The 2018 Economic Playlist: Carry the Tune

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSince the dawn of time music has played a pivotal role in the defining of the times and the progression made. We would like to utilize the artistic genius of these maestros to bring some context to the current pivotal point in the economy and capital markets. Our investment outlook and review of 2017 will be available the first week of 2018. This is meant as an economic backdrop to what we see occurring in 2018.

It is said there are three ways to make a mortal enemy of a stranger – inform them that their kids or pets are unattractive, that their political views are obtuse or that they have poor taste in music. I am sure the songs I’ve chosen will evoke nods of agreement, disdain for some and others who just don’t care. In many cases, these choices weren’t meant to define the modern economy when they were written, however, the timeless wisdom could work in multiple periods. We have also moved from a time when the radio was the only medium and the personalization lay with the DJ relaying tributes over the air. Enter the jukebox that had a collection of songs that exchange quarters for a three-minute moment of social relatability. Then we moved to mix tapes in the ‘80s and everyone thought they were John Cusack in “Say Anything” blaring the boom box in the early morning. Fast forward to playlists that are shared at the drop of a dime with anyone who wishes to listen. Music is meant to amp up the moment, soothe the savage beast and everything in between.

The Overall Theme: Paul Westerberg “Runaway Wind”

You trade your telescope for a keyhole

Make way for the gray that’s in your brown

As dreams make way for plans, See ya watch life from the stands

The trading of the telescope for the key hole is a natural byproduct of the specious state of information. The whirlwind that used to be the daily news cycle has been upgraded to a tropical storm and it doesn’t appear that it will subside anytime soon. As we try to make sense of the contradictory and catastrophic headlines, most are left to downgrade expectations and bury their heads in the sand and money in the backyard. We are more alert than ever but none the wiser. As markets and assets ascend to more rarified air, this sentiment of concern is healthy as it is abnormal to past conditions of such economic and market gains. We see a continuation of many of the stronger economic tail winds that blew in 2017 through 2018.

The Federal Reserve: The Eagles “New Kid in Town”

There’s talk in the street,

It’s there to remind you,

It doesn’t really matter which side you’re on

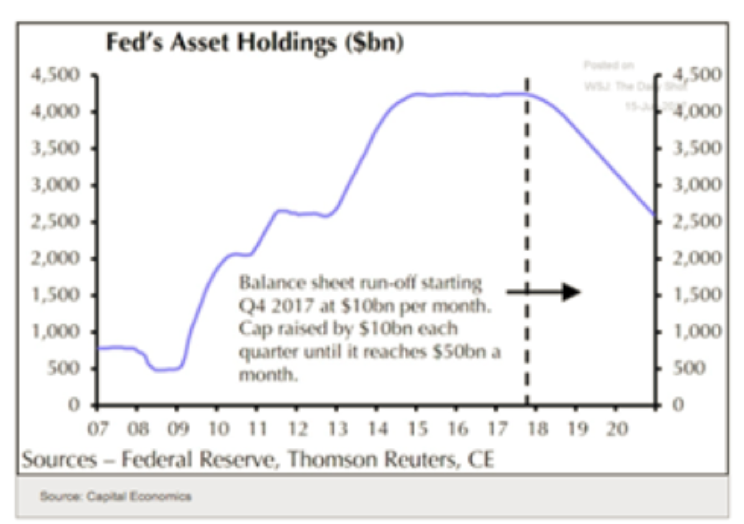

It has been our longstanding belief to not fight the Federal Reserve and we believe that axiom continues to bear fruit for the patient investor. It does not matter which camp you rest your head at night, however, not fighting the Fed is an axiom we should all agree on. The Federal Reserve continued their tepid pace of rate hikes in 2017 and are projecting the same pace in 2018. However, the announcement and details of unwinding their balance sheet added a new and significant twist. Their projection of unwinding was met with a massive “meh” from the markets as if we are playing a massive game of truth or dare. The initial stages are letting Treasuries and Mortgage securities to mature without reinvesting the proceeds. The current level of balance sheet assets total nearly $4.5 trillion, of which 56% are Treasuries and that is up over $3.5 trillion over the last decade. Almost a third of these securities mature in less than five years and promotes the most stable projection is for unwinding at a maturing pace rather than selling securities outright.

The quantitative easing instigated by the Federal Reserve formed an investment environment that went from inhospitable to a very lush environment for investors. And as such, the stages of reversing course from massive accommodation toward small steps of less stimulation, you get the reverse course of anchoring the interest rates. “As above, so it is below” defines what ultimately happens to the yield curve when these begin to shift back to normalcy.

The shifting dynamics of the Federal Open Market Committee: Led Zeppelin “Ramble On”

Leaves are falling all around, It's time I was on my way

Thanks to you I'm much obliged, For such a pleasant stay

But now it's time for me to go ramble on

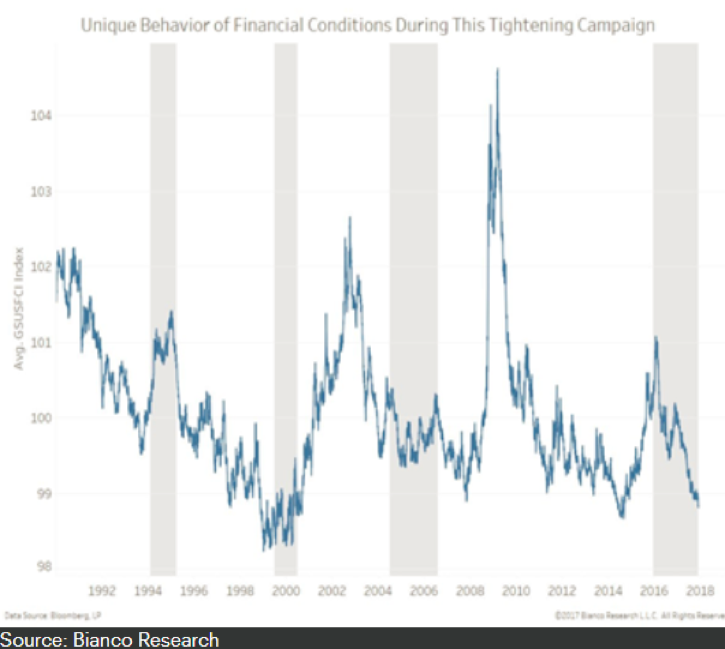

As Chairperson Janet Yellen will be moving on, it is important to tip the cap to growth and stability that the markets exhibited under her watch. She did a tremendous job of juggling the many balls that were handed to her, especially with the heightened political environment that had an increased media coverage and thereby more drive by scrutiny. Consider that financial conditions actually became far more accommodative during the Fed rate hike cycle as compared to the last 30 years.

The board will undergo significant change, even historic in nature. After Yellen and Dudley leave, the board will have its lowest number of Economic PhDs in some time. There is a purpose to bring some business influence to the board and how they construct policy. While the movement of policy has been more hawkish, the new members appear to be a tad bit more dovish than those they are replacing. We don’t believe a stark reversal will be seen, as time has shown that when one moves from the bleachers to the arena, there is a clearer understanding of the gravity of the job. We suspect there will be a continued trajectory of recent actions and tone of such moves.

Inflation: The Police “Walking on the Moon”

Some may say, I'm wishing my days away

No way

And if it's the price I pay, Some say

Tomorrow's another day

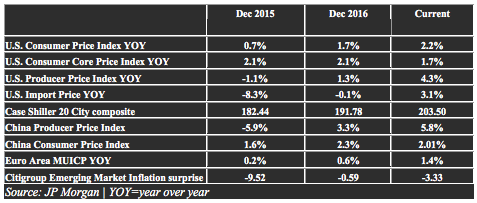

One of our favorite axioms (and duly noted we use ad nauseam) is “the chains of habit are too soft to be felt until they are too hard to be broken.” This is what we continue to see in the inflationary and interest rate environment. As noted by JP Morgan, the Federal Reserve interest rate cycle is the most benign and tepid in history. Prior to the hike in December, the average hike had been 5 basis points (bps) per month as compared to the 18 bps average over the same time frame.

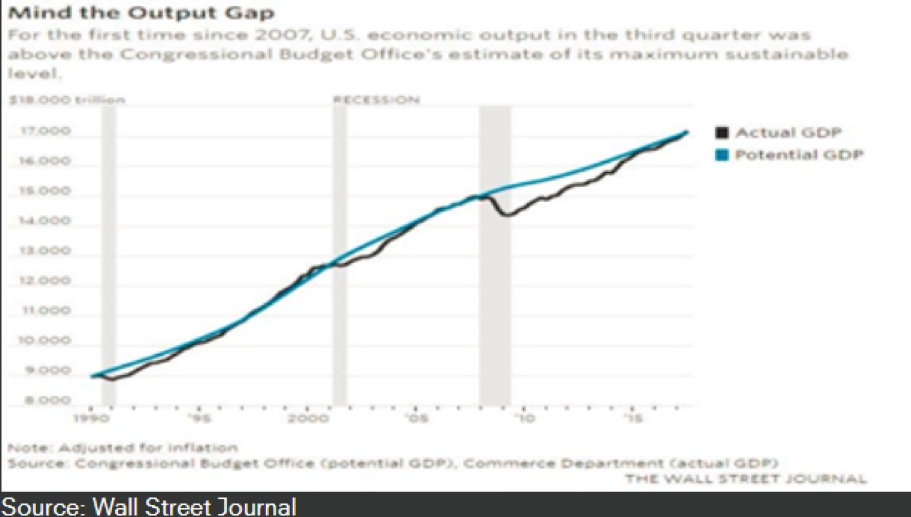

We continue to see the insulator impacts of protectionism that has seen net harmful tariffs up 60% in the last four years across the globe. We have seen a cumulative of 2,552 net harmful tariffs introduced since 2009. Also note that we are running at near full potential via the output gap estimate from the Congressional Budget Office (snicker duly noted, but is corroborated by several other sources).

The output gap is the difference between potential and actual GDP with the conclusion being that as they get closer to each other, inflationary pressures become more prevalent as there is reduced slack. You will see that the output gap was minimal between 1995 and 2000, and 2004 to early 2007. Inflation was slightly above the long-term average during this timeframe, which is what we are calling for. We are not expecting huge spikes in inflation, but rather continued increases in it until the “inflation links” become more rigid. As we point out in the yield curve analysis below, the timing of our current cycle matches much closer to the growth period of the 1990s to 2000.

The Yield Curve: Kansas “Carry on Wayward Son”

Once I rose above the noise and confusion,

Just to get a glimpse beyond the illusion

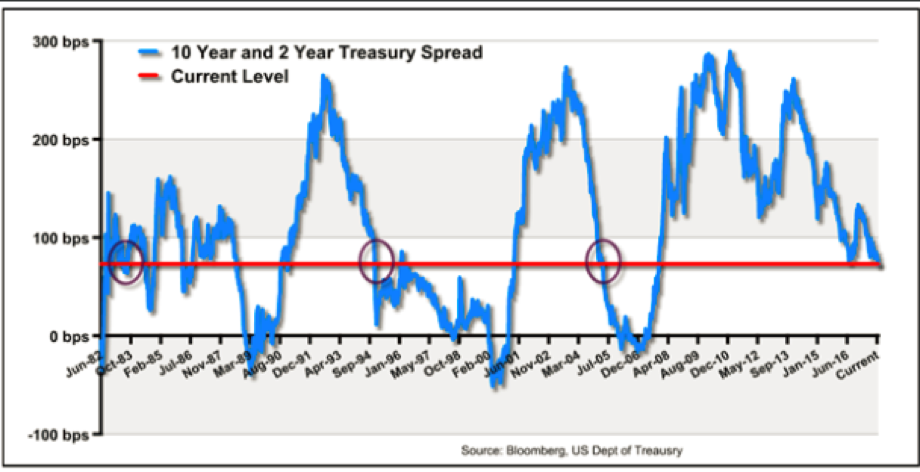

As a byproduct of the Federal Reserve’s anemic hike of interest rates since December 2015, the yield curve has flattened. A flat yield curve relays slowing economic growth while a steep yield curve signifies expanding growth. In fact, it has flattened at such a pace that the flattening has now slowly become a daily indicator much like bitcoin’s level, the price of oil in 2007 and the semiconductor book-to-bill ratio that came out monthly in the mid-1990s. The only thing missing was the intraday price of beanie babies in the early 1990s.

We believe the shape of the yield curve is extremely important and very telling, when done correctly. Currently many use a 10-year chart showing it is at its flattest level. By only using this magical timeframe chart does not provide an ounce of the context one needs to measure its reliability and strength of signal.

In early November we wrote the following to give a better clue when the shape of the yield curve becomes a more viable indicator.

Many market pundits are reminiscent of the sailors listening for sirens of Greek Mythology who were called to their death. Sirens were a mythical creature that would call out with desirable music to lure sailors. There are numerous reports this morning about the flattening of the yield curve signaling the potential for a possible sign that a contingent recession may ultimately be on the horizon. There are as many yield curve spread comparisons available to monitor as there are flavors at Baskin Robbins. Today, the “spread du jour” is the 10-year and 2-year Treasury, so let’s put this in a cone and review its merit.

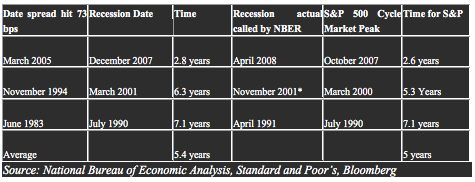

Consider the spread that currently is at 73 bps and that it is at the current cycle lowest spread. Warning sign? When the current level was hit in the last 35 years on the way down from the cycle high, you notice some interesting timing issues.

The monitoring of yield curve spread is important, however, what’s more important is to have a context for this spread as far as time goes and the Fed’s manipulation of the curve via quantitative easing. The latter requires far more artistic license than economists prefer, however, simple truth false analysis states that if quantitative easing lowered market rates, the unwinding should do the opposite. This could be argued about how impactful a monthly drip takes to empty the lake-sized balance sheet, but the direction is straight forward. With reasonable logic, one could argue a curve steepening slightly if the unwinding continues. If the flattening were to continue, the investor should be reasonable about when the typical recession and market peak occurs and not just let analysis without context take place.

We believe that even at the current flattened levels, the average time it takes for a recession to begin is 5.4 years and for the S&P 500 market top to occur is 5 years. However, if you take the most pragmatic and dire case, we are still looking at 2.8 years and 2 years respectively. It is something to watch but it also more important to put into the proper context. The yield curve is still pointing to growth albeit the impact of the Federal Reserve’s actions are having an impact.

Consumer and Business Sentiment: Civil War “Poison and Wine”

You only know what I want you to

I know everything you don't want me to

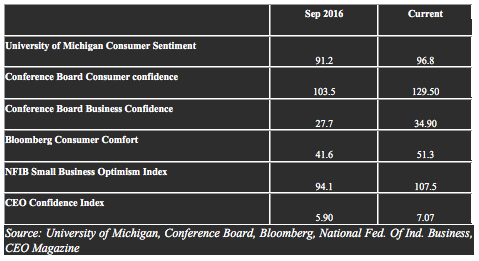

One component that is constantly brushed over is the increased sentiment from consumers to business as the economy has picked up some momentum in the last 15 months (from September 2016 to current).

While this can change abruptly on various aspects, it appears at this time the tax bill will have an overall positive impact to consumers and businesses in 2018. How much is priced in at this time is debatable, however, with the all the ready-start-stop action on it, most investors seem to have fallen into the “it’s trash until its cash” category.

Investor Sentiment: U2 “Every Breaking Wave”

If you go your way, and I go mine,

Are we so helpless against the tide

Traversing the emotional state of the investors in the current climate, we have seen a cautious optimism gained from the downright negative expectation. Many will attempt to combine this shift with the all-time highs of the market as a pure signal of imminent collapse. While we can understand those sentiments, a “correction of unusual size” (ode to the Princess Bride), requires a combination of five qualities:

- Sentiment must be euphoric

- Leverage at near historic levels

- Inversion of yield curve

- Media coverage must be overwhelmingly positive

- Earnings must be rolling over and expectations are tepid in the future.

For those looking to remember this, “SLIME” may be appropriate for those who are frustrated with the legislative process. You can shift it to SMILE for the “ignorance is bliss” in the audience, or LIMES for those who require some Corona or Cuervo to get through this process.

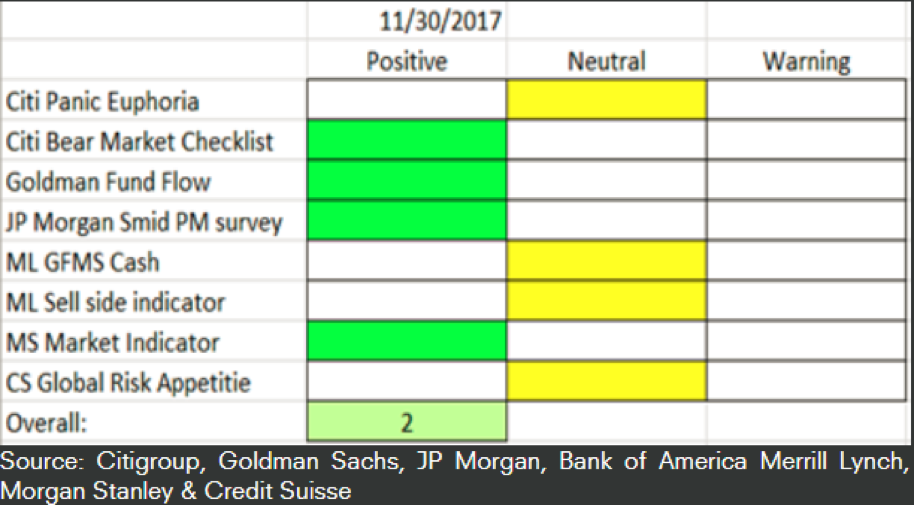

We monitor eight investor sentiment numbers from several sources. Currently four signal stark pessimism and four are neutral. We don’t find any of the indicators showing euphoric belief in the markets moving forward; this is a positive indicator based on history. Though it has shifted over the last year, it appears that there are still positive signs in the economic and investment climate for risk assets in 2018. My dashboard has a current reading of two, which is still in the contrarian bullish camp:

