Our market Outlooks over recent quarters have offered clients our views into topical issues affecting interest rates, economics, and asset prices. We have also endeavored to introduce topics of interest less directly linked to current market conditions (recently, technology valuations and Behavioral Finance). This quarter, for a discussion of Bitcoin and other “cryptocurrencies”, click here.

“A synchronized global expansion is leading to a big shift in monetary policy around the world--toward central banks shrinking rather than growing—with implications for markets, inflation and the outlook for growth”: thus reads the Wall Street Journal’s opening sentence of their “The Outlook” column on October 8th.

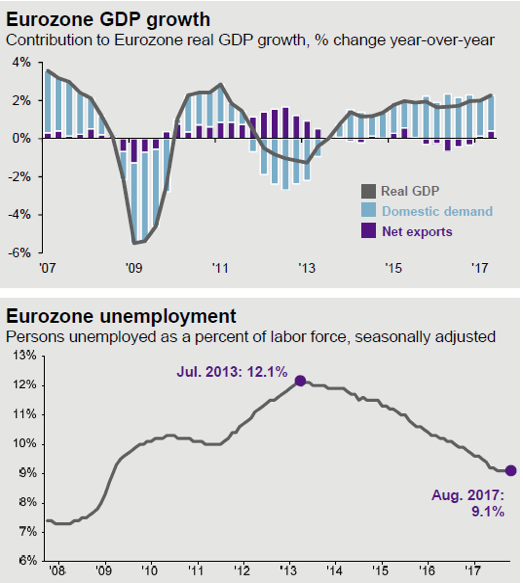

CCR Wealth Management has chronicled the improvement in non-US economies and equities throughout the year as a validation of our overweight position in international investments. Improving global economies act as a salve, of sorts, to soothe nagging concerns about things like the length of the US expansion, current US equity valuations, and of course, Washington politics. Our role is not to make investment commitments based on near-term economic (or political) predictions, but rather to be informed by historical market cycles, while keeping a wary eye out for potential disruptions. A year ago, we cited the busy global political calendar and populist momentum as potential causes for concern. But as the year has progressed, political risk abroad has abated and the likelihood of self-sabotage (in Europe, particularly) has diminished.

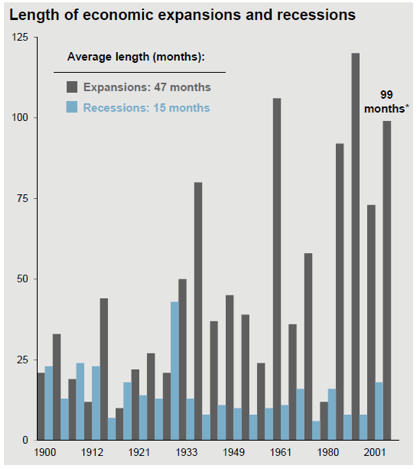

The US economic expansion from the last recession is now in its 100th month. Some pundits have cited this as evidence that the US market cycle is “long in the tooth” and that equity valuations, being above historical averages, should encourage investors to take a more defensive investment posture. Let us consider the following fact. At 99 months (through September), the current US economic expansion is roughly twice as long as the average expansion over the last 117 years. Yet, it trails the expansion of the 1960’s (106 months) and the period from 1991-2001 (120 months). We have said this before, and we will say it again: Bull Markets do not die of old age. Their deaths usually come at the hands of the Fed. We also live in a shifted paradigm, as we pointed out in our July Outlook. The lowest the Fed Funds rate got during the expansion of the 1990’s was 3.0%, and while it dipped below 2% in 1961 briefly, the average through the expansion of the 1960’s was about 4.50%. Of course, in our current expansion, the Fed Funds rate has been effectively 0% for 84 out of 99 months (roughly 85% of the time).

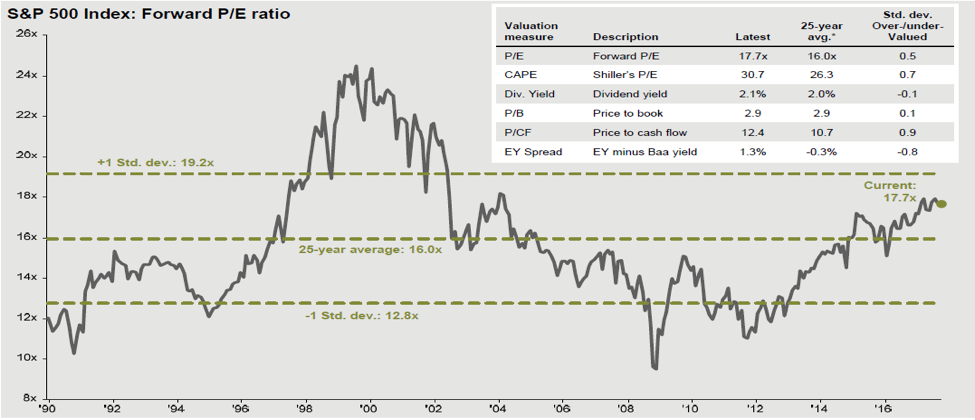

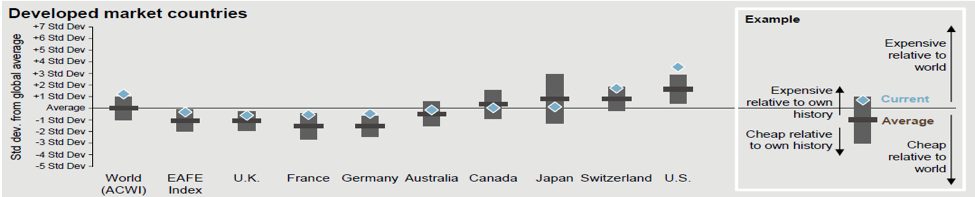

We have frequently tackled the subject of valuations in these pages and we have even dissected the valuations of the most expensive US technology shares in July, so we won’t belabor the point here. Our primary messages on valuation are: 1) while US stocks on average are on the expensive side, it is our belief that they are not unreasonable given economic growth; and, 2) true “value” investors can and should, in our opinion, look overseas for what they seek.

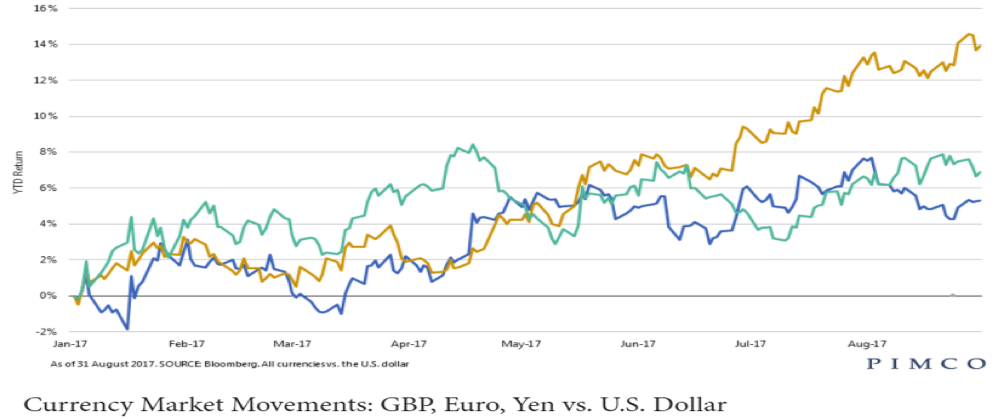

As investors decide how half-full or half-empty the glass is, we cite the improvement of the global economy along with the weakening dollar as decidedly bullish. In 2016 the US exported $2.2 trillion of goods and services. Economically healthier trading partners able to buy more US goods and services with stronger home currencies is undoubtedly a net positive for the US economy, and therefore our stock market. Remember, growing the “E” in the P/E ratio will maintain reasonable valuations.

While political risks overseas have diminished, domestically they are not gone. In July we restated a core belief that investors expect good governance (or governance, at least) from our political representatives. We believe much of today’s stock market valuation is attributable to this expectation. Three failed attempts at healthcare reform (a signature campaign issue in 2016) has us a bit nervous as we contemplate pending tax reform. If the “my way or the highway” approach on healthcare by a handful of Republican Senators is maintained, we think the manifestation in the stock market could potentially be ugly. It is already late in the first year of this administration (with a congressional majority) and we have yet to see any major legislation passed which would advance the Administration’s campaign agenda. Time is of the essence.

Interest Rates

We previously cited Capital Economics’ July out-of-consensus call that there would be no rate hike in September. There was no September rate hike. The same source is in the consensus now, with a single 25 basis point rate hike likely in December, with three similar hikes to occur in 2018. Returns on the Bloomberg Barclay’s Aggregate Bond Index remain anemic over the last 12 months (0.45%), though are no longer negative.

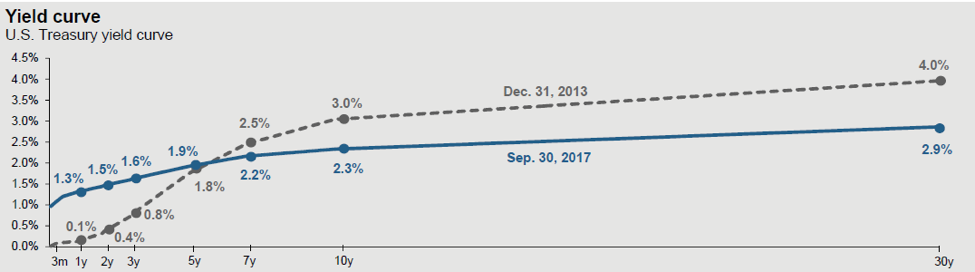

As the Fed began raising rates at the short-end of the yield curve (the Fed Funds rate) nearly two years ago, we have seen longer-term rates actually come down. The result has been a “flattening” of the yield curve. Flattening yield curves are viewed warily by investors and traders—this would counter our sunnier outlook above. Investors willing to accept only small incremental yields from long term bonds over short term bonds suggests deflation is expected.

However, we are less pessimistic and believe the Fed’s balance sheet (which began unwinding this month) has had some influence on suppressing longer-term yields. That said, inflation remains low. Action on infrastructure spending and tax reform would likely steepen this curve, in our view.

The views are those of CCR Wealth Management LLC and should not be construed as specific investment advice. Investments in securities do not offer a fixed rate of return. Principal, yield and/or share price will fluctuate with changes in market conditions and, when sold or redeemed, you may receive more or less than originally invested. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Investors cannot directly invest in indices. Past performance does not guarantee future results. Securities offered through Cetera Advisors LLC. Registered Broker/Dealer, Member FINRA/SIPC. Investment Advisor Representative, CCR Wealth Management, LLC. Registered Investment Advisor. Cetera Advisors LLC and CCR Wealth Management, LLC are not affiliated companies. Cetera Advisors LLC does not offer tax or legal advice. CCR Wealth Management 1800 W. Park Drive, Ste 150, Westborough, MA 01581. PH 508-475-3880

© CCR Wealth Management LLC

Read more commentaries by CCR Wealth Management