SUMMARY:

- The Tale Of Tax Reform

- To Spend Or To Save? That Is The Question

- Emerging Markets Are Taking On More Debt

We’ve been doing some de-cluttering at my house, adapting to life as empty nesters. During a review of some long-forgotten storage bins, I found the very first tax return I ever filed. It listed income of less than $2,000, earned lifeguarding and shelving books at the campus library. Happily, I had a $160 refund due to me; I used the money to buy an engagement ring for my girlfriend. She said yes, in spite of the modest cost of the diamond.

Today, our tax considerations are far more complicated. That’s partially good news; we’ve been fortunate to progress from those modest beginnings. But determining our liability is not simple. The reform of the U.S. tax code that passed late last year adds a substantial degree of difficulty.

It may be many months before individuals and businesses figure out how the new rules affect them, and several quarters before we understand the cumulative impact of the bill on the U.S. economy. But we’d offer the following initial insights from what will likely be a year-long exploration.

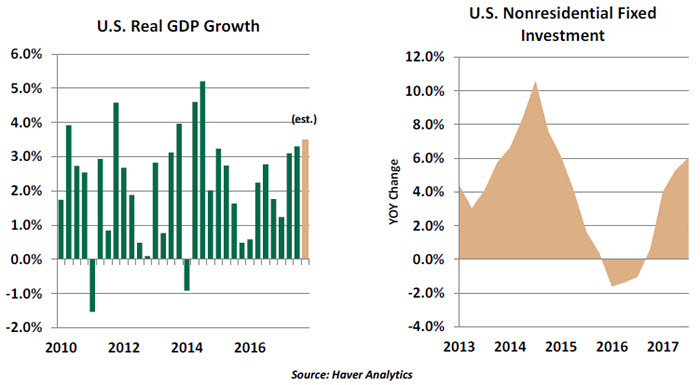

1. Whatever the merits of tax reform, the timing might be questioned. The U.S. economy closed 2017 on a very strong note; real economic growth for the final three quarters of the year proceeded at a pace of better than 3%. This is well in excess of long-run potential growth and unusually robust for an expansion of advanced age.

Consumers have been buoyed by job and wealth creation, and businesses appear to have a renewed commitment to investment. Both trends predate the likelihood of tax reform, and are therefore founded on more fundamental incentives. Some might contend that the American economy does not need additional stimulus at this time.

2. Reform will have its biggest impact in 2018, but effects will dissipate quickly from there. The attraction of immediate expensing for capital expenditures will pull some of that activity forward into 2018, but partially at the expense of future years. The diminished incentive for corporations to leave international profits overseas will deepen the pool of capital available to invest this year.

The reaction of households will occur in two stages. Those whose returns will be enhanced and simplified by the expanded standardized deduction will be the first to benefit. Reduced tax withholding should be implemented within the first three months of the year; history suggests the additional cash flow will be spent, not saved.

Those diagnosing the cross-currents of curtailed deductions, alterations to estate taxes, and the lingering presence of the alternative minimum tax may take a bit more time to arrive at an adjusted trajectory for spending and saving. Earners in the upper reaches have a lower propensity to spend, so the deferral may affect investment more than consumption.

3. Corporations will likely use their savings more for dividends than investments. Formal and informal polls suggest chief executives will use tax savings primarily to boost returns to shareholders. A study of the most recent repatriation tax holiday in 2004 found little resulting increase in either employment or investment.

Capital projects are judged on their expected returns; tax impacts are only a small part of that calculation. Most firms were enjoying a surplus of cash flow and easy access to credit before tax reform, and set their plans accordingly.

The disposition of tax reform proceeds is critical to its economic impact. Additional investment in the supply side of the economy could boost productivity and allow faster growth without inflation. Additional fuel to consumer spending could prove stressful to the factors surrounding the supply of production, which could result in higher inflation. And for that reason…

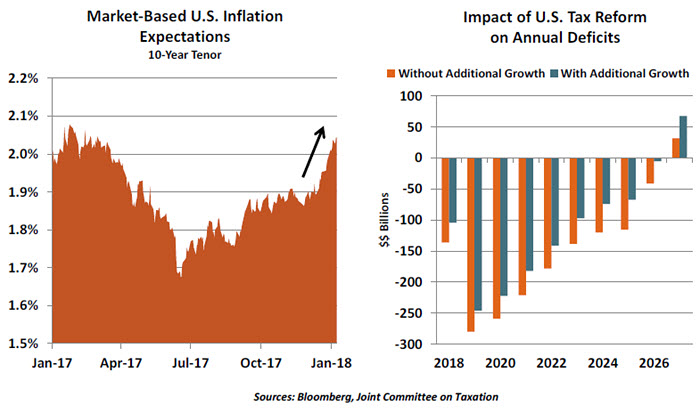

4. The reaction of markets and the Federal Reserve to tax reform may reduce its benefit to economic growth.Inflation has been quiescent across markets, even as the global expansion marches on. At one level, this is not entirely surprising; inflation is inertial, meaning low readings are usually followed by low readings. One reason: expectations of changes to price levels often become self-fulfilling.

When the outlook changes, however, it is hard to reverse. Market-based measures of inflation expectations have increased in the past few weeks, as have long-term U.S. interest rates. It is too soon to declare this a lasting development; but if the trend continues, it could be worrisome. Rates that rise faster than expected could trouble debtors (including the U.S. Treasury) and lead investors to take a fresh look at asset valuations.

5. The outlook for the Federal budget is challenging. Already challenged by slowing growth in revenue and rising growth in entitlement expenses, the fiscal position of the United States will face additional risks from tax reform. Proponents suggest updated incentives will take economic growth to a permanently higher plane; while this certainly could happen, it is unlikely. And that means deficits will deepen—by an estimated $1 trillion over the coming decade, according to the Joint Committee on Taxation.

The Reform Bill also sets up another “fiscal cliff” at the end of its ten-year life. Leadership in 2027 will be faced with the difficult choice between allowing the alterations to expire (which would restore higher tax rates and become a drag on the economy) or sustaining them (which could place the government much more deeply into debt).

As an economic forecaster, tax reform has been a nightmare. As a taxpayer, it promises to be a nightmare as well; I tried to estimate our liability under the new rules, but the calculus became too complicated. On both levels, I expect to be losing sleep for some time to come.

What to Do With a Windfall

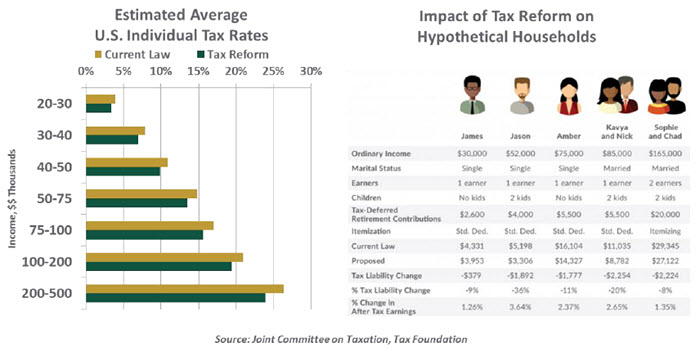

The tax reform package was ratified December 22, 2017, and IRS staff and payroll administrators immediately started working to calculate new withholding schedules. Thanks to their efforts, net pay will start to reflect tax reform as soon as next month. Actual gains will vary with each household’s individual circumstances, but most earners can expect a reduction in liability.

Changes to individual tax rates are scheduled to sunset after the ten-year window covered by the bill. Under the rational expectations hypothesis, we would expect consumers to not change their spending habits, as they would see upcoming proceeds as a windfall that would be reversed in the future. However, we have learned from experience that we spend our short-term gains. Analyses of the tax cuts championed by George W. Bush in 2001 showed that consumers tended to increase spending in response to a change in take-home pay.

The benefits of the tax reform will accrue first to lower earners, who have the greatest marginal propensity to spend. Unfortunately, these households also have the biggest deficits in retirement saving, which will need to be closed at some point. As we wrote last summer, though, people are limited in their ability to appreciate long-term consequences and are therefore prone to indulge in short-term gratification.