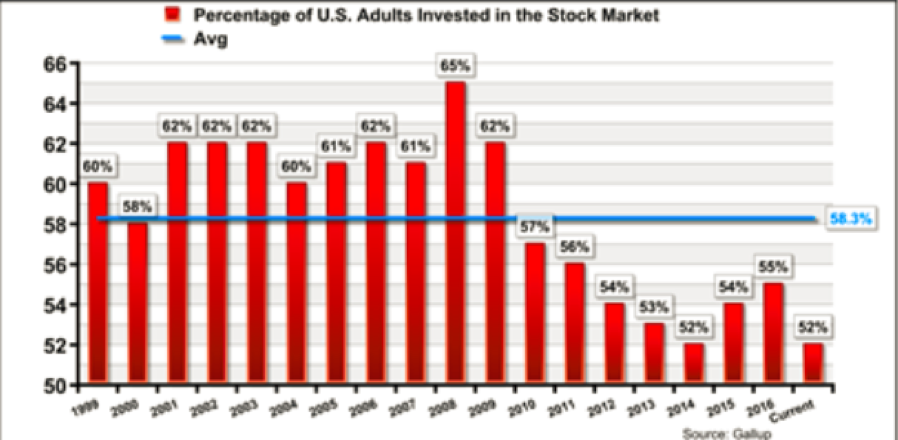

An intriguing component is a survey from Gallup that tracks investors in the stock market over the years. It translates the collateral damage and long memory the general public has when shocking economic events take place. The Great Recession of 2007-2009 and the credit collapse was a once-in-a-generational event and its impression was – and is continuing to – temper positive emotions.

Economic Growth: Cross Canadian Ragweed “Sick and Tired”

You're no longer sick and tired

everything around you feels brand new, yeah.

The days fly by, the nights could be longer,

every day you're just a little bit stronger

The economy in 2017 had some substantive pick up. Since the end of the last recession, we have averaged a 2.1% growth rate. The U.S. averaged 2.53% for the first nine months of the year, with the last two quarters averaging over 3.1% for the first consecutive periods of >3% growth rate since 2014.

The ISM manufacturing PMI index hit its third highest point in the last 30 years in September. The average over the last 30 years is 52.1, which is slightly expansionary. In 2017 this index averaged 57.4, a significant number.

The Leading Economic Index began 2017 at 1.6, a hair under the 30-year average. It currently stands at a robust 5.2 and is picking up steam as this is the high print of 2017.

The Durable Goods order has been volatile as natural disasters have impacted the stability of this number. The 30-year average is a 0.3% number while 2017 averaged double that with 0.6%.

The unemployment rate has dropped to 4.1% and is now beginning to show concerns about the quality of labor and the cost it takes to attract the most talented. The NFIB index that tracks quality of labor as the single biggest problem rose from 12 – about the long-term average – to 18. This mirrors the situation of 1998 when it crossed its current level.

An interesting, but not surprising comparison, is that U.S. personal consumption expenditures have risen 6.8% annually since 1959. U.S. household net worth has grown at an annual rate of 6.9% over that same timeframe.

Consumer: The Ramones “My Brain is Hanging Upside Down”

You’ve got to pick up the pieces,

C'mon, sort your trash,

you better pull yourself back together, maybe you've got too much cash

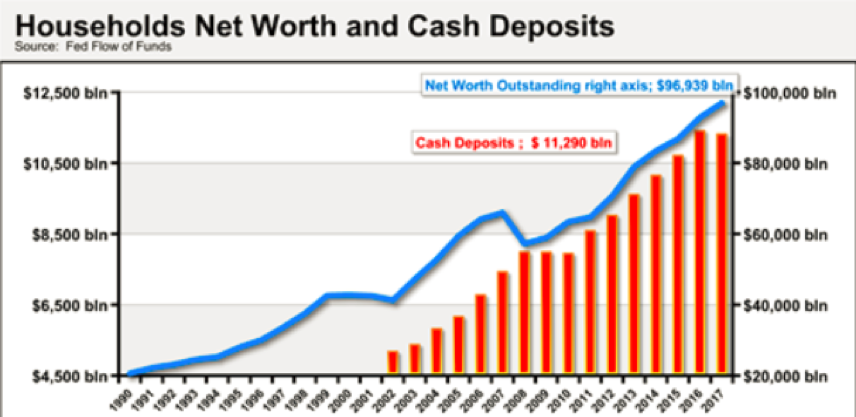

The consumer has been in balance sheet repair for some time and the recent pick up of incremental debt is still at a very tepid rate. A couple of charts signify this and are important for the context.

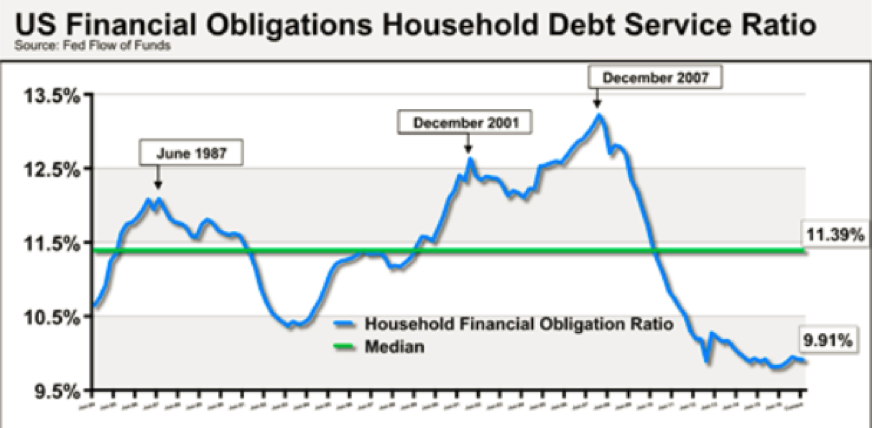

Household net worth and total cash deposits have been increasing annually for some time, yet it took until 2017 for sentiment to begin to match what was occurring on the macro level. On the other side, consider the recalibration on the financial obligation debt ratio for households.

It is extremely important to evaluate the health of the U.S. consumer as they are the largest component of the economy. Currently we stand at $13.5 trillion nominal dollars while the nominal U.S. Gross Domestic Product stands at $19.5 trillion, or 69.5% which is about its long-term average.

Corporate Outlook Grant Lee Buffalo “Arousing Thunder”

Looks like the rain’s holding off, Might as well take this slow

Corporations have been on a more conservative outlook for some time with regard to their prosperity over the last decade or so. They have been choosing on the whole to use much of their earnings and cash flow to buy back stock or increase dividends, both of which are bullish and is not meant to cast a disparaging stone their way. Consider a few important aspects that are having a tremendous impact in 2018:

- In the last six months those companies with focus on spending their money on company cap ex and investment into new areas of growth outperformed those who focused on stock buybacks.

- The tax bill that looks to pass has a significant cut to tax rates to corporations that help ease the uncertainty that CEOs may have about future cash flow. On top of that, the repatriation of cash held overseas (ranges from as low as $1 trillion to as high as $4 trillion) will get a one-time low rate offer to bring it back. This will allow companies to actually do stock buybacks and invest in future sources of productivity and growth.

- According to the Global Fund Manager Survey, portfolio managers at almost 3-to-1 want increased cap ex spending versus improving balance sheet or increase buy backs and dividends.

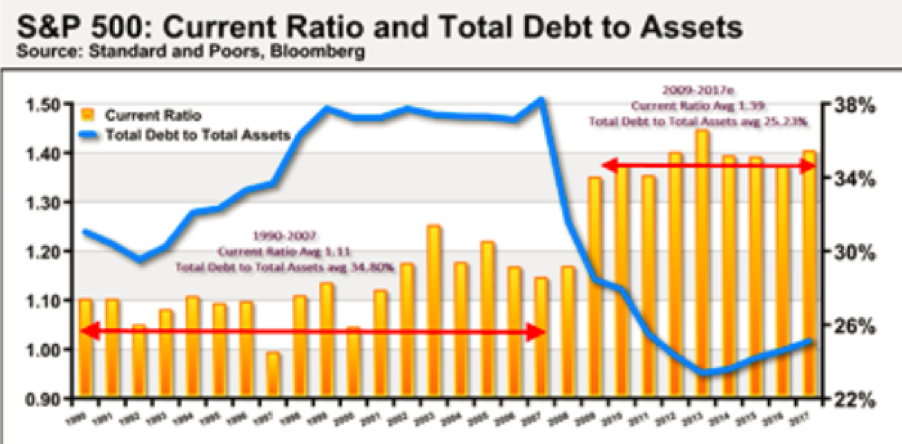

As far as leverage for corporations, there are a few contradicting details being thrown around. Debt has increased at a large pace in corporate America, but so too have assets. Also consider the current ratio of the S&P 500 which has improved substantially since The Great Recession.

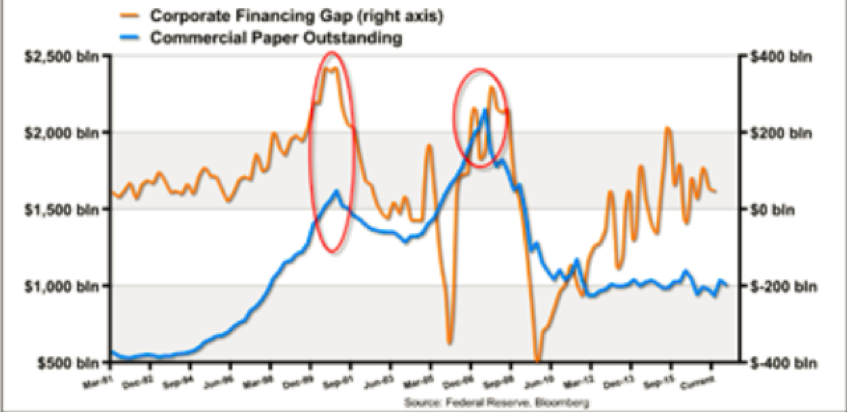

The day-to-day operations of cash flow for corporations have taken a drastic turn in that they have become more prudent about accessing the capital markets. Commercial paper is now half of what it was in 2007. The other complementary aspect to this is the corporate financing gap which ascertains when companies are not able to meet daily needs and need to access capital markets. The two high points also point to the last two significant bear markets and recessions. Though this is still above zero, it is not in warning territory and one could argue that the repatriation and tax cuts would reduce this number further.

Government: The Foo Fighters “Learn to Fly”

Run and tell all of the angels, this could take all night

Think I need a devil to help me get things right

We have now “jumped the S curve” to quote a favorite book of mine by authors Paul Nunes and Tim in that fiscal policy is now beginning to assist what monetary policy has been doing all by itself for nearly a decade. By most estimates, the corporate tax rate cuts are expected to increase corporate earnings in the S&P 500 from $10 to $14 per share. The deregulation actions have started to see a small surge in start-ups. Small business is important because of the 7.67 million businesses in the United States, almost half of those businesses are comprised of fewer than four employees.

The tax bill has the potential to have less of a positive impact on technology companies, but will have an overall positive impact on the entire corporate sector. One area to be concerned with as an investor is those smaller companies that have a lot of debt outstanding due to interest rate deductions. This possibly could push spreads of higher yield debt to lower credit ratings. Make sure you have a professional money manager in this category who can navigate the swirling seas.

Europe and the UK: Billy Joel “The Piano Man”

And the waitress is practicing politics,

As the businessmen slowly get stoned

Yes, they're sharing a drink they call loneliness,

But it's better than drinkin' alone

Europe has been one of our favorite investment destinations over the last few years. We see no reason for that to change next year. The European Central Bank (ECB) is continuing their quantitative easing, corporate earnings have been picking up, and economic activity has been matching the higher sentiment levels. This is in the backdrop of a more stressed political and cultural environment where they battle the Brexit and immigration policy to name a couple.

To put this in perspective, consider:

- The European Commission consumer sentiment number, while measured at a 0.1, is actually not seen in 17 years.

- The European Commission euro-area business sentiment is mirroring the consumer number with a nearly double surge in the last 12 months.

- The Markit Eurozone Manufacturing PMI index is at 60.6 which significantly higher than the last few years. The Services component shows similar growth patters with the most current reading of 56.5, the high point of the last few years as well.

- Jobs have grown quicker than expected as manufacturing and construction showed continued momentum.

Japan: Tom Petty “Stand My Ground”

I’ll stand my ground, won’t be turned around,

And I’ll keep this world from draggin’ me down,

Gonna stand my ground

The Bank of Japan has been stubbornly rigid in their stance to maintain their quantitative easing in spite of the frustration of deflation and anemic growth since 1989. There have been little surges of growth over that time for sure, but one must be impressed with their belief that it will ultimately work. Japan has been one of our favorite places to invest in that we see deep value playing out here. With debt-to-GDP well over 300% and negative yielding debt and no sign it’s going down anytime soon, they have insulated this often dire circumstance by insulating it inside their borders. While the fourth quarter may show some weakness after two, 2% GDP economic growth prints, we see 2018 growth rates being close to 2%.

There are several reasons to continue being bullish in Japan:

- Capital expenditures rose significantly in 2017, with the last two quarters displaying growth of over 4%.

- Their fixed capital formation over the last 20 years has been an anemic 0.04%, yet in the last two years it has been averaging almost 2%.

- One large initiative will be to continue their push to move from deflationary forces to inflate various assets and pricing to consumers.

- With the Bank of Japan owning a large percentage of the assets and debt and no requirement to liquidate, the backstop for higher asset prices appears to be in place moving forward.

China: Red Rockers “China”

Danced wind, danced with fire,

Killed the truth and called the liar,

Bleeding in its mystery when the moon began to fall,

dreamers are not all they seem

At the outset of 2017, tensions were high about a potential trade war with the United States, yet they magically grew at a 6.9% for the year. Throughout the year, the increased tensions with North Korea and the United States put diplomatic pressure on China to intervene and impose and enforce trade, however, this showed mixed results. On several occasions the meetings between the United States and China appeared to be productive yet tensions remained. There has been incessant shouting from the rooftops about an oncoming asset, real estate and debt bubble, yet the resilient markets have progressed. The pattern should be obvious, however, the initial stages of each meeting feels, the opposite appears to be the result.

We continue to see growth and asset appreciation in China, though it may come at the cost of larger swings in the next year. We have discussed the bigger macro theme of the growth of globalization as stalled out and the perceived rise in protectionism as a result beginning to influence numbers such as inflation and exports. This has been influencing China predominantly as they benefitted greatly in the 1980s through 2008, it now is not a great source of growth.

We also pointed out several years ago that Europe and China were going to begin shifting their source of economic growth from manufacturing to a balanced consumption model. We will look for more “clarity” (never as clear as you want or need) when we get the direction from the 19th Party Congress report, though we believe consumption will be a strong undertone. The surprise might be a push for environmental and economic balance which may be more for optics than substance, but it is progress none the less.

Emerging Markets: Bruce Springstein “Born to Run”

We're gonna get to that place,

Where we really wanna go

And we'll walk in the sun,

But till then tramps like us,

Baby we were born to run

After years of inconsistent and selective growth, 2017 finally saw the spark take and the economic flames were fanned. It was not only robust growth but synchronous growth around the globe. The final growth rate for 2017 across the Emerging Market universe looks to come in around 4.6%. It appears that 2018 could approach the 5% growth rate should consumption levels ascend a bit higher than anticipated. This is double the rate of growth in the developed markets, which look to come in around 2.3%. We believe the highest growth rates should continue to come from the Asian region, though the uncertainty of the North Korea situation could hinder some growth components.

One area to watch is inflation in the Emerging Markets where we are beginning to see signs of broad-based pick-ups. This is actually occurring across the globe – which we will address in a separate section. We believe this will have a negative impact on the currency and the debt returns, but we see the equity component not being impacted as greatly. Emerging Markets equities are still our favored way to invest here.

One other area which we believe could have the biggest impacts is the election calendar. The heaviest of this calendar is in South America, where the results could vary greatly. The calendars for Europe, the Middle East and Africa look to be somewhat heavy while Asia looks to have six elections. Emerging Markets will be highly sensitive to these elections as they approach, especially the more polarizing the candidates and binary solution.

Currency: Dire Straits “Romeo and Juliet”

You can fall for chains of silver you can fall for chains of gold,

You can fall for pretty strangers and the promises they hold

The prettiest stranger in the lyric above now is Bitcoin. It is it being touted as the currency that put the Federal Reserve in the hands of the people. If that reminds you of the dot-com paradigm where revenue and profits didn’t matter anymore, only business plans, you’re not alone. Or how about tulips where the fanaticism got to such levels that it is eerily similar to the evolving utopian use for bitcoins and how it will make the world a better place. As our CEO likes to say, “No one in their right mind would price their goods and services in Bitcoin as it oscillates 25% within a day.” As it is limited to 21 million coins, it is not for mass appeal and should they attempt to increase the supply substantially, the value will suffer. Beanie Babies and Tickle-Me Elmo will at least give you something to hold onto when the death of Bitcoin finally occurs.

On to more fundamentally valuable currency (note we are not saying they are not without flaws), the U.S. dollar looks to be in a bit of a trading range moving into 2018. After the consensus was sure the dollar was going to rally, they were shocked it was down almost 10% at one time. We felt it would be weak for 2017, and late in the year expected a bit of a rally. For 2018, we would expect a first half rally and a bit of weakness in the second half of the year.

The pound rallied substantially over 2017, again not a surprise. We don’t think the rumors of the recent royal engagement raising the pound’s value are valid, but hey, we’ve heard stranger things. The euro looks to be in an inverse pattern with the U.S. dollar in the next year where we would expect a little weakness in first half and a steadier pattern in the second half. For the yen, we expect it to weaken as well as most emerging markets currencies.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All