Q1 2018: Goldilocks Need Not Fear the Bear in 2018...But Her Respite Will Be More Fitful

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits2017 In Review

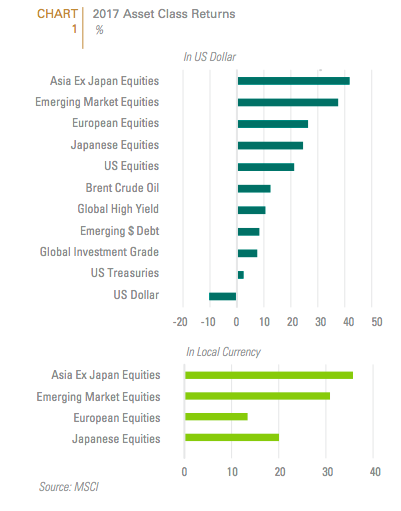

2017 was nearly perfect for risk assets. Buoyant global growth, political stability in Europe, strong earnings momentum, a weak US dollar and a steady policy makers’ hands in China fueled risk assets to extraordinary levels. Most asset classes performed well, with many delivering double-digit returns (see CHART 1). Because the US dollar depreciated by over 10% during the year, non-US investments were especially attractive for US investors.

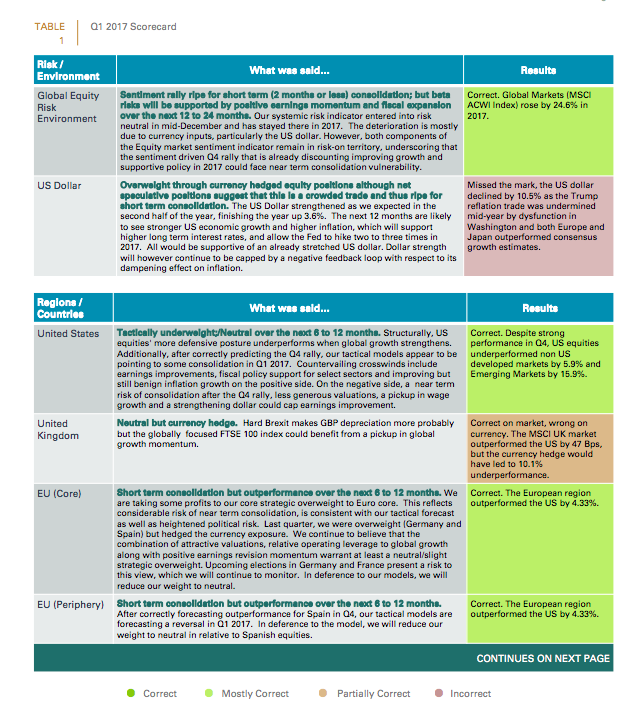

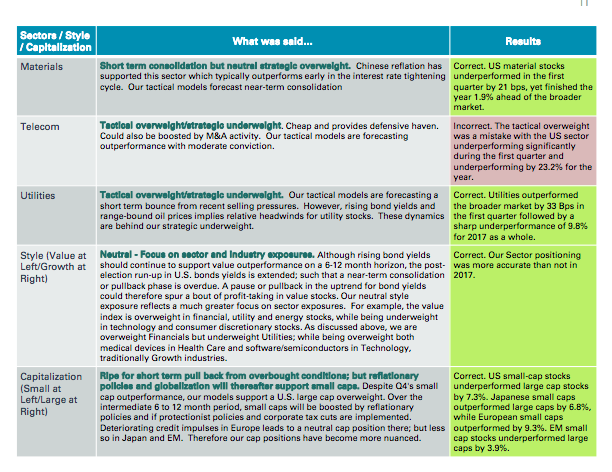

The events many worried about in early 2017 – including the election of a far-right government in France and aggressive US trade policy – didn’t materialize. The MSCI ACWI closed at record highs 61 times, and the 30-day realized volatility of the S& 500 index hit its lowest level since the early 1960s. Global equities were also boosted by falling inflation and basically flat long-term bond yields even as the economy improved while cryptocurrencies posted huge returns. Finally, 2017 was also a year of extraordinary divergences. In the U.S., the top performing sector, technology (up 38%), outperformed the worst-performing sectors, energy and telecom (down around 5%) by more than 43 percentage points. For emerging markets equities, the divergence was even more start. Four Chinese technology stocks – Alibbab, Baidu, JD.com and Tencent – outperformed the MSCI Emerging Markets index by 59%, 5%, 25%, and 75%, respectively and collectively accounted for 19% of index’s performance. For a report card on the performance of our 2017 calls, please see TABLE 1 on Pages 8-11.

