“Pangloss gave instruction in metaphysico-theologico-cosmolo-nigology. He proved admirably that there cannot possibly be an effect without a cause and that in this best of all possible worlds the baron’s castle was the most beautiful of all castles and his wife the best of all possible baronesses.

It is clear, said he, that things cannot be otherwise than they are, for since everything is made to serve an end, everything necessarily serves the best end. Observe: noses were made to support spectacles, hence we have spectacles. Legs, as anyone can plainly see, were made to be breeched, and so we have breeches. . . .

Consequently, those who say everything is well are uttering mere stupidities; they should say everything is for the best.”

(From “Candide: or, All for the Best”, by Voltaire, 1759) (Emphasis added)

Goldilocks is going back for thirds. The beneficent global economic regime we’ve described for the past several months remains solidly in place – global economic growth (especially in manufacturing), strong corporate earnings and revenues, raging equity markets, low interest rates, and an almost frightening level of market complacency.

It seems increasingly probable that Congress will pass some level of tax reform in late 2017 or early 2018, and that will provide a further catalyst to economic growth. Even if the legislation is somewhat pork-flavored and, at the same time, watered down, it should still be stimulative to further economic expansion.

Likewise, the appointment of Jerome Powell seems to be making the markets very happy, given what seems to be his inclination toward following the Janet Yellen slow and steady approach to raising interest rates.

Both wages and inflation are rising, which is positive, and makes the Fed’s decision to raise rates in December a near certainty. Oil prices seemed to have stabilized as well, so while inflation remains somewhat muted given the overall levels of economic growth and low unemployment, the pieces seem to be in place for a future increase in inflation.

We opened with a literary reference, so let us insert another, this time the opening sentence of Charles Dickens’ “Tale of Two Cities” (emphasis added):

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us, we were all going direct to Heaven, we were all going direct the other way – in short, the period was so far like the present period, that some of its noisiest authorities insisted on its being received, for good or for evil, in the superlative degree of comparison only.”

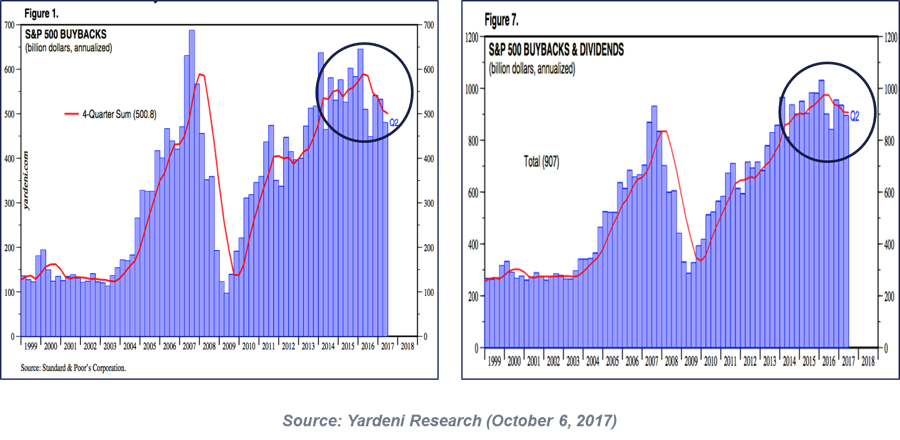

The following graphs illustrate the point.

- It was the best of times:

For the past several years, the market delivered increased earnings in the face of flat to moderate revenue growth, primarily by way of financial engineering – stock buy backs and increased dividend payouts. While a completely legitimate method of enhancing current shareholder value, it is unsustainable. At some point, companies needs to grow top line revenue and re-invest back into internal R&D, capital expenditures, and hiring. What the graphs above suggest is that this is beginning to happen. In the face of increased revenues and earnings, financial engineering is abating. We view this as a very positive signal to further expansion.

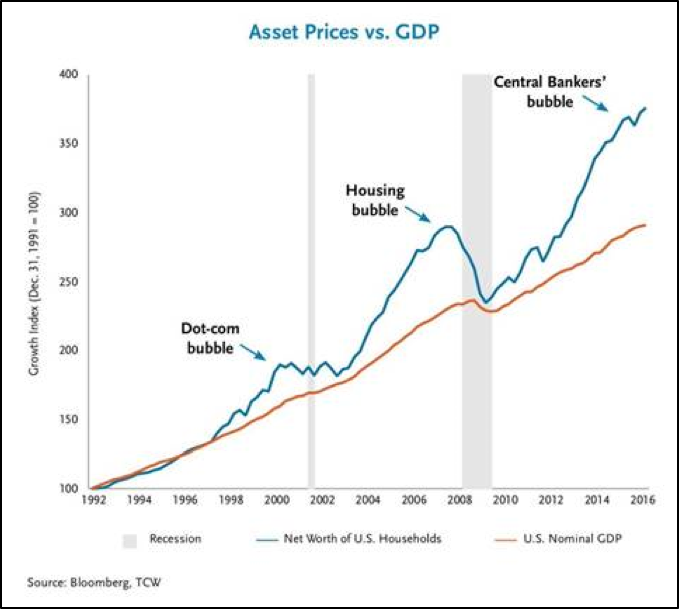

- It was the worst of times, borrowed from our favorite game theorist Dr. Ben Hunt’s Epsilon Theory, who in turn borrowed it from asset manager TCW:

The magnitude of the effect of global quantitative easing on stock prices simply cannot be dismissed or under-estimated. As the US begins an attempt to “normalize” rates and the ECB seems not too far behind, no one should delude themselves (yet again) that, “This time it’s different.”

The Current Economic & Market Landscape

- The global economy remains solidly positive right now:

- US Q3 GDP came in at 3.3%; GDP growth estimates for all of 2017 are now at 2.5% (source: The Wall Street Journal);

- Both the US manufacturing and services sectors remain well in expansionary mode – the ISM manufacturing index came in at 57.8 in October, and non-manufacturing came in at 60.1 (anything above 50 is considered expansionary);

- Inflation remains a question mark – both the “headline” and “core” (which excludes the volatile food and energy sectors) inflation numbers are hovering around 2% YoY (the Fed target). The culprits of this low inflation seem to be:

- - Wage growth – wages are increasing, but not at a pace commensurate with the tightening labor markets, though they seem to be accelerating;

- - Ongoing automation and globalization; and

- - Fairly low and stable energy and commodity prices.

- It is hard to see what might change this dynamic over the medium term;

- S&P 500 companies delivered a 6.6% increase in earnings versus Q3 of last year, on a 6% increase in revenues. Firms reported a 72.3% earnings “beat rate” and a 66.5% revenue “beat rate” – both higher than multi-year averages (source: Zachs Earnings Report);

- The Eurozone Q3 2017 GDP growth came in at 2.5% (annualized); the consensus estimate for Q4 is 2.4% (source: TradingEconomics);

- GDP and manufacturing are expanding across the Eurozone, with the Markit manufacturing index hitting 57.5 in October (anything above 50 is expansionary);

- Unemployment has fallen to 8.9%, an 8-year low, and annualized inflation through October was 1.4%. New hires are at a 17-year high;

- ECB President Draghi announced a “tapering” of quantitative easing, but market interpreted his comments as dovish and “lower for longer”;

- Japan’s Q3 GDP was a positive 2.6% (annualized), and represented the seventh straight quarter of positive GDP growth. The consensus estimate for Q4 GDP growth is 2.4% (source: TradingEconomics);

- China’s (official) growth rate for Q3 was again stable at 6.8%, and (official) estimates for Q4 are 7.0% (source: TradingEconomics).

The Dynasty Economic & Market Outlook:

- The global macro-economic environment remains benign;

- Global inflation remains low – this creates some level of uncertainty regarding central bank policies;

- Moderate (and increasing) probability of tax reform in the US – maybe a “watered down” version in late 2017 or early 2018, but Trump’s agenda is struggling in the face of universal resistance by Democrats and a handful of recalcitrant Republicans;

- Solid GDP, earnings, and revenue growth, combined with low rates and low volatility, make for a “Goldilocks” environment likely to continue for some time, but equities still look very expensive to us;

- EM and EAFE markets continue to have better valuations than the US (though not cheap). The USD trend is the wild card for US investors – we think the year-long slide is ending;

- The US yield curve remains flat but we do not anticipate an inversion – lower for longer and slowly grind higher remains the name of the song;

- At these rates and credit spreads, the public credit markets look very expensive to us;

- For investors who can access them and handle the relative illiquidity, we continue to believe better opportunities lie in the private markets, even though historical spreads to the public markets have compressed due to massive inflows;

- As we anticipated, it is shaping up to be a better year for alternative investments, but we are more optimistic about hedge funds than liquid alternatives because of less liquidity and leverage constraints;

- We perhaps will enjoy a modest rebound in commodities and oil prices as global economic growth expands;

- While we generally are constructive on the global economy and overall market performance, the public markets are not cheap. Clients need to have their expectations managed as to what a diversified portfolio can deliver over a full market cycle.

So, as we review the economic and market landscape, we see many good and positive things – a growing economy, solid earnings, low inflation, and low interest rates. We assign a fairly low probability to that regime not continuing for some time.

However, it is important to remember that Candide was a satire, and while Candide himself was naïve, he was not stupid, as illustrated by the final passage in the book. We seem now to be living in the” best of all possible worlds”, but we still must tend to our garden.

“You are perfectly right, said Pangloss; for when man was put into the Garden of Eden, he was put there ‘ut operaretur eum’, so that he should work it; this proves that man was not born to take his ease.

Let’s work without speculating, said Martin; it’s the only way of rendering life bearable. The whole little group entered into this laudable scheme; each one began to exercise his talents. The little plot yielded fine crops . . . and Pangloss sometimes used to say to Candide:

All events are linked together in the best of possible worlds; for, after all, if you had not been driven from a fine castle by being kicked in the backside for love of Miss Cunégonde, if you hadn’t been sent before the Inquisition, if you hadn’t traveled across America on foot, if you hadn’t given a good sword thrust to the baron, if you hadn’t lost all your sheep from the good land of Eldorado, you wouldn’t be sitting here eating candied citron and pistachios.

That is very well put, said Candide, but we must go and work our garden.”

Warm Regards,

Scott Welch, CIMA®

Chief Investment Officer

Dynasty Financial Partners

Past performance shown is model performance shown is no guarantee of future results. The model portfolio performance does not reflect actual trading or any advisory, management, or transaction fees, all of which could result in substantially lower results. This does not reflect the impact that material economic and market factors have had on decision making. You cannot invest directly in an index.

Source: Bloomberg, Data Analysis, 1/2017-Present

Source: Zephyr, Data Analysis, 1/2017 – Present

Source: Morningstar, Data Analysis, 1/2017 – Present

General Disclosures: Dynasty Financial Partners is a U.S. registered trademark of Dynasty Financial Partners LLC ("Dynasty"). Dynasty is a brand name and functions through Dynasty's wholly owned subsidiary Dynasty Wealth Management, LLC, (“Dynasty Wealth”) a registered investment adviser with the Securities and Exchange Commission when providing investment services. A copy of Dynasty Wealth's current written disclosure statement discussing our advisory services and fees is available for your review upon request. This message is intended for the exclusive use of members or prospective members considering joining the Dynasty Network of registered investment advisors for educational purposes. It is not intended for any other persons, clients or other entities. It should not be construed as an attempt to sell or solicit any products or services of Dynasty, Dynasty Wealth or any investment strategy, nor should it be construed as legal, accounting, tax or other professional advice. Information contained herein is based on sources believed to be reliable, but there are no representations or warranties as to the accuracy of such information.

This presentation is for illustrative purposes only. Past performance is not indicative of future results. The information contained in this presentation has been gathered from sources we believe to be reliable, but we do not guarantee the accuracy or completeness of such information, and we assume no liability for damages resulting from or arising out of the use of such information.

The performance numbers displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. The index is unmanaged and does not incur management fees, transaction costs or other expenses associated with investable products. It is not possible to directly invest in an index. All returns reflect the reinvestment of dividends and other income.

Historical performance results for investment indices and/or product benchmarks have been provided for general comparison purposes only, and do not include the charges that might be incurred in an actual portfolio, such as transaction and/or custodial charges, investment management fees, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices.

The views expressed in the referenced materials are subject to change based on market and other conditions. This document may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. The information provided herein does not constitute investment advice and is not a solicitation to buy or sell securities.

This content may not be modified, distributed or otherwise provided in whole or in part to a prospective investor or someone considering investing in the portfolio models without the express authorization of the party delivering the presentation. Please note that nothing in this content should be construed as an offer to sell or the solicitation of an offer to purchase an interest in any security or separate account. Nothing is intended to be, and you should not consider anything to be direct investment, accounting, tax or legal advice to any one investor. Consult with an accountant or attorney regarding individual accounting, tax or legal advice. No advice may be rendered, unless a client service agreement is in place.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Dynasty Financial Partners, who reserve the right at any time and without notice to change, amend, or cease publication of the information contained herein. This material has been prepared solely for informative purposes. The information contained herein includes information that has been obtained from third-party sources and has not been independently verified. It is made available on an "as is" basis without warranty. Strategies and investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor

DWM is a registered investment advisor with the Securities and Exchange Commission. DWM serves as a sub-advisor to Dynasty Strategist Portfolios (“the Portfolios”), however DWM does not directly manage client assets within the Portfolios. Any reference to the term “registered investment adviser” or “registered” does not imply that Dynasty or any person associated with Dynasty has achieved a certain level of skill or training.

© Dynasty Financial Partners

© Dynasty Financial Partners

Read more commentaries by Dynasty Financial Partners