Healthcare legislative headlines have shifted the focus from fundamentals to politics. However, we believe the fundamentals are likely to outlast short-term legislative uncertainties. Healthcare valuations currently look relatively cheap while underlying fundamentals appear strong. We highlight the biotech and managed care industries as two examples where a focus on long-term trends may be rewarded.

The noise out of Washington regarding changes to the Affordable Care Act (ACA) and healthcare seems to never end. Despite the lingering uncertainty, there are several longer-term industry trends worth highlighting.

Two key themes that may outlast the headlines are demographics and a renewed emphasis on cost control in healthcare services, in our view. Specifically, let’s look at two healthcare sectors that could see the greatest impacts: biotechnology and managed care.

Biotech

From an industry perspective biotech occupies a unique hybrid position. It’s both a tech-like sector, offering secular growth potential, and a healthcare sector, with corresponding defensive characteristics. That defensive position came under attack in 2015 as political rhetoric from both sides zeroed in on perceived unfair drug pricing. Nonetheless, there are two factors worth noting regarding biotech that may make this an entry point worth considering:

It is under-owned, and undervalued: Historically, biotech has traded off fundamental drivers: drug pipelines, product growth, mergers and acquisitions (M&A) activity, and patent protection. However, as the 2015 political imbroglio increased drug price uncertainty, investors pulled money broadly out of healthcare. That shift in sentiment has made current valuations more attractive. Over that past 20 years, the price-to-earnings (P/E) ratio of the Nasdaq Biotechnology Index’s has averaged 2.3 times the S&P 500 P/E ratio; today, the current ratio is mere 1.1x, a 53% discount to its 20-year average.1

Long-term drivers appear intact: Drug pipelines are notoriously challenging to predict over the short term, given the deep level of medical knowledge required, clinical testing, and regulatory review. However, two trends appear supportive over the long-term. First, advances in computational biology, bioinformatics, and artificial intelligence (AI) are features helping reduce the time and cost of drug development. Second, approval rates by the U.S. Food and Drug Administration (FDA) have steadily risen over the past two decades, climbing from 23% in 1994 to 89% and 77% in 2014 and 2015, respectively.2 Biotech’s historical drivers currently appear intact, making it one of the rare sectors that enjoys long-term growth potential at a reasonable price.

Biotech currently appears inexpensive on a relative basis

Managed Care

Few industries occupy an intersection as large or as important as managed care. The $1.3 trillion managed care space is essentially a middle man for the entire healthcare sector, helping to manage, improve, and lower healthcare costs.3 Given its size (62% of addressable healthcare spending) and centrality, it’s worth examining a number of macro trends that point to long-term growth potential.4

Legislative tailwind: In one of the biggest industry surprises this cycle, the ACA has added over 15 million newly insured and by most estimates added roughly $40 billion in recurring industry revenue — turning out to be a tailwind, not a headwind as feared.5 As a result, equity multiples rebounded alongside improving operating fundamentals. A secondary potential tailwind is tax reform. The managed care industry faces one of the highest effective tax rates, meaning any tax cuts could have a larger benefit to managed care than to other, lower-taxed sectors.

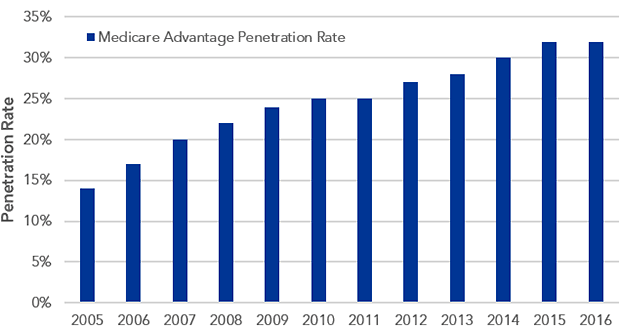

Demographics are destiny: Few sectors stand to potentially benefit from aging demographics as much as healthcare, in our view. Over 10,000 baby boomers age into Medicare each day, and while the commercial market is largely saturated, the federal insurance program remains a growth opportunity for the managed care industry. Medicare spending is roughly 20% (or roughly $650 billion) of total healthcare spending, yet Medicare Advantage (offered by private companies) is only 32% penetrated by managed care companies.5

Cost trends: Healthcare costs are important to monitor as it is a revenue source for healthcare providers, but an expense paid by the managed care space. The good news is the cost-conscious shift from fee-for-service to fee-for-value should put structural downward pressure on the pace of cost growth. The steady push to higher out-of-pocket costs may also help move consumers towards lower-cost alternatives. Managed care could also stand to benefit from any change to drug pricing, making it a potentially attractive hedge against risks to biotech and pharmaceuticals.

Medicare remains an underpenetrated potential growth opportunity

Role in a portfolio

Demographics and managing health care costs are two long-term trends likely to outweigh political uncertainty, in our view. In an uncertain health care policy environment, a complementary focus on biotech and managed care sectors can help investors build an exposure covering both defensive and growth opportunities.

1 Thomson Reuters, as of Sept 26, 2017.

2 Food and Drug Administration.

3 Centers for Medicare and Medicaid Services.

4 Note: Total addressable healthcare spending is $2.1 trillion. Managed care companies service $1.3 trillion (62%), leaving an $800 billion untapped market opportunity ($430 billion in Medicare, $386 billion in Medicaid).

5 Centers for Medicare and Medicaid Services.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

This material represents an assessment of the market environment as of the date indicated; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any issuer or security in particular.

The strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective.

The information presented does not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy or investment decision.

This document contains general information only and does not take into account an individual's financial circumstances. This information should not be relied upon as a primary basis for an investment decision. Rather, an assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a financial advisor before making an investment decision.

Funds that concentrate investments in specific industries, sectors, markets or asset classes may underperform or be more volatile than other industries, sectors, markets or asset classes and than the general securities market.

The iShares Funds are not sponsored, endorsed, issued, sold or promoted by Barclays, Bloomberg Finance L.P., BlackRock Index Services, LLC, Cohen & Steers Capital Management, Inc., European Public Real Estate Association ("EPRA®"), FTSE International Limited ("FTSE"), India Index Services & Products Limited, Interactive Data, JPMorgan Chase & Co., Japan Exchange Group, MSCI Inc., Markit Indices Limited, Morningstar, Inc., The NASDAQ OMX Group, Inc., National Association of Real Estate Investment Trusts ("NAREIT"), New York Stock Exchange, Inc., Russell or S&P Dow Jones Indices LLC. None of these companies make any representation regarding the advisability of investing in the Funds. With the exception of BlackRock Index Services, LLC, who is an affiliate, BlackRock Investments, LLC is not affiliated with the companies listed above.

Neither FTSE nor NAREIT makes any warranty regarding the FTSE NAREIT Equity REITS Index, FTSE NAREIT All Residential Capped Index or FTSE NAREIT All Mortgage Capped Index; all rights vest in NAREIT. Neither FTSE nor NAREIT makes any warranty regarding the FTSE EPRA/NAREIT Developed Real Estate ex-U.S. Index, FTSE EPRA/NAREIT Developed Europe Index or FTSE EPRA/NAREIT Global REIT Index; all rights vest in FTSE, NAREIT and EPRA."FTSE®" is a trademark of London Stock Exchange Group companies and is used by FTSE under license.

The Funds are distributed by BlackRock Investments, LLC (together with its affiliates, "BlackRock").

©2017 BlackRock, Inc. All rights reserved. BLACKROCK, BLACKROCK SOLUTIONS, BUILD ON BLACKROCK, ALADDIN, iSHARES, iBONDS, iSHARES CONNECT, FUND FRENZY, LIFEPATH, SO WHAT DO I DO WITH MY MONEY, INVESTING FOR A NEW WORLD, BUILT FOR THESE TIMES, the iShares Core Graphic, CoRI and the CoRI logo are registered and unregistered trademarks of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

298543

Read more commentaries by iShares