In their first-quarter (Q1) 2018 outlook, K2 Advisors’ Research and Portfolio Construction teams believe favorable dispersion has created reasons for optimism in three main hedge-fund strategies: Long/Short Equity – Europe, Relative Value and Discretionary Macro. We believe offering these insights will help investors better understand the rationale for owning retail mutual funds that invest in hedge strategies.

As the Liquidity Tide Recedes… Will Investors Need a Different Boat?

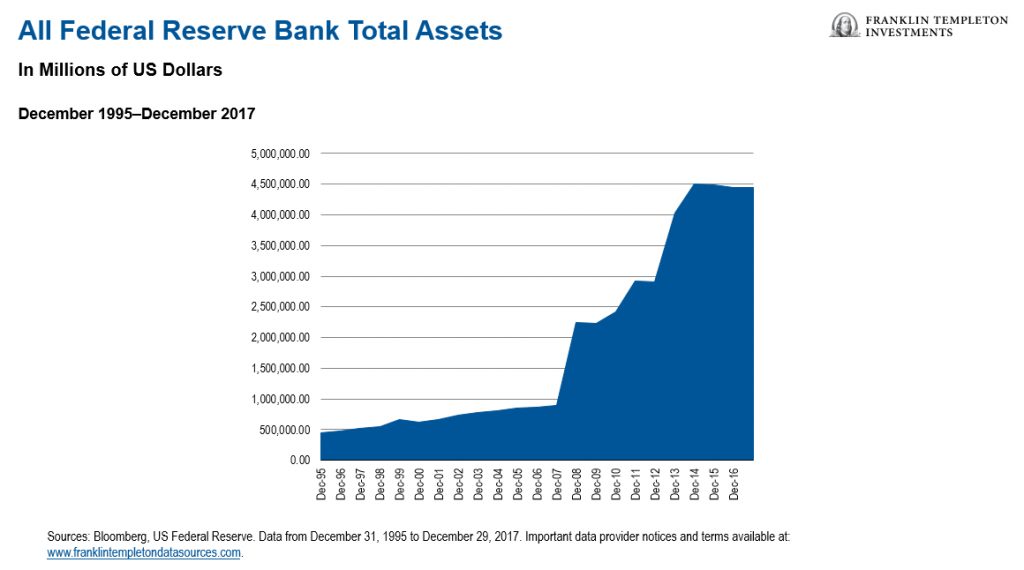

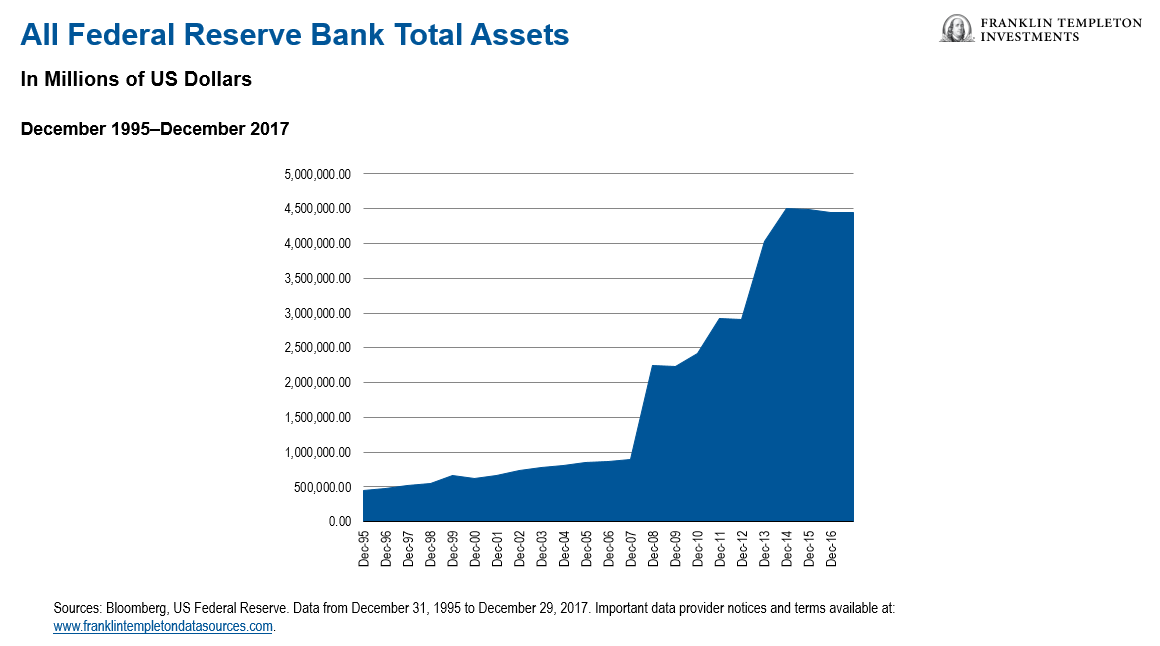

The post-2008 expansion of the Federal Reserve’s (Fed’s) balance sheet from around $900 billion to nearly $4.5 trillion today has been one of the most dominant market-shaping forces over the last decade; a massive tide of liquidity that lifted assets across the globe—in some instances indiscriminately—while influencing investor behavior. In addition to yields being driven toward record lows and stock markets to record highs, many investors migrated toward riskier assets while the cost of capital was kept artificially suppressed. We believe this dynamic is about to change.

The tide appears to be receding. While the Fed has already embarked on its journey toward rate normalization, other major central banks around the world also appear poised to begin unwinding in 2018, with many striking increasingly hawkish tones. In addition, global growth has reset inflation expectations to the upside, led by China’s resilient economy.

Investors who are not prepared for this shift from the recovery era of monetary accommodation to the expansionary post-QE era may be exposed to significant risks, in our view. Markets could see increased volatility and sharp corrections, recalling, for example, the magnitude and speed of adjustments in US Treasury (“UST”) yields that occurred during the fourth quarter of 2016.

One of the challenges for investors in 2018 will be that the traditional diversifying relationship between bonds and risk assets investors expect may not hold true in this new era, particularly if we experience the cycle of UST declines we anticipate. It’s quite possible to see risk assets also decline as the “risk-free” rate (yield on USTs) ratchets higher. Markets have become accustomed to exceptionally low discount rates; a shift higher would materially impact how those valuations are calculated.

Additionally, we feel a sense of complacency has developed across the asset classes as UST returns and risk-asset returns have often had positive correlations1 , along with positive performance, in recent times. However, the positive outcomes achieved under the benefit of extraordinary monetary accommodation can mask the actual underlying risks in those asset categories. As monetary accommodation unwinds, those positive correlations could continue but with the opposite effect—simultaneous declines across bonds, equities and global risk assets as we exit an unprecedented era of financial market distortions. These are the types of correlations and risks we are aiming to reduce in 2018.

The bottom line is that we believe the massive tide of low-cost money that lifted all boats and allowed for carefree sailing is receding. Investors who are not prepared for this change may be exposed to significant risks.

Perhaps it is time to look to add other boats to one’s portfolio, crafts better suited to navigating the sandbars, rocks and muddy waters that we believe will likely surface in the coming quarters. While these developments may affect hedge-fund strategies differently, alpha2 for the hedge-fund universe has historically strengthened in these environments of increased dispersion and volatility, particularly when interest rates rise.

Long/Short Equity Europe

We think Europe is poised for higher economic growth with strong consumer confidence, improving inflation, and decreasing unemployment levels. While these factors should trickle into earnings, markets are currently pricing in low growth.

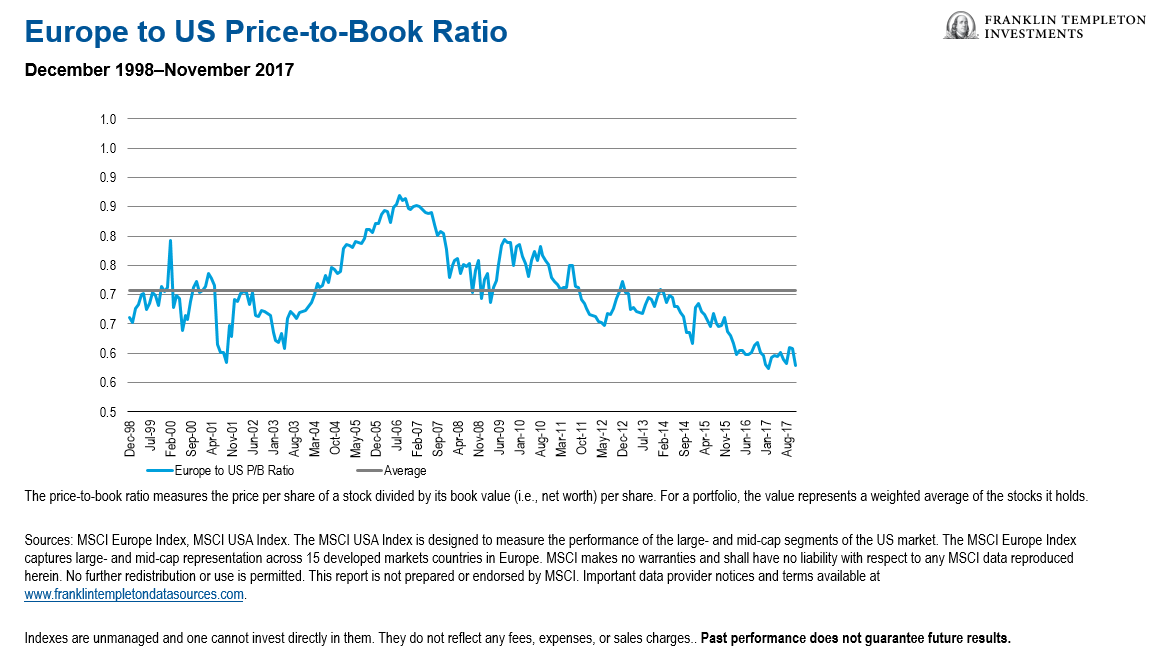

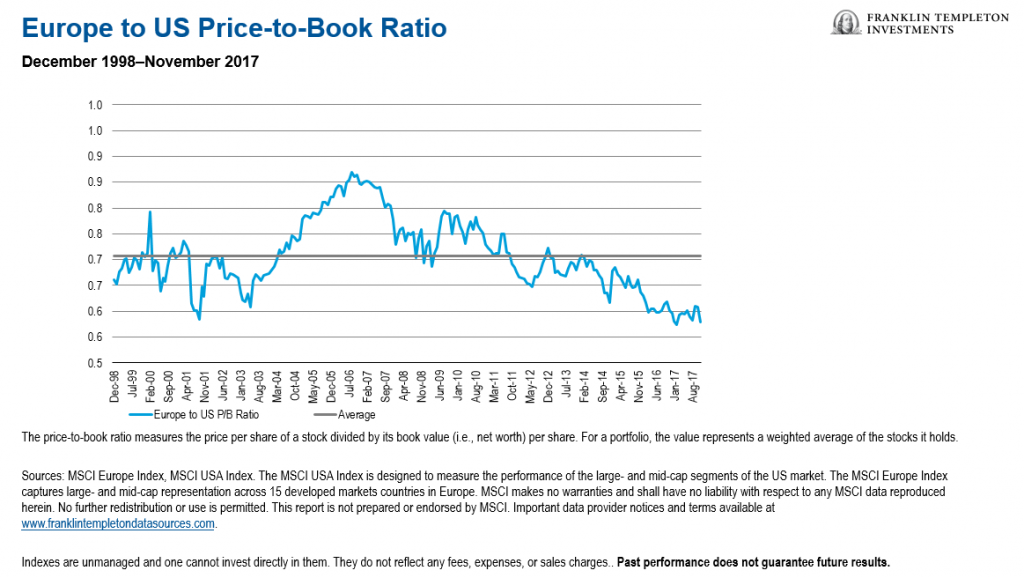

European equity valuations appear more favorable on a historical relative basis. The Europe to US price-to-book ratio remains at record lows (see chart below).3 Recent developments such as Brexit may lead to further bifurcation (i.e. domestic-oriented companies vs. companies with international sales) within Europe, creating clear groups of winners and losers.

Long/short investors within the region may be able to take advantage of this dispersion. It’s our belief that uneven growth across the region will result in increased dispersion of stocks, sectors or countries which should help generate higher alpha. Similar to the United States, rising interest rates driven by the European Central Bank’s unwinding of fiscal stimulus may allow companies to experience similar tailwinds as US companies have.

Discretionary Macro

Shifting central bank policies, changing central bank leadership, the potential for geopolitical instability and other risk factors may all serve to increase market volatility, and could provide discretionary macro managers with an improved opportunity set for trading across fixed income and currency markets.

Additionally, we believe that the calendar of economic and geopolitical events in 2018 should offer attractive trading opportunities for discretionary macro managers focused on fixed income and currency markets.

Relative Value – Fixed Income

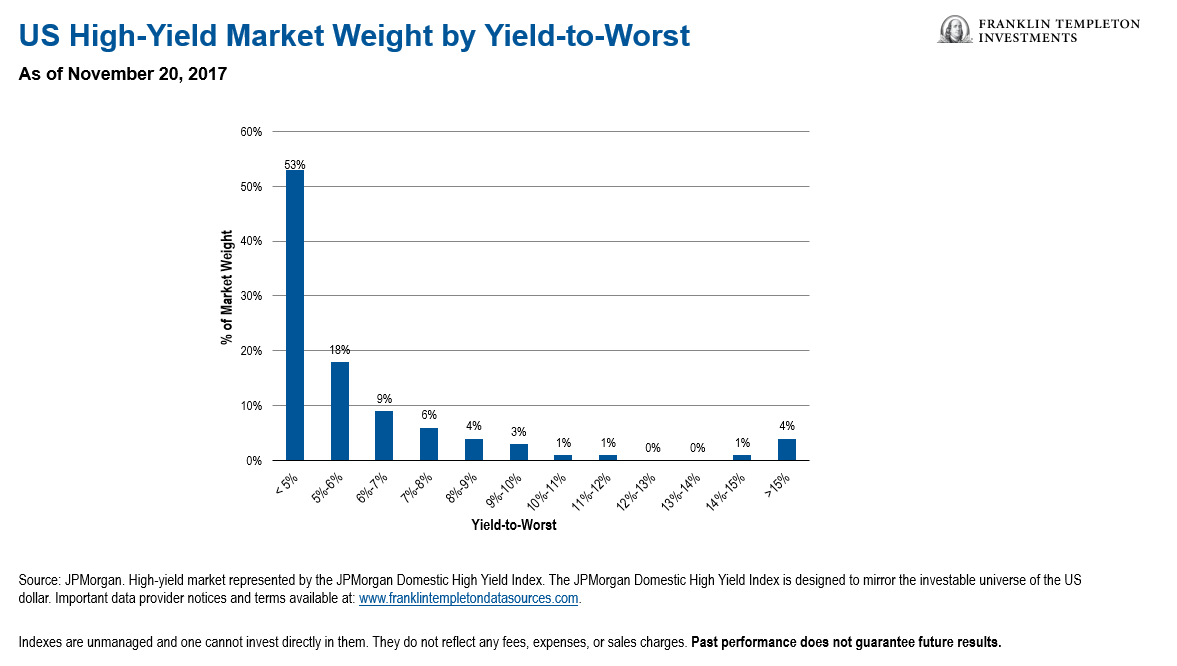

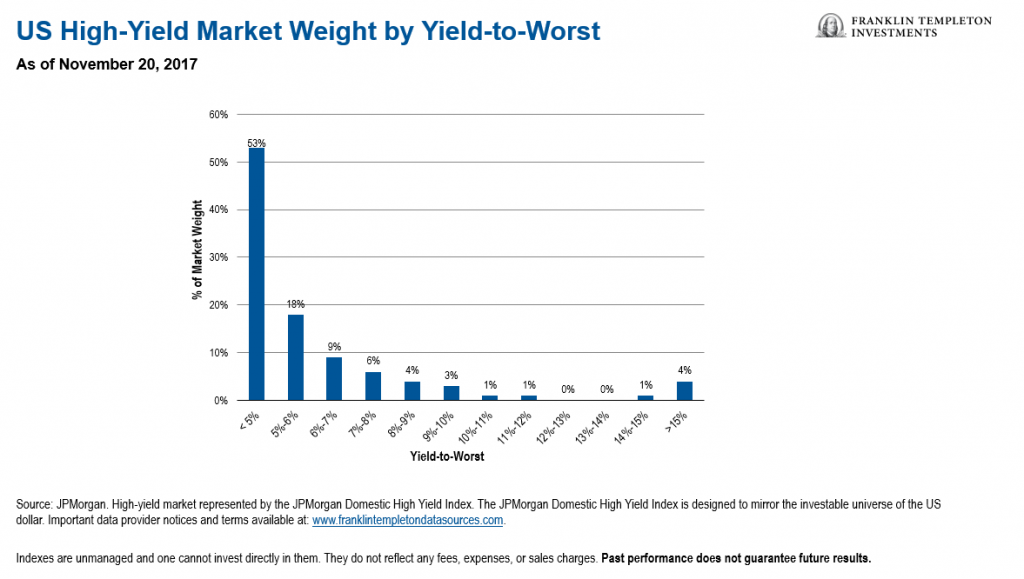

While rates have remained lower for longer than the market originally anticipated, duration risk4 is still prevalent in many fixed income investors’ portfolios. In our view, the high-yield market has never been more interest-rate sensitive.

We believe relative value fixed income managers such as long/short credit managers are well positioned, given their shorter duration portfolios, and should be able to generate alpha from rising sector dispersion.

You can learn more about the types of hedge strategies referenced here in our prior blog, “Solidifying a Case for Liquid Alts.”

Comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

To get insights from Franklin Templeton Investments delivered to your inbox, subscribe to the Beyond Bulls & Bears blog.

For timely investing tidbits, follow us on Twitter @FTI_US and on LinkedIn.

What Are the Risks?

All investments involve risks, including possible loss of principal. Investment in these types of hedge-fund strategies is subject to those market risks common to entities investing in all types of securities, including market volatility. There can be no assurance that the investment strategies employed by hedge fund and liquid alternative managers will be successful. It is always possible that any trade could generate a loss if the manager’s expectations do not come to pass. Hedge strategy outlooks are determined relative to other hedge strategies and do not represent an opinion regarding absolute expected future performance or risk of any strategy or sub-strategy. Conviction sentiment is determined by the K2 Advisors’ Research group based on a variety of factors deemed relevant to the analyst(s) covering the strategy or sub-strategy and may change from time to time in the analyst’s sole discretion.

For more information on any of our funds, contact your financial advisor or download a free prospectus. Investors should carefully consider a fund’s investment goals, risks, sales charges and expenses before investing. The prospectus contains this and other information. Please read the prospectus carefully before investing or sending money.

__________________________________

1. Correlation represents the linear relationship between two return series. Correlation shows the strength of the relationship between two return series. The higher the relationship, the more similar the returns.

2. Alpha measures the difference between a fund’s actual returns and its expected returns given its risk level as measured by its beta. A positive alpha figure indicates the fund has performed better than its beta would predict. In contrast, a negative alpha indicates a fund has underperformed, given the expectations established by the fund’s beta. Some investors see alpha as a measurement of the value added or subtracted by a fund’s manager.

3. Sources: MSCI Europe Index, MSCI USA Index. The MSCI USA Index is designed to measure the performance of the large- and mid-cap segments of the US market. The MSCI Europe Index captures large- and mid-cap representation across 15 developed markets countries in Europe. Indexes are unmanaged and one cannot directly invest in them. They do not reflect any fees, expenses or sales charges. Past performance does not guarantee future results. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com. The price-to-book ratio measures the price per share of a stock divided by its book value (i.e., net worth) per share. For a portfolio, the value represents a weighted average of the stocks it holds.

4. Duration represents a measure of the sensitivity of the price (the value of principal) of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments

Investors who are not prepared for this shift from the recovery era of monetary accommodation to the expansionary post-QE era may be exposed to significant risks, in our view. Markets could see increased volatility and sharp corrections, recalling, for example, the magnitude and speed of adjustments in US Treasury (“UST”) yields that occurred during the fourth quarter of 2016.

Investors who are not prepared for this shift from the recovery era of monetary accommodation to the expansionary post-QE era may be exposed to significant risks, in our view. Markets could see increased volatility and sharp corrections, recalling, for example, the magnitude and speed of adjustments in US Treasury (“UST”) yields that occurred during the fourth quarter of 2016.