There is so much on the calendar next week that it is impossible to choose a single theme. The economic calendar includes all the major reports. It is still the heart of earnings season. Announcements are expected about a new Fed Chair (and perhaps other appointments), the tax reform proposal, and Special Counsel Mueller’s first indictment. The actual Fed rate decision, often the major focus, is almost an afterthought.

It is a paradise for the punditry!

Last Week Recap

In the last edition of WTWA I guessed that there would be plenty of discussion about the lack of fear in markets. That was a reasonable guess as well as an interesting topic to consider. Evidence of the focus on fear came from Wealth Advisor, which teed up a week-old story featured earlier by Business Insider. I had bookmarked this last week for more complete attention, but I was alarmed by an email showing the most popular stories.

The original story was based on an interview with John Hussman who explains every week that the stock market is “overvalued, overbullish, and overbought.” He explains that Mr. Buffett does not really understand the relationship between stock prices and interest rates, and discusses the interest effect on future cash flows. This completely misses the Buffett point, which compares the attractiveness of various assets. A balanced story would have done a better job of explaining the Buffett viewpoint, but it is always popular to predict a 60% market crash.

Trivia question: When is the first time Dr. Hussman used the phrase “overvalued, overbullish, and overbought?” At some point he added “obscene.” Answer at the conclusion of today’s post. Hint: If you read the story on your mobile, you were using the iPhone 4!

The Story in One Chart

I always start my personal review of the week with a chart. This week I am using a chart of the S&P futures from Investing.com. If you visit the page, you can readily change chart style and time frame. The futures show you the overnight action as well as the trading during the day. The “N” indicators will show relevant news if you hover over them.

The change on the week was modest, as it has been in many prior weeks, but it adds up to another new record. Once again, notice that the volatility has been very low. The intra-week range was less than 1.5% and the weekly change only 60 bps. Those who believe that the VIX should be signaling more fear should realize that it has been anchored by the continuing low volatility in the underlying stocks.

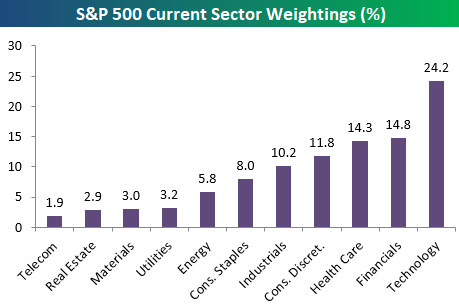

Much of the gain was in the technology sector, which now constitutes 24.2% of the S&P 500. (Bespoke)

Eddy Elfenbein reports an amazing research result:

If you take all the days when the S&P 500 moved more than 1.14% in a day, up or down, the combined return comes out to zero. They completely balance each other out.

The entire return, more than 55-fold over 60 years, comes on the low-volatility days (up or down less than 1.14%).

Would you have guessed that?

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The economic news has been mostly positive.

The Good

-

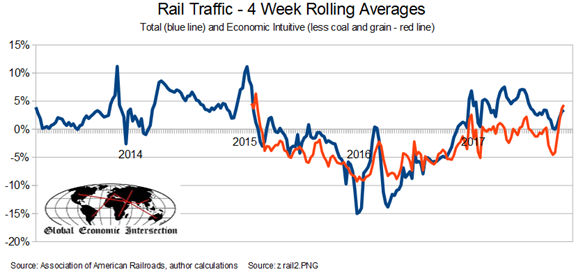

Rail traffic is strong. Steven Hansen (GEI) provides the supporting evidence.

-

Durable goods increased 2.2%, handily beating expectations.

-

Earnings beat rate is 76%. The revenue beat rate of 67% is also above historical averages. The blended earnings rate is less encouraging, with a drag from insurance companies. The market is also reacting less to the strong reports and to earnings misses. (FactSet). Brian Gilmartin notes the continuing strength in forward estimates, musing on the possible tax cut effect. He wonders whether 2018’s earnings estimate might rise from $145.69 to $150.

-

New home sales registered 667K on the SAAR, handily beating expectations.Calculated Risk provides analysis about the “Harvey rebound.”

-

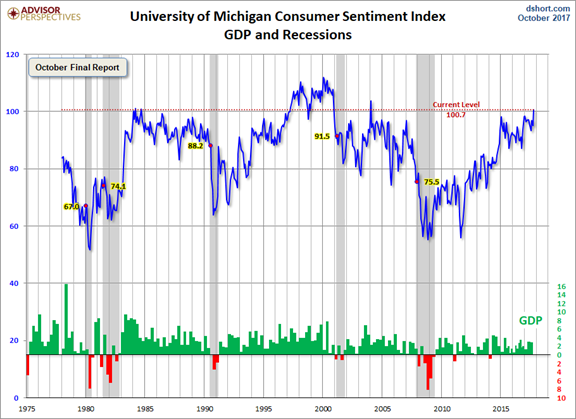

Michigan sentiment remains favorable. Jill Mislinski has my favorite chart on this topic, pulling together all the relevant themes.