For the seasoned investor, 2017’s extraordinary equity returns should give rise to concerns that positive economic news and earnings have already been discounted therefore are ripe for mean reversion. In the U.S., for example, the economic surprise index rose to a six year high during the last week of 2017 and global indices rose by 40%. According to CFRA, in years with above average new highs and below average volatility, the S&P rose the following year only 55% of the time, with an average gain of 3.1%. Conversely, in years where the dispersion between the best and worst performing sectors was high (such as 2017), the S&P 500 was up only 57% of the time in following year, with an average gain of 1.9%. Therefore, it would be reasonable to ask what additional positive economic or earnings surprises await us in 2018 that have not already been discounted? Relatedly, what risks are being underappreciated as the market plumbs to new heights? On PAGE 4 of this report, we discuss four such risks that, in our opinion, bear close monitoring.

2018: A Transition Year

As we turn the page to 2018, there are few obvious clouds on the horizon for the world economy. Business surveys suggest positive sentiment and Purchasing Managers’ indices as well as earnings momentum continue to improve. Global equities will continue to be buoyed by three critical economic locomotives – the U.S., the European Area and China – none of which face an imminent meltdown in 2018. Underpinned by this synchronized global upturn, top-line earnings growth should be able to withstand less accommodative policies by the Fed and ECB. Despite tighter labor markets and above trend growth, our base case is a modest rise in inflation, particularly outside of the U.S., anchored by the deflationary effects of technological innovation and globalized competition which limits the pass through to wages. Therefore, a key risk in the U.S. could be an upside in surprise in inflation.

Nonetheless, we expect 2018 to be a transition year. Stretched valuations and extremely low volatility imply that risk assets are vulnerable to the consensus macro view that central banks will not be able to reach their inflation targets even in the long term. We expect equity markets to begin discounting the next U.S. recession sometime in early 2018, but markers will be vulnerable in 2018 to a bond bear phase and escalating uncertainty regarding the economic outlook. Therefore, as suggested in the title of this research note, the Goldilocks markets will once again gain respite from the bear, but her rest will be somewhat more fitful in 2018.

In the U.S., tax cuts will give business outlays and overall GDP growth a modest lift in 2018. The new legislation will cut individual taxes by about $680 billion over ten years, trim small business taxes by just under $400 billion, and reduce corporate taxes by roughly the same amount (including the offsetting tax on currently untaxed foreign profits). The direct effect of the tax cuts will likely boost US real GDP growth in 2018 by 0.2 to 0.3 percentage points and boost after corporate tax profits by 3-5%. However, much depends on the ability of the tax changes and immediate capital expensing to further lift animal spirits in the business sector and bring forward investment spending. Any infrastructure program would also augment the fiscal stimulus.

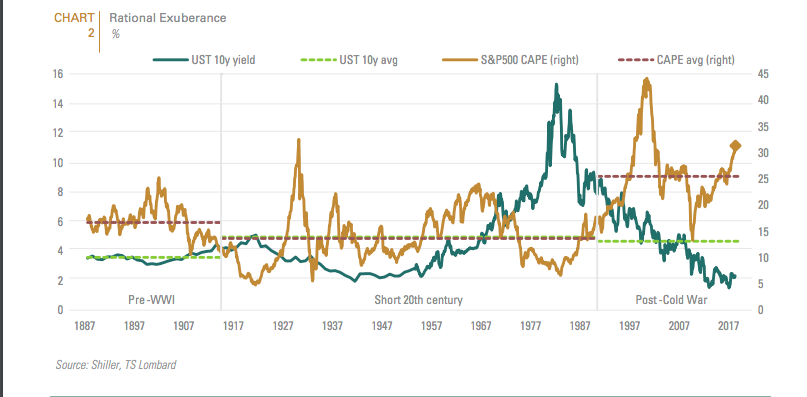

While we recognize that US equities are due for a correction, we doubt that they will plummet into bear market territory in 2018, even if the FOMC implements its interest rate hike projections, because the economic backdrop in the U.S. and elsewhere should remain healthy. Although equity valuations are not cheap by historical standards, they are still attractively valued compared to bonds. Shiller’s cyclically adjusted p/e ratio, for ex- ample, is currently more than 31, well above the post-cold-war average of 25.5. However, 10-year US Treasury yields are also well below their 4.7% average (see CHART 2 below). Moreover, growth in the US economy has tended to slow only gradually in response to higher rates. The party in the stock market has often only ended when it has become clear than the economy is about to stop growing altogether. This is the key reason why we project that the S&P 500 will only slide into bear territory in 2019.

Regionally, the Euro Area and Japanese economies registered the biggest upside surprises relative to IMF and consensus forecast. Moreover, in the Eurozone, growth has become increasingly broad-based both in terms of geography (even Italy is on the rebound) and in sector composition. Heretofore, the recovery was primarily led by export-oriented sectors but leadership is increasingly moving towards domestically oriented sectors such as financials, construction and consumer services. This is one of the reasons why continued strength in the Euro should not disrupt growth. Japan’s strong Q3 GDP performance marked the longest expansion it has experienced this century. Moderate increases in wages and inflation suggest that Japan continues to climb out of its deflationary slumber. However, inflation will remain sufficiently subdued to prevent the BOJ from significantly altering its dovish monetary stance. Equities in the euro-zone and Japan will again outperform US equities next year. Profits in both regions are less likely to be squeezed by rising wages than in the U.S.

Global emerging markets have been turbocharged by both external and internal forces. The initial spark was Chinese reflationary policies which began in late 2015 and continued into 2016, followed by a growth uptick in the U.S. and European Area as well as a weak US dollar in 2017. However, EM equities have also been supported by improving earnings momentum, rebounding export growth, and strengthening balance sheets. With their higher risk premiums, EM companies have disproportionately benefited from yield-seeking in a low-rate world. Accordingly, through September 30, 2017, EM attracted $65 billion in total inflows after approximately $155 billion in outflows from early 2013 to mid-2016.

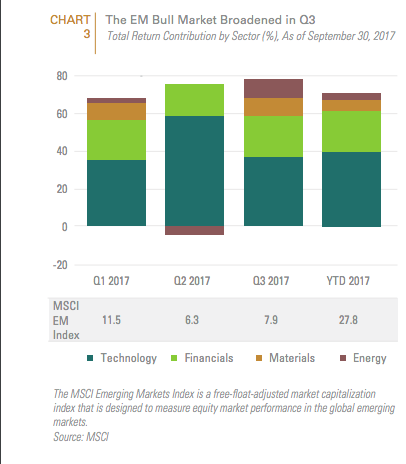

Encouragingly, the rally in EM equities appears to be broadening from one largely confined to Chinese, Taiwanese, and Korean technology companies in the second quarter to greater market interest in energy and materials companies as a result of improving economic data out of both Russia and Brazil as well as stabilizing oil prices. During Q4, earnings growth improved for most EM sectors, which should support rising Emerging Markets equity valuations (see CHART 3).

In China, a newly emboldened President Xi will further centralize economic policies by emphasizing deleveraging in the financial sector; enforcing a more intense anti-corruption campaign focused on the shadow-banking sector; reducing the regional government control over economic policy; and improving the quality and environmental sustainability of Chinese growth at the expense of its capital intensity and pace. As Xi and the top- decision-making Politburo officially stated on December 9, the coming year will be a “crucial year” for advancing the most difficult aspects of the agenda. Therefore, we expect Chinese government policy to become a headwind, after having been a tailwind in 2016-17.

We believe that Emerging Markets will continue to outperform in 2018, but will be challenged over time by China’s changing growth strategy, which will gradually remove a powerful tailwind for EM economies that most directly benefit from its historical capital-intensive growth emphasis. On the positive side, the earnings rebound for many EMs are lagging the cyclical upswing more broadly and is still supported by mostly accommodative central bank policies. At 15.7 times trailing earnings and 12.6 times forward earnings, EM equities offer increasing earnings growth, better (and rising) returns on equity, and slightly higher dividend yields compared to developed markets. Across emerging markets, companies have made inroads in reducing capex over the past two years and free cash flow margins have risen substantially. Despite these fundamental improvements, emerging markets equities continue to trade at a 25% discount to developed markets on a forward basis, suggesting that the runway for the asset class remains decent.

Among the various EM regions, despite short term growth challenges emanating from China’s economic rebalancing, we still expect Chinese equities, particularly H-shares, to outperform the EM benchmark, assuming the economy does not spiral out of control and cause a global rout. President Xi’s goal of “leaping forward” to become a global “new economy” leader in 10 years will result in heavy state sponsored subsidies and protections in renewable energy, biotech, robotics, artificial intelligence and big data. On a sectoral basis, China’s health care, tech, and consumer staples sectors (and arguably energy) all outperformed China’s other sectors in the wake of the party congress, as one would expect of a reinvigorated reform agenda. These sectors should continue to outperform. In our inaugural “Foresights” for 2018, we explore the sustainability of the Chinese tech stock rally.

Late Cycle And Capex Exposed Sectors Will Outperform

As is typical for late in the global market cycle, performance will be driven primarily by earnings as opposed to multiple expansion. With synchronized global growth ensuing for the first time since the GFC, we expect performance leadership from cyclical sectors as well those who primarily benefit from increased business capex. For the Q1 2017 Outlook, we posited that industrials and defense stocks in particular would be buoyed by both their exposure to capex and rising global geopolitical risks. Defense stocks rose by 39% in 2017 and therefore are some- what expensive. However, this sector remains a high conviction sector for us and we believe that it would be worth buying after a generalized pullback. Another high conviction sector is financials, which should benefit from improving economic activity and credit conditions globally and rising interest rates and regulatory rollbacks in the U.S. In Europe and particularly in Germany and Spain, we expect domestically oriented sectors such as construction to outperform. More broadly, technology (whose industries that are exposed to the business capex cycle) is another high conviction sector. However, this sector warrants some discrimination after its stratospheric performance in 2017.

As we begin the year, semiconductor stocks appear to provide the best value. Finally, energy is our fourth high conviction sector. Like industrials and technology, our positive view on this sector is a continuation of our 2017 view, which was based on an expected rebalancing of energy supply/dynamics. While the energy markets did rebalance in 2017 (oil prices rose from 53.75 per bbl. at the beginning of 2017 to 60.35 per bbl. at its close), energy ETFs decoupled and lagged oil prices. Going forward, we expect this discrepancy to close. Moreover, the Trump Ad- ministration’s increasingly bellicose stance towards Iran and un- fettered support for Saudi adventurism in our view adds a geo- political risk premium to oil prices which is not fully appreciated. The last two years have been remarkably benign regarding un- planned oil production outages. Iran, Libya, and Nigeria all re- turned production to near-full potential, adding over 1.5 million b/d of supply back to the world markets. This supply increase is unlikely to repeat itself in 2018, particularly as geopolitical risks remain elevated in Iraq, Libya, Nigeria, and Venezuela.

