Global Economic Outlook - January 2018

-

- Inflation may emerge from hibernation. Growth across developed markets is in excess of long-run potential, which could stress the availability and cost of productive resources. Low levels of unemployment in the world’s largest markets may lead wage growth to break out of the range that has bound it for five years. If that occurs, central banks may have to remove accommodation more aggressively than they would prefer.

-

- Economic nationalism could restrain trade. Leaders in many countries are seeking to put their citizens first, a posture that can involve protectionism. Negotiations involving Brexit and the North American Free Trade Agreement promise to be difficult; trade friction between China and the United States is rising. Any curtailment of global exchanges would have substantial consequences for all participants.

-

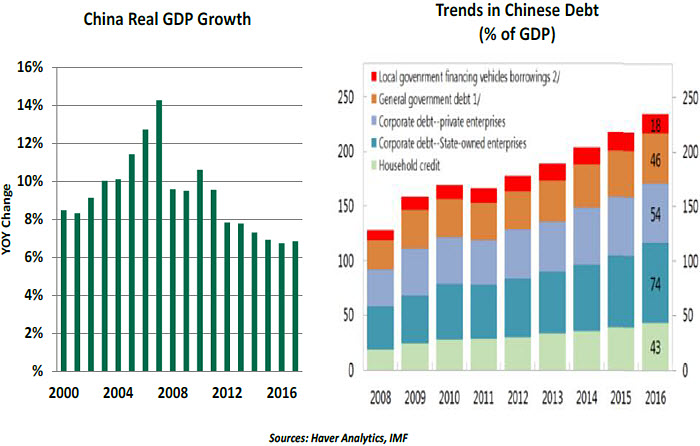

- Debt may become a limitation. Borrowing has been reduced in some sectors and countries since 2008, but has continued to increase in others. Household debt in Canada and Australia is uncomfortably high, China is seeking to better control provincial and financial leverage and government debt in many nations has risen substantially during the last decade. Investor appetite for debt has been strong, but may not remain that way.

-

- Geopolitical risks are legion. The Middle East remains volatile, ethnic and religious tension is elevated in many regions, North Korea is armed for provocation and challenging European elections are on the calendar. The potential for “event risk” is higher than normal.