Four Ways to Drill into Tech

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAlthough tech valuations are elevated, many top tech companies have robust earnings growth, strong balance sheets and growing dividends.

In order to follow the innovation of the sector, investors might want to consider data analytics, cloud computing, cyber security, and semiconductors.

Four ways to drill down into tech

The growth prospects of technology are easy to imagine. What's more challenging is how to invest thoughtfully across the sector. We find that several developments in the sector might be worth particular consideration:

1. Data analytics

2. Cloud computing

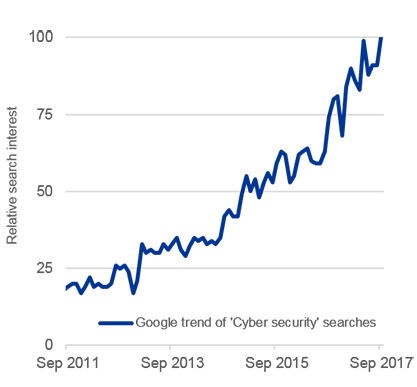

3. Cyber security

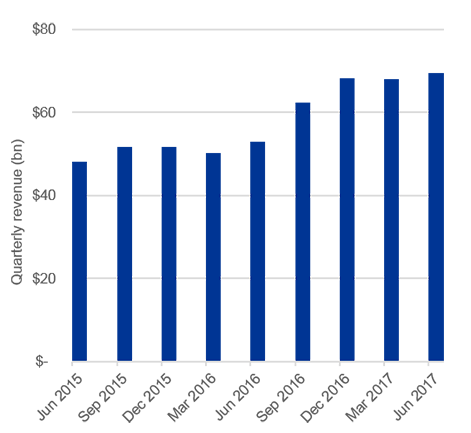

4. Semiconductors

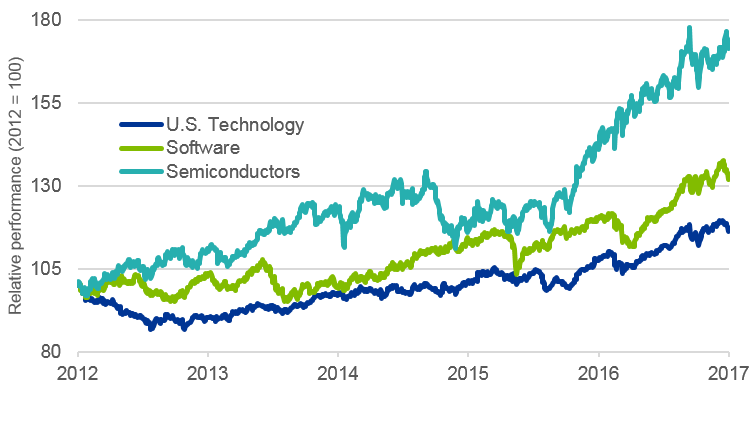

Relative performance of U.S. technology sub industries to S&P 500

Source: BlackRock, Thomson Reuters, as of 9/30/2017.

Notes:U.S. Technology represented by the Dow Jones US Technology Index, Software by the S&P North American Technology – Software Index, and Semiconductors by the Philadelphia Stock Exchange Semiconductor Index. Index performance is for illustrative purposes only. Index performance does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Valuations elevated – for good reason

While it' true that tech tends to trade at a premium, we are far from a dot-com bubble repeat, in our view. Many of today' tech companies feature robust earnings growth, strong balance sheets, and growing dividends. What's more, tech is currently one of the few sectors with a strong secular growth profile. Innovation doesn't ebb and flow with market technicals – it is a structural, disruptive force, permanently separating winners from losers. In that light, we believe it is rational for markets to place a premium on the sector. The premium for tech stocks may be justified if earnings can continue to grow into their valuations. Identifying the next revolutionary product on a company-by-company basis is no easy task. An alternative approach is to identify key themes cutting across the tech sector, driven by innovation and "winner take all" dynamics. We focus on data analytics, cloud computing, cyber security and semiconductors. Each trend has its own fundamental drivers, risk/reward profile, and synergies with other trends.

Data analytics

The growth of "big data" is bringing big opportunities. Major advances in machine learning algorithms, faster hardware, and cheaper computing power are helping companies leverage unparalleled amounts of data. These companies are using analytics to automate operations, understand customer behavior, and monetize data. Data analytics adoption is in its infancy, yet sectors like pharmaceuticals are already analyzing patient data at scale, finding biomarkers, and generating break-through drugs at lower costs and faster speeds.

