How Have Hurricanes Harvey, Irma and Maria Impacted the Municipal Bond Market?

Affected regions’ long-term outlooks largely depend on initial credit conditions

The financial impact of 2017’s three devastating hurricanes has varied greatly depending on the region affected. From a credit standpoint, the most important takeaway is that each region’s ability to withstand the financial impact of the storms depends on its credit quality ahead of the storm. This does not bode well for Puerto Rico and the US Virgin Islands, which have been struggling with deteriorating fiscal conditions for some time. On the other hand, Houston and Florida are beginning the rebuilding process from a much stronger economic and financial position. Below we examine the storms’ impact on each affected region.

Houston

We believe Houston’s strong credit position will enable it to absorb the economic impact of Hurricane Harvey, especially factoring in the ability and apparent willingness of the state of Texas (AAA1) to support hurricane relief efforts. There has been some concern regarding population erosion and the resulting decline in real estate prices and property tax receipts. However, Houston is the most populous city in Texas and the fourth most populous city in the US.2 Its economy is well-diversified, including energy, manufacturing, aeronautics and transportation, and with federal help, we do not expect a mass exodus of residents from the city. We believe Houston is likely to recover from the hurricane with its strong credit quality intact.

Florida

Florida general obligation bonds are rated AAA,3 meaning they are rated the highest credit quality. The major rating agencies have highlighted Florida’s strong employment and population growth, robust general revenues, structural budgetary balance, strong reserves, well-funded pension liabilities and moderate debt burden. Standard & Poor’s has said Florida is “well-positioned, to the extent possible, to confront the potential demands of a catastrophic storm, given the state’s governing framework and infrastructure.” The state’s economic performance is among the strongest in the nation, and it has ample reserves, which, together with trust fund balances, amount to nearly $5.2 billion.4 That said, it is possible the state could experience a short-term drop in tourism, which accounts for nearly 13% of general revenue sales taxes.5

Puerto Rico and the US Virgin Islands

The Commonwealth of Puerto Rico (Ca6) and the US Virgin Islands (rum tax bonds,7 senior lien: Caa18) suffered profound devastation due to Hurricanes Irma and Maria, leading to tragic loss of life and damaged homes, businesses and infrastructure. While the full extent of the human toll and physical destruction remains to be measured, the storms clearly pose a credit challenge to both territories.

Both Puerto Rico and the US Virgin Islands were impacted at a time when they were already suffering financial distress. Puerto Rico is currently undergoing a debt restructuring under US federal oversight, and the US Virgin Islands is facing extremely weak levels of liquidity. We believe that both entities will be heavily reliant on relief from the US federal government.

In Puerto Rico, an important impact of the hurricane has been to lengthen the timing of the fiscal turnaround needed to help restore the island’s credit standing. Previously, economists had estimated that GDP growth would turn positive in the commonwealth by 2021/2022, after 11 years of recession. This has now likely been delayed by a year. On top of the social concerns caused by the hurricanes, Puerto Rico is also facing the additional pressure of debt negotiations, which are also now likely to be delayed.

The Puerto Rico Electric Power Authority (Ca9), which is restructuring its debt in a judicial proceeding, faces severe damage to its electrical grid, and power is out throughout much of the island. While it will receive funds from the Federal Emergency Management Agency (FEMA) and insurance over time, the utility faces numerous challenges, including the age and condition of its present infrastructure and its current financial condition. These factors weaken Puerto Rico’s credit quality and limit its ability to secure financing that would serve as a bridge to permanent FEMA or insurance funding. This lack of financing will inevitably delay needed repairs to its infrastructure and hinder growth. Other public providers of transportation and telecommunications infrastructure also face challenges securing credit.

In the US Virgin Islands, there seems to be some marginally positive market news: Early reports indicate that rum distilleries on St. Croix did not sustain damage from Hurricane Maria, though the damage assessments are ongoing. Even if production were disrupted at these facilities, the flow of revenues backing the rum tax bonds is not projected to be affected for two years.

On the other hand, the combined damage from Hurricanes Maria and Irma is expected to worsen the government of the Virgin Islands’ extremely weak liquidity position, increasing the risk that the government interferes with the flow of pledged revenues to honor its obligations or that the rum tax bonds could be included in an attempt to restructure its debt.

FEMA

Federal reimbursements through FEMA help soften the credit impact from natural disasters. However, it is important to stress that a significant portion of disaster relief funds are in the form of reimbursements, and therefore, affected areas must first make expenditures to repair damage. It is also important to note that FEMA reimbursements can take time.

That is why a municipal government’s recovery from a natural disaster is largely dependent on its credit strength pre-disaster. A key element of this is the affected issuer’s access to the debt market and cash reserves. In the short term, liquidity and reserve levels are important to cover cleanup costs, pay expenses when the timing of FEMA reimbursements is uncertain, and service upcoming debt payments. Access to financing for cash flow purposes is also important.

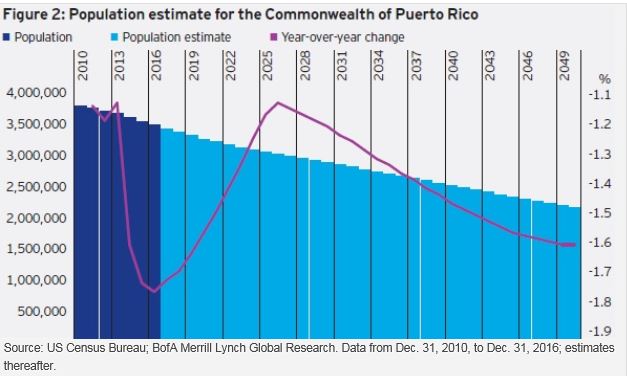

In Puerto Rico, FEMA is not expected to enable an economic turnaround, partly due to demographic issues. The US Census Bureau recently updated its population estimates for Puerto Rico, forecasting that Puerto Rico’s population will fall 1.7% in 2017 and around 11% by 2025 — in total, some 370,000 people (Figure 2). By 2050, the Census Bureau believes the population will decline to 2.1 million, a 38% decline from the 2017 estimated population of 3.4 million (Figure 2). Sharp declines in population mean a sharp decline in aggregate wealth and the commonwealth’s tax base, which could further the vicious cycle of declining credit quality that has been in progress for some time.

Conclusion

While economic losses related to the recent hurricanes have been staggering, municipals have not been affected homogeneously. Rather, the impact of the storms on credit quality and market performance has been idiosyncratic, with the economic starting point before the storms being the most important factor. Looking back at Hurricane Katrina in 2005 and its impact on New Orleans, spreads widened significantly following the storm, and the city’s credit rating was downgraded four notches from BBB+ to BB in 2005. It did not return to BBB+ until 2013. On the other hand, higher-rated New York metropolitan area credits were largely unaffected in terms of ratings and spreads by Hurricane Sandy in 2012.

In short, higher-rated credits have historically recovered relatively quickly from natural disasters. In contrast, lower-rated credits have experienced a slower and weaker recovery. We expect this pattern to repeat itself in the aftermath of this year’s terrible storms.

1 Source: Standard & Poor’s as of Oct. 24, 2017

2 Source: US Census Bureau, May 25, 2017

3 Source: Standard & Poor’s as of Oct. 17, 2017

4 Source: Moody’s as of Oct. 16, 2017

5 Source: State of Florida, Long-Range Financial Outlook, Fall 2017 report

6 Source: Moody’s as of Oct. 11, 2017

7 Much of the US Virgin Islands’ debt is backed by taxes levied on rum sales. Because many of the US Virgin Island general obligation bonds are illiquid, rum tax bonds are viewed as representative of the island’s debt.

8 Source: Moody’s as of Jan. 24, 2017

9 Source: Moody’s as of July 6, 2017

Stephanie Larosiliere

Senior Client Portfolio Manager1

Stephanie Larosiliere is the senior client portfolio manager for the Invesco Municipal Bond team. Ms. Larosiliere works with the fund management team, acting as its representative to retail clients and other intermediaries.

Her responsibilities include working with sales staff and clients to provide insight on the municipal fixed income market and the investment strategies utilized by the team. She is also responsible for ongoing product development and marketing for the municipal bond products.

Ms. Larosiliere joined Invesco in 2011 as a senior product manager supporting the municipal and convertible businesses. Prior to joining Invesco, Ms. Larosiliere served as a vice president in the Goldman Sachs Asset Management fixed income product management team where she was responsible for portfolio analysis, product development, client retention and marketing. Prior to joining Goldman Sachs in 2008, she worked as an institutional product management associate for Brown Brothers Harriman. She began her career in the industry in 2003 as a risk management analyst with JPMorgan Chase where she was responsible for performing daily value at risk (VaR) analysis and monthly stress risk tests on the bank’s credit portfolio.

Ms. Larosiliere earned a BBA degree in finance and investments from Baruch College — The City University of New York (CUNY).

1 Not involved in managing assets of any fund.

Important information

Blog header image: Sasa Kadrijevic/Shutterstock.com

Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa.

An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Municipal securities are subject to the risk that legislative or economic conditions could affect an issuer’s ability to make payments of principal and/or interest.

Junk bonds involve a greater risk of default or price changes due to changes in the issuer’s credit quality. The values of junk bonds fluctuate more than those of high quality bonds and can decline significantly over short time periods.

A credit rating is an assessment provided by a nationally recognized statistical rating organization (NRSRO) of the creditworthiness of an issuer with respect to debt obligations, including specific securities, money market instruments or other debts. Ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest) and are subject to change without notice. For more information on the Standard and Poor’s rating methodology, please visit standardandpoors.com and select “Understanding Ratings” under Rating Resources on the home page. For more information on the Moody’s rating methodology, please visit moodys.com and select “Rating Methodologies” under Research and Ratings on the home page.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

How have Hurricanes Harvey, Irma and Maria impacted the municipal bond market? by Invesco