WISE WORDS FROM WISE MEN

Benjamin Graham: “The best way to measure your investing success is not by whether you’re beating the market but by whether you’ve put in place a financial plan and a behavioral discipline that are likely to get you where you want to go.”

“The investor’s chief problem — and his worst enemy — is likely to be himself. In the end, how your investments behave is much less important than how you behave.”

Warren Buffett: “The stock market is a device to transfer money from the impatient to the patient.”

Jack Bogle: “Your success in investing will depend in part on your character and guts and in part on your ability to realize, at the height of ebullience and the depth of despair alike, that this, too, shall pass.”

Peter Lynch: “Thousands of experts study overbought indicators, head-and-shoulder patterns, put-call ratios, the Fed’s policy on money supply… and they can’t predict markets with any useful consistency any more than the gizzard squeezers could tell the Roman emperors when the Huns would attack.”

“Far more money has been lost by investors trying to anticipate corrections, than lost in the corrections themselves.”

John Kenneth Galbraith: “The function of economic forecasting is to make astrology look respectable.”

— From DAVIS ETFs:

http://davisetfs.com/investor_education/quotes?utm_source=Foreside+Fund+Services%2C+LLC+List&utm_campaign=2d97b0 8ab2-VALUE_OF_A_FINANCIAL_ADVISOR&utm_medium=email&utm_term=0_fe2a9dbc30-2d97b08ab2-66006745

EATING IN THE FIFTIES (MY GENERATION)

From my friend Janeen:

• A take-away was a mathematical problem.

• Pizza? Sounds like a leaning tower somewhere.

• Oil was for lubricating; fat was for cooking.

• Cubed sugar was regarded as posh. When did that stop?

• Healthy food consisted of anything edible.

• Cooking outside was called camping.

• “Kebab” was not even a word, never mind a food.

• Prunes were medicinal — they still are.

• Surprisingly muesli was readily available. It was called cattle feed.

• We called sushi “bait” — Deena still does.

• The one thing that we never, ever had on or at our table in the fifties… was elbows, hats, or cell phones.

WONDER WHERE WE GO FROM HERE?

SAME SONG, SECOND VERSE

From the Wall Street Journal. Another guru bites the dust:

“Oil’s $100 Million Man Pays Price for Bad Bets

“Andrew Hall, a legendary trader who made billions betting on oil’s rise, is shutting down his hedge fund after he misjudged the impact of a boom in U.S. production that upended the market.”

DID YOU KNOW?

U.S. organizations spend 166 percent more on legal services per dollar of revenue compared to their legal counterparts. (From a survey by Acritas of about 2,200 chief legal officers and general counsel around the world)

— ABA Journal

GOOD PEOPLE

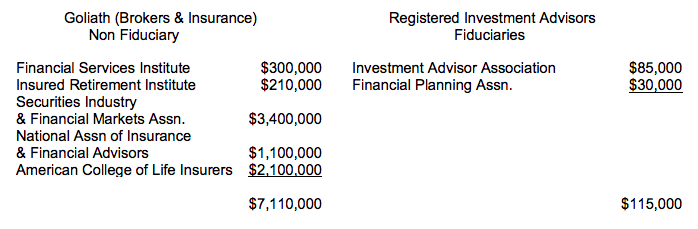

DAVID VS. GOLIATH

The battle over requiring those providing advice to be held to a fiduciary standard (currently, brokers and insurance agents are not) continues unabated. Unfortunately, Goliath has a LOT more money. Here’s how much has been spent during the first half of 2017 on lobbying.

That’s okay. We’ll keep fighting — and remember, David won!

MORE WISE WORDS…

Warren Buffet from Business Insider:

- “The wealthy are accustomed to feeling that it is their lot in life to get the best food, schooling, entertainment, housing, plastic surgery, sports ticket, you name it. Their money, they feel, should buy them something superior compared to what the masses receive.”

- “In many aspects of life, indeed, wealth does command top-grade products or services. For that reason, the financial ‘elites’ — wealthy individuals, pension funds, college endowments and the like — have great trouble meekly signing up for a financial product or service that is available as well to people investing only a few thousand dollars. This reluctance of the rich normally prevails even though the product at issue is — on an expectancy basis — clearly the best choice. My calculation, admittedly very rough, is that the search by the elite for superior investment advice has caused it, in aggregate, to waste more than $100 billion over the past decade. Figure it out: Even a 1% fee on a few trillion dollars adds up. Of course, not every investor who put money in hedge funds ten years ago lagged S&P returns. But I believe my calculation of the aggregate shortfall is conservative.”

- “Much of the financial damage befell pension funds for public employees. Many of these funds are woefully underfunded, in part because they have suffered a double whammy: poor investment performance accompanied by huge fees. The resulting shortfalls in their assets will for decades have to be made up by local taxpayers.”

- “Human behavior won’t change. Wealthy individuals, pension funds, endowments, and the like will continue to feel they deserve something ‘extra’ in investment advice. Those advisors who cleverly play to this expectation will get very rich. This year the magic potion may be hedge funds, next year something else. The likely result from this parade of promises is predicted in an adage: ‘When a person with money meets a person with experience, the one with experience ends up with the money and the one with money leaves with experience.’”

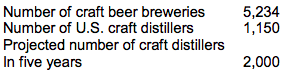

BOOZE ON THE RISE

From AARP:

A WORD ABOUT THE RICH

Capgemini report from Financial Advisor:

“The number of millionaires [those with investable assets of $1 million or more] in the world rose by nearly 8 percent last year to an all-time high of around 16.5 million people…. In the United States, their rank rose to 4.8 million from 4.46 million, while the number of millionaires in China rose to 1.13 million from just over 1 million.”

CHOOSE THE BEST

Need a hospital or surgeon? More from AARP:

https://www.medicare.gov/hospitalcompare/search.html

For hospitals, the Medicare.gov Hospital Compare site is the place to go. It rates 4,000+ hospitals based on 57 quality measures and best practices.

You might also check out:

https://health.usnews.com/best-hospitals

https://www.consumerreports.org/health/hospitals/ratings

How about a surgeon?

http://certificationmatters.org/

http://fsmb.org/policy/contacts

https://projects.propublica.org/surgeons/

http://surgeonrating.com/

WOW!!

From the TexasLawer:

“JPMorgan hit for $4 billion Over Mishandled Estate

“A Texas jury has hit JPMorgan chase for more than $4 billion in damages for mishandling the estate of former information technology executive who pioneered American airlines SABRE reservation system…. In addition to the $4 billion in punitive damages, the jury awarded $4.7 million in actual damages and $5 million in attorney fees.”

I wonder if they might appeal.

MORE DAVID VS. GOLIATH

EVEN MORE DAVID AND GOLIATH

Next time you think you might like to compete with institutional managers, keep in mind with whom you are competing. I came across this profile recently when preparing for one of my Wealth Management classes. Although this data is close to 20 years old, my guess is that the standards are even higher today.

• Attended an Ivy league or comparable schools in the Northeast (one in seven went to Harvard), was in the top half of his class, studied finance, economics, or business as an undergraduate and went on to get his MBA.

• Works an average of 54 hours per week.

• Had seven and a half years of investment experience prior to joining his current firm and has been with his present employer 11 years.

• Earned somewhere between $250,000 and $750,000 (that was in 1996).

That’s just the AVERAGE!

KEEP OR PITCH?

From a LinkedIn posting by financial planner Allen Yee: There’s a fine line between keeping financial records for a reasonable period of time and becoming a hoarder. It’s ultimately up to you to determine which records you should keep on hand and for how long, but here’s a suggested timetable for some common documents.

1. Store permanently: tax returns, major financial records

Your tax returns are important documents to keep as part of your financial history. You’ll want to keep a permanent electronic or hard copy of each year’s tax return and any payments you make to the government. Additionally, it’s a good idea to hold onto records of major financial events such as legal filings or inheritances.

• Birth and death certificates

• Social Security cards

• Estate plan documents (trust, wills, power of attorney, and advanced healthcare directives)

• ID cards and passports

• Marriage license

• Business license

• Any insurance policy (good to keep even if they have a digital copy in case problems come up)

• Vehicle titles and loan documents

• House deeds and mortgage documents

• Investment/Mutual Fund statements

2. Keep for three to seven years: supporting tax documentation

Depending on your filing circumstances, the IRS may be able to ask you for supporting documentation for three to seven years after you file a return. Knowing that, a good rule of thumb is to save any document that verifies information on your tax return — including Forms W–2 and 1099, bank and brokerage statements, tuition payments and charitable donation receipts — for three to seven years. **The IRS requires taxpayers to keep records that support income, deductions, and credits shown on their income tax returns until the period of limitations for that return runs out — generally three to seven years, depending on the circumstances.

3. Store for one year: regular statements, pay stubs

Keep either a digital or hard copy of the past years’ worth of your monthly bank and credit card statements. You should also hold on to pay stubs so that you can use them to verify the accuracy of your Form W-2 when tax season arrives.

• Medical records and bills (keep at least a year after payment in case of disputes)

• Pay stubs and bank statements

4. Keep for one month: utility bills, deposit and withdrawal records If you’re self-employed, you may need your utility, cable, and cell phone bills for tax purposes. Otherwise, you can dispose of them as soon as you verify your payment was processed. You can also dispose of bank withdrawal and deposit slips after verifying them with your monthly statement. Finally, the last subset is the documents you need to keep the most recent version of:

• Social Security statements

• Annual insurance policy statements

• Retirement plan statements (401(k), 529, IRA, etc.)

I KNEW THAT

Kiplinger Names Financial Advisor a Top 10 Best Job for the Future Kiplinger recently reviewed 785 jobs and designated 10 high-salary jobs poised for strong growth in the coming decade — including “Personal Financial Advisor” as “Top 10 Best Jobs for the Future.” The report cited a 23.8% projected job growth rate for financial advisors from 2016-2026, and noted that “Certification from the Certified Financial Planner Board of Standards enhances an advisor’s credibility.”

YOU THINK IT’S HOT HERE

Hell on Earth: With an average temperature of 107.39 degrees in July, Death Valley set the record for hottest month at a single location in U.S. history. Keep in mind that this number is an average of all the high and low temperatures. The average daily high temperature was an unbearable 119.6 degrees.

Hope you enjoyed,

Harold Evensky

Chairman

Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

Read more commentaries by Evensky & Katz / Foldes Financial Wealth Management