Cloud computing

The "cloud" is a broad concept covering software as a service (SaaS), platform as a service (PaaS), and infrastructure as a service (IaaS). While SaaS is already being adopted by companies, PaaS and IaaS are still underpenetrated markets presenting nascent growth opportunities. The economics driving cloud migration are powerful and sustainable. Companies can access secure, scalable computing power on demand, and at lower costs than traditional IT systems. This is the power and scale needed to integrate sophisticated data analytics into business processes.

Cyber security

Brand and customer trust are critical to all companies, yet recurring headlines describing the latest hacks are constant reminders of the reputational and financial risks facing these companies. As companies increasingly rely on data analytics to power their business strategy -- and as the cost and sophistication required to commit cyber-attacks continue to fall -- they'll need to increase security budgets to safeguard their data. Despite cloud migration, which has its own security measures, many companies still believe in a second layer of onsite cyber security measures. As cloud migration continues, cyber security may find a second source of demand.

Semiconductors

The backbone and future of the tech industry rests largely with semiconductors. Every year more chips are required to power an increasing number of devices while end user markets have broadened to include autos, communications, and internet of things applications. Industry consolidation has led to better supply discipline just as the demand base expands, which we believe may help dampen cyclical booms and busts yet preserve potential long-term growth opportunities. Growing demand for Artificial Intelligence (AI) and data analytics across all sectors may provide another boost for semiconductors as data analytics, collection, and storage drive demand for chips and semiconductor memory technologies.

Conclusion

Returning to the two concerns at the start, valuations are indeed elevated, but for good reason. Investors waiting for a more attractive entry point might risk prioritizing market timing ahead of owning potentially strong, durable growth trends. In our view, advisors can uncover long-term growth opportunities and enrich client conversations by monitoring dominant tech themes.

Public interest in cyber security has increased steadily |

Semiconductor 2yr compound annual revenue growth at 20% |

|

|

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

This material represents an assessment of the market environment as of the date indicated; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any issuer or security in particular.

The strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective.

The information presented does not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy or investment decision.

This document contains general information only and does not take into account an individual's financial circumstances. This information should not be relied upon as a primary basis for an investment decision. Rather, an assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a financial advisor before making an investment decision.

Funds that concentrate investments in specific industries, sectors, markets or asset classes may underperform or be more volatile than other industries, sectors, markets or asset classes and than the general securities market.

Technology companies may be subject to severe competition and product obsolescence.

The iShares Funds are not sponsored, endorsed, issued, sold or promoted by Barclays, Bloomberg Finance L.P., BlackRock Index Services, LLC, Cohen & Steers Capital Management, Inc., European Public Real Estate Association ("EPRA®"), FTSE International Limited ("FTSE"), India Index Services & Products Limited, Interactive Data, JPMorgan Chase & Co., Japan Exchange Group, MSCI Inc., Markit Indices Limited, Morningstar, Inc., The NASDAQ OMX Group, Inc., National Association of Real Estate Investment Trusts ("NAREIT"), New York Stock Exchange, Inc., Russell or S&P Dow Jones Indices LLC. None of these companies make any representation regarding the advisability of investing in the Funds. With the exception of BlackRock Index Services, LLC, who is an affiliate, BlackRock Investments, LLC is not affiliated with the companies listed above.

Neither FTSE nor NAREIT makes any warranty regarding the FTSE NAREIT Equity REITS Index, FTSE NAREIT All Residential Capped Index or FTSE NAREIT All Mortgage Capped Index; all rights vest in NAREIT. Neither FTSE nor NAREIT makes any warranty regarding the FTSE EPRA/NAREIT Developed Real Estate ex-U.S. Index, FTSE EPRA/NAREIT Developed Europe Index or FTSE EPRA/NAREIT Global REIT Index; all rights vest in FTSE, NAREIT and EPRA."FTSE®" is a trademark of London Stock Exchange Group companies and is used by FTSE under license.

©2017 BlackRock, Inc. All rights reserved. BLACKROCK, BLACKROCK SOLUTIONS, BUILD ON BLACKROCK, ALADDIN, iSHARES, iBONDS, FACTORSELECT, iTHINKING, iSHARES CONNECT, FUND FRENZY, LIFEPATH, SO WHAT DO I DO WITH MY MONEY, INVESTING FOR A NEW WORLD, BUILT FOR THESE TIMES, the iShares Core Graphic, CoRI and the CoRI logo are registered and unregistered trademarks of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

The Funds are distributed by BlackRock Investments, LLC (together with its affiliates, "BlackRock").

284437

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All