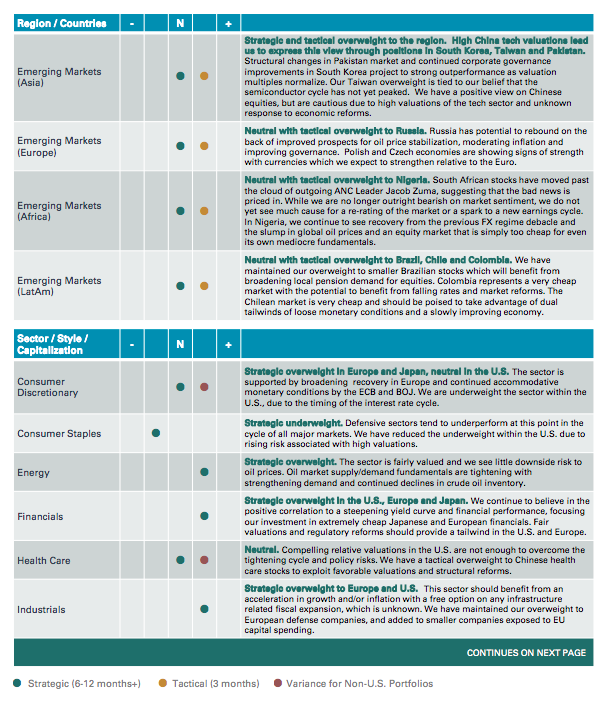

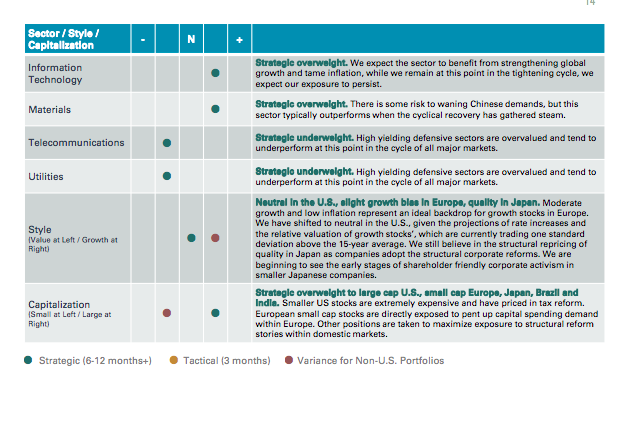

On PAGES 12-14, please find a summary of our regional and sector positions (TABLE 2).

Potential risks to an otherwise rosy scenario for global equities in 2018 include:

- Aggressive fed rate hikes

- A “melt-up” in the US dollar

- Mean reversion of the market’s extraordinarily low volatility

- Market relevant geopolitical red herrings

Below, we discuss our perspective on all four.

1. Aggressive Fed Rate Hikes

Ever since the 2013 taper tantrum, the markets and the Fed have been locked in a game of chicken in which the market has consistently (and thus far correctly) ignored the Fed’s projections. This game has continued into 2018. The FOMC is projecting three rate hikes in 2018; but financial markets have only priced in one rate hike.

It remains to be seen whether incoming chair Jerome Powell will continue Chair Yellen’s dovish and cautious approach. For the Trump Administration, continued dovishness by the FOMC along the lines of the market’s expectations would be the most politically expedient. This would prolong the current Goldilocks environment and prompt a melt-up in risk assets along the lines of 1999 in 2018.

Ultimately, the path taken by the Fed to increase interest rates will follow the trend in inflation expectations. To date, the Fed, like its counterparts in Europe and Japan, has made little progress in returning inflation to target since the FOMC started its tightening cycle. In November, the annual core CPI inflation rate fell to 1.7% from 2.3% in January 2017, with most of the drop coming from shelter, medical care and wireless services. As discussed previously, inflation has been plagued by structural headwinds emanating from both globalization as well as technological disruption. However, it is possible that the market may be underappreciating the risk of inflation surprising to the up- side. For one, economic slack is disappearing at the global level. The OECD as a group will be operating above potential in 2018 for the first time since the Great Recession. Secondly, oil prices have further upside potential. Higher energy prices will add to headline inflation and boost inflation expectations in the U.S. and the other major economies. Thirdly, focusing on the U.S., the lagged effects of dollar weakness as well as the Trump Ad- ministration’s fiscal expansionism in an economy which is close to or at full employment (see CHART 4) would also be expected to boost prices. As a result, we believe that conditions may be in place for at least 3 rate hikes in 2018.

2. A “Melt-Up” In The US Dollar

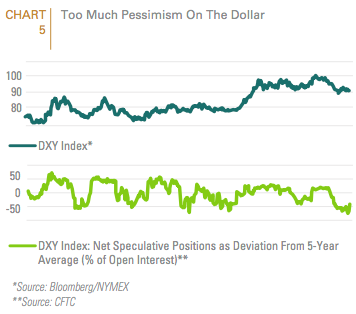

In 2017, the US dollar depreciated by 10.5%. This was a major source of pain for our portfolios as we were positioned for a rising US dollar. The weak dollar also supported EM risk assets and commodities. US dollar weakness in 2017 resulted primarily from a combination of factors. The first is that investors were massively bullish and long the dollar at the end of 2016, making the market vulnerable to disappointments. And disappointment did come with US inflation weakening and accelerating in the Euro Area. Additionally, there were positive political surprises in Europe, especially the presidential victory of Emmanuel Macron in France. In the U.S., the government’s failure to repeal Obamacare forced investors to lower expectations about fiscal stimulus. As a result, while investors were able to price in an earlier first hike by the ECB, they cut down the number of rate hikes they anticipated out of the Fed over the next 24 months. In terms of the current environment, positioning could not be more different because investors are aggressively shorting the dollar. (See CHART 5). The hurdle for the dollar to deliver positive surprises is thus much lower than a year ago. Moreover, the successful passage of the tax cut bull will help restore the Trump reflation trade which boosted the dollar early in 2017. This is why as it became evident that the tax cut bill would succeed the dollar began to show some renewed strength.

A rising US dollar would provide a less hospitable environment for emerging markets and will remove a currency-based tail- wind for US multinationals that may mute the earnings supportive tax reduction on foreign assets. We believe EM currencies as well the Yen are most vulnerable relative to the greenback. The European Area’s positive trade balance coupled with the Euro’s still reasonable valuation on a purchasing power parity basis renders that currency less vulnerable to depreciation against the US dollar.

3. Mean Reversion Of The Market’s Extraordinarily Low Volatility

Implied volatility is a mean-reverting series which can remain at depressed levels for extended periods, especially when global growth is robust and synchronized. The danger for the current market is complacency, based largely on widespread assumptions that despite globalized cyclical growth, central banks will proceed slowly in tightening interest rates and that we are close to peak rates. This assumption is in turn anchored by the belief that technological advancement in robotics and AI as well as new economy companies such as Amazon have structurally constrained inflation in advanced economies even in a full employment economy. Consequently, consensus assumptions for prolonged Goldilocks macroeconomic conditions have given rise to a “Teflon” market which has shrugged off both policy and political uncertainty. Moreover, with declining volatility, trading models encourage more risk taking, such that lower volatility enters a self-reinforcing feedback loop. Should Fed tightening exceed expectations, towards the end of 2018 or early 2019, the current extraordinarily low level of volatility could therefore quickly change from a virtuous to vicious self-reinforcing feedback loop.

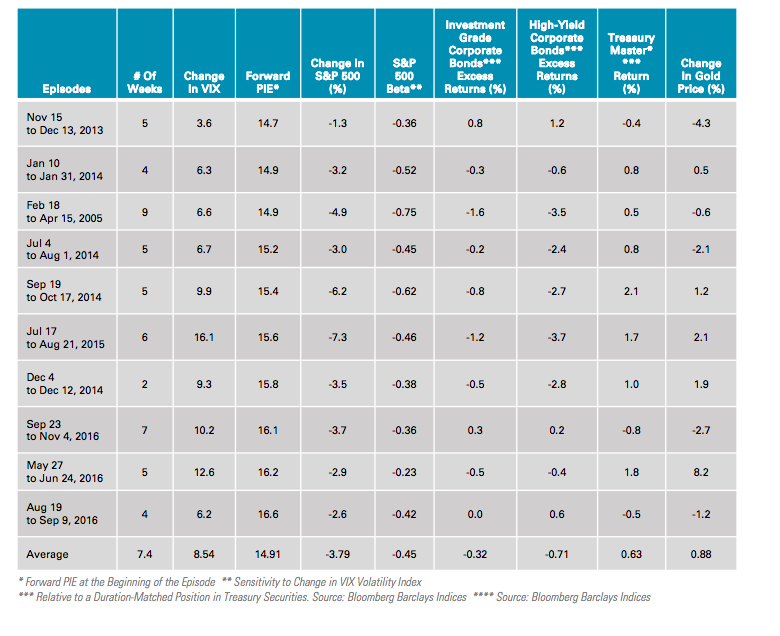

Table 3 evaluates the relationship between changes in the VIX and the return of various assets. The “VIX Beta” column shows the ratio of the percent decline in the S&P 500 to the change in the VIX. The average beta over the 15 episodes suggests that stocks fall by almost a half of a percent for every one percent increase in the VIX.

In light of currently lofty stock valuations, it is interesting to note that the equity market reaction to a given jump in the VIX does not appear to intensify when stocks are expensive heading into the shock. Today, the VIX would have to rise by about 7.5% to reach the median value, implying that the S&P 500 would correct by roughly 3.5%. Investment – and speculative-grade corporate bonds would underperform Treasuries by 22 and 46 basis points, respectively, in this scenario. The implication is that a shock that simply returns the VIX to “normal” would not be devastating for risk assets. The shock would have to be worse.

4. Market Relevant Geopolitical Red Herrings

2017 began with a mountain of geopolitical concerns which either turned out to be red herrings or were overcome by positive market fundamentals. Consequently, we have a nagging concern that market participants enter 2018 somewhat anesthetized to lurking geopolitical risks that could become market relevant.

First, the most likely red herring in terms of market relevance (as opposed to political or constitutional relevance) is the Russia collusion/obstruction of justice investigations being conducted by Congress and Special Counsel Robert Mueller. While the Mueller investigation could catalyze drawdowns in equity markets throughout the year, we believe that strong market fundamentals will present a buying opportunity should that occur. Moreover, even if the Democratic Party were to take control of the House of Representatives in 2018, impeachment proceedings are not likely to begin in 2019 and would require ratification by the two/thirds of the Senate, a decidedly uphill climb.

Similarly, last quarter, we suggested (and still believe) that the market was correct to treat North Korea related tensions as a red herring. We stated that it would require a major provocation (i.e. a direct attack on the U.S. or its allies), for tensions to escalate from current levels, reflecting a level of recklessness by Pyongyang which is difficult to fathom. However, while we believe that a full-out war is unlikely, a ratcheting of tensions and minor military skirmishes are quite likely before Pyongyang returns to the negotiating table. The most relevant market threat is to South Korean equities, which traditionally experience a pullback when tensions escalate. Thus far, each such pullback has given rise to a buying opportunity. With currently positive fundamentals (fiscal and monetary policy support, that market’s exposure to the global trade cycle, as well as corporate governance reform), we would agree with such action.

Of greater concern, is the risk of increased foreign policy adventurism as well as a ratcheting up of protectionist trade policy by the Trump Administration both to distract from domestic political troubles and feed red meat to the President’s base. It is in this context that we are keenly monitoring the recent ratcheting up of tensions with Iran. The Trump Administration’s increasing bellicosity towards Iran and their open support for Saudi adventurism risks further igniting regional tensions, particularly if Tehran feels encircled and decides to retaliate against any re-imposition of economic sanctions by Washington. Not only could Tehran retaliate by ratcheting up the insurgency in Yemen, deepening the political conflict in Lebanon, or supporting Shia dissenters in either Bahrain or even Saudi’s own eastern provinces, if pressed it could even go back to its favorite tactic from 2011: threatening to close the Straits of Hormuz. Another critical issue to consider is how the rest of the world would respond to the re-imposition of sanctions against Iran. Under IFCA, the Trump Administration would be able to sanction any bank, shipping, or energy company that does business with the country, including companies belonging to European and Asian allies. A move by the U.S. to re-open the front against Iran, with no evidence that Tehran has failed to uphold the nuclear deal itself, would throw US alliances into further flux. The implications of such a decision could therefore go beyond merely increasing the geopolitical risk premium. Saudi assets are not yet widely held by global investors, but Emirati stocks are. Abu Dhabi has thus far been supportive of the new aggressive Saudi policies in the region, and the market is largely leveraged to real estate assets which are in turn highly dependent on the stability and neutrality of Dubai as a regional entrepot. A deterioration, or perceived deterioration in that neutral status could put significant pressures on local equities.

Important Disclosures:

This report is neither an offer to sell nor a solicitation to invest in any product offered by FIS Group, Inc. and should not be considered as investment advice. This report was prepared for clients and prospective clients of FIS Group and is intended to be used solely by such clients and prospects for educational and illustrative purposes. The information contained herein is proprietary to FIS Group and may not be duplicated or used for any purpose other than the educational purpose for which it has been provided. Any unauthorized use, duplication or disclosure of this report is strictly prohibited.

This report is based on information believed to be correct, but is subject to revision. Although the information provided herein has been obtained from sources which FIS Group believes to be reliable, FIS Group does not guarantee its accuracy, and such information may be incomplete or condensed. Additional information is avail- able from FIS Group upon request.

All performance and other projections are historical and do not guarantee future performance. No assurance can be given that any particular investment objective or strategy will be achieved at a given time and actual investment results may vary over any given time.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits