Tocqueville Gold Strategy Fourth Quarter 2017

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsGold: Connecting the Dots

Gold rose 11.63% in US dollar terms in 2017, an excellent year for the metal. More important, it has been the top-performing asset since the dawn of radical monetary experimentation by world central banks in 2000 (better than equities, bonds, and other key commodities). The US dollar, anointed “King Dollar” by Larry Kudlow – a view shared by most leading economists at the beginning of 2017 – has been a bust. It suffered its worst annual performance in 14 years, down 9.84% (DXY, an index of the dollar against major currencies). Still, gold is shunned by mainstream investors. Nonetheless, our outlook for gold for 2018 and beyond is positive. What we believe is a compelling case for investing in gold now is summarized in the bullet points below. We discuss each at greater length in the following paragraphs and attempt to connect the dots from a gold perspective:

- Extreme Valuations of Financial Market Assets

- Worsening US Fiscal Position

- Rising Inflation

- Precarious Financial Market Structure

- Bullish Supply and Demand Outlook for Physical Gold

- Expected Further Weakening of US Dollar

- Gold as an Ideal Portfolio Diversifier and Risk Dampener

- Potential Boost from Bitcoin

- Brief Comment on Gold Mining Shares

Market Valuation

“Nothing sedates rationality like large doses of effortless money.” –– Warren Buffet

We believe that renewed interest in gold will be triggered by financial-market losses. Valuation is a notoriously poor aid to market timing, but there can be little debate that financial asset prices now sit at valuation extremes that have been, without exception, followed by periods of meaningful disappointment. In our view, valuation excesses signify systemic risk. Identifying the precise precipitants and timing of events that would lead to an unwinding of the “wealth” perceived by the investment consensus to exist in the current valuation mania would be pure speculation. One only needs to know that the aftermath of ultra-expensive is cheap, and that now is the time to be deploying strategies that are proven to curtail risk.

Gold has a long and unambiguous history of dampening risk. If the valuation extremes depicted in the chart below persist, or even exceed current stretched levels, gold exposure may be no worse than “dead money,” and would likely cause only a minor drag on overall returns. Because the cost and risks associated with physical gold exposure are low, we believe it can be seen as cheap insurance on a possible significant retreat from current valuation extremes.

US Fiscal Position

The federal deficit is rising rapidly late in a mature business cycle when, according to normal historical patterns, it would have been expected to decline. The deficit will rise even faster under the new tax bill. According to the Tax Foundation, the average annual loss of revenue over 10 years would be $147 billion on a static basis and $45 billion on a dynamic basis. Dynamic scoring assumes a pickup in average annual GDP growth of 1.7% over the next ten years. Even under dynamic scoring, however, revenue loss to the government is front-loaded due to accelerated tax write-offs for certain forms of capital investment.

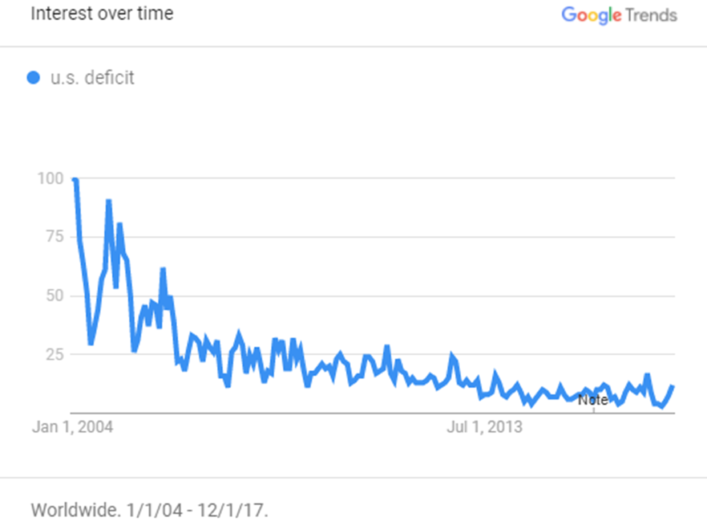

The fiscal deficit for 2017 was approximately $700 billion, and for the first time public debt surpassed $20 trillion, only 9 years after it topped $10 trillion, a level not exceeded in the previous 200 years. The math is daunting and the path geometric. However, investment world concern is at Alfred E. Neuman levels:

Searches related to the U.S. government deficit have declined by ∼90% since Google began tracking its searches, as seen on the chart below.

Even assuming current quarterly rates of GDP growth continue into 2018, we believe the deficit could rise by several hundred billion under the new tax code. In addition to lower revenues due to the new tax bill, rising interest rates would have a significant impact on the deficit as the Fed withdraws support from the bond market, as planned according to the “quantitative tightening” (QT) schedule. For each 1% increase in interest rates, the deficit would rise by $140 billion. Since 50% of the debt matures within 3 years, the impact of higher rates would quickly affect federal outlays.

Because interest and mandatory outlays under transfer programs represent 70% of total government outlays, there seems little reason to expect meaningful “cost savings” from reducing other “discretionary” categories of government spending. Between the tax cuts and an assumed 2% rise in interest rates on outstanding debt, it seems to us that a $300-$400 billion rise in the fiscal deficit, or $1 trillion+ for 2018 and 2019, is in the cards. Only extraordinary sustained multi-year economic growth would, in our opinion, alter the very negative US fiscal picture and prevent a significant, gold supportive, decline in the value of the US dollar.

The capital market impact of rapidly expanding fiscal deficits also seems quite problematic. The financial market readily absorbed net marketable borrowing by the Treasury of $593 billion in 2017. However, because of QT, treasury borrowing seems likely to rise at a substantially faster pace than the 30% increase that would result from the tax cut and a 2% rise in interest rates. The chart below shows US borrowing needs rising sharply, but does not take into account lower taxes and higher rates. We conclude that unless the Fed abandons QT, there is a strong likelihood that government borrowing will begin to “crowd out” private needs.

FED Impact on Net Borrowing

Further complicating the fiscal outlook is the fact that capital gains represent approximately 20% of all tax receipts. Even a mixed stock market, let alone a substantial decline, could add substantially to what we regard as a negative US fiscal outlook. Under such circumstances, it seems to us that considerable political pressure would be directed towards the Fed to suppress interest rates, to abandon any pretext of QT, and to revert to QE. As noted by Alan Greenspan (May 2015),“A surprisingly large percentage of US income tax receipts are tied to a rise in US stock prices. When the US stock market just stops rising…not falls, but just stops rising, that will put pressure on the receipt side of the US fiscal picture, which no one is talking about.”

Rising Inflation

The financial media have all but written off inflation as worthy of discussion. We believe that a resurgence is likely in 2018, and that it will become a mounting concern apt to have an adverse impact on valuations. In our view, the addition of stimuli (Tax Cut and Jobs Act, expanding deficits) when the economy is running at full steam will find its way into the CPI and other widely followed inflation gauges.

There are already important signs that inflation is on the rise – signs that are not being measured by the CPI. The little known ECEC (Employer Costs for Employee Compensation) rose 4.4% in Q3 2017, up sharply from 1.3% at the beginning of 2016. As noted by the astute Fed watcher Fred Kalkstein, “The ECEC requires employment counts for every category of labor” and is therefore more current than the widely followed Employer Cost Index (ECI), which uses a theoretical “sample weight held fixed during the entire time it remains in the sample, generally, ten years.” In other words, the ECEC is a better reflection of what is actually taking place with respect to labor costs than the ECI. It is telling us that labor costs are rising sharply.

Kalkstein asks,

“…how is it possible that inflation remains below 2% when…on an annualized basis, wages across the nation increased from 1.3% to 4.4%? Since wages and salaries are a major business cost, rising salaries and wages along with non-rising prices would result in lower business profits. But corporate profits are, and have been, going up. Yet product and service wage and salary costs remain stagnant? It doesn’t make sense. And that relates to inflation and interest rates.”

Only time will tell if the Fed anticipates rising inflation with more aggressive policy-tightening measures. Our guess is that it will not, and will react as it has historically: too late, with too little restraint. If we are correct, the implication would be a widening spread between nominal and real interest rates, along with a weakening US dollar and a rising USD gold price.

Precarious Financial Market Structure

Historically high financial market valuations, in our opinion, have been driven to extremes in large part because of the dominance of passive investing and machine-driven trading. Machines have no risk perception and react to inflows or outflows with robotic buying or selling. As we noted in our 2017 second-quarter letter:

ETFs and index funds are reflexive: Inflows have led to indiscriminate buying and outflows will lead to indiscriminate selling. John Bogle, founder of Vanguard, has stated that 50% of trading is controlled by ETFs. The $3 trillion ETF industry has grown nearly tenfold over the past 10 years in terms of assets under management. In our view, the greatest danger of ETFs is the illusion of liquidity. The liquidity of these surrogates in many cases far exceeds the liquidity of the underlying securities and commodities that they represent. Capital inflows into ETFs over the past 10 years have driven equity valuations. Outflows will drive valuations down, fundamentals aside.

The widespread adoption in recent years of risk-mitigating strategies such as volatility targeting and risk parity are reminiscent of portfolio insurance leading up to the 1987 market crash, according to Frank Brosens of Taconic Capital, speaking at the Fall Grant’s Conference (presentation available on the Grant’s website). According to Mr. Brosens, the lesson from the market crash of 1987 is that liquidity is a state of mind, and that complacency changes to fear more quickly than anyone expects. Current market stability near spot prices is illusory. Capital deployed on the assumption that risk can be modeled based on historic volatility and correlations between asset classes encourages leverage and risk-taking. It can therefore be systemically destabilizing. What works for risk-prevention in theory becomes destabilizing to the entire market when too widely adopted. Think Long Term Capital management, for example. As with LTCM, and again in 1987 (portfolio insurance), risk-mitigating strategies that exceed critical mass create a false sense of safety, encourage leverage, and thereby conflate downside risk.

Should equity values stray beneath a 3% decline, downside volatility is, in Brosens’ view, spring-loaded. He referred to the eerily low volatility displayed by the Nikkei average in 1989 prior to the subsequent crash and loss of 80% of value. The potential for reflexive selling could be even greater than in 1987 because of the potential outflows from passive instruments such as ETFs and index funds, which were not a factor in the ’87 meltdown.

We agree with the comments of our colleague Simon Mikhailovich (of Tocqueville Bullion Reserve) that the asset-management industry has undergone a qualitative transformation that almost guarantees large-scale capital flight from equities in the event of a sudden or prolonged market downturn:

Any industry that turns on its customers, and the asset-management industry has, is vulnerable to disruption. After decades of underperformance, conflicts of interest, and egregious excess, many investors are forsaking active managers for passive strategies, which rely on dubious and unproven financial technologies, such as ETFs, robo-advisory software, levered derivatives, etc. These new strategies carry significant risks that are being widely ignored so long as the markets keep making new highs. However, having moved away from the relationship to the transactional model, the new strategies do not engender loyalty and are vulnerable to mass defections whenever the markets reverse and reveal their embedded weaknesses.

Bullish Supply and Demand Outlook for Physical Metal

In the real world, physical gold is in short supply. We believe that mine production has peaked out and is likely to decline for the next three to five years. Even an unexpected sharp price increase would not change the glide path of forward production because capital, environmental, and political headwinds are lined up against building new mines. Demand, notwithstanding minor year-to-year fluctuations, is on a steady growth path. Only the continual liquidation of above-ground inventories stored in London or other Western vaults over the past several years has prevented the mismatch between supply and demand from driving the gold price higher.

Gold Supply

Unlike physical, gold is abundant in the synthetic world because physical bars are replicated almost infinitely due to the magic of a system known as hypothecation and rehypothecation. Bets on the gold price are expressed via futures contracts on COMEX and over the counter between financial institutions with big balance sheets. The bets are settled in cash, and almost never involve physical metal. In Western capital markets, synthetic gold is actively traded. In Asia, only physical gold is accepted. The burgeoning Shanghai Gold Exchange requires 100% backing of futures contracts by physical metal. We believe that the pricing power and credibility of COMEX and the surrounding bullion banking system will erode due to the migration of physical gold to India, China, and other Asian nations. In addition, the emergence of platforms such as the recently launched Allocated Bullion Exchange (ABX) in Australia, which requires full backing of physical gold, will in our opinion chip away at synthetic gold trading. We believe that relocation of active gold trading on platforms that require full gold backing will lead to improved price discovery and higher gold prices.

Expected Further Weakening of the US Dollar

Because we expect inflation and the fiscal deficit to rise, we expect the dollar to weaken further in 2018. Gold and silver are unique among all commodities because they trade as a foreign exchange (FX) cross or pair trade. If one follows the movements of DXY (US Dollar Index – a basket of currencies), euro, and yen vs. the dollar, there is typically high correlation over the short term. A strong DXY is bad for gold and vice versa. Synthetic gold is a convenient and liquid market in which to mobilize large pools of capital to express macroeconomic views. The basic idea is that gold prices are heavily influenced by speculative pools of capital. These pools are deployed across several asset classes in synthetic form. They can easily be calibrated or rigged to achieve profitable short-term commercial outcomes for option positions held by financial institutions and hedge funds, without regard to longer-term fundamentals for either the metal or capital markets.

Virtually no physical gold changed hands during headline-making shakeouts in the gold price during 2017. In our view, the shakeouts were a component of trading algorithms thought up by macro traders as the core component of the world-view that a resurgent US economy would be wrought by the pro-business policies of the Trump administration. A strong US dollar would be the inevitable offshoot of a resurgent US economy. The Appendix contains several examples of synthetic raids that relied upon naked short-selling (selling something not in the possession of the seller). In our view, the appendix clearly shows deliberate efforts to drive the gold price down. (For a more granular look at how synthetic gold raids are orchestrated, see our 1/7/16 website article, “Paper Gold: Utopia for Alchemists”.) Despite multiple orchestrated post-Trump election “bear raids,” the gold price achieved a strong increase in the past year and managed to survive the application of the Trump myth to all asset classes.

It is noteworthy that, notwithstanding a very “dollar bullish” outcome in terms of the success of the Trump agenda – including the tax bill and significant deregulation – the trade-weighted dollar is slumping. We wonder whether this anomaly should be taken as an early warning that other cracks may soon appear in the bullish façade of the investment world.

Gold: Efficient Diversification and Effective Risk Mitigation

In our opinion, CIOs of university endowments, pension funds, and foundations need to revisit gold. An allocation to gold would reduce downside exposure during periods of market stress and would, we believe, also result in significant outperformance over a longer period of time. Instead, many of these presumably elite investors have resorted to exotic, fee-laden, risk-mitigating strategies as discussed in the previous comments on market structure. Few, if any, appear to have investigated a gold strategy to diversify and moderate overall portfolio risk.

Below we show that a 10% allocation to physical metal employed since 1987 would have resulted in substantial outperformance versus a “traditional” allocation of 60% equities and 40% treasuries. In this case, the inclusion of gold was a simple “buy and hold,” and did not employ complicated trading strategies.

Gold Performance During Uncertainty

Gold exposure is far less expensive than exotic strategies designed to protect capital. In fact, gold has outperformed equities, bonds, and key commodities since 2000, the dawn of radical monetary experimentation by world central banks (chart below). Yes, gold has no internal rate of return and there are storage charges to boot. However, the storage charges are miniscule relative to fee structures of complex risk-mitigating “products.” In addition, at ultra-low interest rates, the return on cash or treasuries is nothing to write home about.

Gold has outperformed equities, bonds, and key commodities since 2000

Source: Bloomberg

A Boost from Bitcoin

Distrust of money-printing by world governments is a key part of the rationale for Bitcoin and other cryptocurrencies. In this sense, cryptocurrencies attempt to mimic one of the key attributes of gold: a liquid real asset with no counterparty risk. We share the millennial distrust of fiat paper, welcome the advent of digital currencies, and understand why governments view them with great concern. We view cryptocurrencies as contributors, and possibly as accelerants, to the long-term undermining of all paper currencies. We see them as allies of gold and threats to fiat currency, not as an existential threat to the metal, as they have been so frequently portrayed.

Bitcoin, in our view, manifests the rejection by private citizens of centralized government authority. Governments without exception have sounded the alarm. Andrew Bailey, head of the UK Financial Conduct Authority, told the BBC that neither central banks nor the government stood behind the “currency” and therefore it was not a secure investment. As noted by 13D Research (12/7/17), “The worst nightmare for central banks is a rising price of gold because it means they are behind the curve, bond yields will rise, and people are losing confidence in paper money.” That nightmare only worsens as acceptance of cryptocurrencies rises.

Now that the CME (Chicago Mercantile Exchange), through which all futures contracts enjoy full US government credit backing, has opened trading in Bitcoin futures contracts, the sledding for cryptocurrency prices could become difficult. The recent 40% price break in Bitcoin and other cryptocurrencies coincided with the launch of futures trading that began in mid-December 2017. The opening of futures trading on the CME created an organized platform on which to mobilize a synthetic supply of the cryptocurrency. Previously, Bitcoin was a one-way market, with few natural sellers and only 3600 new Bitcoins mined per day, or 1.3 million per year on a base of 16.5 million in circulation (BBC, 12/17), vs. a theoretical limit of 21 million for total supply. Through the sorcery of large financial institution balance sheets (without any Bitcoin inventory), a synthetic supply materialized overnight on the Merc. Enter the CME, and there was suddenly a two-way market in which large financial interests could profit from volatility, break the cockiness of the most strident advocates, and perhaps even dampen the price surge.

Cryptocurrency price behavior, in our opinion, is a distraction from the real threat to fiat money, the blockchain technology that makes cryptocurrencies possible. Blockchain in the long run will make it possible to settle transactions between private parties outside of the banking system and away from the eyes of government tax authorities. An obvious shortcoming in the utility of Bitcoin to function as a currency and medium of exchange (an essential attribute of money) is the extreme price volatility exhibited to date. However, and in our view, a gold-backed cryptocurrency is feasible and is likely to be launched within the next year or two. A marriage of real money to blockchain technology would, in our opinion, be the worst possible nightmare for advocates of fiat, centralized ledgers and the existing banking system.

A Kind Word for Gold Mining Stocks

The underperformance of gold mining shares relative to the metal price in 2017 is uncharacteristic of the normal relationship. For example, gold mining shares rose 8.13% (basis XAU) in 2017 vs. an 11.63% increase in the metal price. We believe this is attributable to poor money flows into the precious-metals sector and competition from strong equity returns just about everywhere else. We believe that if unexpected dollar weakness and gold strength persists into 2018, mining shares will return to favor and show significant outperformance relative to the metal. In our investment portfolios we continue to focus on select equities that have continued to add value on a per-share basis despite the drought of interest by generalist investment funds.

The Compelling Case for Gold Now

In our opinion, when the make-believe world of synthetic gold, algorithmic trading, ETFs, fake interest rates, and passive investment collide with the realities of an uncontrollably rising budget deficit and mismatches between surrogates and underlying assets, gold (the real asset) will benefit. To us, it is obvious that the US and other Western governments are simply printing money to service their own debt. When is the tipping point of public recognition of these facts? Perhaps as soon as 2018 or 2019. The catalysts will be higher inflation and interest rates, and lower financial-market valuations. There is no way to predict the moment, but it seems to us that an eventual loss of confidence in paper currencies, including the US dollar, is inescapable, and most likely coming sooner rather than later. It is not, in our opinion, too soon to embrace exposure to gold.

John Hathaway

Senior Portfolio Manager

© Tocqueville Asset Management L.P.

January 3, 2018

This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be construed as investment advice. No representation is made concerning the accuracy of cited data, nor is there any guarantee that any projection, forecast or opinion will be realized. References to stocks, securities or investments should not be considered recommendations to buy or sell. Past performance is not a guide to future performance. Securities that are referenced may be held in portfolios managed by Tocqueville or by principals, employees and associates of Tocqueville, and such references should not be deemed as an understanding of any future position, buying or selling, that may be taken by Tocqueville. We will periodically reprint charts or quote extensively from articles published by other sources. When we do, we will provide appropriate source information. The quotes and material that we reproduce are selected because, in our view, they provide an interesting, provocative or enlightening perspective on current events. Their reproduction in no way implies that we endorse any part of the material or investment recommendations published on those sites.

Appendix

We have included daily charts of some of what we believe to be the more egregious 2017 orchestrated bear raids below. The commentary is from Zero Hedge and reflects the opinion of the commentator at the time of the event. It does not necessarily reflect the opinion of Tocqueville.

Flash Crashes

3/28/17

6/26/17

7/6/17

First it was gold last week, then it was half of Nasdaq on July 4th, and now it’s silver that is taking it’s turn in the ‘glitch’ camp. As Japanese markets opened tonight, spot silver prices crashed around 6% in a few seconds only to instantly rip back higher…

7/19/17

The last time gold plummeted by just over $30 per ounce (dragging down silver and bitcoin with it) and resulted in a crash so furious it led to a “Velocity Logic” market halt for 10 seconds, was on January 6, 2014. Many said this was just perfectly normal selling, although we explicitly said (and showed) that it was a clear case of an HFT algo gone wild (following an order to do just that and slam all sell stops) when someone manipulated the market and repriced gold substantially lower.

Precisely one month ago, some 18 months after the incident, the Comex admitted as much, when it blamed the collapse on “unusually large and atypical trading activity by several of the Firm’s customers and caused the mass entry of order messages by Zenfire, which resulted in a disruptive and rapid price movement in the February 2014 Gold Futures market and prompted a Velocity Logic event.” Curiously despite the “errant” order, gold did not rebound because the entire purpose of the selling slam was to reset the prevailing price far lower. This is what the Comex said in Disciplinary action 14-9807-BC:

Pursuant to an offer of settlement Mirus Futures LLC (“Mirus” or the “Firm”) presented at a hearing on June 16, 2015, in which Mirus neither admitted nor denied the rule violations upon which the penalty is based, a Panel of the COMEX Business Conduct Committee (“BCC”) found that it had jurisdiction over Mirus pursuant to Exchange Rule 418 and that on January 6, 2014, Mirus failed to adequately monitor the operation of its trading platform (Zenfire), and connectivity of its trading system (Zenfire) with Globex. This failure resulted in unusually large and atypical trading activity by several of the Firm’s customers and caused the mass entry of order messages by Zenfire, which resulted in a disruptive and rapid price movement in the February 2014 Gold Futures market and prompted a Velocity Logic event.

The Panel found that as a result, Mirus violated Rules 432.Q. (Conduct Detrimental to the Exchange) and 432.W.

We bring this up because moments ago, just before 9:30pm Eastern time or right as China opened for trading, gold (as well as platinum, silver, and virtually all precious metals) flashed crashed when “someone” sold $2.7 billion notional in gold, resulting in a 4.2% or about $50 to just over $1,086/oz, the lowest level since March 2010.

7/19/17

8/30/17

After the shenanigans in US mega-tech stocks over the last two days and the seemingly well orchestrated melt-up to pre-J-Hole levels in the dollar, why should anyone be surprised that ‘someone’ decided to try to sell $1.1 billion notional into the Asian open…

9/4/17

While stocks have been limping higher since around 2am ET (following headlines on an imminent ICBM launch) they remain lower from Friday’s close:

9/4/17

11/3/17

11/8/17

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits