Are ICOs Replacing IPOs?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

This week I was in Barcelona speaking at the LBMA/LPPM Precious Metals Conference, which was attended by approximately 700 metals and mining firms from all over the globe. I found the event energizing and stimulating, full of contrary views on topics ranging from macroeconomics to physical investment markets to cryptocurrencies.

My keynote address on Tuesday focused on quant investing in gold mining and the booming initial coin offering (ICO) market. I’m thrilled to share with you that the presentation was voted the best, for which I was awarded an ounce of gold. I want to thank the London Bullion Market Association, its members and conference attendees for this honor.

Speaking of gold and cryptocurrencies, the LBMA conducted several interesting polls on which of the two assets would benefit the most in certain scenarios. In one such poll, attendees overwhelmingly said the gold price would skyrocket in the event of a conflict involving nuclear weapons. Bitcoin, meanwhile, would plummet, according to participants—which makes some sense. As I pointed out before, trading bitcoin and other cryptos is dependent on electricity and WiFi, both of which could easily be knocked out by a nuclear strike. Gold, however, would still be available to convert into cash.

It’s a horrific thought, but the poll results show that the investment case for gold as a store of value remains favorable. Goldman Sachs echoed the idea this week, writing in a note to investors that “precious metals remain a relevant asset class in modern portfolios, despite their lack of yield.” The investment bank added that precious metals “are still the best long-term store of value out of the known elements.”

Metcalfe’s Law Suggests Crypto Prices Could Keep Rising

This isn’t meant to knock bitcoin and other virtual currencies. Because they’re decentralized and therefore less prone to manipulation by governments and banks—unlike paper money and even gold—I think they could also have a place in portfolios.

Even those who criticize cryptocurrencies the loudest seem to agree. JPMorgan Chase CEO Jaime Dimon, if you remember, called bitcoin “stupid” and a “fraud,” and yet his firm is a member of the pro-blockchain Enterprise Ethereum Alliance (EEA). Russian president Vladimir Putin publicly said cryptocurrencies had “serious risks,” and yet he just called for the development of a new digital currency, the “cryptoruble,” which will be used as legal tender throughout the federation.

Follow the money.

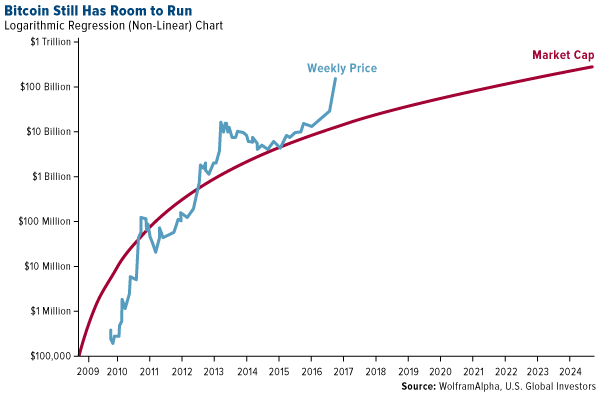

Metcalfe’s law states that the bigger the network of users, the greater that network’s value becomes. Robert Metcalfe, distinguished electrical engineer, was speaking specifically about Ethernet, but it also applies to cryptos. Bitcoin might look like a bubble on a simple price chart, but when we place it on a logarithmic scale, we see that a peak has not been reached yet.

Bitcoin adoption could multiply the more people become aware of how much of their wealth is controlled by governments and the big banks. This was among the hallway chatter I overheard at the Precious Metals Conference, with one person commenting that what’s said in private during International Monetary Fund (IMF) meetings is far more important than what’s said officially.

I have a similar view of the G20, whose mission was once to keep global trade strong. Since at least 2008, though, the G20 has been all about synchronized taxation to grow not the economy but the role government plays in our lives. Trading virtual currencies is one significant way to get around that.

The Incredible Shrinking IPO Market

Just as water takes the path of least resistance, money flows where it’s respected most.

You need only look at the mountain of cash U.S. multinationals have stashed overseas, currently standing at an estimated $2.6 trillion. The steep 39 percent U.S. corporate tax rate—the highest among any country in the Organization for Economic Cooperation and Development (OECD)— discourages companies from bringing their profits back home and reinvesting them in new equipment and employees.

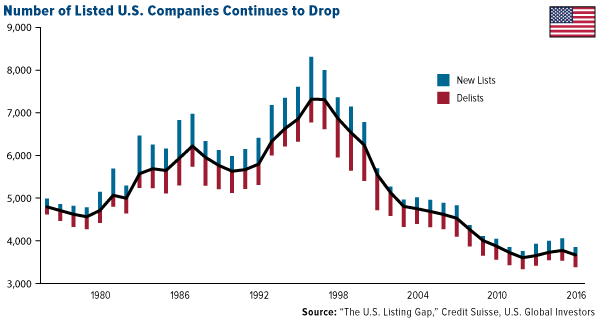

Of course, taxes aren’t the only type of friction money can run up against. More and more stringent financial rules and regulations have been one of the top destroyers of capital and business growth over the past 20 to 30 years. The Sarbanes-Oxley Act, signed in 2002, is widely blamed for limiting the number of initial public offerings (IPOs) that occur in the U.S. The legislation has made it prohibitively expensive for many smaller firms to get listed on an exchange. Between 1996 and 2016, the number of investable U.S. companies was cut in half, falling from 7,322 to 3,671.

This has ultimately hurt everyday retail investors who not only have fewer stocks to invest in now but also lack access to many of the same potentially profitable opportunities enjoyed by angel investors, venture capitalists and other institutional investors. Private equity and venture capital can be much higher-yielding investments than common asset classes such as Treasuries and equities, but for the most part, only accredited investors can participate.

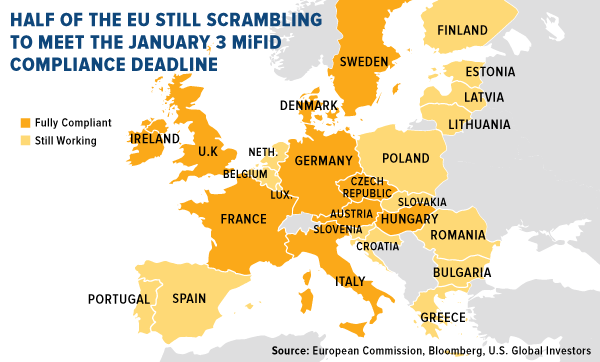

IPOs could be squeezed even further after the implementation of the European Union’s (EU) revised Markets in Financial Instruments Directive (MiFID), set to go into full effect January 3. The directive, initially passed in response to the financial crisis, acts as a sweeping reformation of existing trading rules that affect everything from stocks to bonds to commodities. All 28 EU nations must have laws in place to comply with MiFID by the January deadline—or face litigation and fines.

With less than two months left on the clock, 17 countries, including Spain, Portugal and the Netherlands, are still scrambling to convert MiFID into national law, according to Bloomberg. This is creating all sorts of financial uncertainty for banks, insurers and money managers on both sides of the Atlantic.

One rule in particular could threaten U.S. IPOs. It states that, to be more transparent, banks must now “unbundle” the costs of investment research from that of executing trades, a practice that’s been routine for decades. To produce stand-alone research, banks must register as investment advisers, a costly process that might prompt some firms to avoid it altogether. This would limit investors’ exposure to only the largest companies and, in turn, discourage smaller U.S. firms from pursuing an IPO, according to Cowen & Co. analysis and reported by Bloomberg.

MiFID is just the latest in a long string of regulations that, while conceived with good intentions, carry unintended consequences. It’s doubly unfortunate that an EU rule could so impact U.S. companies’ ability to gain the publicity necessary to go public.

But hasn’t this been the trend for years now? In many ways, doing business in the EU has only gotten more challenging, and bureaucrats seem determined to take punitive steps against successful American firms.

Look at how Facebook, Google and other large tech companies have been treated in Europe. Back in June, the search giant was slapped with a record $2.8 billion antitrust fine and has since been strongarmed into changing its online shopping service.

A restrictive regulatory backdrop is largely responsible for this. Because rules are so tight, European companies have a hard time innovating and staying competitive. So instead of building its own Facebook or Google, the EU’s only other recourse is to take a protectionist approach and wrap the 28-member bloc in more and more red tape.

For Many Startups, ICOs Are a Solution

I believe this is part of the reason why we’re seeing such a massive surge in ICOs, which, at the moment, are nearly unregulated in the U.S. and Europe. In an effort to bypass the rules and costs associated with getting listed on an exchange, many startups now are opting to raise funds by issuing their own digital currency based on blockchain technology. And unlike with private equity, smaller retail investors can participate.

Again, money flows where it’s respected most.

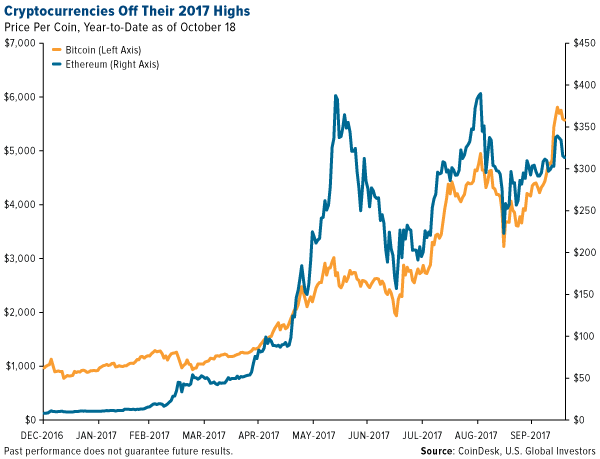

Bitcoin and Ethereum are the best known cryptocurrencies, but there are more than 1,000 being traded around the world, with a combined market cap of around $150 billion, according to Bank of America Merrill Lynch (BoAML).

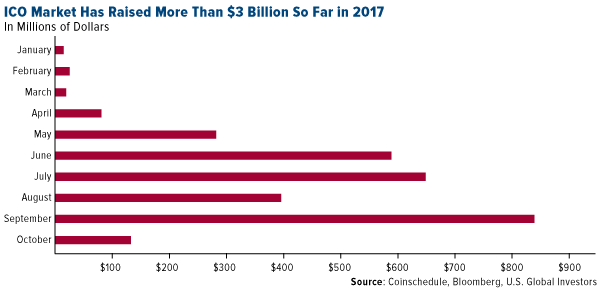

As of this month, IPOs have raised over $3 billion in 2017, more than seven times the amount generated in all years prior to 2017 and far surpassing expectations of around $1.7 billion for the year.

To give you some perspective, the U.S. IPO market raised $4.1 billion from 29 deals in the September quarter alone, according to Renaissance Capital. Although this dwarfs the ICO market in dollar terms, both the number of IPOs and the amount raised are significantly lower than the same quarter in 2014, which saw an impressive $37.6 billion raised from 60 deals.

As long as the barriers to getting listed remain high, I expect we’ll see this trend of fewer IPOs and more ICOs continue.

Not all cryptocurrencies will survive, obviously, and we’ll likely see huge transformations in the space before clear leaders pull away from the pack. Remember, no one knew in 1997 which internet companies would eventually dominant the others.

But for now, it’s an exciting time for an asset class that didn’t even exist 10 years ago. Trading above $6,000 for the first time this week, bitcoin reached a market cap of $96.7 billion. Amazingly, that’s more than Goldman Sachs’ market caps of $92.9 billion.

It’s important for investors to know that cryptos do face potential regulation risk. What kind of risk, though, is currently up in the air as U.S. regulators debate whether digital currency is a security or commodity. One would place it within the jurisdiction of the Securities and Exchange Commission (SEC), the other within the jurisdiction of the Commodity Futures Trading Commission (CFTC). Unsurprisingly, both agencies see cryptos as their own.

This week also highlighted a new risk in the fledgling market. Tezos, the firm behind what was at the time the largest ICO in history, revealed a significant slowdown in the progress of its virtual coin, the “tezzie.” Back in July, Tezos made headlines for raising a then-unprecedented $232 million. But today, the group, headed by a husband-and-wife duo, is faced with a number of setbacks including a lack of developers and a highly-publicized management dispute.

According to the Wall Street Journal’s Paul Vigna, this has “put trading of Tezos tokens held by investors in limbo while also putting some of the technology on hold as well.”

Diwali Fails to Light Up Gold

Turning to gold, the yellow metal made healthy gains last week, climbing more than 2.3 percent as we headed closer to the first day of Diwali. As I’ve explained numerous times before, it’s considered auspicious to give gifts of gold bullion and jewelry during the Hindu Festival of Lights, and in years past we’ve seen some price appreciation in the days and weeks leading up to the celebration.

This week, though, the gold price fell below $1,300 an ounce as stocks continued their record-setting bull run.

But as the LBMA poll shows, it’s prudent to have some gold in your portfolio, as it’s negatively correlated with other assets. As always, I recommend a 10 percent weighting, with 5 percent in physical gold and 5 percent in gold stocks, and remember rebalance every year.

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 2 percent. The S&P 500 Stock Index rose 0.86, while the Nasdaq Composite climbed 0.35 percent. The Russell 2000 small capitalization index gained 0.44 percent this week.

- The Hang Seng Composite gained 0.05 percent this week; while Taiwan was up 0.04 percent and the KOSPI rose 0.64 percent.

- The 10-year Treasury bond yield rose 11 basis points to 2.38 percent.

Domestic Equity Market

Strengths

- Financials was the best performing sector of the week, increasing 1.97 percent compared to an overall increase of 0.77 percent for the S&P 500 Index.

- W.W. Grainger was the best performing stock for the week, increasing 14.78 percent.

- The Dow Jones Industrial Average breached the 23,000-mark for the first time on Tuesday. The blue-chip index has surpassed four similar 1,000-point milestones this year, indicating investor faith in the bull market despite lofty stock valuations.

Weaknesses

- Consumer staples was the worst performing sector for the week, falling 1.23 percent.

- United Continental was the worst performing stock for the week, falling 11.35 percent.

- Nordstrom postponed its effort to go private. The stock fell as much as 7 percent on Monday after the Nordstrom family postponed its attempt to take the company private, struggling to raise enough debt to finance the deal.

Opportunities

- Morgan Stanley says that Netflix is benefiting from a virtuous circle. "Netflix's recent price increases in the U.S. and abroad are a positive indication of its confidence in the subscriber opportunity ahead," analysts write. Additionally, Netflix beat its subscriber growth targets, adding 5.3 million during the third quarter.

- An activist hedge fund wants to break up Credit Suisse. The Swiss hedge fund RBR Capital Advisors, which is led by Gaël de Boissard, a former co-head of investment banking at Credit Suisse, wants to split up the bank after its stock has fallen 20 percent since Tidjane Thiam took over as CEO in 2015, according to the Financial Times.

- The company behind Burger King wants to take over fast food and could buy Papa John's as a result. Restaurant Brands International has recently snapped up popular fast food chains including Popeye's.

Threats

- In a client note, Morgan Stanley analysts write that "if stocks follow the pattern they have been all year, actual earnings season will be a sell the news event and we could have a decent pull back or consolidation. Near term, a correction is looking more likely.” The analysts lay out five possible negative catalysts that could spur such a correction: the unwinding of the Federal Reserve's balance sheet; tax-cut legislation that proves to be more difficult; the announcement of a new Fed chief could that could disrupt financial conditions; the U.S. dollar, which looks to be reversing to the upside; and leading economic indicators which are hitting extremes, suggesting peaks are "more likely than not."

- Morgan Stanley analyst Adam Jonas published a research note on Monday in which he explored the complexity of Ford's "restructuring roadmap" under the company's new CEO Jim Hackett. The goal is to generate $12 billion in cost savings by 2022. Jonas scrutinized a range of options and wrote, "we believe many of Ford's restructuring actions are meant to ensure the fitness of the company's operations during a highly uncertain time which may include a reduced value of its products in the second-hand market, particularly as Ford and its peers introduce superior technologies in critical areas such as connectivity, propulsion and automation." His report suggests that when radically new and different vehicles, like electric and self-driving vehicles, begin to hit the market, the cars that lack these technologies will be abandoned. This would leave carmakers with losses for the plunging residual values of their "Auto 1.0" products.

- Wall Street's short sellers are beginning to talk about health care as the next major threat to the U.S. economy.

October 16, 2017Car Manufacturers Are Electrifying Copper, “The Metal of the Future” |

October 11, 2017Germans Have Quietly Become the World’s Biggest Buyers of Gold |

October 9, 2017Here’s Why Bitcoin Won’t Replace Gold So Easily |

Strengths

- The Empire Manufacturing Index came in much stronger than expected at 30.2 versus forecasts of 20.4.

- U.S. industrial production recovered month-over-month, posting a 0.3 percent gain after last month’s reading of negative 0.9 percent.

- Existing home sales beat expectations. Month-over-month sales grew 0.7 percent, ahead of forecasts for a 0.9 percent drop.

Weaknesses

- The U.S. posted its largest budget deficit since 2013 in the fiscal year that just ended, as a pickup in spending exceeded revenue gains. The federal government’s gap grew to $665.7 billion in the 12 months through September 30, compared with a $585.6 billion shortfall in fiscal 2016, the Treasury Department said Friday.

- The leading economic index for September came in at negative 0.2 percent, below the forecast for a 0.1 percent gain.

- September housing starts came in at 1.127 million, below expectations for 1.175 million and below the previous month’s figure of 1.180 million.

Opportunities

- The yield spread between two- and 10-year Treasuries fell to 75.3 basis points on Tuesday, brushing up against the lowest intraday level since 2007. According to BMO Capital Markets strategists, this is just the beginning, with the Federal Reserve seemingly on track to raise rates again in December. The curve has flattened by an average of 21.5 basis points between the fourth and fifth hikes in a tightening cycle, the analysts said, meaning the spread should be closer to 60 basis points in two months. That would favor a longer duration positioning in the near-term.

- The Senate passed its budget, clearing a huge hurdle for President Donald Trump's tax plan. The 2018 budget resolution passed with a 51-to-49 vote, paving the way for Republicans to pass a tax bill without support from Democrats.

- Trump’s closest advisers are steering him toward choosing either Stanford economist John Taylor or Federal Reserve Board Governor Jerome Powell to be the next Fed chief, according to several people familiar with the process.

Threats

- Puerto Rico’s most actively traded bonds dropped for the sixth straight day on Wednesday, pushing the price to a record low, amid speculation that the devastation caused by Hurricane Maria will leave investors facing deeper-than-anticipated losses. GO bonds due in 2035 fell to an average of 30.4 cents on the dollar. The price has tumbled 47 percent since the storm struck in September.

- It’s been more than eight years since the last recession, but nearly a third of U.S. states aren’t ready for the next one. Fifteen state governments don’t have enough money saved to make up for the revenue that would disappear during a moderate recession, with Louisiana, North Dakota and Oklahoma the least prepared, according to stress tests conducted by Moody’s Analytics. New Mexico, Illinois, Colorado, New Jersey, Pennsylvania, Missouri, Kansas, Virginia, Vermont, Arizona, Arkansas and Connecticut were also judged ill-equipped. Moody’s Analytics isn’t forecasting a recession, though it said another one is only a matter of time.

- U.S. high-yield bonds are trading in the tightest range in 20 years, emphasizing the notion that the grab for yield has made investors complacent. So far this year, the difference between the highest and the lowest spread notched at the index level is 71 basis points. The range is narrower than in 1997 and 2006, years that marked the peak of the global credit cycle, according to analysis from CreditSights.

Gold Market

This week spot gold closed at $1,280.50, down $24.07 per ounce, or 1.85 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.59 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index came in off just 0.99 percent. The U.S. Trade-Weighted Dollar reversed course this week and rose 0.64 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-17 | Eurozone CPI Core YoY | 1.1% | 1.1% | 1.1% |

| Oct-17 | Germany ZEW Survey Current Situation | 88.5 | 87.0 | 87.9 |

| Oct-17 | Germany ZEW Survey Expectations | 20.0 | 17.6 | 17.0 |

| Oct-18 | Housing Starts | 1175k | 1127k | 1183k |

| Oct-18 | China Retail Sales YoY | 10.2% | 10.3% | 10.1% |

| Oct-19 | Initial Jobless Claims | 240k | 222k | 244k |

| Oct-25 | Durable Goods Orders | 1.0% | -- | 2.0% |

| Oct-25 | New Home Sales | 555k | -- | 560k |

| Oct-26 | Hong Kong Exports YoY | 6.6% | -- | 7.4% |

| Oct-26 | ECB Main Refinancing Rates | 0.000% | -- | 0.000% |

| Oct-26 | Initial Jobless Claims | 235k | -- | 222k |

| Oct-27 | GDP Annualized QoQ | 2.6% | -- | 3.1% |

Strengths

- The best performing precious metal for the week was palladium, off 1.44 percent for the week. Citigroup favors palladium in the short term, in response to pollution control, but says substitution risks prevent the bank from taking a more bullish view long-term as the price of palladium is now higher than the price of platinum.

- After the Indian government eased rules on gold purchases, the country’s demand for gold jewelry and branded coins appears to be better than the last quarter, according to P.R. Somasundaram, MD for India at the World Gold Council. The ensuing wedding season is the key for quarterly demand performance, Bloomberg reports, and with a good monsoon season, stable gold prices should encourage consumers.

- In the month of September, Swiss gold exports doubled month-over-month to 148.4 metric tons, reports Bloomberg. In August, exports were only 72 tons, according to the Swiss Federal Customs Administration. Specifically, Swiss exports to China rose 21 percent and to Hong Kong rose 92 percent.

Weaknesses

- The worst performing precious metal for the week was platinum, off 2.41 percent as palladium seems to be the more crowded trade.

- September makes 11 months straight of China officially reporting a zero increase in the level of its gold reserves, writes Lawrie Williams. The only time in recent years that the Asian nation has published any month-by-month gold reserve accumulations was in the 16 months ahead of the yuan being accepted as an integral part of the International Monetary Fund’s (IMF) Special Drawing Rights basket of currencies, Williams continues. “We don’t think it coincidence that such month-by-month reporting effectively ceased once the yuan became part of the SDR, thus paving its way for acceptance as a reserve currency,” the article reads.

- Barrick Gold and the Tanzanian government have been in talks for months to resolve a dispute that has hit Barrick’s operations in the country. The two sides announced that Barrick will give Tanzania a 16 percent stake in three gold mines, a 50 percent share in revenues from the mines and a one-off payment of US$300 million. Following a surge in shipments in recent months, India moved to curb gold-trade irregularities by preventing some trading houses from importing the metal, reports Bloomberg. This comes after a jump in purchases from overseas nations like South Korea and Indonesia—which have free-trade agreements with India—“as traders try to bring in gold at zero tax and avoid paying a 10 percent import duty,” the article continues.

Opportunities

- Up or down, the stock market may support gold, according to Bloomberg Intelligence. Gold is trading at half the price-to-value of the S&P 500 Index. “The first revisit near 0.50 in the XAU/SPX ratio in eight years coincide with the first Federal Reserve rate hike in December 2015,” the article notes. This marked not only a bottom for gold, but also in gold ETF holdings. Investors who are scared to sell strong-momentum stocks are buying more gold to diversify. In addition, according to a survey of attendees at the LBMA Precious Metals Conference in Barcelona this week, gold will be at $1,369 an ounce by this time next year.

- Pierre Lassonde, chairman and co-founder of Franco-Nevada, has pioneered the royalty business model in the gold mining sector and is arguably one of the most successful individuals in the mining space, reports Zero Hedge. According to Lassonde, however, the gold industry hasn’t made any large discoveries for years. He points out in a recent interview that over the last 15 years, we have found no 50 million or 30 million-ounce deposits, and only very few 15 million-ounce deposits. In addition, Lassonde says that production is coming off, meaning the upward pressure on the gold price could be very intense. He continues with a discussion on funding and explains that investor risk appetite is gone, and juniors haven’t had any money for nearly 10 years, despite the fact that more than half of the new discoveries over the years have been made by junior companies. His thoughts end with his sentiment on the yellow metal despite all of this. “I think for an average investor, it should be the absolute rule to hold around 5 to 10 percent gold in your portfolio, like rule number one.”

- Even though there are claims stating that Goldman Sachs has considered launching a bitcoin trading operation, the bank says that digital currencies “are not the ‘new gold’” and that gold is still the “best long-term store of value,” reports CNBC. This can be shown in a recent Bloomberg Intelligence article, which shows that precious metals is the only sector that consistently gains when stocks decline sharply—with gold leading the way. Gold is the “consistent diversifier.”

Threats

- Even before new regulations come in, the average net daily volume of gold settled by London Precious Metals Clearing fell 12 percent in two months on London’s over-the-counter (OTC) market, to 18.5 million ounces in August, reports Bloomberg. In New York, London’s biggest rival, trading in gold contracts jumped more than 25 percent in the third quarter, specifically with activity during European hours surging 32 percent, the article continues. Traders are now scratching their heads over how changes to EU rules over transaction reporting could affect their costs in London. The issue is whether OTC trading of gold should count as derivative trading.

- In Europe, registrations for cars over the last six months have only grown 1.57 percent year-over-year on average—that’s down from 8.02 percent growth during that same six months last year, reports Macro Strategy Partnership. This low growth suggests a substantial slowdown and could spell trouble for palladium.

- A special science note: Business Insider reports this week that scientists who won a Nobel Prize for their discovery of gravitational waves announced the first-ever detection of the collision of two neuron stars on Monday. The team alerted astronomers worldwide, who helped them point telescopes directly at the crash scene. “These images revealed a radioactive soup giving birth to unfathomable amounts of platinum, gold and silver—not to mention the iodine in our bodies, uranium in nuclear weapons and bismuth in Pepto-Bismol—while blasting those materials deep into space,” the article reads. According to some estimates, this neutron star collision produced around 200 Earth masses of pure gold, and maybe 500 Earth masses of platinum. But at 130 million light years away, don’t count on getting your hands on this anytime soon.

Energy and Natural Resources Market

Strengths

- Copper was the best performing major commodity this week, rising 1.1 percent. The metal’s price rallied on the back of strong factory-gate price inflation in China, suggesting industrial demand for commodities and commodity-related output remains strong.

- The best performing sector this week was construction and materials. Major suppliers of construction materials rose 4.5 percent as recent hurricanes in the U.S. are expected to result in positive demand growth, while customers seek additional supplies for reconstruction work. In addition, the passing of the 2018 U.S. budget suggests the much-anticipated Trump infrastructure plan may be able to move forward.

- DQ New Energy Corp., a producer of photovoltaic cells for use in solar power, was the best performing stock in the broader resource market this week. The stock rallied 12.25 percent to a 52-week high after it announced its decision to proceed with a major capacity expansion, suggesting that demand has been much stronger than anticipated.

Weaknesses

- Zinc, a critical steel-making ingredient, was the worst performing major commodity this week, dropping 3.6 percent. The commodity dropped after China’s leadership, at the 19th Party Congress, reiterated its commitment to clean air and the enforcement of environmental policies that have resulted in the early closure of numerous steel mills in the country.

- The worst performing sector this week was oil and gas services and equipment. The group dropped 5.2 percent after weekly data showed a considerable decline in U.S. oil production, together with a drop in active oil rigs. The data suggests that crude producers are not growing production at these crude price levels, thus requiring less services and equipment.

- The worst performing stock for the week was Polski Koncern Naftowy Orlen. The Polish refiner and distributor of gasoline and fuels dropped 7.8 percent after reporting disappointing third quarter results which showed weaker than expected refining and downstream margins.

Opportunities

|

- Iron ore prices may be set for a sustained rally as the top four producers tighten the grip on supply, according to a Bloomberg story. The top four ore producers—Vale SA, BHP Billiton, Rio Tinto Group and Fortescue Metals Group—will see their share of the seaborne market jump from 75 percent to about 85 percent in 2022, according to Evraz Plc, Russia’s second-largest steelmaker. “With such a market consolidation, it will allow them a certain impact on prices. They will have more ability to control the market,” Nikolay Ivanov, Evraz’s chief financial officer, said in an interview in London on Wednesday.

- China's factory-gate prices shot up to a six-month high last month, the Wall Street Journal reports. Mining stocks were pushed up after China’s producer prices leapt 6.9 percent in September compared with the same period a year ago, beating a 6.4 percent rise forecast by economists.

- Steel prices may see incremental demand from automakers as manufacturers have figured out how to make steel lighter without compromising its strength or versatility. ArcelorMittal, a global steel manufacturer, expects automakers’ global demand for press-hardened steel sheet, which is strong and malleable for complex stamped parts, to grow 36 percent by 2020 to 3.7 million metric tons.

Threats

- The U.S. dollar posted a broad-based rally as Stanford University economist John Taylor is said to have made a positive impression on President Donald Trump. Taylor is the namesake of the well-known “Taylor Rule” that would generally advocate higher interest rates. Currently, independent calculations suggest the “Taylor Rule” implied Federal Reserve rate should rise to 3.5 percent, a move that would normally result in a sizeable appreciation of the U.S. dollar, and a drop in commodity prices.

- China’s economy growth for the third quarter disappointed. GDP rose 6.8 percent in the third quarter, below expectations of 6.9 percent. Fixed-asset investment by private enterprises, a measure that is highly correlated with commodity demand in China, grew only 6 percent through the first nine months of the year, below expectations, and behind the 11 percent pace for government-related groups.

- U.S. September housing starts disappointed market analysts and suggest demand for construction materials may weaken. Housing starts for September posted a 4.7 percent drop, significantly below the rate expected. Starts were driven lower by the South region, likely reflecting some hurricane impact on the measurements.

Strengths

- South Korea’s KOSPI Index rose 64 basis points and Singapore’s Straits Times Index climbed 48 basis points in a week of relatively quiet trading regionally.

- China’s third quarter GDP came in right in line with analysts’ estimates for a showing of 6.8 percent, reassuring investors and maintaining a robust growth rate heading into the 19th Party Congress meetings that started this week.

- China also put out several other strong data, with retail sales, industrial production, new yuan loans and aggregate Financing all coming in higher than expected, albeit just slightly so.

Weaknesses

- Thailand’s SET index, which was closed last Friday in honor of the anniversary of the death of King Bhumibol last year, finished down 1.15 percent this week.

- China’s September period year-over-year Fixed Assets Investment, or FAI, dropped to 7.5 percent from 7.8 percent in August, coming in slightly below expectations for a 7.7 percent print.

- Both year-over-year imports (at 13.13 percent) and exports (at 15.60 percent) missed in Indonesia.

Opportunities

- China’s 19th Party Congress has thus far not brought any major surprises. The Congress continues, and investors will pay particular attention to membership in and possible messages of the powerful Politburo and the even more powerful Standing Committee—the very top leadership in China—which will be announced near the conclusion of the Congress. President Xi Jinping’s three-hour speech this week at the opening of the Congress indicated a furthering of steps already in motion and discussed: e.g. deleveraging, supply-side reforms, etc. Notably (although once again, not new either for Xi or China at this point), President Xi referenced China in customary ways but also introduced the adjective “beautiful,” probably implying greater emphasis upon growing and official incorporation of environmental protection as a national priority in the future. Note also that Xi’s roadmap extended beyond the usual “Five Year Plan” to look out as far as 2050.

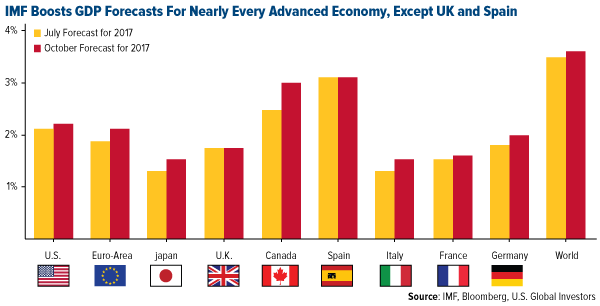

- According to the International Monetary Fund (IMF), the global economy is set to grow 3.6 percent this year and 3.7 percent next year, with Asia contributing 63.3 percent of the expansion, reports Bloomberg. The revival of import demand in China has been a source of strength across Asia, along with a revival of Asian exports to the U.S. and Europe.

- Bloomberg reports that the Philippine Stock Exchange Inc. is in talks with China’s Shenzhen bourse about a possible investment. The CEO of PSE, Ramon Monzon, said, “[W]e want to have a Shenzhen-Manila connect” program.

Threats

- People’s Bank of China Governor Zhou Xiaochuan warned at an event on the sidelines of the 19th Communist Party Congress in Beijing this week, that a sudden slide in optimism could trigger a jolting collapse in asset prices, reports Bloomberg. “When there are too many pro-cyclical factors in an economy, cyclical fluctuations will be amplified,” Zhou said. “If we’re too optimistic when things go smoothly, tensions build up, which could lead to a sharp correction, what we call a Minsky Moment.”

- Lab experiments on a new strain of the H7N9 bird flu in China suggest that the virus can transmit easily among animals and can cause lethal disease, writes Reuters. This strain raises the alarm that the virus could “trigger a global human pandemic,” according to researchers.

- Secretary of State Rex Tillerson said in an interview on Thursday that the U.S. isn’t necessarily frustrated with China, but made clear the administration wants more progress, reports Bloomberg. These remarks follow his speech Wednesday where he accused the Asian nation of undermining the “international, rules-based order.” Tillerson is quoted as saying, “We’re expecting to see some change, we’re expecting to see some movement, whether it’s North Korea, or whether it’s the South China Sea, or whether it’s trade.”

Strengths

- Turkey was the best performing country this week, gaining 2 percent. Airlines and airport operators were among the best performing stocks this week, rebounding from last week’s sell off after Turkey and U.S. mutually suspended visa service.

- The Czech koruna was the best relative performing currency this week, gaining 10 basis points against the dollar. Czech Republic has the lowest unemployment rate in the 28-member Eurozone, and the koruna has been the best performing currency in the past two decades among major currencies worldwide. The Czech Republic’s central bank was Europe’s first to hike rates earlier this year.

- Industrials was the best performing sector among Eastern European markets this week.

Weaknesses

- Poland was the worst performing country this week, losing 2.5 percent. Polski Koncer Naftowy (PKN), a refinery, and LPP SA, both declined more than 8 percent. PKN missed third-quarter earnings, and LPP announced plans to invest 1.5 billion zloty in network expansion by the end of 2020.

- The Turkish lira was the worst performing currency this week, losing 1 percent against the dollar. The currency is very sensitive to the dollar strength, and as the dollar moves higher, the lira becomes weaker. Turkey extended its state of emergency for the fifth time after the failed coup attempt in July of last year.

- The consumer discretionary sector was the worst performing sector among Eastern European markets this week.

Opportunities

- The World Bank revised up its 2017 GDP growth forecast for the Central Europe region by 0.5 percentage points to 3.7 percent and its 2018 view by 0.3 points to 3.4 percent. Poland’s economic growth is projected to reach 4 percent in 2017, up from 2.7 percent in 2016, on the back of robust consumption, a strong labor market and the child benefit program “Family 500+”, according to the World Bank’s latest Regional Economic Update, “Migration and Mobility in Europe and Central Asia.”

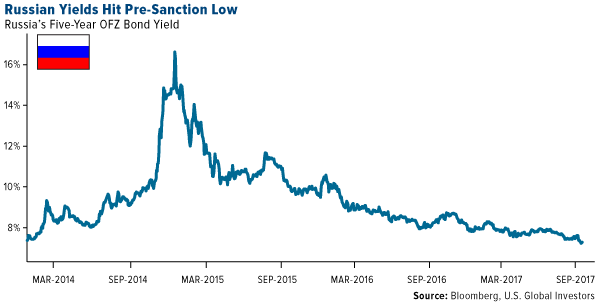

- According to Bloomberg, Russian yields last seen before the 2014 annexation of Crimea are unlikely to diminish the appetite of investors looking for higher returns in emerging markets. With five-year government bonds yielding around 7.5 percent, and inflation falling to to 3.1 percent, Russia still offers one of the highest real rates in emerging markets. Foreign ownership of government bonds, called OFZs, reached a new record high of 32 percent in August, according to Central Bank data.

- Czech Republic parliamentary elections will take place this weekend, and opinion polls are showing billionaire Andrej Babis, leader of the ANO party, as the most likely winner. Wood & Company analysts Leo Wang, Raffaella Tenconi and Marta Jerzewska-Wasilewska predict that ANO will lead the next government in coalition with two smaller parties. “A perceived business-friendly government, together with robust growth backdrop, should be favorable for stocks and may also help tighten government bonds yields,” the team writes.

Threats

- German Chancellor Angela Marker is in talks to bring together her center-right movement, the Christian Democratic Union; its Bavarian sister party, the Christian Social Union; the pro-business, euroskeptic Free Democratic Party; and the liberal environmentalist Greens. It seems like these parties have more policy disagreements than overlaps, ranging from immigration policy to tax cuts. Merkel is at her weakest in her 12 years in power after her party received the lowest score since 1949, which analysts say will hinder her ability to compromise.

- The price of Brent crude oil is rising with global political tensions. Iraqi forces took control of the oil-rich province of Kirkuk, just three weeks after Kurdistan voted for its independence from Iraq. Iraqi Kurdistan exports nearly 600,000 barrels of oil a day, mostly through a pipeline that runs to Turkey, and some shipments already stopped. Also, President Donald Trump threatens to end the 2015 nuclear agreement with Iran, whose oil exports already returned to their pre-sanctions levels. Higher oil prices are negative for Turkey, as Turkey is a net importer of oil, and positive for Russia, as Russia generates most of its revenue from the sale of oil and gas.

- Uncertainty about the ultimate status of Catalonia is prompting companies to move their official addresses outside of Catalonia to different parts of Spain. Banks, for example, have a right to do business anywhere in the EU’s 28 states, but should Catalonia secede and break out from Spain and the EU, the banks would lose that right overnight if they are still officially based in Catalonia. Ratings companies Standard & Poor’s and Fitch Ratings placed Catalan debt on negative watch, signaling an increased chance of a downgrade.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All