Q3 Recap

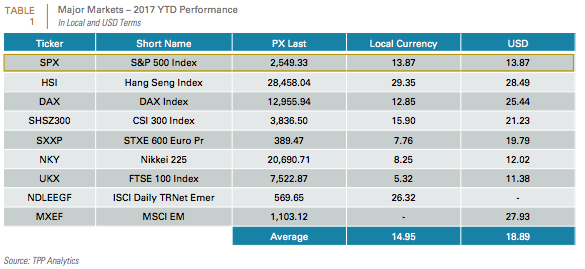

Growth accelerated in Q3, with inflation quiescent in most countries; perpetuating the “Goldilocks” conditions that have generally favored risk assets since early 2009. Global equity markets continued their gallop in Q3, with the MSCI ACWI and the S&P 500 reaching all-time highs. Among developed markets, the MSCI Eurozone index outperformed the MSCI ACWI by 28 bps; Japan trailed by 44 bps whilst Emerging Markets (EM) bested the global benchmark by roughly 300bps. With the US dollar having fallen 8% year to date, a significant portion of the relative performance advantage for international equity markets came through currency gains. (See TABLE 1).

Among sectors, IT, energy and materials outperformed the global equity index whilst consumer staples and health care underperformed in all three major regions. Financials outperformed in the U.S. and the Eurozone, but trailed in Japan and EM. Industrials also outperformed in the Eurozone and Japan but lagged in the U.S. and EM. Consumer discretionary, utilities and telecom services trailed the broad market and were a mixed bag across the three major regions.

In the U.S., growth rebounded sharply after a seasonally weak Q1. First-half GDP growth came in at 2.2% (above trend, which is estimated at 1.8%), and the manufacturing ISM reached 57.7 in September. The two big hurricanes will probably knock around 0.5 points off Q3 growth but the lesson from previous disasters is that this will be more than made up over the following three quarters. Rebounding capex, and consumption aided by a probable acceleration in wages, should keep GDP growth strong. With Q2 GDP growth 2.3% YoY and the manufacturing PMI at 57.4, Europe’s growth surpassed the U.S., reflecting its greater degree of cyclicality, with the German IFO growth index plumbing new heights and manufacturing wages growing by 2.9%YoY.

Japan has been buoyed by the external sector (with exports rising 18%YOY and industrial production 5%), but has thus far still been plagued by weak household spending and core inflation. Despite potential uncertainty with the impending election later this month, we expect a continuation of earnings-supportive Abenomics (monetary accommodation as well plus structural market reforms). Finally, China’s PMI has oscillated around 50 all year, as the authorities tried to stabilize growth ahead of October’s Party Congress. But money supply and credit growth have been slowing all year, and this is now showing through in downside surprises in fixed asset investment and retail sales data. Especially if the Congress moves towards structural reform and short-term pain, growth may slow further.

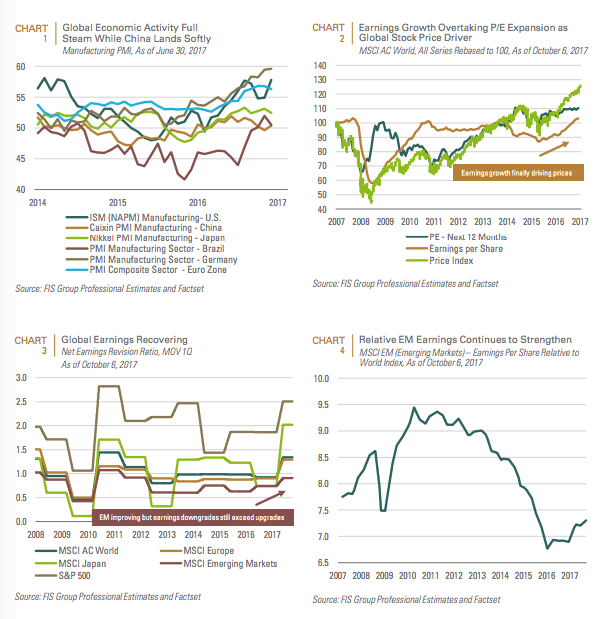

Going forward, we expect growth to remain strong for the balance of 2017 and much of 2018. Accordingly, the Citi Economic Surprise Indices (see CHART 1 on the next page), show strong upward surprises in all major markets except for China, which since early this year has been undergoing a notable deceleration of money and credit growth.

