Weighing the Week Ahead: Is this an Inflection Point for Both Stocks and the Economy?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is normal, but some of the results might not be released on schedule. If the government remains shut down, economic news may take a back seat to the political maneuvering. While we don’t know how that will play out, we can expect an important stream of corporate earnings reports. With competing news from several fronts, I expect pundits to focus on possible changes in direction. Many will be asking:

Should we be probing for an inflection point? In stocks, the economy, or both?

Last Week Recap

In the last edition of WTWA I expected a focus on earnings reports and the confusing impacts of the recent tax legislation. There was some of that, but much more attention on the shutdown saga. Even that could not compete with the public interest in the name for a baby.

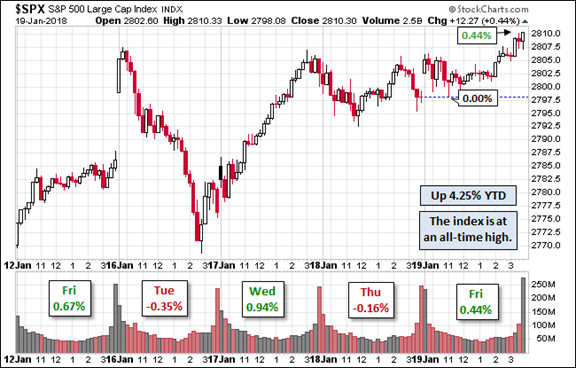

The Story in One Chart

I always start my personal review of the week by looking at a great chart. I especially like the Doug Short design with Jill Mislinski updates and commentary. You can see many important features in a single look. She notes the new records along with other indicators. The entire post is well worth reading for the collection of charts and analytical observations.

The trading range for the week was still below 2%, but it was nearly covered in a single day. The moves seemed dramatic, but are still well below the long-term averages.

Personal Note

I am off next weekend. Wish me luck. I am the teammate of Mrs. OldProf and her favorite bridge partner. Much is expected! I will try to do an abbreviated update including the indicators.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The economic news leaned positive. I thought that the Beige Book might draw more attention, but it lacked significant changes. I recommend Steven Hansen’s summary – an effective and efficient way to get any important information.

The Good

- Industrial production increased 0.9% after a small decline last month. This beat expectations of 0.4%.

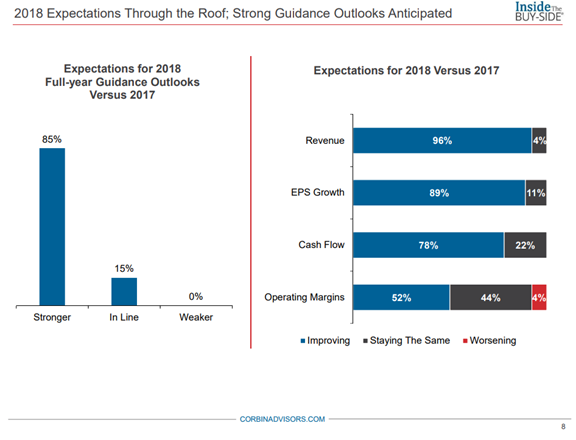

- Industrial sentiment is strong, setting records in some categories. The Corbin Advisors Survey has excellent information from sources not easily reached otherwise. The report is chock-full of interesting charts, helping you get a lot of information with a modest commitment of time. Here is a taste:

- Rail traffic improved in the last reported week. Steven Hansen (GEI) focuses on the “economically intuitive sectors” to tease more signal from this indicator. Check out the charts and analysis in the full post.

- Building permits were about even with the prior month at a SAAR of 1302K, but this beat expectations of 1280K.

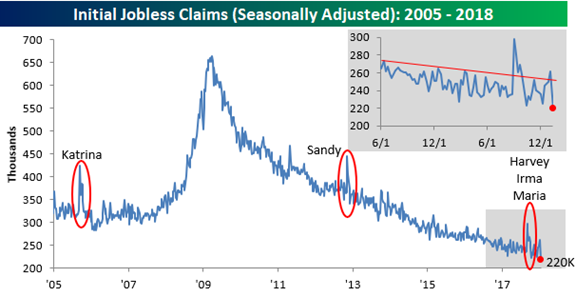

- Initial jobless claims plunged from 261K to 220K. The chart from Bespoke does a nice job of showing the recent detail as well as a longer-term trend.

The Bad

- Michigan sentiment declined to 94.4 from the prior month reading of 95.9. While this is only the preliminary survey, it is a big miss from expectations of 97.

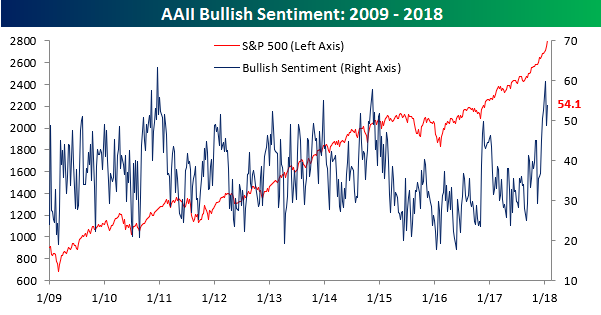

- Sentiment is more bullish which is viewed as a contrarian indicator. Bespoke has the story.

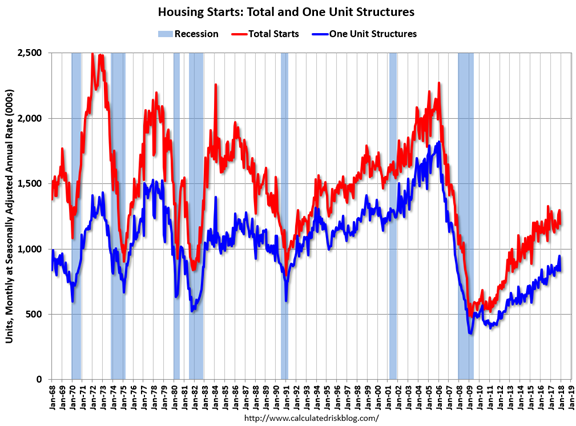

- Housing starts declined 8.2% from November to December and 6% on a year-over-year basis. Calculated Risk, the leading source on housing, cites this as confirmation of two important trends. First, multi-family starts are decreasing while single family increases. Second, the “wide bottom” in housing, which Bill accurately predicted years ago, continues to unwind. Here is the single-family chart.

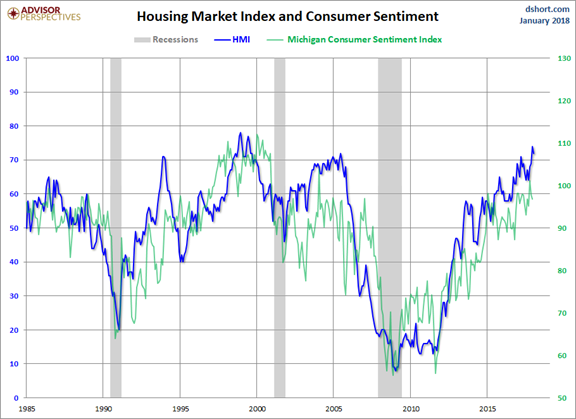

- NAHB Housing Index declined from the prior month and slightly missed forecasts. The NAHB emphasized that this remains a very strong reading. Jill Mislinski reports, including a helpful chart showing the close fit with the Michigan Sentiment survey.

The Ugly

The shutdown “negotiations.” Last week I said I was getting “more worried” about this topic. As I write this, there has been little progress, despite apparent widespread agreement about most of the pieces and the costs of a shutdown – even a temporary one. Part of this is built into the process, but part is due to the participants. Here is an important fact that I have not seen mentioned in any reports: The roots of this problem stem from the 2011 debt limit debate. That is the one that resulted in the so-called “Super-Committee” that was supposed to hammer out a spending compromise. The debt limit was raised, but without a compromise there would be sequestration of funds, balanced between defense spending and social programs. This was supposed to encourage participants to reach agreement.

My son Derek (now in law school at Iowa) helped me by writing an excellent profile of the committee members. I wrote the conclusion to that post and explained why I thought the process could work. They remained deadlocked. The failure of the Super Committee sparked a wide range of economic and market worries, which I reviewed at the time. Almost seven years later, and despite power shifts and changing characters, we are still living with the consequences from 2011.

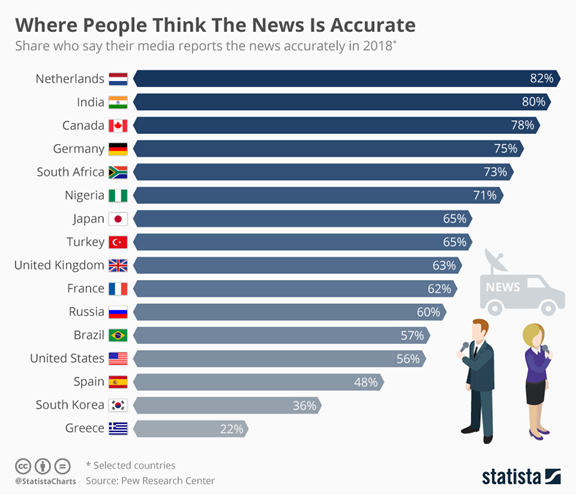

Much of the current debate is about who is at fault. To decide that a citizen would need to have an accurate source of news, which makes this chart even more depressing. (Pew Research Center via Statista).

And a follow up on the Hawaii false alarm. It was not just a “wrong button.” It was a selection from a complex menu and it required extra confirmation. Two days later, Japan also issued a false alarm. These incidents are serious, harmful, and dangerous.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

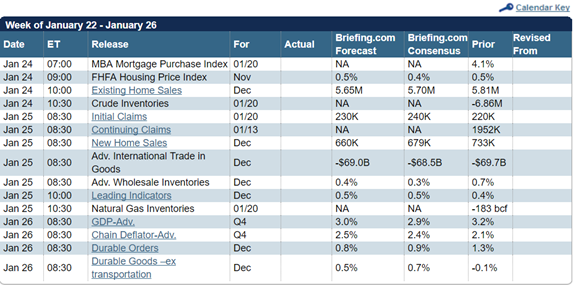

The Calendar

We have a normal economic calendar, but without the most important economic reports. Many observers swear by the leading indicators. I am more interested in new home sales. The GDP report is backward-looking, but always interesting as a foundation for tracking the economy. Some of these reports may not be released on time if the government shutdown continues.

The most important news will once again be corporate earnings reports, especially discussions of outlook.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

The normal calendar may be abbreviated if the shut down continues. Fed Speakers will not be on furlough, so they will continue on the speaking circuit. We are getting come clarity in corporate earnings, and the effects vary widely by sector. To some observers, it is time to expect a new direction. As usual, they disagree strongly on what that will be! The debate will raise the question:

Are we at an inflection point for stocks and the economy?

As usual, here is a typical range of opinion, from bearish to bullish. As an extra complication, the viewpoints are a mixture of technical analysts’ conclusions, market valuation and fundamentals, one-time tax cut effects, and lasting tax-cut effects. It is a bit clearer than last week, but not by much.

- An over-valued stock market can be toppled by the slightest source of bubble pricking.

- Regardless of long-term values, stocks are overbought and overdue for a pullback. The Fear and Greed Traderlooks at both sides.

- That is healthy, needed, and benign; or

- This would be the first sign of a much bigger decline.

- Stocks may be reaching the limits of growth (Scott Grannis). Except the tax cut effects may not be included, he notes. Recession Alert issues a similar warning based upon their S&P forecasting model.

- Some economic indicators seem to be rolling over. Is this an inflection point, or the Q1 weakness seen in recent years?

- There is a one-time tax cut for many companies, increasing S&P 500 earnings by 7 or 8 percent beyond current levels. (FactSet).

- Investment stimulus from the cuts can foster economic (and earnings) growth beyond the initial effects. Apple, Inc., for example, has $252 billion in overseas cash, will pay $38 billion under the reduced taxes, and add $30 billion to its US investment plan. The cash may also fund additional buybacks and dividends.

To summarize, there could be an inflection point in stocks (either a correction or major decline) or in the path of economic growth. As usual, I’ll suggest my own interpretations in today’s Final Thought.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

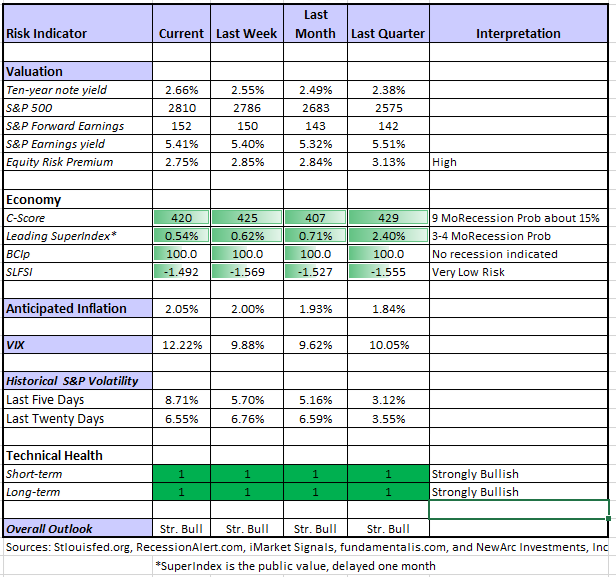

The Indicator Snapshot

Despite higher stock levels, the earnings yield as actually increased. Brian Gilmartin’s coverage explains the change, which is reflected in our Indicator Snapshot.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Georg Vrba: Business cycle indicator and market timing tools. None of Georg’s indicators signal recession.

Doug Short: Regular updating of an array of indicators. Great charts and analysis.

Guests:

Jeff Hirsch, editor of the Stock Traders’ Almanac, notes that the current VIX level is not worrisome, despite descriptions of the “spike.” As I noted on Twitter, this article has plenty of sound information for those watching a much-misunderstood indicator.

Insight for Traders

Our discussion of trading ideas has moved to the weekly Stock Exchange post. The coverage is bigger and better than ever. We combine links to trading articles, topical themes, and ideas from our trading models. This week’s post discusses the challenges for traders in a bull market, with many still on the sidelines. We cite leading sources and update ideas from our models. Performance updates are published, and of course, there are updated ratings lists for Felix and Oscar, this week featuring the NASDAQ 100 components. Blue Harbinger has taken the lead role on this post, using information both from me and from the models. He is doing a great job, presenting a wealth of new ideas and information each week.

This week we featured advice from Brett Steenbarger, who showed how some traders were locked into a market viewpoint that provided little chance for gain. As is so frequently true with Dr. Brett’s posts, the message is useful for investors as well.

Imposing your trading “style” on markets regardless of regime can be hazardous to your wealth. Assuming that all you need to do to make money is double down on your “style” and work on your mindset only compounds the problem.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be the Barron’s Roundtable issue. Individual investors will find it a refreshing overall perspective. I was impressed that so many good managers, representing quite different approaches, could all find stocks that are attractive, and even cheap, on an earnings growth basis. The website has some (but not all) of the picks, but you really need to read the full story to get the full picture. I found many interesting ideas, and you will, too.

Stock Ideas

I suggest investors join me in reading selections from the first-rate Seeking Alpha Positioning for 2018 series. There are many good ideas. If you missed my contribution, you can read it here. I give this piece special effort and appreciate that I am often hitting clean-up on this series.

The Internet of Things is a great place to go shopping, and the Consumer Electronics Show featured plenty of ideas. Some will gain traction, some will not, and all are exposed to possible problems. Barron’s mentionssecurity specialists (Cisco and Fortinet) as well as storage leaders (Micron Technology).

“Memory and storage is at the sweet spot in what’s happening in IoT,” says Micron CEO Sanjay Mehrotra. The venerable company offers both flash memory and drives to manage and protect the vast amount of data floating among so many devices, earning it an important spot in the IoT ecosystem.

“If you don’t protect your devices, all that convenience adds up to nothing,” he says.

Blue Harbinger’s work always reflects careful and extensive research. While this preferred issue is trading at a slight premium, Mark likes the 10.9% yield, growing revenues, and shrinking debt.

As an investor, which would you prefer: Sprint, AT&T, T-Mobile, or Verizon? Hale Stewart’s analysisillustrates how to do such a comparison and it also provides a helpful conclusion.

Can a REIT investment centered on shopping centers be attractive? Colorado Wealth Management, with a careful look at fundamentals and plenty of charts, concludes that Taubman Centers (TCO) is on sale. One needs to look at the underlying assets and the quality of properties.

IBM? Stone Fox Capital balances the positives against the recurring complaints about lack of revenue growth and financial engineering.

David Fish has an update on Dividend Challengers, with 153 increases expected this quarter.

Interested in the DJIA? Peter F. Way’s method of analyzing real experts – those trading and hedging stocks each day – provides a risk/reward analysis for each of the 30 components.

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich continues his excellent series. While theoretically aimed at advisors, there are many themes of interest for individual investors. This week included several great entries, but my favorite is his post on the role of luck in investing. He raises several great points, highlighting his own conservative approach as well as a Bitcoin post from Roger Nussbaum. Gil is using the Bitcoin story as an important illustration.

I strongly endorse the idea of risk control, which is why I have repeatedly advocated modest trading positions (if any) in crypto currencies. If you hit big on something, beware of thinking that you are a genius. Risk control means dialing back the size.

Abnormal Returns has a special Wednesday focus for individual investors. There are a variety of ideas, and nearly always something you will find useful. This week’s highlight of the BloombergGadfly is especially helpful. Many do not realize that well-known discount brokers are not fiduciaries. Your contact is probably getting paid more for recommending certain products – and you don’t know it.

Watch out for

High-yield debt. “Overhyped” says an analysis discussed by Joe McGrath of Institutional Investor.

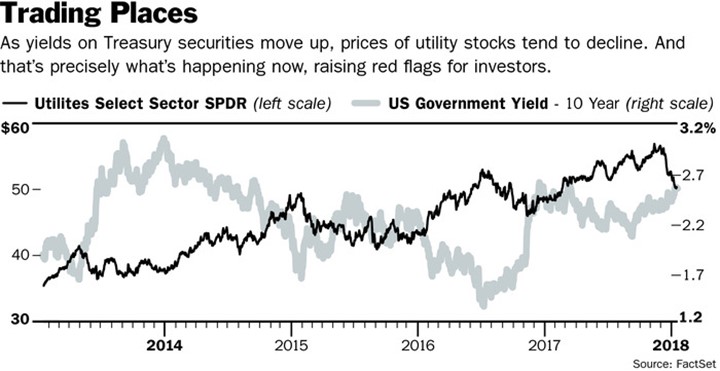

Utilities. I understand that I am repeating this theme, but it is an important one affecting many. Even the small recent move in interest rates has had a dramatic effect on utilities. I agree with Lawrence C. Strauss, Don’t Chase High Utility Yields, a bond proxy that did not benefit from the tax changes. Some may be able to generate adequate growth and raise dividends, but you should not expect the stock price (and therefore total return) to keep up.

“Hidden risks” in ETFs (Enterprising Investor). Many do not accurately track benchmarks. Some international funds do not accurately reflect the expected country exposures. Mohammed El-Erian and BlackRock have both concluded that funds “over-promote” the liquidity in underlying holdings.

If the performance of ETFs that track specific indices can be that variable, what about the funds with more idiosyncratic objectives?

Take the iShares MSCI BRIC ETF (BKF) and the Guggenheim BRIC ETF (EEB) as cases in point. Both seek to provide diversified exposure to Brazil, Russia, India, and China, but how much of each? The iShares offering had 61.5% invested in China and 7% in Russia at the time of this writing, while Guggenheim’s fund had 20.2% in China, 13.9% in Hong Kong, and 18.1% in Russia.

You would think targeting just four countries would make the innate challenge of defining emerging markets simpler, but that’s just not the case. Fund structures can only mask the intrinsic complexity of markets, not eliminate it.

Final Thoughts

The confusing array of strongly-held opinions seems more intense than usual. It is probably augmented by the sharp partisan disagreement on many issues. For investors, this raises the stakes and challenges us to focus on meaningful data.

- Many investors probably cannot define “overbought” but it certainly sounds bad. If we simply said that the market showed more strength than it has in 20 years or so, that would be both accurate and less threatening. Overbought conditions can continue for months and deliver significant added gains. It is not a magical timing indicator.

- I do not see corrections as “healthy” but we should all accept the reality of the occasional 15-20% drawdown. There is no schedule for corrections and no established method for accurate forecasting. It is part of the inherent risk when one invests in stocks.

- Part of the explanation for market strength has been an improving economy and significantly higher earnings.

- The tax cuts will provide a significant earnings boost for some sectors, helping to support the overall market. That is a major positive for the year ahead.

- Additional economic growth can come from increased business confidence and repatriation –both factors that will increase investment. It might also come from an infrastructure bill, if we could get some compromises out of Washington.

On balance, the prospects look good. The inflection point may prove to be another leg up for the economy and earnings. The notion that good things must end is a powerful, intuitive feeling. Some day it will be true, but it has nothing to do with the age of the bull market. At the first sign of weakness, I expect to see a bull market in fear!

When the volume of the noise increases, reliable risk indicators become even more valuable.

I’m more worried about:

- Spillover from the shutdown. The inability to find a compromise has an immediate economic effect. If it reduces confidence, that effect will be magnified.

- The “rolling over” psychology. Many economic indicators currently signal great strength. Some are beginning to show a slower rate of growth. If reasonable strength is maintained it is not really a cause of concern. News reports, however, will start to talk about slowing growth and economic weakness. Elevated expectations may be missed. This can also be something of a self-fulfilling prophecy as confidence is reduced.

I’m less worried about:

- The Fed. There are no signs of sharp policy changes that would block economic growth. The measured reduction in the balance sheet is not a cause for concern.

- Bitcoin volatility and the market. Many believed that a selloff in Bitcoin would be a problem for stocks in general. After last week there seems to be little support for that hypothesis.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits