The End of QE Didn't Kill The Bull Market. The Start of QT Won't Either

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSummary: Quantitative Easing (QE) ended 3 years ago today. This was widely expected to mark the end to the bull market (post). Instead, US stocks have risen another 37%.

Why was this view wrong? In truth, the narrative about the Fed's policy has shifted over time as equities have risen. As late as 2012, QE was viewed as bearish. Into 2014, it was only the continued QE inflows that were considered bullish. When stocks kept rising after QE ended, the narrative shifted to the large Fed "balance sheet" and then to global central bank actions.

The Fed's policies have clearly led US equities higher, but not in the way that it has been popularly perceived. The Fed established the conditions for fundamental growth in consumption, investment, employment and corporate profits, creating the confidence in investors to place their cash into the financial markets. All of these factors have a strong causal relationship to share price that long pre-date 2009 and the QE programs.

The Fed will now embark on a reduction of its balance sheet (QT). This appears to be the most pivotal event facing markets in 2018. But it stands to reason that so long as the positive fundamental conditions continue, US equities can be expected to remain firm.

None of this implies that the US equity market will continue to appreciate without any interim drama. As noted in the charts that follow, investor sentiment is very bullish and equity valuations are very high. Since 1980, it has been normal for the S&P to correct by an average of 10% during the course of each year of a bull market. With the last correction of that magnitude starting 2 years ago, one of that magnitude, or larger, is arguably overdue in the coming months. That, not the tapering of the Fed's balance sheet, is the relevant risk for investors to focus on in 2018.

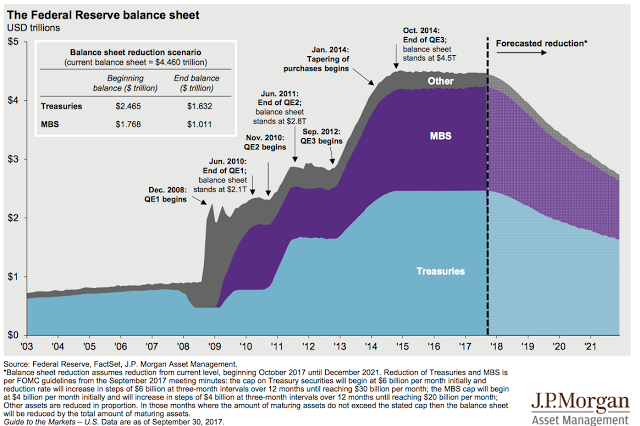

On September 20th, the Fed formally announced that it will begin to reduce its balance sheet, primarily by ceasing reinvestment from maturing bonds. This process is being termed "Quantitative Tightening" (QT) as it is the reverse of the bond buying program known as Quantitative Easing (QE).

QT will begin slowly, with a reduction of just $10b per month during the first 3 months. If there are no major market disruptions, then the pace of QT will be increased by $10b per month every quarter. To put that in perspective, $10b equals 0.2% of the Fed's total assets. By the end of the year, the Fed's balance sheet will have been reduced by less than 1% (from JPM). Enlarge any image by clicking on it.

It is a massive understatement to say the Fed's role in the 9 year bull market is a source of contention. This post examines the Fed's role in the bull market and the two primary ways QT could affect US equities.

1. Balance Sheet Reduction

The first way QT could affect US equities is based on the following premise: US equities rose as the Fed's balance sheet expanded and will therefore fall when the balance sheet is reduced. In other words, the current bull market is mostly a fabrication of the Federal Reserve printing money (QE) and then forcing that money into the stock market.

As evidence, supporters of this view show how QE, the Fed's balance sheet and stock prices have risen together since 2009 (we'll call this the "balance sheet chart").

Behavioralists will quickly recognize that the balance sheet chart as a prime example of "framing." A recent post on how framing is frequently used to mislead readers is here. A modestly experienced investor knows that stock markets are not driven by a single factor; by presenting only two variables in isolation, the balance sheet chart uses framing to force the reader to make the mental effort to fill in the missing data. The human mind resists making this effort, so it interprets the chart as "what you see is all there is."

Have stocks risen with the Fed's actions? Of course. But the correlation implied by the balance sheet chart is much less than it appears. Consider the following:

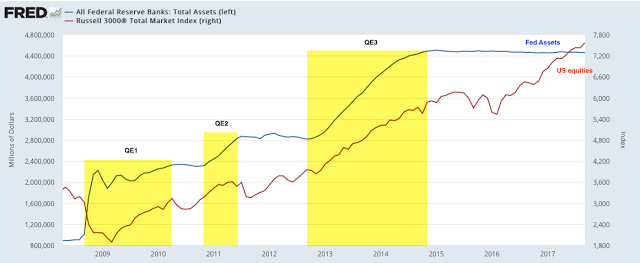

QE1 was announced in late November 2008. After the first three months, the S&P was 22% lower, a bear market by the most common definition.

The S&P rose 10% during QE2. But it also rose 10% after QE2 ended and before QE3 began, a time during which the Fed's balance sheet shrank.

The S&P rose an impressive 43% during QE3. But it has risen an equally impressive 37% since QE3 ended in October 2014, during which the balance sheet shrank.

The S&P rose about 1000 points during QE1, 2 and 3 (4 years). The S&P has risen about 700 points between and after the QE programs (which ended 3 years ago).

So the S&P rose during the Fed's QE programs, but also rose in-between those programs and has risen much more since those programs ended. There were sharp sell offs both during QE and after QE. This is a weak example of correlation and makes a poor case for arguing direct causation.

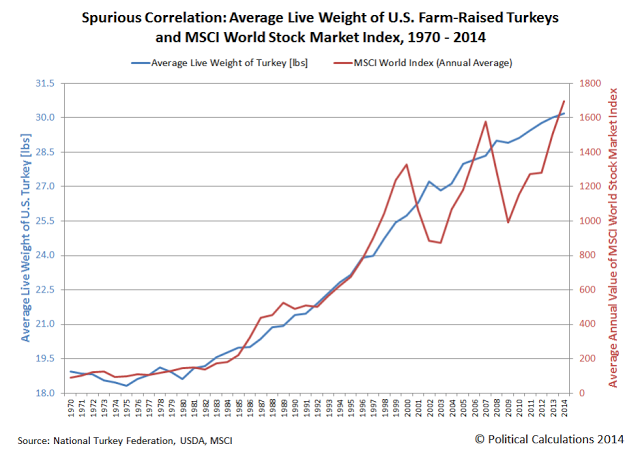

In fact, the S&P has a better correlation over much longer periods of time with several macro and financial factors, which we will detail in a minute. Note, too, that the S&P has a very high correlation to the average weight of turkeys (r-squared of 96%), an example of how even a good correlation is not proof of causation.

In truth, there is substantial "hindsight bias" built into the balance sheet chart. Many of the savviest investors did not believe the Fed would create an equity bull market until it was already several years old. The balance sheet chart was fashioned after the fact to explain a bull market that many hadn't expected.

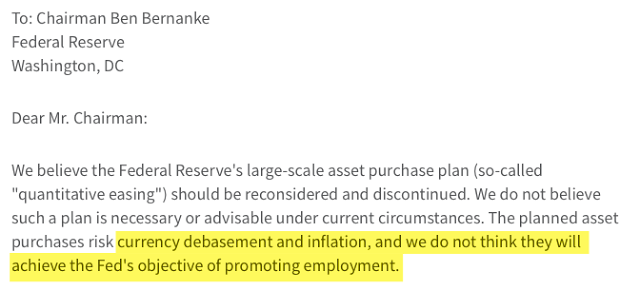

For example, in November 2010, two years after QE1 was launched, Jim Chanos, Cliff Asness, Richard Bove, James Grant, Seth Klarman, Paul Singer and many others wrote an open letter to then Fed chairman Ben Bernanke, warning that the QE program would lead to hyper inflation, surging interest rates and a dollar crash, conditions under which equity markets would fall hard (that letter is here).

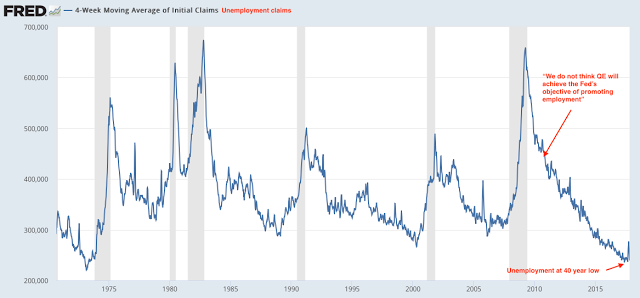

All of this proved to be wrong. Core inflation has steadily remained near 2%, interest rates have moved lower than prior to QE2 and the dollar gained 10% in the next year and 30% in the next 4 years. Economic growth has been fine with unemployment claims steadily falling to the lowest level in more than 40 years.

These investment professionals were expressing the consensus view that prevailed well into 2012, that the QE program was bearish. Investment managers surveyed by BAML were 40% underweight equities in early 2009 and held one of the highest proportions of cash in the survey's history. That was also true as QE3 was starting in September 2012. In neither case did investment professionals view the Fed's actions as obviously bullish. That narrative was crafted in hindsight (from BAML).

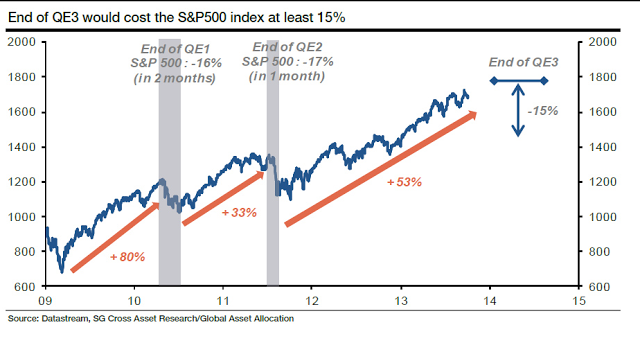

Having earlier missed the link between the Fed's policy and asset prices, by 2014, respected investors like Jim Bianco (and many others) graduated to a new narrative: the QE inflows had caused the bull market. They now, therefore, expected the end of QE3 in October to be a "profound negative for equity prices" (here).

Analysts at SocGen expected the SPX to fall at least 15% to 1500 when the QE3 inflows ended. Instead, stocks rose another 8% to 2130 over the next 9 months.

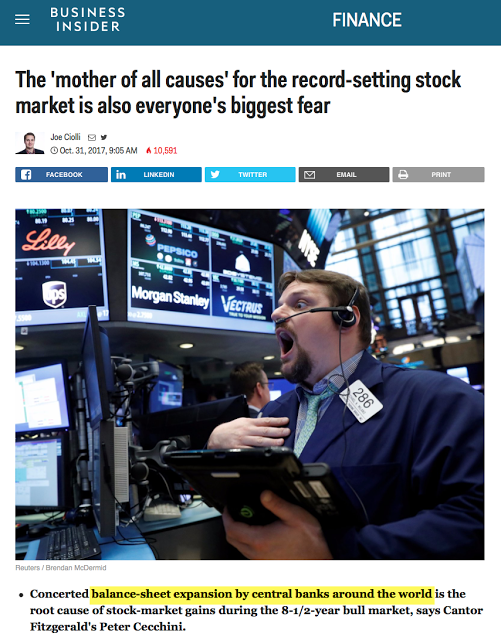

Since the end of QE3 three years ago, the narrative has again been forced to change in order to explain the continued rise of equities without any additional inflows from QE. The new narrative is that it is global central bank balance sheets, including the Fed's, which is driving US equities higher (from Business Insider).

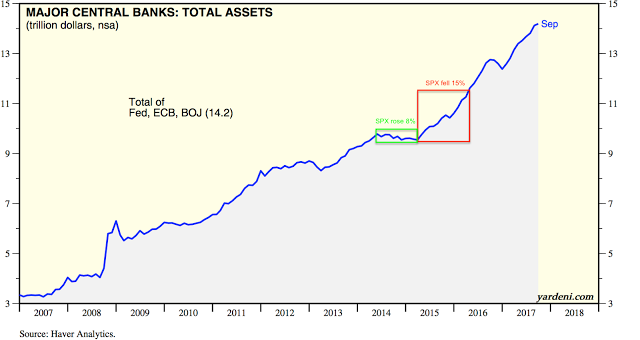

Leave aside the strange logic of European and Japanese bankers wanting to create a wealth effect outside their own country, the evidence suggests this is narrative is also wrong. For example, from the middle of 2015 to February 2016, US stocks fell 15% - a big and long enough fall for many to consider it a bear market - yet during this time, global central bank balance sheets increased by $2 trillion (red box). In the prior 12 months, those central bank balance sheets declined in size, yet US stocks rose 8% (green box). There is no correlation here (from Yardeni).

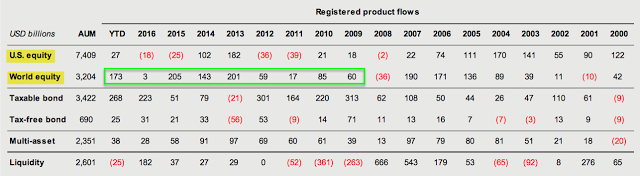

Four times more money has flowed into non-US equity mutual funds and ETFs than into the US, and those flows have been greater every year. US equity flows were negative in 2015 and 2016 and have been exceedingly modest so far in 2017. In short, there is no evidence that "excess liquidity" from Europe and Japan is flowing into the US (from JPM).

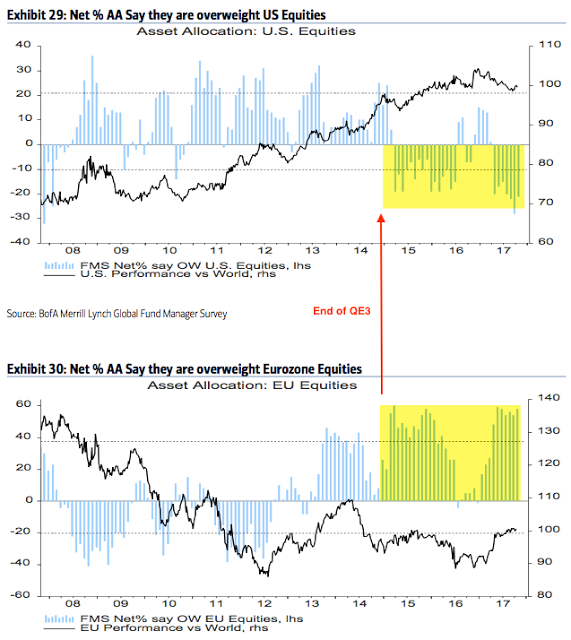

Since the end of QE3, global fund managers have been consistently overweighting Europe (lower panel) and Japan and underweighting the US (upper panel). The US has outperformed the rest of the world by 17 percentage points despite expectations that global central banks (or other factors) would lead non-US markets to do better (from BAML).

None of this is to say that the Fed's QE program was ineffective or that it did not lead to a rally in US equities. On the contrary, it's been hugely successful, but the mechanism is different than what is popularly assumed. This provides the best explanation for how the Fed ignited the bull market.

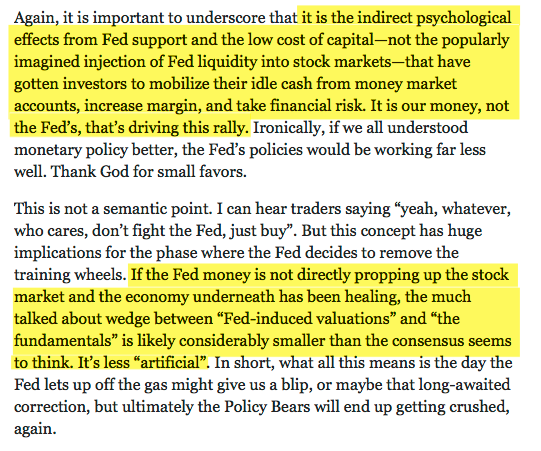

As Mark Dow explains, it isn't the Fed's money (i.e., QE inflows or its balance sheet) that's driven the bull market; instead, the Fed created an environment that motivated investors to invest their cash (his post is here).

Mr. Dow's assertions are backed by the evidence.

Start with investor sentiment. At the equity low in March 2009, only 10% of those surveyed by the University of Michigan expected stock prices to be higher in a year. This was an extraordinarily pessimistic view. It has since risen to more than 60%. There is a very clear (and, yes, troubling) correlation to equity prices, indicating that investors have in fact, "mobilized their idle cash to take financial risk" (from Dana Lyons).

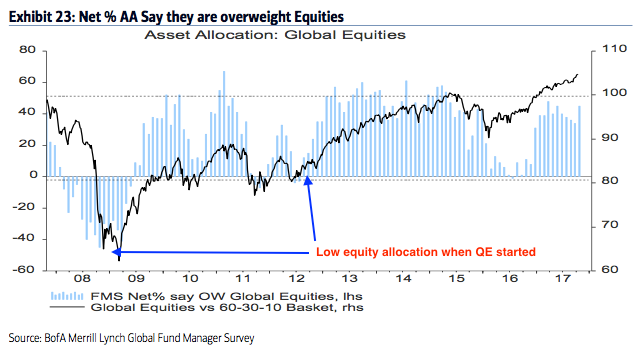

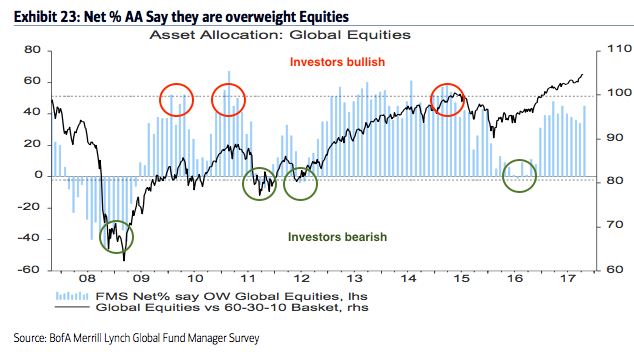

Likewise, professional money managers went from exceedingly underweight equities in early 2009 to quite overweight equities, corresponding to the rise in the market. In fact, the peaks in the S&P in 2010, 2011 and 2015 (red circles), as well the subsequent lows (green circles), are much better explained by the investment allocation of fund managers than by changes in the Fed's balance sheet (from BAML).

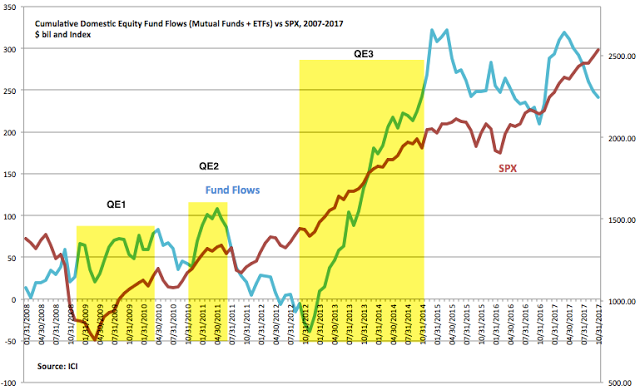

Changes in sentiment mobilize funds for investment. The three phases of QE (yellow shading) generally correspond with the significant net inflow of money (blue line) to mutual funds and ETFs that invest in the stock market (from ICI).

Former Fed Chair Ben Bernanke explicitly acknowledged the importance of improved investor confidence and higher asset prices in spurring fundamental improvements in investment and consumption.

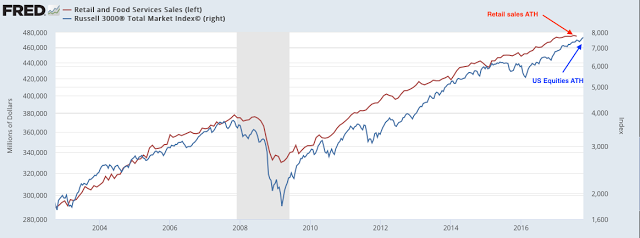

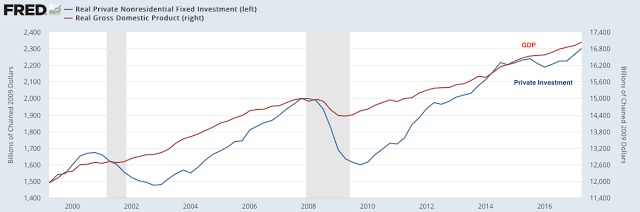

This has been born out in practice. Retail sales - a good proxy for consumer consumption - has risen to new highs along with equity prices. The correlation is not perfect, but very good, and long pre-dates the QE program.

The increase in consumption in turn catalyzed growth in private investment.

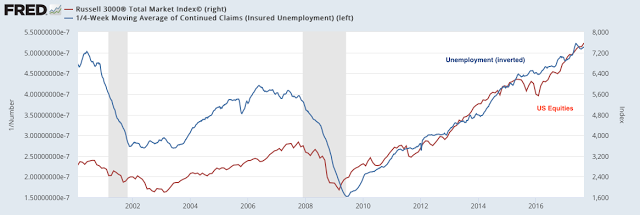

Consumption and investment drive better employment (in a positive, self-reenforcing cycle), which has a long record of being highly correlated with equity prices.

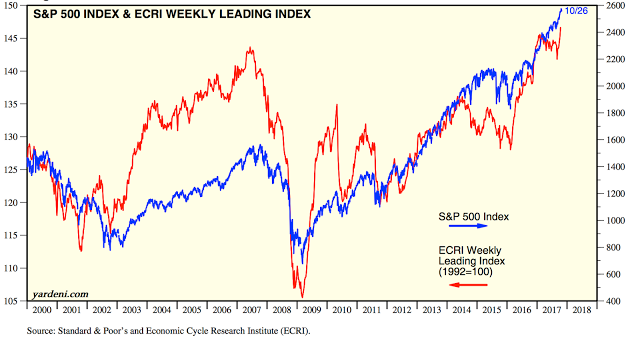

The ECRI's weekly leading index - a weighted composite of 7 economic and market measures including unemployment claims, corporate bond yields, industrial material prices, real estate loans, business failures and real money supply - bottomed in 2009 and is now at a new high. Macro fundamentals have traced the same pattern as equity prices, even dipping together in 2010, 2011 and 2015-16 (from Yardeni).

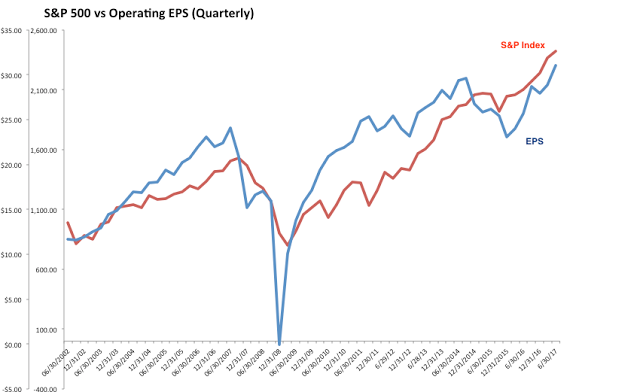

This positive trend in the macro environment has, unsurprisingly, led to a rise in corporate earnings, which also have a long record of being highly correlated with equity prices. The "earnings recession" (due almost entirely to the 75% plunge in oil prices) mostly explains the fall in equities in late 2015 and early 2016, as well as the subsequent rise over the past 20 months A post on this is here.

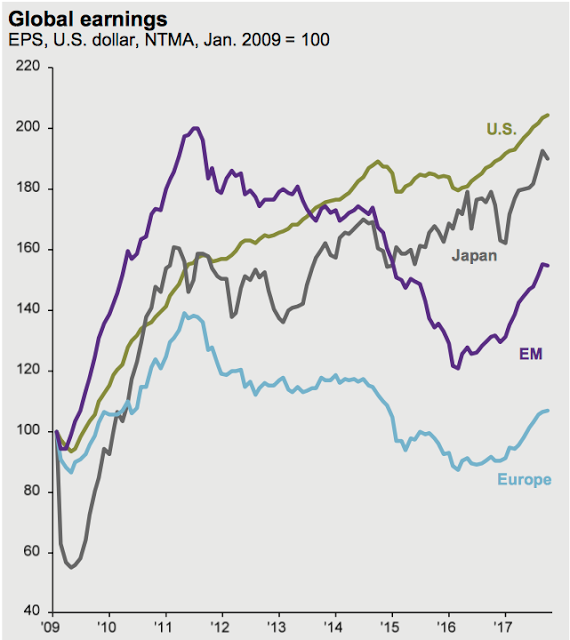

Earnings also helps explain why the US market has outperformed non-US markets since the end of QE in the US and with ongoing QE elsewhere: earnings growth has been better in the US (from JPM).

Equity markets are driven by changes in both fundamentals and valuations. Not surprisingly, valuations express investor confidence. As the economy has mended and corporate profits have grown, valuations have risen (to, yes, levels where 3-5 year forward returns are low).

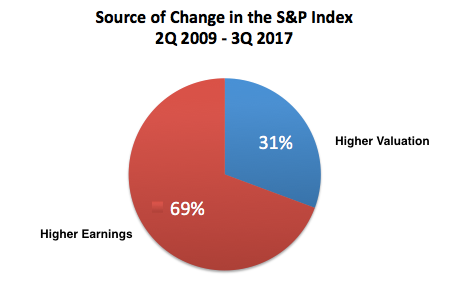

But this has been primarily a fundamentals-driven bull market. In the past 8 years, 69% of the rise in the S&P is explained by GAAP earnings growth, 31% by a valuation increase. Less than 3 percentage points of earnings growth has come from share reductions (e.g., corporate buybacks). In comparison, 75% of the gain in the S&P between 1982-2000 was derived from a valuation increase (that data from Barry Ritholtz; other data and the chart below from S&P).

In summary, the increase in the Fed's balance sheet has clearly led US equities higher, but not in the way that it has been popularly perceived. Objectively, the Fed created the conditions for fundamental growth in consumption, investment, employment and corporate profits, and the confidence for investors to place their cash into the financial markets. All of these factors have a strong causal relationship to share prices that long pre-date 2009 and the QE programs.

It stands to reason that so long as these conditions continue, US equities should be expected to remain firm even as the Fed reduces its balance sheet.

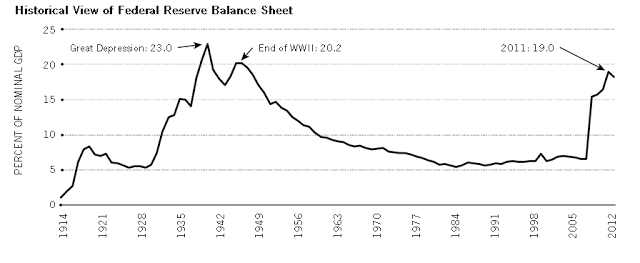

Furthermore, the only prior example of the Fed unwinding its balance sheet did not end badly. In the aftermath of the Great Depression, the Fed's balance sheet swelled to 23% of GDP, the exact same proportion as today. That balance sheet began to shrink relative to the economy starting in 1946. In the next 10 years, GDP per capita grew 2.4% per annum and the S&P grew 6.6% per annum (both measured in real terms; more here). It wasn't an uninterrupted rise - there was a mild bear market and recession for part of 1948-49 - but a new secular bull market was underway.

To be clear, one example from 70 years ago under different circumstances is not proof that reducing the Fed's balance sheet is benign. However, it does show that other factors - not the balance sheet itself - are likely more important determinants of what next happens to the economy and the S&P. As Mark Dow stated: "If the Fed money is not directly propping up the stock market and the economy underneath has been healing, the much talked about wedge between “Fed-induced valuations” and “the fundamentals” is likely considerably smaller than the consensus seems to think. It’s less artificial.”

2. Higher Interest Rates

The second way that the Fed's QT program could affect US equities is through higher interest rates. That narrative works like this: under QE, the Fed bought bonds, lowering their yield and making equities a more attractive investment.

By this logic, the reverse of QE (i.e., QT) should raise yields and make equities less attractive, lowering their price. In other words, the era of equity outperformance is over. But there are at least two problems with this line of reasoning.

The first problem is that yields may not rise strongly during QT. Note that yields rose during each of the 3 rounds of QE, the opposite of what this narrative suggests. Why? Most likely because the Fed was signaling its commitment to spurring economic growth which usually leads to higher prices and thus higher yields (from the WSJ).

To be clear, yields are slightly lower now than they were before QE, and the rise in yields during each round of QE was not dramatic. In between rounds, yields fell, as they did after QE3 ended; again, exactly the opposite of what this narrative suggests. But if you step back and take a long term view, you quickly see that yields have been falling in a clear channel for nearly 4 decades. It is, objectively, too soon to say that a 37 year pattern of falling yields will dramatically reverse. More likely, with modest growth and inflation, it's possible that a long period of yields between 2-4% is ahead. That is our expectation.

That yields rose during QE and are not much changed from when QE started 9 years ago doesn't mean that QE was ineffective. On the contrary, the US economy has added new employment for 83 months in a row, the longest such streak in its history. By signaling its commitment to low rates and higher growth, the Fed stabilized markets that were in hysteria following the financial crisis.

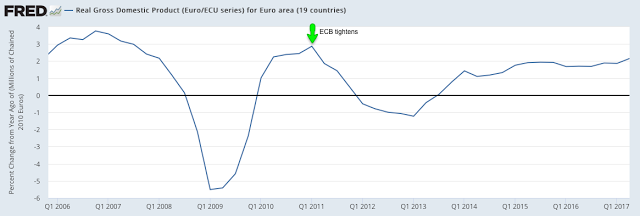

Moreover, the best counterfactual to QE comes from Europe, where the ECB decided to raise rates in 2011, four years before the Fed and too soon after the crisis. The region subsequently fell into a second recession during 2012-13. The negative impact on European growth and inflation is not hard to spot.

The second problem with expecting QT to cause higher yields and thus lower equities is their empirical relationship. During each round of QE, equities rose together with higher treasury yields. In other words, higher growth expectations led investors to buy equities.

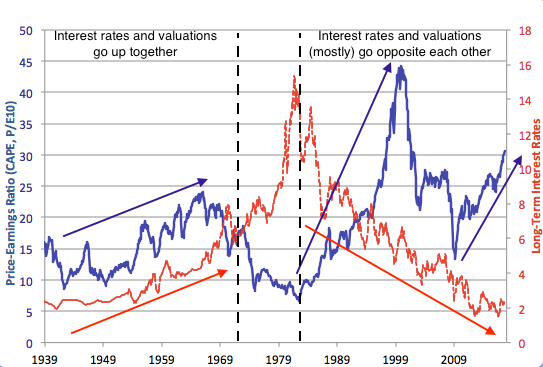

Some might view that as anomalous. After all, valuations have mostly been rising since the early 1980s, during which time interest rates have fallen. These two seem to move opposite each other. But if you were looking at the relationship in 1970, you would have seen the opposite correlation: interest rates had been rising for 30 years, and so had valuations. This made sense to everyone at the time: when the economy and companies are growing faster, there is greater demand for money, so interest rates are higher. And bigger, faster growing profits make companies more valuable, so valuations are higher (chart from Robert Shiller).

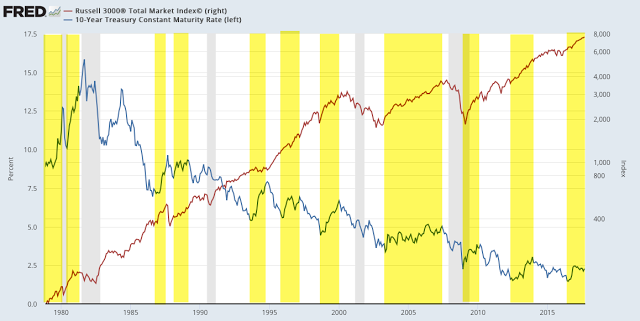

Even over the past 40 years, stock prices (red line) have frequently risen with yields (blue line; yellow shading).

In the chart above, you can see that stock prices have also fallen with yields, and sometimes they have moved in opposite directions. Clearly, interest rates alone are not the dominant determinant of equity prices. Macro growth, earnings growth, valuation and investor sentiment are much more important.

Valuations are also not correlated to interest rates. The conventional wisdom is that a higher discount rate makes company cash flows worth less, hence valuations fall when rates rise. All other things being equal, that might be true. But all other things are not equal since higher rates almost always arise from higher growth.

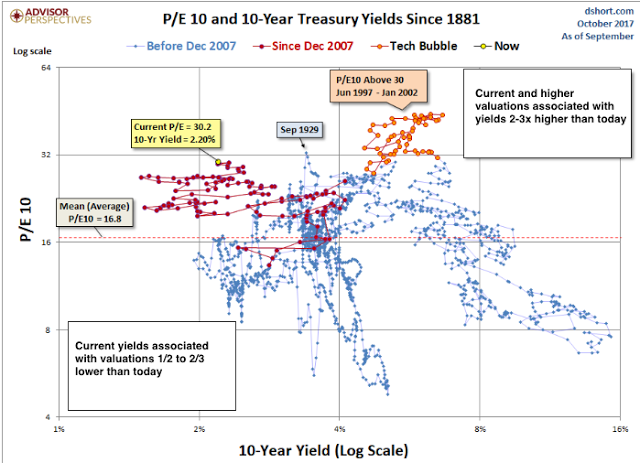

The chart below compares valuations and treasury yields. Current and higher valuations have more often been associated with treasury yields 2-3 times higher than today's. And current yields have more often been associated with valuations that are much lower. There is little discernible correlation between rates and valuations to suggest that higher rates will necessarily cause current valuations to tumble (from Doug Short).

In summary, interest rates are mostly a function of growth and inflation, both of which remain modest. Unless these unexpectedly begin to accelerate, it is likely that the QT program will not, by itself, usher in a period of much higher rates. In any case, equity prices and valuations are not strongly inversely correlated to rates: they often rise together as faster growth makes companies more valuable.

Quantitative Easing ended 3 years ago today. This was widely expected to mark the end to the bull market. Instead, US stocks have risen another 37%.

In truth, the narrative about the Fed's policy has shifted over time as equities have risen. As late as 2012, QE was viewed as bearish. Into 2014, it was only continued QE inflows that were considered bullish. When stocks kept rising after QE ended, the narrative shifted to the large Fed "balance sheet" and then to global central bank actions.

The Fed's policies have clearly led US equities higher, but not in the way that it has been popularly perceived. The Fed established the conditions for fundamental growth in consumption, investment, employment and corporate profits, creating the confidence in investors to place their cash into the financial markets. All of these factors have a strong causal relationship to share price that long pre-date 2009 and the QE programs.

The Fed will now embark on a reduction of its balance sheet. This appears to be the most pivotal event facing markets in 2018. But it stands to reason that so long as the positive fundamental conditions continue, US equities can be expected to remain firm.

None of this implies that the US equity market will continue to appreciate without any interim drama. As noted in the charts above, investor sentiment is very bullish and equity valuations are very high. Since 1980, it has been normal for the S&P to correct by an average of 10% during the course of each year of a bull market. With the last correction of that magnitude starting 2 years ago, one of that magnitude, or larger, is arguably overdue in the coming months. That, not the tapering of the Fed's balance sheet, is the relevant risk for investors to focus on in 2018.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All