Weighing the Week Ahead: The Millennial Effect on the Housing Market

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar includes many reports, but few of the most important. I expect the housing market to attract attention. There are several relevant releases on tap, and the sector is especially important. Some will take up a special slant, asking:

Will Millennial buyers extend the housing market rebound?

Last Week Recap

In the last edition of WTWA I mused on the confluence of records in the data and in stock market indexes. I suggested that some of the punditry would start worrying that things were “as good as it gets.” This was a topic for some, including David Templeton, who responded with a qualified “no,” but suggested the need to look beyond the mega cap stocks. Check out his reasoning and persuasive charts.

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short via Jill Mislinski. She notes the loss of 0.21% on the week. Once again, it was a week of very low volatility; the intra-week range was only a touch more than 1%. Historically 1% moves are commonplace — each day!

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read the entire post for several more charts providing long-term perspective, including the size and frequency of drawdowns.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The economic news has been mostly positive, as summarized by New Deal Democrat’s helpful compilation of long, short, and coincident indicators. His conclusion is neutral on the long term and positive in shorter time frames.

The Good

-

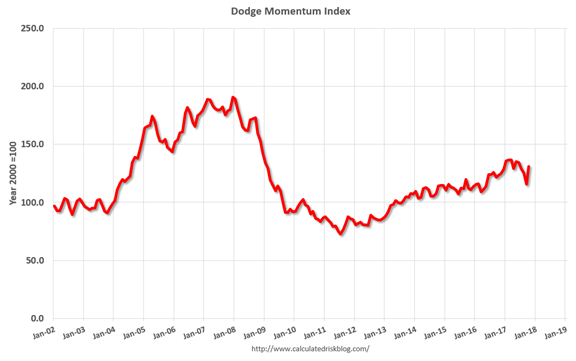

Leading index for commercial real estate improves. Calculated Risk notes that the Dodge Momentum Index rose 13.2% in October versus September. According to Dodge, this indicator leads non-residential construction spending by one year.

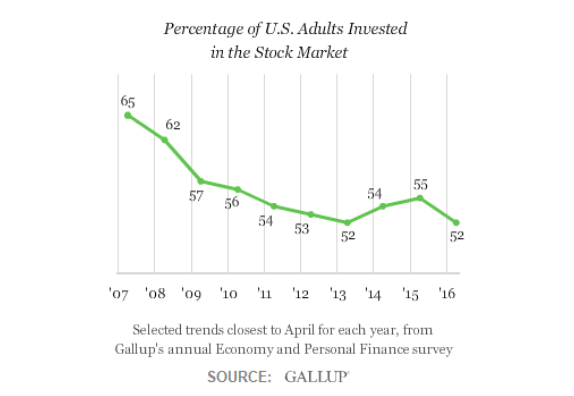

- Household stock ownership is at the lowest level in almost twenty years.Chris Ciovacco uses Gallup data to refute the notion of a current, euphoric bubble.

-

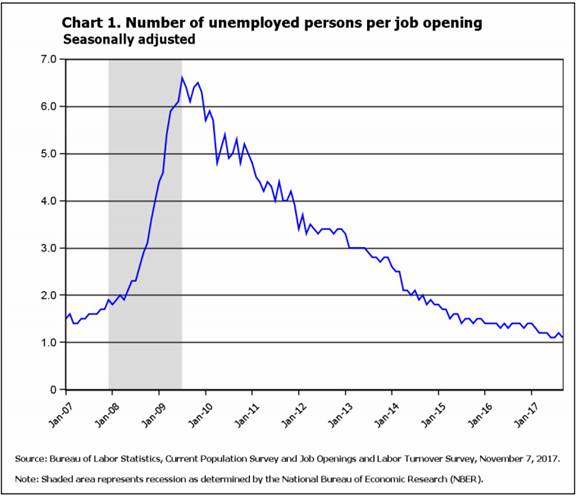

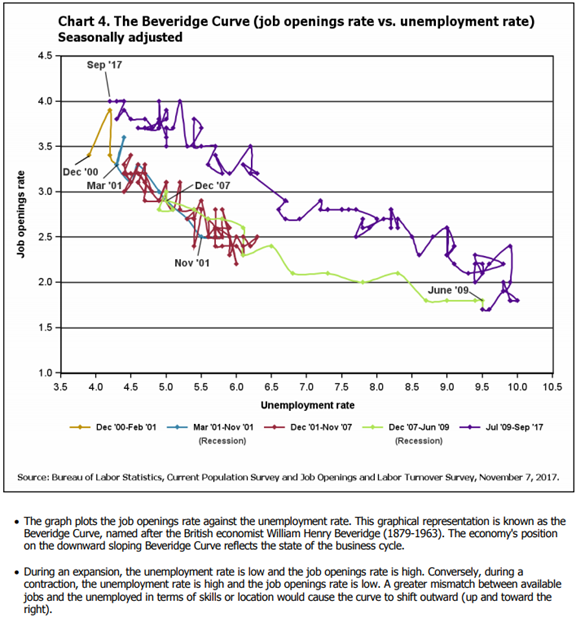

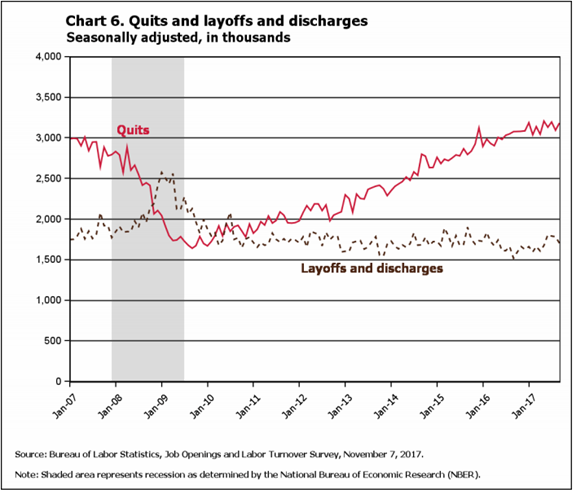

Job openings increased….and other good news from the JOLTS report. No one does a good job of analyzing this report. Many try to interpret it as a sign of employment growth, a purpose for which it was not designed. With fewer indicators to summarize this week, let me suggest the key things we should watch for.

- Ratio of unemployed to job openings.

- Beveridge curve – indicator of labor market structure.

- Reason for job separations —layoffs or voluntary. Layoffs get a lot of news. A high quit rate shows confidence on the part of employees.

The Bad

- Jobless claims were 239K, 10K higher than last week, and worse than expectations.

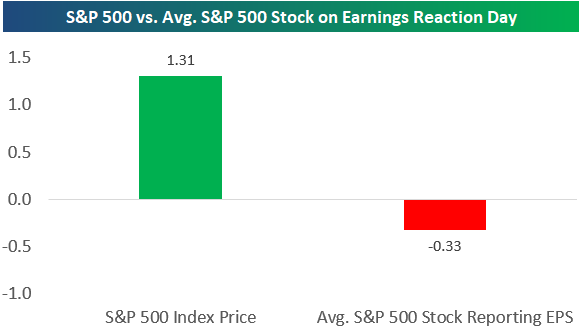

- Response to earnings was weak. Bespoke reports that despite solid earnings, there is a divergence between the overall S&P and the average member stock.

- Michigan sentiment dipped to 97.8 from last month’s 100.7 and expectations of 101.

- Rail traffic weaker via Steven Hansen of GEI. He looks beyond the headline data to elements he has identified as more predictive. While still better than a year ago, the improvement is decelerating.

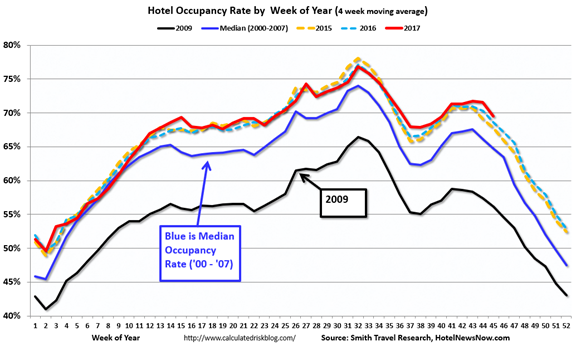

- Hotel occupancy rate declined 0.9% last week. The rate remains ahead of the record-setting pace of 2015. (Calculated Risk)

The Ugly

Each week seems to bring another case of outlandish violence. While there are some common themes among the perpetrators, there is no consensus about solutions – or even whether to act. Opinions about the best policy reaction seem to depend more upon beliefs rather than facts. That is always a tough situation for public policy proposals.

Millennial Notes

My research always leads me to a few items that are interesting, but not necessarily relevant to the week ahead. One such item was a list of terms and expressions that Millennials would use, but older people would not. I had the inspiration to write a paragraph or two using these terms, in the Blazing Saddles tradition. Mentioning this to Mrs. OldProf, she informed me that this was one of my dumber ideas. She was right, of course. A quick look at another source showed that many terms from the first source are now (already?) retired.

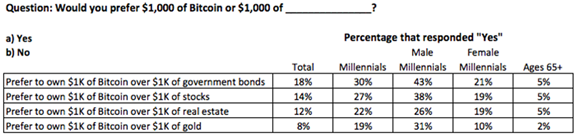

Millennials are far more likely to prefer bitcoin to stocks or bonds.

And this is despite their low ownership; only 4% have ever owned bitcoin.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

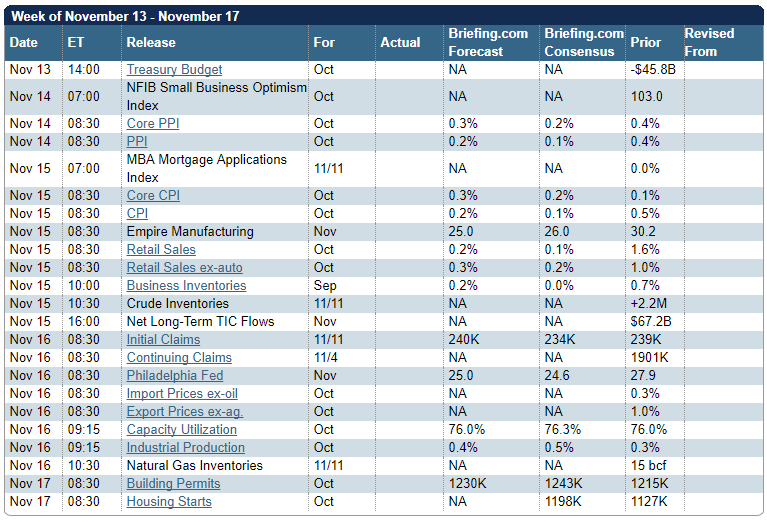

The Calendar

We have a normal calendar. The inflation data is edging up to a level where it will attract more interest. Retail sales is always an important report, as is industrial production.

That said, I see the Friday reports on housing as the most significant news. Building permits are an important leading indicator. That data series and new housing starts are volatile series. That makes them a challenge to interpret, but no less important.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

The calendar is a busy one, but not one to suggest important surprises. If inflation picks up, that will attract more analysis of the business cycle and the Fed. With several housing reports on tap, that may well be the focus of attention. So far, the recovery has been led by consumer spending, with little help from business investment or housing. If the rebound is to continue, more sources of growth are needed. The answer may come from the changing U.S. demographics, leading people to ask:

Can Millennials provide the push for an extended housing rally?

Here are some perspectives, in my customary bearish to bullish range.

- Get ready to revisit the housing bubble! (The IMF – a partial warning; Jesse Colombo, who sees many, many bubbles; and 58% of homeowners themselves)

- High prices (contra-Calculated Risk)

- Rising mortgage rates

- More rigor in loan requirements

- Lack of supply (Zillow)

- Down payments a challenge for new buyers

- Tax proposal killing the mortgage interest deduction (By the Numbers)

- Gen Y is growing in economic importance (Calculated Risk)

- Now the largest group of home-buyers (Washington Federal)

- Factors sparking the decision to buy a home (few readers will guess the most frequent – answer at the end of today’s post)

As usual, I’ll have more in the Final Thought, where I always emphasize my own conclusions.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

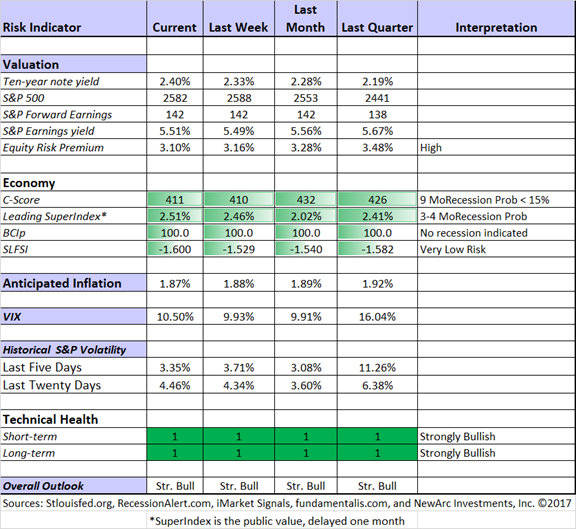

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Georg Vrba: Business cycle indicator and market timing tools.

Doug Short: Regular updating of an array of indicators. Great charts and analysis.

Guest Source:

The BLS. Most observers engage in plenty of discussion about the initial release of employment data. Why? It is an important topic, so people grab on anything, ignoring the problems in short-term measurement. Each quarter the BLS releases a new installment of the Business Dynamics series. Because this uses state employment data, reviewed and aggregated for this purpose, it is much more accurate than the monthly estimates. In fact, it makes sense to review the various estimates using this result as the “right answer.”

For Q1 2017 the net increase in private jobs was 654K. The sum of the initial monthly reports on employment Friday was 553K. The actual difference would have been a major source of debate if known at the time.

Also worth noting is the massive change – much more important than the net result. 7.3 million jobs were created. And of course, 6.7 million were lost. Opening establishments accounted for 1.3 million new jobs, something that the birth/death adjustment truthers should study.

It also demonstrates that many more people are touched by unemployment than the official rate indicates. No wonder economic perceptions are often worse than the data seem to show.

Insight for Traders

We have not quit our discussion of trading ideas. The weekly Stock Exchange column is bigger and better than ever. We combine links to trading articles, topical themes, and ideas from our trading models. This week’s post continues our discussion of the strength of combining different trading approaches – a blended approach. To illustrate, we provided some historical data on the trading models. And of course, there are updated ratings lists for Felix and Oscar, this week featuring small caps. Blue Harbinger has taken the lead role on this post, using information from me and from the models. He is doing a great job.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Brett Steenbarger’s analysis of Frustration, part of his trading psychology series. While I most frequently cite Dr. Brett when we specifically deal with a trading theme, there is often an overlap with investor decision making. This is such a case. Investors with a sound overall approach can become frustrated at a stretch of losses or concern about reaching their goals.

…frustration is a great example of the principle that strengths, taken to an extreme, can become vulnerabilities. When we are achievement oriented and demanding of ourselves, having something get in our way breeds a natural frustration. That frustration, in turn, triggers a fight/flight state and suddenly we are no longer nicely grounded in our brain’s prefrontal cortex. Instead, we activate motor areas to cope with the situation and act in ways that we would never entertain if we were calm and focused at the start of the trading day.

This often describes the behavior of individual investors, especially those who constantly chase what worked last month or last year. Polling from Pew Research shows that many share this sentiment.

[Investors feeling frustration might find helpful my paper on Investor Pitfalls. If your frustration relates to missing the rally and/or being behind on your retirement program, I have another piece on how to edge your way back into the market. Both are available for free from main at newarc dot com].

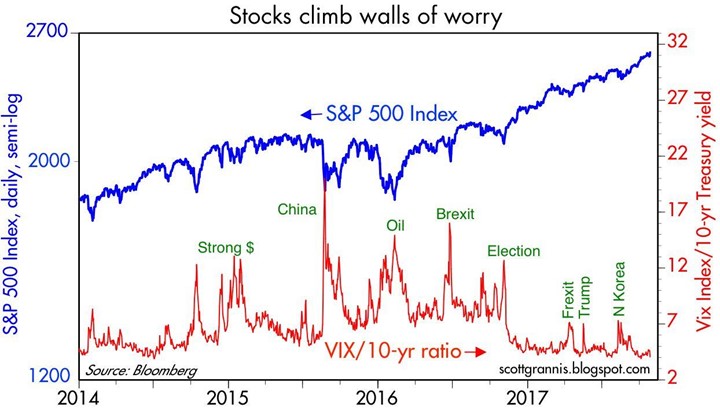

Scott Grannis shows how the perceived problems have actually provided fuel for the stock rally.

Stock Ideas

“Doghouse stocks?” Ray Merola is reviewing some recent occupants. In this post he is analyzing Celgene (CELG). He takes note of the high risk in trials and the disappointing sales of a key product. He concludes that the market has over-reacted. This is a data-driven analysis worth reading.

Starbucks or Facebook? Peter F. Way’s unique approach to risk/reward suggests Facebook. Check it out.

Brian Gilmartin shows what’s hot and what’s not in corporate earnings trends. Energy rolling, and financials depressed. Which is the opportunity?

Homebuilders “hammered” by the tax plan?

Interested in Speculation?

Brad Thomas looks at Puerto Rican debt via DDR Corp. (DDR)

Or Contrarian Choices?

Here are the six most shorted Nasdaq stocks.

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich has an interesting topic every day. While his series’ theme emphasizes financial advisors, the topics are usually of more general interest. His own commentary adds insight and ties together key current articles. It is a valuable daily read. My favorite this week discusses the possible value of an annuity in your retirement plan. He cites an article by Dick Cotton, showing how the annuity can provide a foundation for other, more aggressive investments.

This is a great example of Gil’s series expanding horizons for many advisors.

Alan Steel (HNW Magazine) shares his customary wisdom with a discussion of current exaggerated pessimism, something that many seem to ignore. Here is his analysis:

Some folks are calling it a secular bull that is both old and decrepit, and busily sunning itself through its golden years from the light of a few big stocks as it has done since about March 2009.

Others consider the market crashes within that eight year (plus) period, like the 21.6% S&P 500 drop from May to October 2011, and the recession-level peak-to-trough numbers in the US, Japan, China, and emerging markets (amongst others) from mid-2015 to early 2016 (details here), put the age of this bull at somewhere around 4.5 years, or perhaps just a year and a half.

Then there are the gloomier folks who, despite the long-term upward trend, positive corporate earnings, basement level inflation, low unemployment, respectable jobs growth, and historically low interest rates, habitually pick at the scabs of negative investor sentiment and draw dotted lines between now and the ghosts of recessions past.

These apostles of Joe Granville have helped position that latter category as the people’s choice.

As such, independent investor sentiment levels about the stock market are about as euphoric right now as a stomach ulcer.

He goes on to cite the Gallup data I noted above, before concluding:

For me, I think the majority of investors are doing what they always do – waiting around for some kind of wonderfully perfect moment that will finally have built up enough financially fibrous scar tissue to replace the skin torn away by events like 2008/09, 2000/02, and even (for the oldies) way back to 1987 and its less memorable ilk.

Unfortunately, market nirvana is almost always either a day away or the day we missed.

So, when it comes to investing, perfect is always the enemy of good.

Abnormal Returns is always interesting, but the Wednesday edition is especially geared to individual investors. My favorite this week takes up specific steps that investors might follow to “improve our behavior.” These are great ideas, but my sense is the choice of “hire a coach” might be the only real winner for most people.

Watch out for….

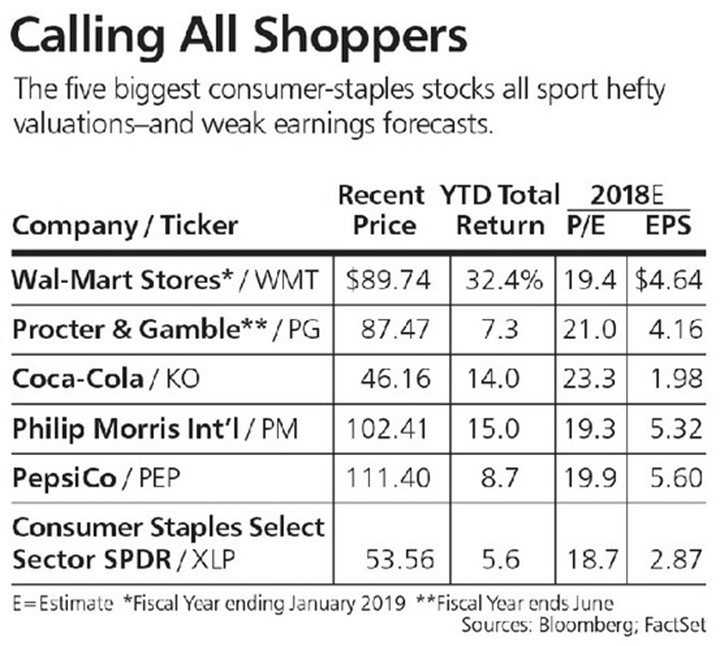

Consumer staples stocks. Barron’s notes that the sector might not be as safe as most think. (I agree). The full article provides a complete analysis, but here is a helpful summary.

Tupperware (TUP). Simply Safe Dividends looks at the sustainability of the dividend.

Stocks attracting the rare Wall Street “sell” rating.

Final Thoughts

Taking advantage of demographic trends is an important way to improve your investment results. The growing economic significance of Gen Y is obvious. The change in the housing market is an important example.

Housing àEconomic Growth à Stronger Stocks

Strength in housing ripples through many other parts of the economy, including materials, employment, construction, and transportation. (Ritholtz). I have recommended home building stocks many times over the last year, and it has worked out well.

The “bubble” skeptics seem to reason that if sales or prices reach a former peak, that should be a warning. This simplistic approach would never recognize an overall positive trend in anything!

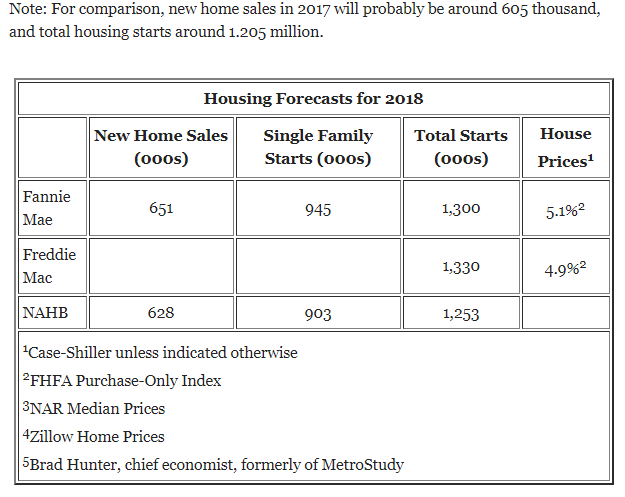

Here is a look at the 2018 Housing forecasts (Calculated Risk).

What worries me…

- The debt limit is now on our radar. It is time to see some progress on this issue.

- Trade issues. While there were no accidents on the Asian trip, there are also no indications of policy progress. The I wish the President had more willingness to use expert advice. The advantage of free trade is probably the most widely shared conclusion of economic experts.

…and what doesn’t

- Stalled tax reform. The current plans are very unlikely to get enough votes within the Republican party alone. Taking more time and gaining some bipartisan support will not happen until next year, but the result will be stronger.

- The economy. Our indicators show little risk and there is plenty of upside.

Surprising answer to a key reason for Millennial home buying: Dogs.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits