back to the United States. Low volatility will remain. The markets have been extremely resilient to global geopolitical events. The S&P 500 has risen 120% over the past five years with the backdrop of low volatility, its longest rally under low volatility conditions.

We are concerned with the concentration of large cap tech names that is driving index performance. The 50 largest companies by market capitalization represent over 50% of the S&P 500 today. We expect small cap stocks will outperform large cap as the effects of the Tax Bill work through the economy.

We would expect international stocks will perform well in 2018. Europe’s infrastructure buildout as part of Brexit will be stimulative to the Eurozone economy. In addition, Japan is starting to show economic growth and seeds of inflation are taking root.

With the improving trend in GDP growth combined with the reduction in monetary stimulus, we expect interest rates will increase and the 10 year US Treasury yield to test 3%. However, we expect there is a natural ceiling to how high rates will move. There are two reasons we believe rates will remain low: there is a large amount of money sitting on the sidelines ready to come into the market and there is a lack of sustained inflation.

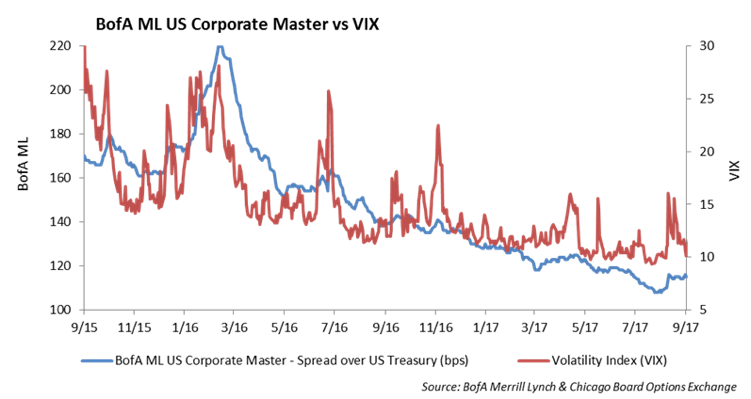

The investment grade credit market once again had record issuance in 2017. With the opportunity to move cash back from overseas, we expect investment grade new issuance will subside in 2018. This will help to keep spreads tight and support low spread volatility levels. The high yield market has also shown tremendous strength over the past year. With spreads near historic tight levels and volatility low, we are cautious on high yield and would take this opportunity to underweight the asset class. Default rates are below 3% according to Moody’s which bodes well for credit spreads.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2018 Winthrop Capital Management

Read more commentaries by Winthrop Capital Management