-

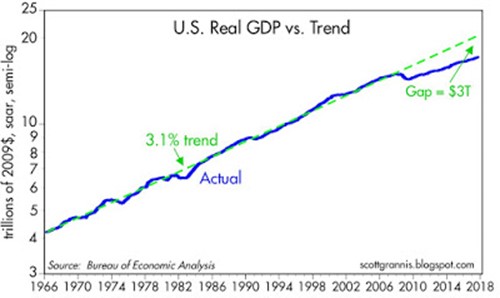

Q3 GDP increased 3% for the second consecutive quarter. New Deal Democrat notes that some internal “leading indicators” are negative. Scott Grannis notes that growth is still below trend.

The Bad

-

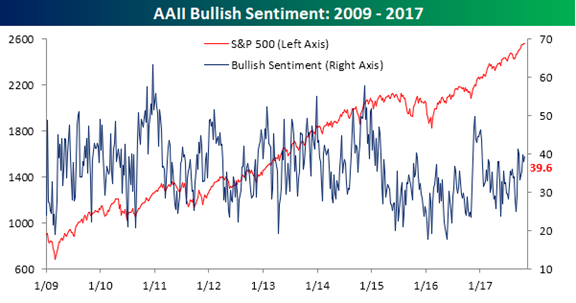

Bullish sentiment is higher, a contrarian indicator explained by Bespoke.

-

Pending home sales hit a three-year low. (Diana Olick). She reports that low supply remains a problem.

Following Up

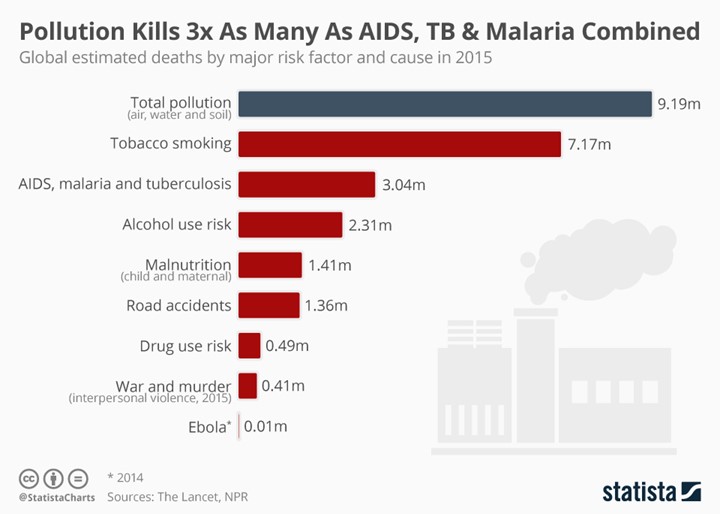

Last week some readers were skeptical about the poll I cited showing pollution concerns. Statista’s data from The Lancet and NPR shows the overall deaths from pollution.

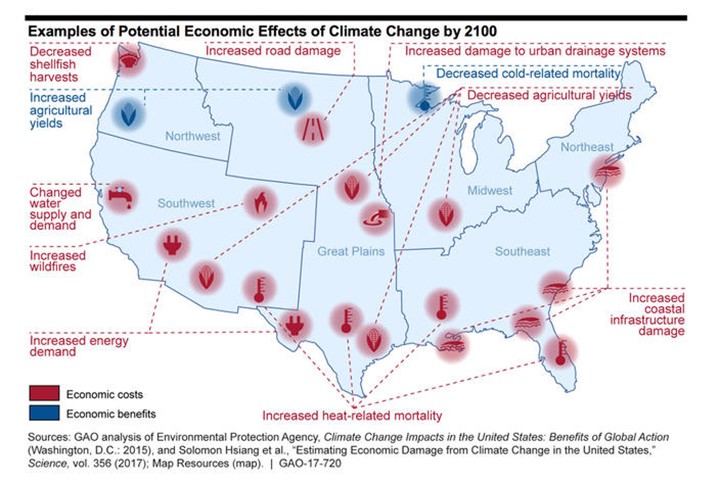

Similarly, Barry Ritholtz cites a powerful study discussing economic and other effects of climate change. He has little patience for climate change deniers. I’ll just suggest doing a lot of reading before making up your mind.

Methods used to estimate the potential economic effects of climate change in the United States—using linked climate science and economics models—are based on developing research. The methods and the studies that use them produce imprecise results because of modeling and other limitations but can convey insight into potential climate damages across sectors in the United States.

The Ugly

A possible pandemic? The IMF is tracking some early indicators and improving preparations, including a simulation at their last meeting.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

We have a massive economic data calendar. As usual, the employment report will claim the featured spot, but wait — there’s more. Both ISM reports, personal income, and auto sales are very important. There are several others that are less significant only by comparison.

It would be easier to say that I am interested in everything on this list, while most should focus on the items I listed above.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

In addition to the big economic calendar, we have expected announcements on appointments, tax proposals, indictments. The Fed will announce a decision on rates. Earnings season is in full swing. I have gone out on a limb before in predicting the likely theme for the week, but this time it is impossible!

After the recent weeks without much solid, fresh news, there is a plethora. We should expect A paradise for pundits!

It is natural to expect a volatility spike from so much news in so little time. Perhaps. But oftentimes the results are expected, or one offsets another. Here is the short list of items to consider, with disparate viewpoints on each

-

Political

- Fed chair announcement – with Powell in the lead over Yellen and Taylor.

- Other Fed appointments – might include Taylor to balance Powell.

- Tax reform proposal.

- Special Counsel Mueller’s first indictment(s).

-

Economic

- Most data reports have been stronger. Will this continue? Especially in employment?

- Some have disparaged what they call “soft” data. Will that continue?

-

Earnings

- Overall strength has been solid.

- Sector variation has been important, and will keep the spotlight.

- Reduced guidance is getting stern market punishment. Many are looking for reasons to sell.

-

Fed decision – No one is expecting a rate change, so the focus will be on the statement.

As usual, I’ll have more in the Final Thought, where I always emphasize my own conclusions. In this case, it includes what I see as most important.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

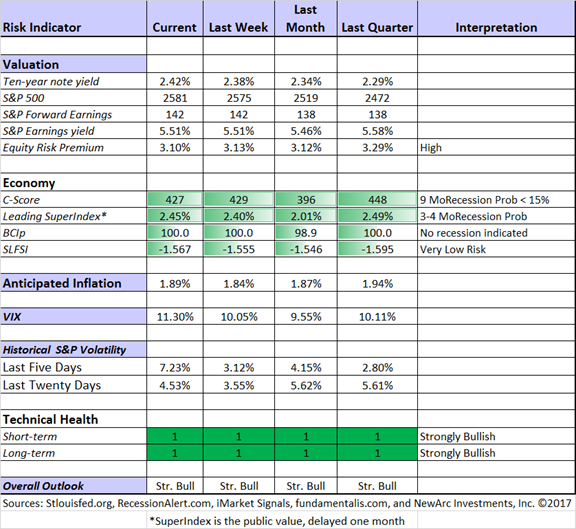

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Georg Vrba: Business cycle indicator and market timing tools. It is a good time to show the chart with the business cycle indicator.

Doug Short: Regular updating of an array of indicators. Great charts and analysis.

Guest Sources:

Steven Hansen looks at employment data, wondering whether the tables based upon education are most helpful. He notes that 100 million of the 125 million non-farm jobs are non-supervisory. Many times, the job requirements include credentialism versus actual needs. He makes an interesting argument that many can do better financially without a college education.

Insight for Traders

We have not quit our discussion of trading ideas. The weekly Stock Exchange column is bigger and better than ever. We combine links to trading articles, topical themes, and ideas from our trading models. This week’s post compared trading and investing with a focus on Bitcoin. Just for fun, we also added Bitcoin to the ratings list for Felix and Oscar. Blue Harbinger has taken the lead role on this post, using information from me and from the models. He is doing a great job.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility!

Best of the Week

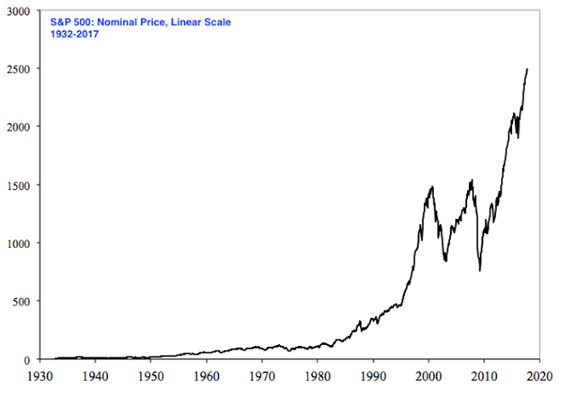

If I had to pick a single most important source for investors to read this week it would be Urban Carmel’s series (Two parts for now) on investor psychology. The first segment looks at how data framing in charts affects perception. Here is a chart of the S&P 500 the way it is often presented.

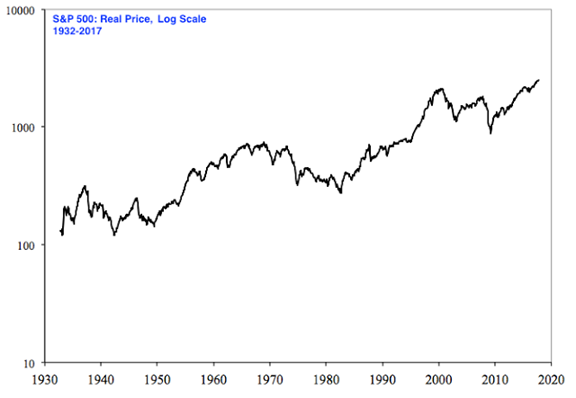

And how it looks on a log scale (which is necessary to make percentage changes over time equivalent) and also with an adjustment for inflation.

Part Two explains why following the stock market is bad for your returns. He writes as follows:

The human mind has a tendency to assess risk based on prominent events that are easily remembered. The 1987 crash, the tech bubble, the financial crisis and the flash crash in 2010 are all events that are easily recalled. The mind automatically assigns a high probability to prominent (but rare) events. It ignores the more important “base rate” probability that better informs decisions. The fact that the stock market rises in 76% of all years, that it gains an average of 7.5% per year and that annual falls greater than 20% occur less than 5% of the time, are ignored in decision making. The mind interprets every 10% correction as the beginning of something much worse, even though a 10% fall is a typical, annual occurrence during bull markets.

The overall analysis is excellent, including plenty of charts for your consideration.

Stock Ideas

I always try to illustrate methods of analysis as well as stock ideas. I do not always hold the positions mentioned, but I regard the idea and analysis worthy of consideration. With eight different investment programs, we have an extensive watch list. That is what I am trying to share.

Value Investing

Chuck Carnevale is the leading resource in this method. His tools are invaluable and inexpensive. His regular (free) articles provide a wealth of ideas as well as a master class in how to evaluate a stock. We never take on a new This week there are two great examples. First, he continues his series on the DJIA with a look at five fairly-valued names. Take time to study the method and check back on the prior entries which you might have missed.

And also, Celgene (CELG) still looks good, even after the reduction in earnings expectations.

Market Maker Hedging

Peter F. Way’s unique approach takes another look at IBM, especially considering the institutional ownership of the stock and market maker hedging. The market maker’s position is temporary, reflecting a professional judgment about how far the stock might move – in either direction.

Finding a Niche

Strong Bio (the work of a multiple PhD analyst) takes a careful look at Cara Therapeutics and analyzes their niche—pain management and pruritic. This may be especially interesting as an approach to dealing with the opioid epidemic.

Focus on Income

Blue Harbinger continues his focus on income with a review of preferred stocks and also some put sales in selected names. This method can work very well with sound stock selection and proper size.

Kirk Spano (endorsed by Mrs. OldProf because he is a Packer fan) combines the covered put approach with an analysis of energy and solar, recommending SunPower (SPWR). I urge readers to follow his advice that you should sell puts only when you are willing to buy the stock at the indicated price.

Assets Versus Currencies

Leading valuation expert Aswath Damodaran begins with an analysis of bitcoin. He uses this as a basis for explaining the differences between assets, commodities, currencies and collectibles. This is a great post, which most people will need to read twice. He also shows why bitcoin is a trading vehicle, not for investors. Here are the key distinctions:

Consistent with this attention to investing versus trading, I was especially interested in John Rhodes’ idea about Bitcoin miners. This would seem to be an asset rather than a currency. He ends by rejecting MGT Capital Investments (MGTI), but the concept is worth watching. I usually prefer buying gold mining stocks rather than the metal.

Combining Technical Analysis with Dividends

Bonddad looks carefully at the attractions of Kimberly Clark. While there is an emphasis on dividends, fans of technical analysis will not be disappointed.

Sell-Side Recommendations

Morgan Stanley thinks that Broadcom is undervalued. (Paul Farrell, Barron’s)

And maybe biotech is a bargain (Barron’s).

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich has an interesting topic every day. His own commentary adds insight and ties together key current articles. As usual this week he had several good articles, but my favorite this week discusses the timing of negative investment returns. It is a good explanation of the concern, but the answers are more complicated than the sources suggest.

The CBO (via GEI) has some good analysis on retirement needs. One reason I regularly read GEI is John Lounsbury’s widespread search for ideas and articles.

Tadas is back on the job with his regular Wednesday post on personal finance. My favorite this week is some solid advice on what to do if you know that your credit report has been compromised.

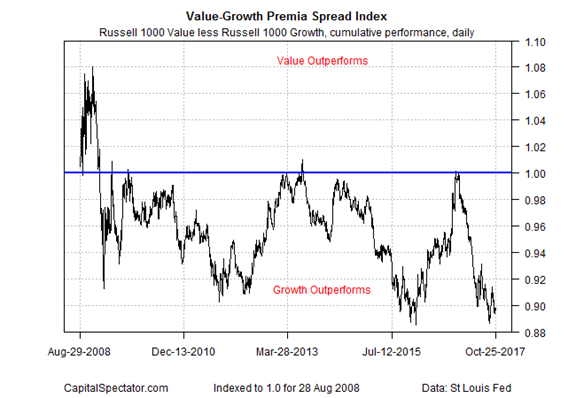

Value Investing

The balance between value and growth is once again tilting toward the latter. Does recent history provide evidence for the future?

James Picerno provides analysis and this interesting chart.

This was a week for the high-profile tech stocks, where the earnings and other metrics were celebrated.

David Van Knapp emphasizes that there are many ways to achieve investing success. Developing a process and sticking with it is the key. No method will be the best in each quarter. David’s well-reasoned article is a must-read piece regardless of your approach. Right now, it has special relevance for dividend and value investors.

Watch out for….

Lockheed Martin (LMT). Stone Fox Capital looks carefully at whether current values are justified.

Stone Fox Capital also warns about Sprint (S), especially if the planned merger does not come off.

Final Thoughts

I have my own expectations on each of the key question, including which are more important.

-

Political

- The Fed Chair appointment will not matter much if it is Powell or Yellen. Anyone else will get a reaction.

- Other appointments are fine if they are mainstream. A single exception will not matter much. The addition of a hard money, non-economist like Judy Shelton would attract a lot of attention. It would also be a good dissertation topic for some student.

- The tax reform proposal will get plenty of buzz, including analyses of who would benefit. It is irrelevant, a mere step along the path to finding a centrist majority. Current market levels reflect little if any “Trump effect” despite the constant media chorus on this facile theme.

- The original indictments are this week’s wild card. Will a Trump relative be included? How might the President respond? (Roll Call)

- Economic – I expect the economic news to be solid, but perhaps affected by weather.

- Earnings – expectations in most sectors have been beaten by more than the historical average levels.

- Fed – I expect nothing from a policy change and little from the statement. I expect a rate hike in December and three more next year. This week’s Barron’s cites the Eurodollar market as implying two hikes in this time period. Eurodollars are futures based upon Libor at a specified future date. Many casual observers confuse this with the Euro currency market, which is quite different. Eurodollar trading is a deep and liquid market, where one can construct a trade for any point on the yield curve.

There is plenty to watch this week. As usual, understanding the schedule and expectations will help you navigate the waters.

What worries me…

- Mueller indictments and President Trump’s response. If a Trump family member is included and the President fires Mueller, the Nixon-era Saturday Night Massacre comparisons will get headlines. N.B., I refer not to the substance of the issue, but to the market reaction.

- Government computers. We all have a sense of dilapidated infrastructure in roads and bridges. Decades of cuts in government spending have had many under-the-radar effects. As a former government employee, I know how hard it was to get a new computer in a timely fashion. Put his together with recent news on hacking, and you will understand my concern.

…and what doesn’t

- The Fed. We are still more than a year away from when changes in Fed policy will be important for stocks, despite the popular focus on this topic. It also does not matter (in the short run) whom President Trump selects to be the new Fed Chair, or his other appointments.

- Low VIX readings. The so-called “fear gauge” is low because actual trading volatility is low.

Trivia question answer

The earliest time I could find was October of 2010. Reader corrections are welcome. That was the year of the BP oil spill and the OldProf’s Dow 20K call. I am still waiting for Dr. Hussman to respond to my post about his ever-changing chart. Many follow the conclusions from this chart; they understand Hussman’s point; but no one seems able to understand or replicate it. It keeps changing when prior forecasts did not work. It would help if, like Dr. Shiller, he shared his data and process with other investigators.

If I had been so wrong about something for so long, I would be taking a hard look at my methods. Instead of quoting ZH, I might be bringing in a few astute critics as consultants. Calling out Warren Buffett would be low on my list, although once you have blamed your own missed forecasts on the Fed, what is left?

© NewArc Investments, Inc.

Read more commentaries by NewArc Investments, Inc.