As 2018 approaches, investors may want to take some time to reexamine their high-income strategies. We’ve got some advice: Be selective. Be diversified. And, perhaps most importantly, be patient.

If you’re an income-conscious investor, abandoning a high-income strategy isn’t an option. But simply setting a course and sticking with it, irrespective of changing conditions and valuations, can lead to trouble. That’s especially true at a time when yields are low and fixed-income assets look expensive.

In situations like these, patience really is a virtue. Investors should resist the urge to reach for yield, and concentrate on maximizing opportunity and reducing risk. A global, multi-sector strategy can provide access to multiple sources of income and return.

But it’s also important to take a broad sector-by-sector approach to the market, followed by a deeper dive into individual securities. This can help investors identify and avoid areas of the market where risk appears to exceed potential return.

Here are a few things to think about as the new year nears:

Get into a European State of Mind

High-yield corporates are an important component of any high-income strategy. But valuations are high on both sides of the Atlantic, so investors have to pick their spots carefully. In particular, we see value in subordinated European financial bonds. These bonds offer attractive yields to compensate investors for the risk they’re taking by buying a bond that’s further down the capital structure. But we think a stricter regulatory environment significantly reduces the probability that these types of securities will default on their obligations.

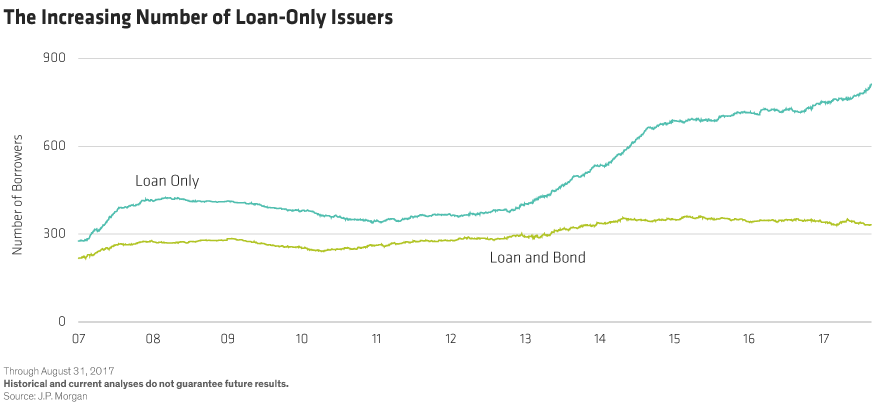

Contrast that with US high-yield bank loans. One of the reasons they’ve been in high demand is their senior position in the capital structure; if a borrower defaults, loan investors usually get more principal back than bond investors. But more than half of loan issuers today have no unsecured bond debt cushioning their balance sheets (Display). That means no cushion for loan investors should these companies run into trouble. Being subordinate in European high yield looks more attractive than being senior in US bank loans.

Finally, European high yield may be especially attractive to US-dollar–based investors, who hedge the currency exposure back to the dollar. This is because short-term rates in the US are much higher than in the euro. By hedging back to dollars, an investor can pick up more than 200 basis points in yield.

Stay Exposed to US High Yield—but Be Selective

While the Fed is likely to keep hiking rates in 2018, policy will probably remain relatively accommodative. That’s why we don’t expect the US high-yield default rate to rise too far above 2%. Typically, default rates don’t pick up until a year or two after the US fed funds rate has peaked.

Even so, investors who skip their credit homework do so at their own peril. High-yield credit quality and valuations vary widely across sectors. In 2018, a flexible and tactical investment strategy is a must for those who want to uncover value and minimize risk.

To see what we mean, let’s look at three different sectors.

Retail: The rise of Amazon and the erosion of pricing power at brick-and-mortar retailers isn’t a new story. US consumers are spending, but they’re doing it online. That’s a problem for many highly leveraged retailers who haven’t properly invested in technology and online capabilities.

But things could get worse in 2018. One reason: pending tax legislation is likely to cap the deductibility of interest payments on corporate debt. That will hurt the most highly leveraged issuers most, including most CCC-rated companies. Higher-rated, investment-grade retailers, on the other hand, have less debt and will benefit from a lower corporate tax rate. That will further widen the gap between the winners and losers in the sector.

Healthcare: The story here is a more nuanced one. Among pharmaceutical firms, drug sales are increasing but prices for generics continue to decline. Branded drug prices are still rising, but at a much slower pace. But valuations are reasonable and most companies’ balance sheets appear strong enough to withstand a potentially stressful year.

Healthcare service providers, meanwhile, may face some pricing pressure in an environment where insurance companies are increasingly integrating vertically by buying service providers such as ambulatory-care companies and physician groups. There’s value here, but finding it calls for detailed research and a selective approach.

Homebuilders: These issuers stand to benefit from continued improvement in the US housing market, and several companies in this sector may even see their credit ratings rise into investment-grade territory in the years to come. Credit spreads—the extra yield credit assets offer over comparable government bonds—are generally wider than those on similar companies in other sectors, providing a potential pick-up in yields.

Making Room for Emerging-Market Debt

Emerging-market (EM) currencies had a volatile 2017, but valuations are still broadly attractive. What’s more, local-currency–denominated EM debt offers much higher inflation-adjusted, or “real,” yields than do comparable developed-market bonds.

There’s probably more market and political volatility to come in 2018, so investors need to be selective. If the Fed tightens US monetary policy more quickly than expected and the US dollar appreciates, some EM assets could struggle. But we still see plenty of opportunity in this sector, particularly in countries that have exhibited a commitment to political and economic reform.

Markets may be more volatile and less predictable in 2018 than they were in 2017. But some things never change, no matter the year: investors need their bonds to generate income. There are risks on the horizon. But there are opportunities, too. Just be patient—and don’t limit yourself to a single sector or region.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

© 2017 AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein