What happened: Japanese Prime Minister Shinzo Abe’s Liberal Democratic Party (LDP) and its coalition partners scored a convincing win that will maintain its large majority in both houses of parliament. This should extend the lifespan of "Abenomics," including the Bank of Japan's (BoJ) mega stimulus.

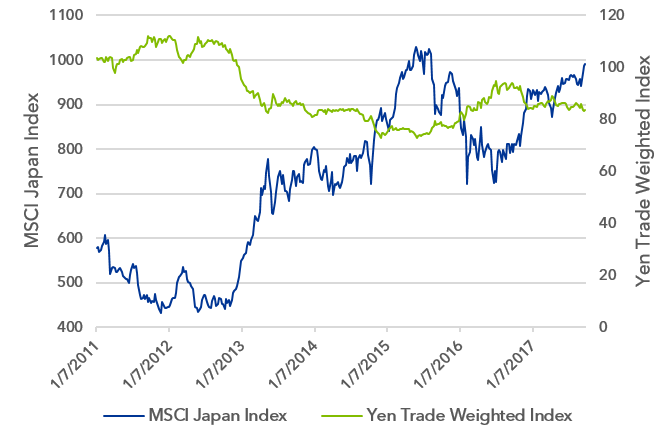

Potential market impacts: We see the outcome as a mild positive for Japanese equities, though recent strong performance may spark some profit taking. We're positive on Japan thanks to the synchronized global expansion that currently appears to be supporting growth, attractive valuations and solid earnings momentum. We also see the election result as a mild negative for the yen and Japanese government bonds.

Policy continuity: We don't expect major changes to fiscal or monetary policy. Although we see a less than 50-50 chance that BoJ Governor Haruhiko Kuroda stays on for a second term after his term expires in 2018, in what would be a first at the BoJ, any successor is likely to be a similar policy dove, given that inflation is stuck well short of its 2% goal. Yet we see the potential for greater uncertainty with a new governor at the BoJ's helm

Why investors should care

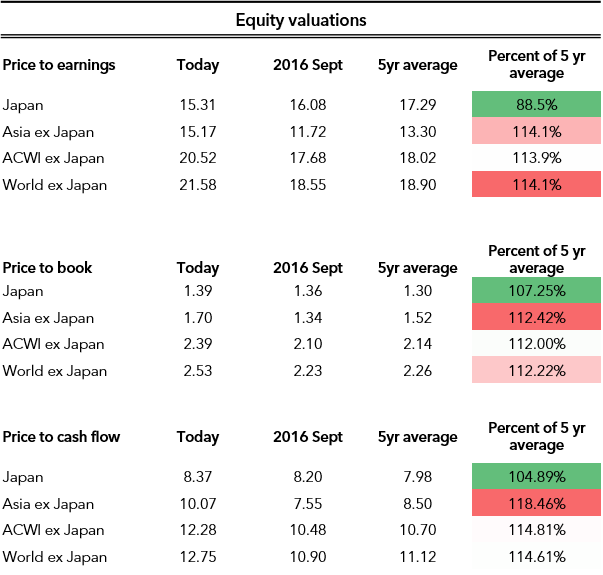

Market view: Japanese equities have recently begun outperforming the U.S. this year, after lagging for much of the year, rising 17.95% as of October 18th (Source: Thomson Reuters, based on MSCI Japan Index). We continue to favor Japanese equities for several reasons, including: currently attractive valuations, improved earnings outlook, and continued BoJ accommodation. The composition of the next government, therefore, has consequences for the future path of reform and BoJ policies.

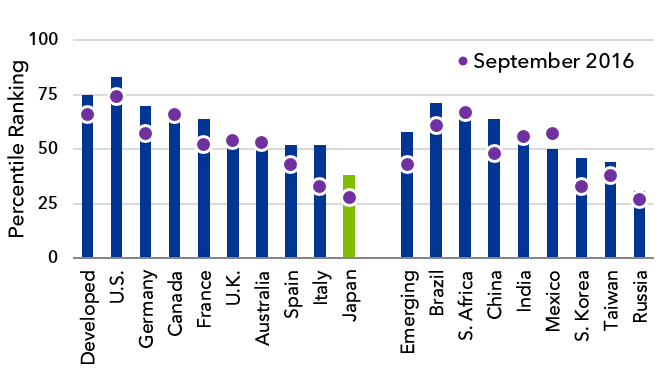

Valuation of Japanese equities vs. history

and other regions

Current valuation (bars) vs. one year ago (dots)

Sources: BlackRock Investment Institute and Thomson Reuters, September 29, 2017. Percentile ranks show valuations of assets versus their historical ranges. Example: If an asset is in the 75th percentile, this means it trades at a valuation equal to or greater than 75% of its history. Valuation percentiles are based on an aggregation of standard valuation measures versus their long-term history. Equity valuations are based on MSCI indexes and are an average of percentile ranks versus available history of earnings yield, trend real earnings, dividend yield, price to book, price to cash flow and 12-month forward earnings yield. Index performance is for illustrative purposes only. Index performance does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.