Summary

- How Should The Fed React To Tax Reform?

- The Inflation Puzzle Persists

- Financial Conditions Are A Growing Concern

The U.S. Federal Reserve will conduct its final monetary policy meeting of the year next Tuesday and Wednesday. It is practically a foregone conclusion that short term rates will be lifted for a third time this year; the U.S. economy has been strong, and Fed officials have been dropping hints of an impending tightening for a couple of months. It looks very much like the Federal Open Market Committee (FOMC) will end up following the path of short-term rates that appeared in its forecasts a year ago.

The Fed also delivered on its promise to begin reducing its balance sheet, with billions of dollars in bonds returning to private hands each quarter. Communication with markets has been handled virtually flawlessly; there have been fewer false starts and surprises for investors than there were in 2016. A smooth leadership transition is underway. And while the Fed is still operating short-handed, recent nominations to the Board of Governors suggest that help is on the way.

But the task of normalizing monetary policy will not be easy from here. Recent events suggest the Fed may not be able to continue moving at the slow, measured pace it might prefer. Here is a matrix analysis of the factors that are likely to tell the tale in 2018.

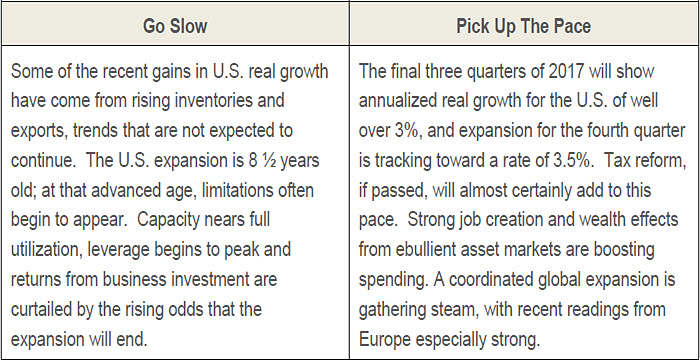

Economic Growth

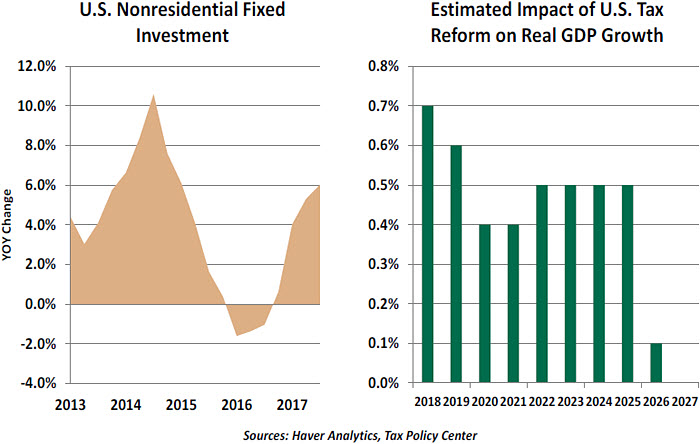

The U.S. expansion may be mature, but it is not acting its age. Even prior to the enactment of tax reform, business investment had resumed a powerful upward trajectory, providing an ingredient that had been absent from the growth picture for three years. The list of potential 2018 tailwinds is a long one, suggesting this cycle could get stronger even as it approaches a record length. (The current benchmark is the 10-year expansion that lasted from 1991 until 2001.)

Our take on tax reform can be found here. The likelihood of passing legislation prior to year-end has risen sharply, with House and Senate conferees hard at work reconciling the proposals passed by each chamber. The political urgency behind the process is likely to propel the measure to passage in the next three weeks.

In essence, tax reform will act as a substantial fiscal stimulus, with deficits projected to expand by more than $1 trillion over the coming decade. The influence on growth will be front-loaded, as corporate tax reduction will lead to a windfall that can be used to invest or reward shareholders. (Either is helpful to economic activity, albeit through different avenues.)

Up to this point, the Fed’s projections do not appear to have reflected this influence; it will be interesting to see whether the summary forecasts released next Wednesday afternoon show a noticeable upward adjustment. And if they do, alterations to the group’s paths for inflation of interest rates will be warranted.

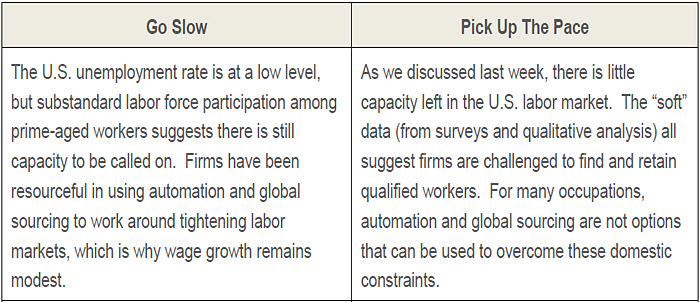

Employment

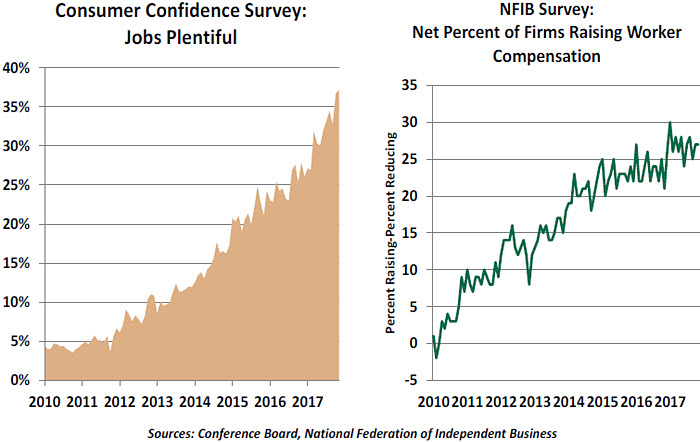

The November employment report was a microcosm of the year as a whole. It described tremendous job creation: 228,000 new positions were added, post-crisis lows were reached in broad measures of unemployment and labor force participation rates improved. Surveys and anecdotes suggest advancing labor market tightness.

The bad news, at least if you are a worker, is that wage growth remains subdued. The failure of compensation to respond even modestly to advancing utilization levels in the labor force remains a bit of a puzzle for the Fed.

Last week’s analysis of the U.S. labor market concluded there wasn’t much capacity left to call upon. The Fed should be able to declare “mission accomplished” in its quest for full employment – and remain on guard to see if the cost of labor begins to rise.

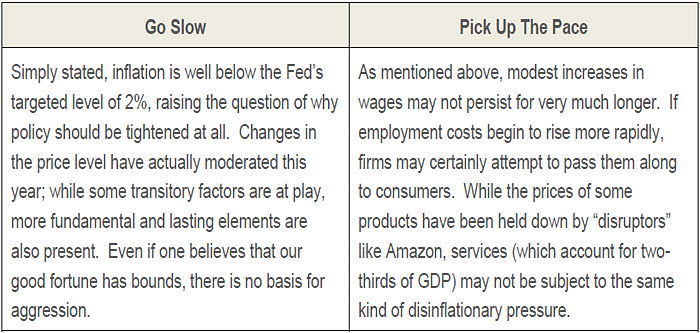

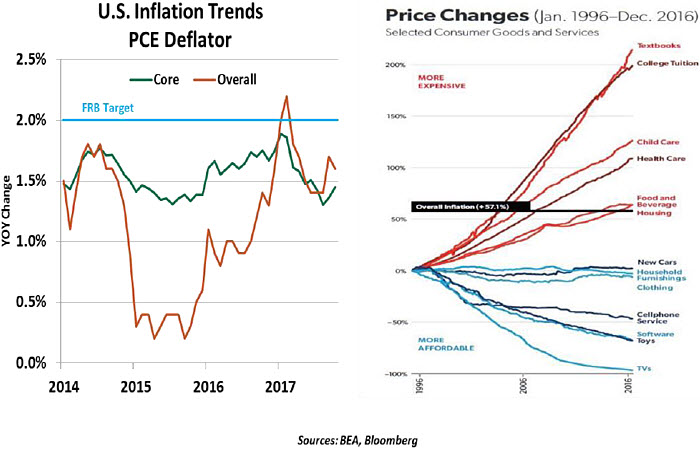

Inflation

There are two kinds of economists in the world: those that look at inflation from the top down, and those who look from the bottom up.

The top-down perspective uses the following logic. Potential real growth for the United States is thought to be about 2% over the long term. If the economy continues to grow at a pace closer to 3%, that should signal the absorption of economic capacity and rising prices for the factors of production. If traditional relationships hold, this would certainly lead inflation toward the Fed’s target of 2%.

The traditional relationships have not held, however. The disconnect between wages and inflation was discussed earlier, and advancing technological and competitive change is presenting a new paradigm for pricing in several areas. This has certainly delayed pricing increases—but will it do so permanently?

The bottom-up view looks at prices for a range of products and makes conjecture about how the individual components will evolve. Prices for services (such as health care, education, and lodging) have been rising faster than prices for goods. The former are much less likely to be heavily influenced by technology and trade, and their prices are linked more closely to wages.

We’ve had good fortune with health care costs and lodging in 2017, but continued gains in employment wealth could certainly pressure the price level.

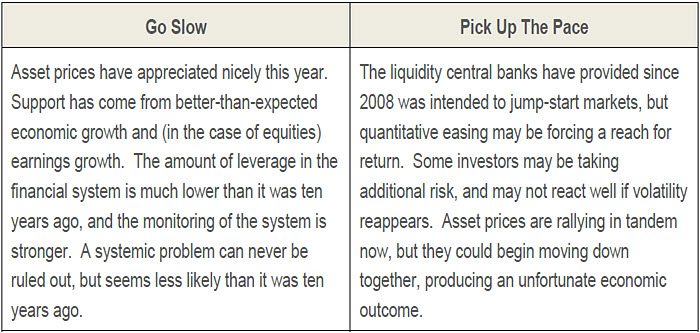

Financial Conditions/Stability

Financial stability does not appear in the Fed’s official mandate, but it is an important means to the ends that it does pursue. The lessons of 2008 are still fresh in many minds; feedback loops between markets and the economy are stronger than previously thought.

The Fed took considerable criticism for holding interest rates too low for too long after the 2001 recession, a strategy that may have contributed to housing excess. In our view, other factors were far more important in the development of imbalances. But central banks do not want to invite another crisis, and if liquidity is no longer needed to promote growth, it might be best to remove it.

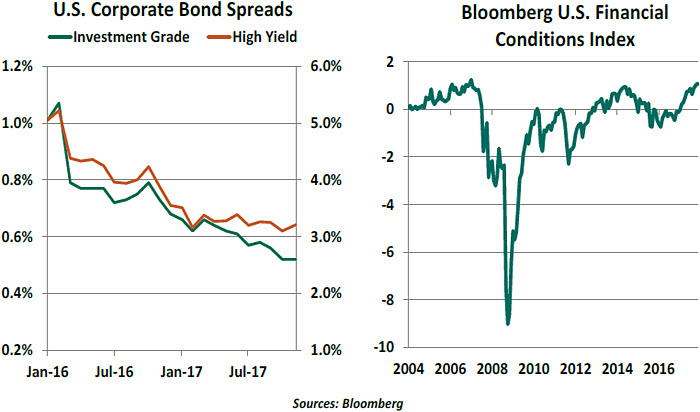

The FOMC must feel frustrated that its efforts to bring some restraint to financial conditions have been offset by easier credit conditions in the marketplace. Bond spreads have narrowed substantially since the beginning of 2016, volatility is almost completely absent and rising asset prices are providing ample collateral for further leverage. Broad measures of financial conditions are as easy today as they were just prior to the financial crisis.

The Fed has touted “macroprudential” tools like capital requirements and regulatory rulemaking as ideal means to address financial stability. But applying them effectively requires clear diagnosis of markets and a will to lean against perceived imbalances. One requires clairvoyance, and the second requires political fortitude. It is not clear that the Fed has either in sufficient quantities. It would be hard to envision it making an aggressive move solely on this basis.

Our view is that the Fed’s post-meeting materials will signal at least three interest rate increases for 2018. Apart from the push that monetary policy might get from tax reform, a more hawkish cast of incoming voting members may push the FOMC to act somewhat more aggressively.

Communication will continue to be key. Incoming chair Jerome Powell has five years of experience to draw upon, but others who will be expressing views are newer to the process. The potential for confusion will have to be carefully managed.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust