Key themes

Room to run: We see a synchronized global economic expansion with room to run in 2018 and beyond, albeit with less scope for upside growth surprises. We believe markets are underestimating the durability of this expansion.

Inflation comeback: We see U.S. core inflation rising and, as a result, potentially higher U.S. yields ahead. However, price pressures elsewhere are minimal, which could herald greater divergence in policy and rates.

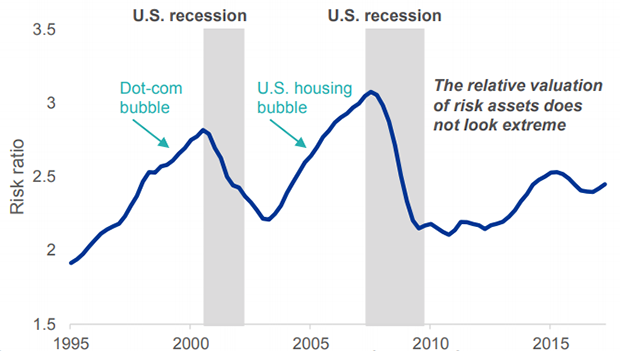

Reduced reward for risk: It was a near-perfect year for risk assets in 2017, but the road ahead looks more challenging. The valuations of all risk assets have risen, but we believe investors could still get compensation for taking risk in 2018.

Market views

We prefer to take economic risk in equities over credit given tight spreads, low yields and a maturing cycle. We expect increasing profitability to power equity returns, especially in Japan and emerging markets (EM). The steady expansion supports the momentum style factor, albeit with potential for reversals; we see the value factor as a diversifier. We prefer inflation-protected over nominal bonds, especially in the U.S.

Not so exuberant

BlackRock U.S. risk ratio, 1997-2017