The aerospace and defense (A&D) industry has captured investors' attention following President Trump’s election, rising geopolitical tension, and potential tax reform. Many of the A&D industry’s fundamental drivers have been in place long before these recent developments. However, these recent developments may offer upside optionality yet are not solely reliant on political outcomes. A steady improvement in existing long-term fundamentals and new fundamental catalysts, in addition to policy developments, may warrant a closer look by investors

Aerospace and defense led markets sharply higher following Trump’s election and the idea of fiscal stimulus – lower taxes, higher defense spending - it ostensibly promised. However, as political headwinds continued to mount this year, markets began to price out fiscal stimulus and “Trump Trade” began to unwind, leaving many advisors to ask, “What now?” Investors may want to consider the following:

- Longer cycles, more growth potential

- New buyers

- Shifting line items in the DoD budget

- Valuations may have room to run

- Aerospace & defense relative performance

Aerospace & defense relative performance

Aerospace

Airline service has deservedly gotten a bad rap, but we believe the aerospace industry has a lot going for it. The sector can be divided into two segments, original equipment manufacturers (OEMs) and industry suppliers. Overall, the sector has grown faster than nominal GDP, has maintained consistent pricing, and has kept new entrants at bay with highly technical intellectual property.

Longer cycles, more growth potential: OEMs have benefitted from a long, secular growth trend since the 1980s. While OEM growth cycles have historically been short and sharp in magnitude, they have lengthened over time. Indeed, since 9/11 the industry has been in a ‘super cycle,’ as aircraft shortages, emphasis on fuel efficiency, and the rise of new emerging and low-cost air carriers have driven orders. Large backlogs at OEMs have continued to grow (albeit at a slower pace). Meanwhile, suppliers’ returns have consistently outpaced even OEMs due to higher aftermarket content for used parts, lower upfront investment, and lower program risks. Although aftermarket growth has slowed to high single digits, it has continued to track nominal GDP. What’s more, global traffic, measured as revenue passenger mile (RPM), has grown about twice as fast as nominal GDP over the past 40 years.1

New buyers: The mix of air traffic has shifted dramatically in recent years towards regional carriers in the developing world, particularly Asia and the Middle East, where they serve a rising middle class. In 2000, the U.S. and Europe accounted for 65% of the 2 trillion in global RPM. By 2025, the U.S. and Europe are estimated to account for just 44% of the 5.1 trillion in global RPM.2

Defense

Aerospace isn’t the only U.S. industry that has seen international demand driving growth. U.S. military spending is roughly a third of the $1.7 trillion global defense market.3 However, the question going forward is what will the U.S. military look like under the Trump administration.

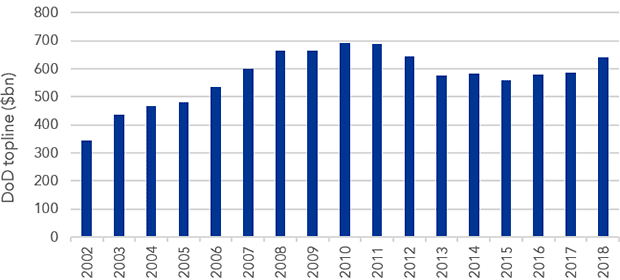

Shifting line items in DoD budget: Early signals suggest that increasing the defense budget will remain a priority for the current administration. Heavyweights in the industry are quite dependent on the U.S. government for their revenues, but there has been a recent shift in focus. Following the 2013 budget sequestration, the Department of Defense (DoD) has prioritized capability over capacity. We believe the emphasis on capability may bode well for industry revenue, as manufacturers have been forced to deliver efficiency gains, and defend or increase margins in the leaner years. The government is having another, less direct impact on defense spending, namely an increase in demand for weaponry and tech as geopolitical tensions rise.

Valuations may have room to run: Defense spending growth is likely to continue under the Trump administration, in our view. Thus, the rise in price-to-earnings multiples for the group may be justified, as spending is sticky and somewhat predictable in the short run. Other factors are harder to predict, however. From a balance sheet perspective, any relief from potential tax reform and flexibility on capital spending deductions may be a boost, while higher interest rates may help ease pension liabilities; that said, we believe even stable or lower rates should make their historically stable dividends increasingly attractive.

Department of Defense topline spending increasing 9% from 2017 to 2018

Role in a portfolio

The Aerospace and Defense sector comprises a broad mix of companies with unique super-trends that historically helped their performance. This can help add diversification benefits as part of the industrials sector within a cyclical basket. U.S. government policy has a big impact on the sector, and the current administration makes a good upside case, in our view. Any downside will be determined by spending patterns and emerging market demand, although both have been stable and are structurally improving at the moment. Regardless of the outcomes of such large unknowns, macro patterns like the growing emerging market middle class, shifts in global defense budgets and the impact of technology and efficiency, have made Aerospace and Defense stocks a sector to consider in a long-term portfolio.

1 Airline Monitor.

2 Airline Monitor, World Bank.

3 International Peace Research Institute

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

This material represents an assessment of the market environment as of the date indicated; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any issuer or security in particular.

The strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective.

The information presented does not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy or investment decision.

This document contains general information only and does not take into account an individual's financial circumstances. This information should not be relied upon as a primary basis for an investment decision. Rather, an assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a financial advisor before making an investment decision.

Funds that concentrate investments in specific industries, sectors, markets or asset classes may underperform or be more volatile than other industries, sectors, markets or asset classes and than the general securities market.

There is no guarantee that dividends will be paid.

Diversification and asset allocation may not protect against market risk or loss of principal.

The Funds are distributed by BlackRock Investments, LLC (together with its affiliates, "BlackRock").

©2017 BlackRock, Inc. All rights reserved. BLACKROCK, BLACKROCK SOLUTIONS, BUILD ON BLACKROCK, ALADDIN, iSHARES, iBONDS, FACTORSELECT, iTHINKING, iSHARES CONNECT, FUND FRENZY, LIFEPATH, SO WHAT DO I DO WITH MY MONEY, INVESTING FOR A NEW WORLD, BUILT FOR THESE TIMES, the iShares Core Graphic, CoRI and the CoRI logo are registered and unregistered trademarks of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

294442

Read more commentaries by iShares