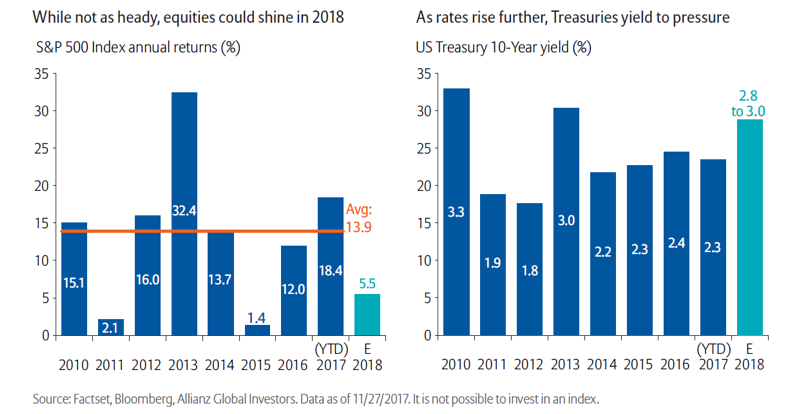

As we look back on 2017, investors are struck by the resiliency of US equity markets, which reached all-time highs in 10 out of 12 months of the year; they also sustained remarkably low volatility across risk assets. The markets were driven by several key themes, including a second-half rebound in economic growth (alongside a global growth rebound), corporate earnings resiliency (S&P earnings up 10.2% in 2017 through December 11), and a continuation of “low and slow” rates from Janet Yellen and the Federal Reserve. And of course, there was the ongoing fiscal saga of US tax reform, which was another source of optimism as investors fed on hopes of corporate and individual tax cuts.

For 2018, we remain cautiously optimistic on US equity market returns. While we do not anticipate a repeat of 20% plus returns, we believe the markets could yield mid-single digits in 2018, and we continue to see above-potential real GDP growth around 2.5%. In addition, we see rates continu- ing a slow march upward toward 3.0% (10-year Treasury yield), and curve flattening continuing to be an ongoing theme as the Fed raises rates. We remain cognizant that global demand for

US Treasury bonds in a rising rate environment can continue to pressure yields, particularly when sovereign yields in major economies such as Europe and Japan continue to remain low.

As we are well into our eighth year of a bull market in the US, our antennae are now firmly attuned for signals of a turn in the cycle. While we believe we are in the final stages of this economic cycle, history has shown us that equity markets could perform well at this stage, as the Fed continues its rate-hiking path and there is no sign of a US recession in the next 12 to 18 months. We recommend continuing to remain long risk going into 2018, with an eye on the following four themes:

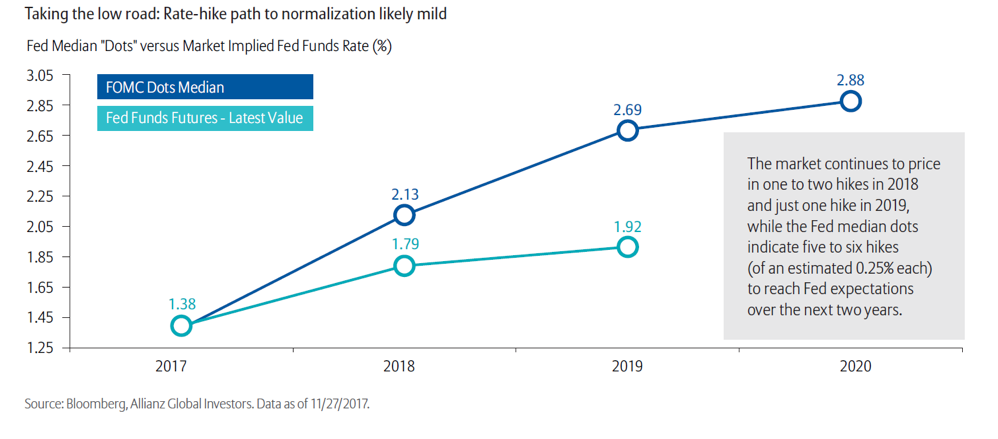

1. The Fed rate-hike cycle should continue: Beware of inflation

With Jerome Powell now established as the new Chair of the Federal Reserve, and Janet Yellen stepping down in February, Mr. Powell will be faced with the challenge of continuing the rate hiking and balance sheet tapering begun by his predecessor.

We continue to believe that one rate hike in December, and three hikes in 2018 is the most likely normalization path for the Fed over the next 12 months. Given the current benign economic backdrop and financial conditions remaining accommodative, the Fed has an opportunity to continue normalization and regains a valuable policy tool (cutting rates) in the case of a downturn going forward.

We do see two sources of potential inflation upside surprises, including 1) wage growth accelerating, and 2) tax reform creating inflationary pressures. With the unemployment rate at its lowest post-crisis (and rapidly approaching levels below 4%), we believe wage growth will emerge more prominently in 2018. In addition to wage inflation, tax reform could also create inflationary pressures, as cash comes back into the US economy, both from repatriation and lowered corporate tax rates. These potential inflationary pressures will keep the Fed on high alert to ensure it is not behind the curve. As inflation expectations rise, we believe the markets will begin to price in Fed rate hikes, pushing interest rates up.

2. Tax reform is now a reality: Find the winners and losers

Now that the drama of passing tax reform is nearly behind us, investors have the job of rolling up their sleeves and determining which of their investments benefit from the new tax reform bill. Generally, we believe domestically oriented firms will benefit most from the reduced corporate tax rate, which would favor value and small and mid-cap positions from a style and size perspective. We also see the technology and health care sectors as potential beneficiaries from the repatriation tax legislation, although it remains to be seen whether these funds would be used for capex/growth or share buybacks/dividends.

As the euphoria around tax reform subsides, investors may also begin to consider the longer-term implications of tax reform, namely the increase in the deficit and the potential exacerbation of income inequality. Deficit spending over time can in theory “crowd out” productive government spending, as the government will have to pay down debt rather than invest productively – ultimately reducing growth rates. We believe this will be an overhang on tax reform, and we have seen President Trump start to discuss welfare reform, perhaps as a potential offset to deficit spending. In addition, there is a subset of middle- class Americans that will end up not benefiting from tax reform, while the wealthiest Americans will benefit from the repeal of legislation like the AMT and estate tax. These are two downside scenarios of tax reform that we will be monitoring closely, as they may continue to impact politics and populism in the US.

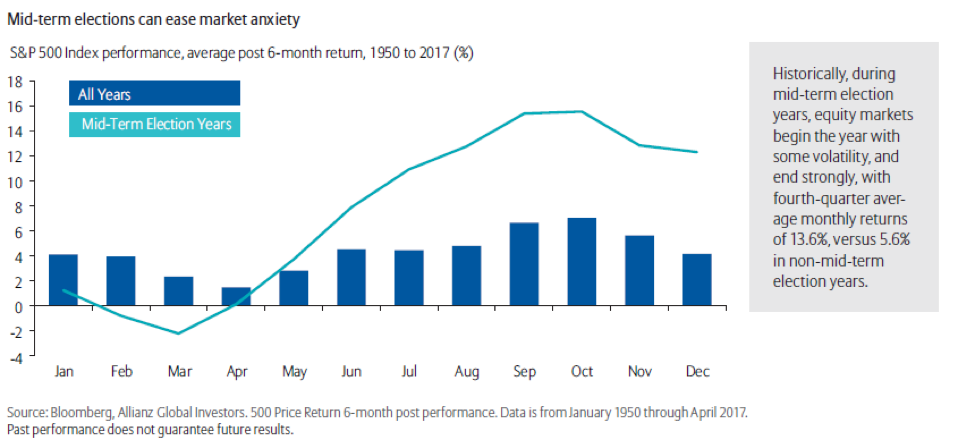

3. Politics and geopolitics: Mid-term elections in the US could provide a bump

In recent quarters, the stock market has shrugged off politics and geopolitics, natural disasters, terrorist activity and ongoing scandals. This is not surprising, as historically these events have not had a material impact on the economy. However, the US is facing important mid-term elections on November 8, 2018. Historically, after these elections the S&P 500 Index rises more than average, regardless of the winner, as market uncertainty is lifted.

Prior to November, however, the elections remain an overhang on the markets and a source of potential volatility. Thus, as we look at the path for equities in 2018, we could envision a scenario where markets are more volatile in the quarters prior to the election, and then end the year with momentum.

4. A return to volatility (finally): The case for active management and long-term views

With the Federal Reserve removing liquidity from the system, some global central banks beginning their tightening cycles (e.g. BoE, ECB, BoC), and tax reform now a reality, we believe volatility in the markets may finally reemerge. As rates begin to move back upward, investors are once again presented with options beyond equity markets to gain a reasonable return. Increased volatility typically brings lower correlations and higher dispersions in risk assets, making it more imperative for investors to shift some of their assets to active management, as market winners and losers become clearer.

Longer term, we believe investors will need to incorporate themes such as an ageing US population (and demographic shifts from the baby boomer to the millennial generation), as well as emerging disruptive technologies, globally and across sectors, into their investment portfolios. We also see a shift in trend toward environmental, social and governance (ESG) investing, particularly in the form of “integrated ESG,” which encourages portfolio managers to engage actively with corporations and has empirically seen favorable returns. We believe it is imperative that investors be mindful of these trends as they develop their risk portfolios.

Finally, as the Fed continues its normalization in 2018, it is also important to keep in mind that 10 of the last 13 Fed cycles post-WWII have ended in recessions. And it is during these recessionary periods that equities tend to enter bear market territory. As noted, the US is inching closer to a turn in its cycle, ahead of many of its developed-market peers, and we believe investors should begin to align themselves with global and active strategies that can provide absolute return, global exposure, inflation protection and yield, which over the next 12 to 18 months should become a bigger part of all diversified portfolios.

Follow Us on Twitter

For more investment insights and market perspectives from our global research network, follow @AllianzGI_US on Twitter or visit us.allianzgi.com.

Important Information

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, us.allianzgi.com, 1 800 926 4456.

340654