Is There Slack Left in the U.S. Labor Market?

SUMMARY

- Is There Slack Left in the U.S. Labor Market?

- Consumer Protections Debated

- Power Over Oil

My boss came to me recently and asked if I would be willing to take on some additional responsibility. I was flattered that he’d think I could be of assistance, but my plate is already quite full. After trying to divine the course of the global economy, enumerate risks to the outlook and accept blame from partners and clients for pretty much anything that goes wrong, I have little capacity left.

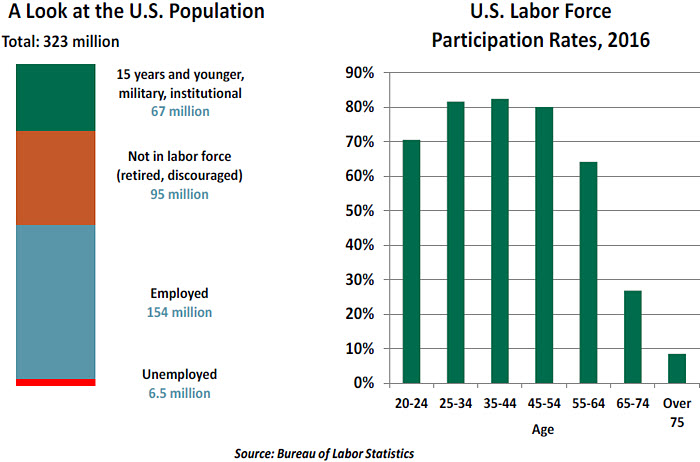

On a broader scale, many are wondering how much capacity is left in the American labor market. Joblessness is at a very low level, and yet wage growth has not accelerated. One potential explanation for this seeming contradiction is that the level of untapped human resources in the economy is greater than that suggested by the unemployment rate. A look through the details of the data finds that this contention is not likely true.

The left-hand chart below gives a broad breakdown of who’s doing what (or not doing anything) in the United States. Comments on each segment follow.

- Workers under the age of 16, those serving in the military and those confined to penal or mental institutions are not considered part of the labor force. The vast majority of this group is composed of younger citizens; their labor supply is restricted by law. There are 2.2 million Americans currently in prison. (The United States has, by far, the highest incarceration rate in the developed world.) Those in jail are not candidates for employment; sadly, those on probation and parole face an uphill climb to find steady work.

- Of the remaining population, less than two-thirds are actively participating in the labor force. The vast majority of those on the sidelines are retired; the likelihood of someone working declines considerably past the age of 65. The Federal Reserve Bank of Chicago has estimated that the transition of the baby boomers into retirement is responsible for about two-thirds of the recent decline in the country’s labor force participation rate (LFPR).

As we highlighted in our piece “Still Laboring” a couple of weeks ago, an increasing fraction of senior citizens are choosing to remain within the labor force, whether by necessity or choice. Enticing experienced workers to remain at their posts might certainly expand the capacity in the American labor markets. And some of those workers may not necessarily insist on the highest wages, as their finances are already in good order.

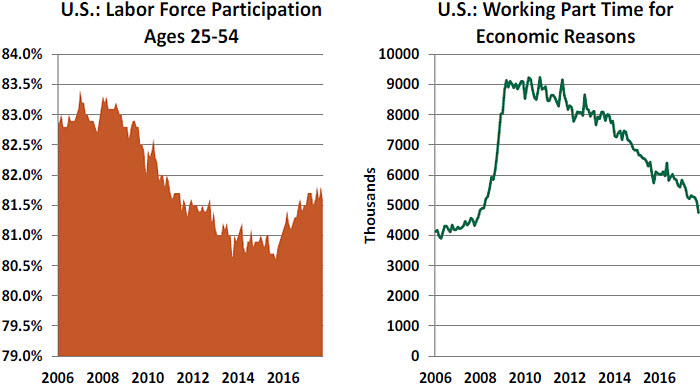

A considerable amount of attention has been paid to the decline in participation among workers between the ages of 25 and 54. Starting from well over 83% in 2007, the participation rate for these “prime-aged” women and men dropped below 81% in 2015 before beginning a slow recovery.

Retirement is a minor factor in this trend, as few have accumulated sufficient fortunes by their mid-fifties. Instead, the leading theories for labor force departure include:

a) Disability. The Federal Reserve Bank of St. Louis estimates that 11 million Americans have a disability that limits their ability to work. About 4.5 million are receiving disability benefits from the Social Security Administration; some are unable to work and others would require wage offers in excess of their benefits to change status. One economist estimated that disability accounts for about 0.3 percentage points of the recent decline in the LFPR.

b) Inertia. While the ranks of the long-term unemployed have almost returned to pre-crisis levels, this metric does not include those whose unemployment led them to leave the labor force. When workers are away from work for a long time, their skills atrophy and their attraction to employers diminishes. Economist Erik Hurst has found that young people who are jobless have gotten more comfortable with their condition, and even prefer it.

c) Addiction. A study from economist Alan Kreuger found that nearly half of workers who are not in the labor force are taking pain medication on a daily basis. The issue of opioid addiction has been rising in the national consciousness, and was recently identified by the president as an epidemic. Those who suffer from addiction may not be able to work, and if they are, employers would be reluctant to hire them.

Bringing these challenged cohorts back to full-time employment will require the aggressive application of social policy and personal responsibility. These efforts will take time, and are not likely to result in substantial amounts of new labor supply.

- More than 95% of those participating in the labor force are currently employed. But about five million of them are working part-time for economic reasons. These women and men would likely prefer full-time work if it were available, and could be called into more complete participation. In sum, this cross-sectional review reveals only limited pockets of underutilized American labor market capacity. If the country is not at full employment, we are not far from it. And given a more conservative stance on immigration, new entry to the labor force could slow in the years ahead.

- What this suggests is that sectors reliant on domestic workers and relatively difficult to automate should begin to experience wage increases. Anecdotes to that effect filled the Federal Reserve’s recent Beige Book summary of regional economic conditions. But the presence of (or potential for) offshore and automated alternatives may continue to hold down compensation levels for other employees.

- And that’s where the conversation with my boss got testy. I suggested that an increase in salary would be an appropriate reward for an expansion of responsibility. In response, he shared an article describing the success robots are having in analyzing economic trends and writing about them. If you see a computer’s name on this publication soon, you’ll know my fate.

Bureau-crazy

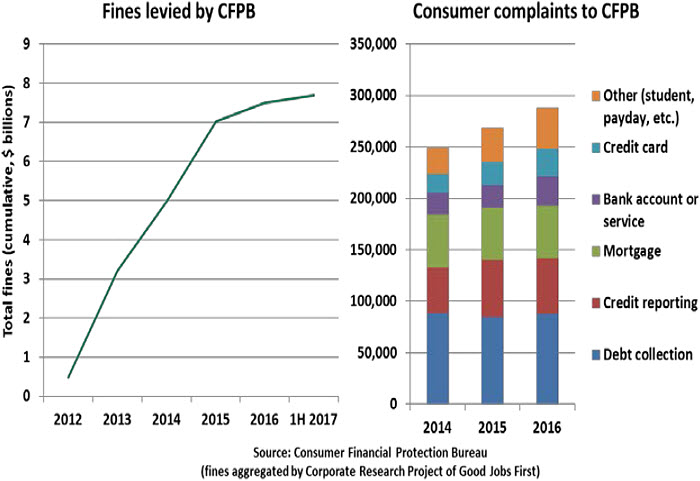

Headlines this week featured the dispute over the leadership of the Consumer Financial Protection Bureau (CFPB). Mick Mulvaney will fill the seat, concurrently with his role as director of the Office of Management and Budget. These developments have prompted some reminiscence about the origins of the CFPB and questions over whether it is still serving a useful purpose.

The CFPB was born as part of the bundle of reforms in the 2010 Dodd-Frank Act. Its goal was to consolidate the regulation of consumer financial products including mortgages, credit cards and student loans, as well as oversight of debt collections and credit bureau reporting. Each of these markets had been monitored by multiple agencies, rarely with the primary purpose of consumer protection. The CFPB sought to take a more unified, consumer-oriented approach.

At the time of Dodd-Frank’s passage, the case for the CFPB was supported by widespread concerns about financial practices that set up consumers for harm. Exotic mortgage products made mortgage payments appear affordable, but many resulted in default. The easy flow of credit cards, especially those targeting younger consumers, left many Americans with derogatory credit records before they had established their financial footing. While some of these problems were resolved through means other than the CFPB, such as tighter agency mortgage underwriting policies, they set the tenor for a feeling that consumers were at a disadvantage in the financial marketplace.

Financial services entities governed by the CFPB have a host of concerns about the regulator. They object to the power vested in its single director with authority to make broad enforcement actions. This powerful role raised the stakes of installing an acting director upon Richard Cordray’s resignation last week. Detractors would prefer a board of directors, which would serve to make the body more deliberative. Additionally, the CFPB is not subject to the annual congressional appropriations process that funds many government agencies. While this structure was intended to prevent political tampering with the bureau’s budget, it removes a layer of accountability and further concentrates the director’s authority. More philosophically, lenders object to being defined by the behavior of their least ethical competitors. Consumers who were harmed already had recourse directly with lenders, and through the legal system. Is an additional regulator necessary?

The case against the CFPB would be more compelling if not for recent headlines showing continued malpractice among certain financial services entities. Last September, Wells Fargo faced a fine of $185 million for certain bankers’ years-long practices of opening millions of unwanted accounts in consumers’ names. They recently returned to the news for overcharging mortgage, auto insurance and foreign exchange customers. This is not to single out Wells Fargo. The CFPB took significant enforcement actions against student loan servicer Navient, several major consumer banks, many mortgage servicers and all three consumer credit bureaus.

The CFPB’s Office of Consumer Response works to ensure investigation of consumers’ concerns. As of July 2017, the bureau has handled over 1.2 million complaints, with volumes rising each year. While the majority of these investigations result only in the company explaining its actions, the good news for consumers is that 97% of complaints sent to the CFPB have received a prompt response. Consumers can feel confident they were heard.

Markets work best when information flows freely and transparently. Through recent news events, we have seen that, even under the supervision of a bureau chartered for consumer support, common financial products can be a pitfall for less vigilant consumers. Policymakers would do well to move at a measured pace and ensure deregulation does not leave their constituents at a disadvantage.

Electrifying

This week, the Organization of Petroleum Exporting Countries (OPEC) announced new limits on the supply of oil. Russia, which is not an OPEC member, was an honored guest; its cooperation is important to the success of any effort to support prices.

As we have written, the cartel does not have the influence that it once did. Non-OPEC producers have become more prominent, and obedience within the cartel has been tenuous at best. But the biggest long-term threat to OPEC might be the advancing use of alternative fuels for transportation.

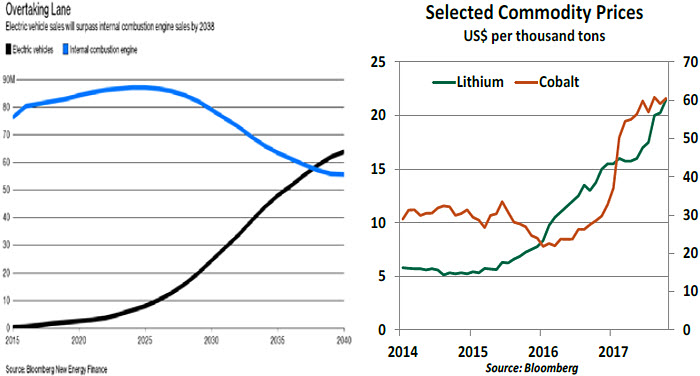

At present, there are about 1.2 million electric vehicles in use around the world. This represents only 0.2% of the global fleet, but the figure is growing fast. Climate management objectives and a desire for additional energy independence have led states and nations to commit to higher utilization of electric cars. According to Bloomberg, sales of electric vehicles will exceed those powered by internal combustion engines within the next 20 years.

As with other emerging technologies, there is a chicken and egg situation. Drivers, worried by “range anxiety,” are reluctant to change until there are enough powering stations to keep their cars running. But the infrastructure to support electric cars may be slow to develop until there are a sufficient number of them on the road.

Recent breakthroughs in battery life are helping things along. The minerals the batteries rely on, such as lithium and cobalt, have skyrocketed in price over the past two years. (This has provided a nice windfall for countries blessed with deposits of these commodities.) Petroleum accounts for 92% of transportation fuel, but only 4% of global power generation. So the shift to electric cars will be a major detriment to oil producers.

Some suggest that we are near, or even past, the tipping point for electric vehicles. A strategy to sustain high oil prices might only serve to hasten this progression. OPEC and its adjutants should be careful what they wish for.

© Northern Trust