“It’s the end of the world as we know it, and I feel fine.”

- E.M.

Value investing is under attack. The US equity market is at its most expensive level in history1 and has spent most of the past six years in the top quintile of expensive.2 In addition, value equities have underperformed the broad market and more widely growth equities for over ten years. Yet, value investing is a principle-based process backed by well over one hundred years of empirical data and sound logic. The style has gone through fallow periods before, but the current famine is surely one of the longest. Still, we remain confident that value investing’s principles are eternal and they will prove so as the current cycle turns – whenever that may be. Nonetheless, we recognize the length of the current cycle makes what is always a difficult process to maintain almost untenable. This has led us on a multi-year quest to refine our own value-oriented process to become more robust and open to a greater breadth of environments while maintaining the core of the value framework.

We spent the bulk of our last quarterly letter3 discussing the very real link between asset class valuations and prospective returns. It is a familiar topic in these communications the past few years. Some might say we beat the horse dead many letters back. Yet, it is critically important. While valuation provides no indication of asset class return over the next 1, 3, or even 5 years, it becomes exceedingly explanatory over 7, 10, and 12-year periods.

As a reminder, by some measures (price to sales), the S&P 500 is more expensive now than it has ever been in measured history, and thus prospective returns are very low. As of September 30, 2017, GMO forecasts a -4.1% annualized real return for large capitalization US equities over the next 7 years!4 To put this in perspective, if the forecast is correct and you invested $1000 in large capitalization US equities today, you would have approximately $750 in 2017 dollars towards the end of 2024.

With that brief reminder concerning the broad US equity market, this quarter we are going to discuss portfolio construction a level or two below the asset allocation decision. Once we decide to allocate to equities (for example), we need to decide which equities. For Grey Owl Capital Management, just as we focus on valuation at the asset class level, we focus too on valuation at the individual security level. Rather than buy a broad equity index, we aim to buy equities that afford a value orientation (i.e. are “cheap” and offer a “margin of safety”).

The historical record demonstrates that moderating exposure to broad asset classes (e.g. US equities) as they become more expensive and, within asset classes (e.g. US equities), focusing on those securities that are statistically “cheap” works. These tactics have improved returns and limited downside volatility for the last one hundred years of available data. Unfortunately, improved performance comes with a cost, one we are all quite familiar with today. The trade-off or cost to employing these value-tactics is that they can underperform fully invested equity indices for multiple years at a time. And, for the last several years, they have.

Is Value Investing Dead?

“Is Value Investing Dead? It Depends on How You Measure It.” That was the title of the September 24, 2017 Wall Street Journal blog, The Experts, Wealth Management.

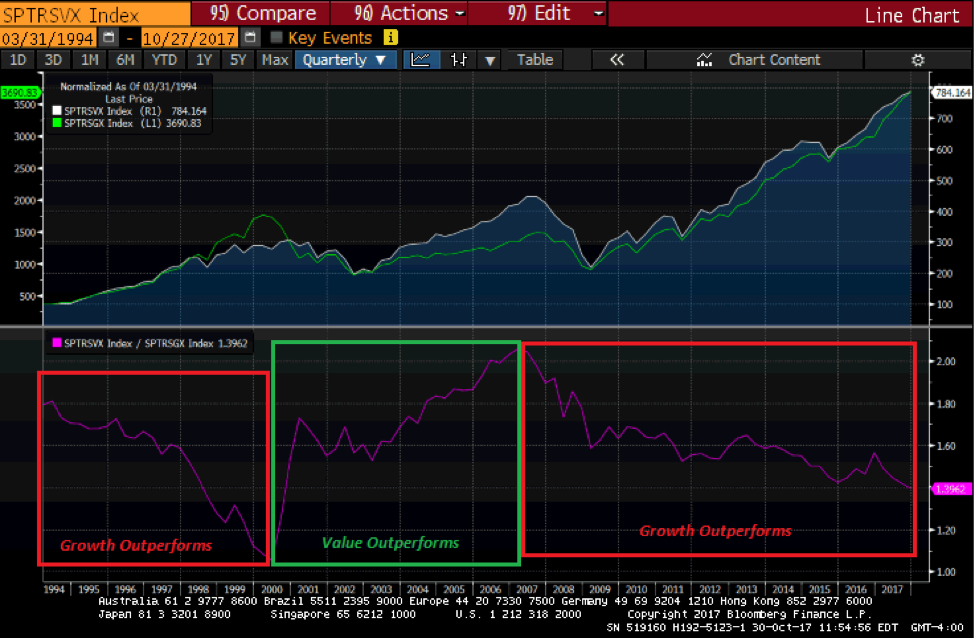

If you measure it the way Standard & Poor’s does, “value investing” certainly appears to be on life support. The chart below shows both the S&P 500 Value Index (white in the top panel) and the S&P 500 Growth Index (green in the top panel) for the period from March 1994 through the last full week in October 2017. The purple line in the bottom panel shows the ratio of the two. When the purple line is rising, value is outperforming. When the purple line is declining, growth is outperforming. For the last ten years, growth has significantly outperformed value.

Yet long-term data show that value eventually outperforms. For example, in Rethinking Conventional Wisdom: Why Not a Value Bias?5 Research Affiliates looks at data from 1962-2015 and shows that a “value” portfolio outperformed the S&P 500 by 1.8% annualized over that full period.

Extended value underperformance is not new. For the five years from 1995 through 1999, S&P 500 Value underperformed the S&P 500 on a total return basis by a cumulative 25%. Then, from 2000 through 2006, S&P 500 Value outperformed the S&P 500 by a cumulative 34%. Now, growth has gone on an extended, 10-year tear and through the end of 2016 was outperforming value by over 12% cumulative. This recent period is not unique. In the Research Affiliates study, 26% of the time the “value” portfolio was behind on a rolling 3-year basis.

Time Horizon

We have discussed the concept of time horizon before, but it too is worth revisiting in the context of the 10-year, value-style underperformance. Time horizon means the period over which someone evaluates the performance of a particular activity, for instance, an investment manager or investment style.

As we describe above, value-investing works – it outperforms, but it comes at a cost: years of underperformance relative to an index (e.g. the S&P 500) and other styles (e.g. growth). Value investing requires a long (sometimes very long) time horizon.

As you know, Grey Owl Capital Management employs a value-oriented process with the expectation that the process will outperform over a full-investment cycle (market peak-to-peak or trough-to-trough). We probably reinforce that concept in these quarterly discussions to excess. Due to convention and clients’ reasonable need for transparency, we also communicate performance on a quarterly basis. This inherently introduces a conflict. Typically, the cycle is such that the conflict lasts for only a short period. The recent period has been so long it unsurprisingly adds greater tension to the time horizon challenge.

The current cycle would test the patience of Job. Two pillars of the Grey Owl Capital Management process, moderating exposure to the equity asset class as valuations become stretched and focusing individual security selection on value-oriented securities have both been out of favor for years. No matter clients’ initial time horizon intention, one cannot help but shift toward scrutinizing a shorter period (something less than a full cycle). We recognize (and feel) the pain and thus have and continue to work extensively on enhancing our approach to mitigate this conflict going forward while at the same time maintaining the necessary components of the existing process so that we have the opportunity to harvest the “value alpha”6 down the road.

Root Causes of the Current Cycle

An important step to improving a process is to study the environmental factors that have caused it to deviate or stretch historical precedents. Given the length of value’s recent underperformance, it is worth investigating why the current environment favors growth. In Goldman Sachs Mulls the Death of Value Investing7 from June 2017, Bloomberg does just that, coming up with…

Two plausible explanations:

- Slower economic growth (we remain in the slowest economic expansion in US history) and the eventual consensus that growth will in fact be “lower for longer” has increased investors’ appetites for scarce growth.

- Continued asset purchases by the Federal Reserve and other global central banks has lifted valuations uniformly. For example, “the distribution of price-to-earnings multiples among S&P 500 companies tightened to ‘historical extremes’ in 2013.”

We will add a third reason:

- The ongoing shift from active to passive management creates a constant bid for all securities with no regard for price and value. Passive investing just buys the “market.” There is no consideration for the relationship between the price of the market or any individual security and reasonably expected future cash flows to the investor.

If the above factors do in fact explain why value has underperformed for so long, can we expect value to stage a comeback anytime soon? It is hard to say. The academic theories for value’s long-term outperformance are still sound. Cheap businesses are typically in sectors under siege (think traditional brick and mortar retail today). In addition, the market is not perfectly efficient so some businesses in these “risky” sectors get too cheap (are “mispriced”). There is nothing to argue that the overlapping concepts of compensation for additional “risk” and mispricing have been eliminated. That leaves us with a basic understanding of why we have experienced an elongated cycle, a belief that value still has merit, but a concern that the cycle may continue for longer.

Momentum

Efforts to improve our existing investment process through question and study led us to examine what many believe is the antithesis of value investing: momentum.

Like value, momentum is an investment approach that demonstrates historical success, outperforming capitalization-weighted indices over long periods and across numerous markets and geographies. Unlike value, which is long-term oriented, momentum is essentially a short-term strategy. While the value investor buys an asset he deems cheap (either quantitatively or qualitatively) and expects over time the market will come to the same conclusion, the momentum investor buys an asset that is already performing well (with no regard for long-term value) in the expectation that the asset will continue to do well because of human behavioral/emotional traits.

Most interesting for the value investor is that while consensus wisdom holds that momentum is in direct conflict with value, it turns out momentum can be viewed as very much a compliment to value. Empirical evidence shows that both value and momentum outperform the market over time and they are negatively correlated, so when combined, they enhance a portfolio. From a client’s perspective, adding momentum to a value portfolio will also smooth out periods of over/under performance and make the ride a little easier to tolerate without giving up the opportunity for outperformance. As such, we will add exposure to the momentum factor in the future (via individual equities or using low-cost, exchange traded funds (ETFs) that track a momentum index.)

Summary

Something exceptional is going on. The current investment cycle is longer and more extreme than almost all past cycles. Central bank activity, demographic changes, and technological advances, are perhaps resetting norms (at a minimum they test investors’ patience). Today we discussed an extended period of growth outperforming value at the individual security level. In past letters, we discussed the prolonged overvaluation of the US equity market as a whole. All of this means that the traditional value investor is under assault. However, it does not mean that a value investor must abandon ship. Rather, we believe the value philosophy is still sound, but could benefit from some modifications/enhancements – the momentum complement discussed above being one. We discuss four enhancements to the Grey Owl Capital Management process below.

Implications for Grey Owl

Process refinement is a continual effort, but sometimes it warrants more aggressive attention. We have certainly been spending a lot of time on the issue. We have touched on enhancements/modifications in the past and here are a few more:

- Traditionally, we have fished in the value pond of low price-to-earnings and price-to-book ratios. That is too limiting. More recently, we have expanded our purview to include excellent businesses that may at first blush appear statistically expensive. Many will in fact be overvalued, but some will likely warrant a price-to-earnings ratio of 30, 40, or even 50.

- Recognize that optionality may be the hardest-to-price asset factor, and thus the most prone to being underpriced (value). Traditional value investments are often companies with little room for growth. Think a tobacco company with shrinking markets, paying a high dividend, and maintaining very low growth due to pricing power. Compare that to a company that sells books online and has a plan to grow into a broad online retailer. It is easy to draw a box around the tobacco company’s future, not so much the ecommerce firm. Nevertheless, the ecommerce firm’s growth optionality has value and it should not be dismissed out of hand.

- Because value can underperform for so long, a balanced portfolio should incorporate momentum, as a compliment. Momentum is anathema to the typical value investor and therein may lie the opportunity.

- Historically, we have constructed portfolios in a two-step process. Decide on the allocation (e.g. stock vs. bonds) based on asset class valuation. Then, fill up the (e.g. equity) allocation with individual securities. We have expanded our approach to look at an in-between level – sectors and geographies. (This topic could fill an entire letter in and of itself.) Today, when value exists at the sector or geography level, we will own exchange traded funds (ETFs) until we find an individual security in that bucket that offers a better opportunity. Our recent purchases of index ETFs representing Europe, Asia, Far East (EFA) and emerging markets (EEM) are examples of this new process enhancement.

We maintain confidence that our value-oriented approach will prove sound over a full cycle. However, we still do not know when the cycle will turn. In the meantime, we believe value’s current underperformance has afforded us an opportunity to enhance our process. It is now more robust and open to a greater range of environments and we will continue to improve it every day. The investment management business is highly competitive and challenging. It is equally challenging to be an investor that entrusts their savings to a manager and process that is different. In the short-run, passive, index investing is a much easier approach to stomach. The risks are hidden, but they are real. Thank you for your continued trust.

*****

As always, if you have any thoughts regarding the above ideas or your specific portfolio that you would like to discuss, please feel free to call us at 1-888-GREY-OWL.

*****

Sincerely,

Grey Owl Capital Management

Grey Owl Capital Management, LLC

This newsletter contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves the potential for gains and the risk of losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Any information prepared by any unaffiliated third party, whether linked to this newsletter or incorporated herein, is included for informational purposes only, and no representation is made as to the accuracy, timeliness, suitability, completeness, or relevance of that information.

The stocks we elect to highlight each quarter will not always be the highest performing stocks in the portfolio, but rather will have had some reported news or event of significance or are either new purchases or significant holdings (relative to position size) for which we choose to discuss our investment tactics. They do not necessarily represent all of the securities purchased, sold or recommended by the adviser, and the reader should not assume that investments in the securities identified and discussed were or will be profitable. A complete list of recommendations by Grey Owl Capital Management, LLC may be obtained by contacting the adviser at 1-888-473-9695.

Grey Owl Capital Management, LLC (“Grey Owl”) is an SEC registered investment adviser with its principal place of business in the Commonwealth of Virginia. Grey Owl and its representatives are in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which Grey Owl maintains clients. Grey Owl may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements. This newsletter is limited to the dissemination of general information pertaining to its investment advisory services. Any subsequent, direct communication by Grey Owl with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of Grey Owl, please contact Grey Owl or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov).

For additional information about Grey Owl, including fees and services, send for our disclosure statement as set forth on Form ADV using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

1 Measured by price-to-sales.

2 Measured by the cyclically adjusted price earnings (CAPE) ratio since 1871 using Robert J. Shiller’s data.

3 http://www.greyowlcapital.com/uploads/letters/GOLetterQ22017.pdf

4 https://www.gmo.com/docs/default-source/research-and-commentary/strategies/asset-class-forecasts/gmo-7-year-asset-class-forecast-(3q2017).pdf?sfvrsn=3

5 https://www.researchaffiliates.com/en_us/publications/articles/560_rethinking_conventional_wisdom_why_not_a_value_bias.html

6 Alpha refers to outperformance compared to a benchmark; typically a passive index.

Read more commentaries by Grey Owl Capital Management