On the earnings front, Q3 2017 was the second quarter in a row in which the price appreciation in global equities was driven by earnings growth, as opposed to expansion in the forward price-to-earnings ratio (which contracted by 2% compared to Q2). Additionally, earnings upgrades continue to outpace downgrades. Even emerging markets earnings, that have been in steady decline since 2011, have turned a corner. (See CHARTS 2-4).

Although we expect less flattering base-effects going forward (as we move pass the late 2015/early 2016 slump in earnings), top-line growth underpinned by a self-sustaining global upturn through at least mid-2018 should allow global equities to withstand less accommodative policies by the Fed and ECB. Moreover, although equity valuations are not cheap by historical standards, they are still attractively valued compared to bonds, especially after the recent safe-haven buying drove global bond yields to very depressed levels.

As we approach 2018, the following factors bear monitoring.

1. The disconnect between the Fed and the market on the path of interest rates and inflation. The US Federal Reserve continues to confirm that it will start shrinking its balance sheet soon. This should be dollar bullish. However, the key risk is whether inflation, which has been soft this year, will rebound and force the Fed to tighten monetary policy in line with its current projections. This would likely cause long-term rates to rise and the U.S. dollar to appreciate, which would hurt government bonds, commodities and some emerging markets. A potential preview of this risk occurred in the latter half of September when after months of pricing in flat-lining inflation, after a more stable core inflation report, the probability of a December Fed hike priced by the futures market moved from 25% to 75%.

While our baseline expectation is that the Fed will raise rates in December as well as at least two more hikes next year, this expectation may be adulterated or enhanced by personnel changes at the Fed. With Chair Yellen’s term due to expire next February and four other vacancies on the FOMC, personnel changes could significantly change the Fed’s direction. For the Trump Administration, the most politically expedient course of action is a series of appointments that steer the Fed in a direction which is more tolerant of rising inflation. This would prolong the current Goldilocks environment and prompt a melt-up in risk assets along the lines of 1999. On the other hand, some of the names being circulated (such as Kevin Warsh and Jerome Powell) are likely to be more hawkish than current Chair Yellen. Either such appointment would again be dollar bullish.

2. Fiscal policy uncertainty. The Trump Administration’s recently proposed tax legislation, if enacted, would represent a form of modest fiscal stimulus late in the economic cycle when the economy is at or very close to full As currently proposed, the legislation would cut taxes by around $1.5 trillion with modest offsets of around $500 billion. A pro-cyclical fiscal stimulus should be bullish for U.S. small caps, companies that maintain significant assets overseas (because of the potential asset repatriation tax break) and bearish for 10 year Treasuries.

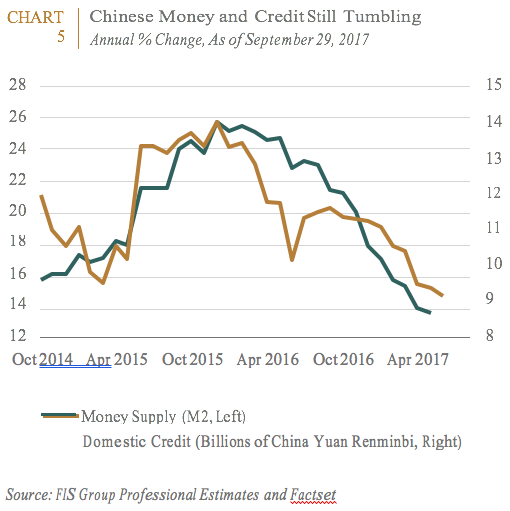

3. Credit slowdown and structural reform in China. Money supply growth in China continues to slow (See CHART 5). This slowdown could be exacerbated if a newly re-elected President Xi Jinping moves forward with structural reforms; even at the expense of a short-term growth slowdown. From a global perspective, a significant slowdown in Chinese money and credit growth should negatively affect demand for China exposed export sectors in Asia and Europe.

Geopolitical risks emanating from North Korea. Despite the constant chest-pounding and saber-rattling from the leaders of both North Korea and the U.S., investors appear to have become relatively desensitized to geopolitical risks emanating from North Korea. We do not believe that the market is wrong in this assessment. In this regard, it is encouraging that both of North Korea’s allies, China and Russia have turned up the pressure; which is starting to impinge on critical fuel supplies there. It would now require a major provocation (i.e. a direct attack on the U.S. or its allies), for tensions to escalate from current levels, reflecting a level of recklessness by Pyongyang which is difficult to fathom. However, while we believe that a full-out war is unlikely, a ratcheting of tensions and minor military skirmishes are quite likely before Pyongyang returns to the negotiating table. The most relevant market threat is to South Korean equities, which traditionally experience a pullback when tensions escalate. Thus far, each such pullback has given rise to a buying opportunity. With currently positive fundamentals (fiscal and monetary policy support, that market’s exposure to the global trade cycle, as well as corporate governance reform), we would agree with such action.

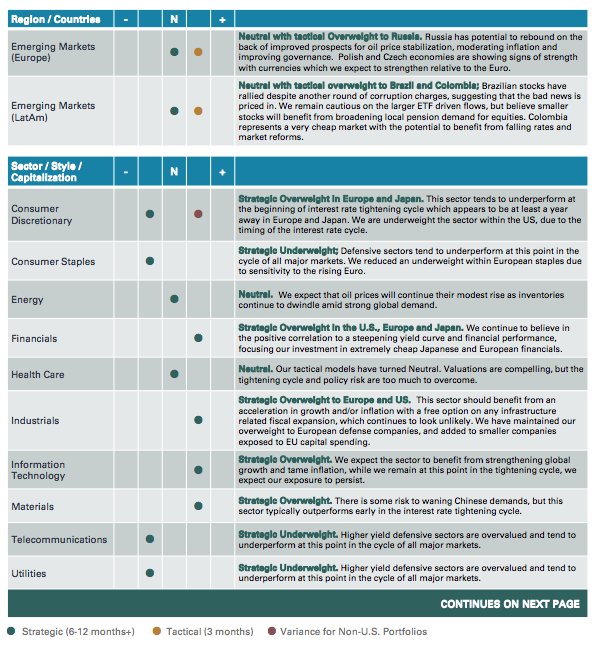

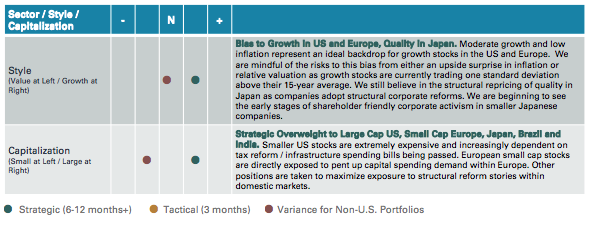

Our Q4 2017 Strategy is delineated in the TABLE 2.

Important Disclosures:

This report is neither an offer to sell nor a solicitation to invest in any product offered by FIS Group, Inc. and should not be considered as investment advice. This report was prepared for clients and prospective clients of FIS Group and is intended to be used solely by such clients and prospects for educational and illustrative purposes. The information contained herein is proprietary to FIS Group and may not be duplicated or used for any purpose other than the educational purpose for which it has been provided. Any unauthorized use, duplication or disclosure of this report is strictly prohibited.

This report is based on information believed to be correct, but is subject to revision. Although the information provided herein has been obtained from sources which FIS Group believes to be reliable, FIS Group does not guarantee its accuracy, and such information may be incomplete or condensed. Additional information is avail- able from FIS Group upon request.

All performance and other projections are historical and do not guarantee future performance. No assurance can be given that any particular investment objective or strategy will be achieved at a given time and actual investment results may vary over any given time.

© FIS Group

Read more commentaries by FIS Group