What To Expect With Tax Reform

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThis Strategic Insights discusses how to bolster tax revenue by increasing potential growth, job opportunity, and productivity. This may be achieved by lowering tax rates, reforming regulation, simplifying the tax code, and incentivizing investment to enhance global competitiveness. Various guiding principles outlined herein suggest how to tackle the broader issue of fiscal reform, including spending and tax reform.

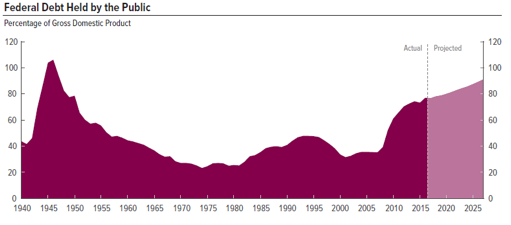

Today’s fiscal deficit remains high and unsustainable by global historical standards with rapidly expanding entitlement programs in excess of inflation. U.S. Debt/GDP exceeds 80% with a current 3% fiscal deficit---spending exceeds tax revenue by 3% of GDP. Treasury debt has doubled to $20 trillion since 2009. Only by extinguishing the fiscal deficit can we begin to bend the curve below.

Source: Congressional Budget Office (CBO)

Tax reform is one side of needed fiscal reform—spending also must be addressed to turn a high fiscal deficit into surplus during periods of economic growth. Raising tax rates historically slowed real growth in GDP and tax revenue as inflation increased. Growth has disappointed since 2009 due to higher tax rates1, spending, fiscal stimulus, and new regulations2, which limited growth and therefore tax revenue. Debt/GDP should be falling now, if not for misguided fiscal and regulatory policies. Pro-growth tax and regulatory reform can do the heavy lifting of fiscal reform with additional discipline of spending reform.

Drivers of spending growth are obvious in the chart below, including Social Security, retirement liabilities, health care, and interest. Mandatory outlays plus interest totalling $2.8 trillion in 2017 are 70% of the budget. Staring at this chart, we realize growth in mandatory spending programs must slow. Spending reform is politically difficult, but must be coupled with tax reform to extinguish our unsustainable fiscal deficit.

Meaningful tax reform should begin from first principles to simplify our complex tax code, distorted by decades of horse trading. Starting from scratch can reform tax administration, compliance and enforcement, while discarding deficient portions of the 70,000 page tax code. Meaningful tax reform was last enacted a generation ago in 1986. A simple flatter tax rate schedule to begin with allows Congress to incorporate majority-supported income deductions and tax credits that society deems equitable, without regard to special interests. Federal individual taxes were 14% of adjusted income versus the top rate of 39.6% in 2014. The 14% is a baseline for a flat tax that is often discussed. Final tax reform legislation will be compared to current law, but starting from scratch affords an opportunity to look beyond just winners and losers.

America’s fiscal profile has deteriorated over the past decade. Although bond yields remain low, soaring debt crowds out investment and increases credit risk premiums that can drive higher cost of capital. As interest rates normalize and central banks reduce bond holdings, interest on our $20 trillion debt of $270 billion will rise. The need to extend average Treasury maturity from a 50-year low of 4 years also will increase interest expense (Federal Reserve remits interest earned on Treasury holdings to Treasury---2.5% x $4T = $100B). The White House estimates that interest cost will exceed $700 billion in 2019. Tax, spending, and regulatory reform are needed to bolster potential growth and extinguish our fiscal deficit.

Government waste, fraud, and redundancy can be reduced in rationalizing the public sector. Private sector companies realized tremendous benefit from process improvement, cost rationalization, and technological innovation. The 2017 estimated fiscal deficit of $723 billion is -3.8% of GDP. If our debt burden fell, then raising the debt ceiling would not be required and threat of default would be mitigated.

Source: Strategic Frontier and U.S. Government

While often discussed, there must be opportunity for running our government more efficiently given the progress achieved in the private sector to increase profit margins by rationalizing costs and leveraging technology with process innovation as prices of consumer goods lagged inflation. Lack of spending discipline requires looking no further than the American Recovery and Reinvestment Act (fiscal deficit impact: $862 billion), which squandered so much money with no economic multiplier, nor increased productivity. Politicians hoped to reap good will, but there is discontent about how the money was spent, which added nearly a $1 trillion in debt. Hopefully, this precedent is an economic lesson well remembered.

The Unified Tax Reform Framework provides guidelines of key tax reform principles jointly embraced by Congress and the White House, but the framework is short of a legislative term sheet. It seeks to: improve tax administrative efficiency (lower tax collection, compliance, and enforcement costs), restore fairness (simplify tax code, eliminate special interest exemptions, and increase global competitiveness), and lower tax rates for all taxpayers to keep more of what they earned. This is a time for listening and debate to consider reform options, so we offer a perspective.

Perspectives in Fiscal and Tax Reform Principles

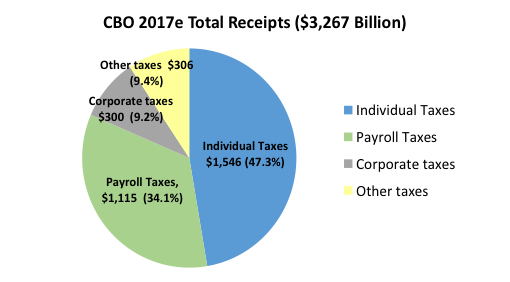

Various theories, facts, assumptions and forecasts from many perspectives will be considered over the coming months. We believe that tax reform is best achieved by starting from scratch. Corporate tax revenues are just 9.2% of budget, while individual (47.3%) and payroll (34.1%) taxes comprise over 80% of taxes collected. Estate and excise taxes are most of “other” taxes collected. Cutting corporate tax rates has far less impact on the budget than lowering individual tax rates, but we’d expect lower taxes to increase the corporate share of tax revenue, particularly if incentivizing repatriation of foreign earnings does increase. Foreign S&P 500 revenues have increased to over 50%, so it is not surprising corporate share of tax revenue has declined even with a steady 35% tax rate. Unrepatriated foreign earnings have been a material reason for the decline in corporate share of tax revenue. Finally, do consider the amount of payroll tax collected for Social Security and Medicare3. Think about it next time benefit means-testing is suggested.

Legislative Reform Objective: Increase potential growth, bolster productivity, increase free market competition, enhance global competitiveness, restrain inflation, reduce special interests, simplify tax code, reduce tax administrative costs, and balance budget, thereby bolstering prosperity and living standards that turn fiscal deficit to surplus, expand job opportunities.

Constraints: Primary functions of government include:

· Establish justice to enforce contracts and protect citizens from crimes,

· Strong national defense to protect U.S. interests,

· Defend individual rights of life, liberty and pursuit of happiness, including property rights,

· Insure tranquility and promote general welfare.

Everything else that government does is a decision based on democratically determined economic, social, and political objectives. That includes every social and entitlement program, as well as regulatory rules that incur government cost for which we tax income. Mandatory spending results from future benefits we promised to provide, and collected taxes to do so.

Permanent tax policies change taxpayer behaviors. Legislation must prioritize permanent fiscal policies, without sunsets or holidays, to incentivize investment, job creation, entrepreneurial activity, innovation, and production onshoring, while reducing barriers limiting repatriation of foreign earnings. Temporary initiatives or credits tend to limit benefits of fiscal reform objectives.

- Permanent tax policy changes provide the greatest improvement toward fiscal reform objectives.

Global average corporate tax rates have declined since the 1980s, as many followed America’s lead in tax reform. It is clear from the chart below that we are at a global competitive disadvantage as most other nations continued to cut rates. The growing divide in tax rates suggests why foreign earnings growth was faster and remains offshore unrepatriated.

This chart suggests a federal corporate tax rate of 20% would neutralize our competitive disadvantage. State and local tax rates boost the combined rate to 24% versus a comparable global average of 22%. The permanence principle suggests altering taxpayer behaviors is most effective with permanent policy changes, rather than tax holidays or temporary credits, as tried previously. Political battles arise seeking to extend temporary measures when tax changes sunset.

- A corporate rate of 20% is most politically feasible, encouraging greater investment and repatriation.

A 35% federal corporate rate (39.1% combined federal and average state tax rate) is the highest globally, which exceeds a comparable OECD average of 22% (23.5% comparable combined tax rate). Effective corporate tax rates averaged 29% with dispersion across taxpayers, so the statutory rate gap highlights the fairness disparity under current law. The Federal corporate rate needs to decline toward 20% to improve global competitiveness, resulting in a 24% combined tax rate. Tax simplification would eliminate special interest deductions and credits to narrow the gap between effective and statutory tax rates. Doing so may encourage higher tax rate states to simplify and improve fairness for their taxpayers. Comparative forces observed globally are visible across America between states, driving migration of those businesses and individuals taxed the most.

Source: Office of Management and Budget (OMB)

Given U.S. corporate tax rates are the highest globally, companies seek to avoid paying an additional 35% tax on foreign earnings, which now exceed $2.6 trillion based on public company balance sheet analysis. It is difficult to tally private company assets, but these unrepatriated assets encourage companies to invest offshore, buy foreign companies, or pursue inversions (change domicile to avoid U.S. tax). Such tax avoidance schemes are economically inefficient and nationally undesirable, but beneficial to net earnings.

A low permanent repatriation tax rate would encourage significant repatriation of most foreign earnings, and generate material tax revenue, while availing investment capital to boost our economic potential. A repatriation tax has had bipartisan support for years, but stalled because it is one source of tax revenue that politicians have hoped to couple with broader reform. Consideration of a one-time tax on accrued foreign earnings is a terrible idea and is likely unconstitutional as a wealth tax, but we don’t expect it in legislation. Apple’s CEO suggests they won't repatriate their profits without a lower or "fair" U.S. tax rate. We suggest a 10-15% fair tax would encourage repatriation by narrowing the gap to the cost of capital. Realized tax revenue would be significant. Upon implementation, an initial expected repatriation surge would boost capital for research and investment development. Foreign acquisitions and inversions would be less desirable.

- Lower corporate tax rates would encourage foreign earnings repatriation, but a 10-15% tax rate encourages more repatriation and better results.

Companies pay qualified dividends to shareholders from after-taxed profits, so government has already assessed these earnings. Dividends should not be doubly taxed, but a preferential top rate of 20% (many households pay 15%) is otherwise assessed. Tax rates on capital gains are similar, and both may be subject to an additional 3.8% for Unearned Income Medicare Contribution (UIMC) Tax for higher incomes.

- Restore flat tax of 15% for dividends and capital gains, while eliminating the 3.8% UIMC surtax of Obamacare on investment income.

The tax code has become too complex and costly to administer, resulting in insidious inefficiencies that reduce global competitiveness. Higher rates are needed to accommodate special interest concessions. The total cost of compliance and tax avoidance strategies across household and corporate sectors is staggering and growing. Various studies4 suggest 10-15% of taxes collected are required to administer tax compliance before tax aversion strategies from legitimate tax avoidance and honest misinterpretations to tax evasion that complexity affords. Simple is better: The voluminous tax code is too complicated, difficult to administer, expensive, and challenging to enforce.

- With less tax complexity and fewer deductions, an Alternative Minimum Tax (AMT) is not needed.

Taxable income should count retained income, not earnings given to charity or taxed by government agencies, including income and property taxes. These earnings aren’t available for the pursuit of happiness. High tax rate and property value states appear to benefit most from earnings deductions, but homeowners pay property taxes in every state. It is insidious to tax earnings paid to government agencies, including state income and property taxes.

- Income taxes should be assessed only on retained income with a top rate of 33%. Earnings to pay taxes or given to charity should be deductible.

Suggesting that paying taxes and giving charitable gifts are relatively equivalent exposes a failure to grasp conceptual differences and presents an ideological problem for democratic society. Neither civil society nor the market can fulfill the role of government. Donors decide how to support institutions, but they are not morally or constitutionally obligated to fund the public common good, as some government representatives suggest. Qualified charities such as endowments, foundations, and other non-profits are tax-exempt from donation and investment income, but Congress may reconsider this exemption. Policy debates regarding tax-emptions for university endowments recently increased, observing relatively low yearly spending. Some organizations have since responded by increasing spending rates.

- Charitable contribution deductibility should be retained, but taxing income from donations or investment gains of non-profits may be considered.

The individual tax code is already highly progressive, as suggested in the chart below, meaning that higher income tax brackets pay a higher tax rate. Higher income taxpayers have the resources and incentive to effectively shelter income by hiring smart accountants and lawyers. Simplifying the tax code will reduce the gap between statutory and effective rates. Effective rates reflect federal taxes, but not state income, real estate, or sales taxes. The notion that high income taxpayers don’t pay their fair share is simply not reflected in the chart below from 2014 tax returns.

Source: IRS

While businesses are able to deduct their cost of health care insurance and employee contributions from income, many small businesses leave employees to pay for individual insurance after tax. They can’t take advantage of group discounts or income deduction to pay for health insurance premiums. Expanding HSAs might help, but Obamacare needs to be replaced.

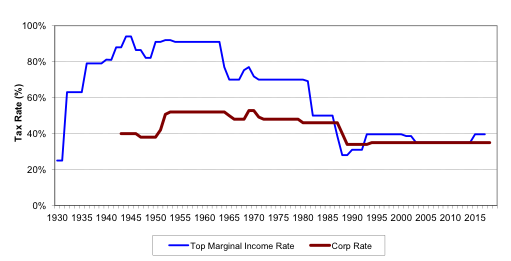

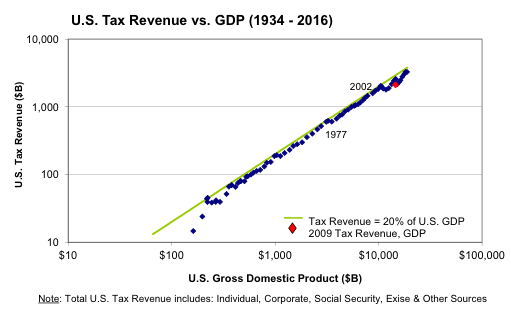

We have written about Hauser's Law. It is remarkable that total federal tax revenue has never exceeded 20% of GDP, despite wide swings in corporate and individual tax rates since 1934. Notable variations appear after the economy stumbles through recession, causing income to decline (ex: 1977, 2002, and 2009). Raising tax rates never boosted tax revenue, because raising taxes slows economic growth and earnings, which reduces growth in tax revenue. Similarly, if tax rates are cut and real growth increases, then tax revenue growth increases.

Source: Office of Management and Budget

The Simpson-Bowles National Commission on Fiscal Responsibility and Reform recognized the necessity for comprehensive fiscal reform in limiting spending to 20% (Hauser’s Law) of GDP in 2010. The Commission highlighted the need to increase growth in tax revenue with lower tax rates offset by eliminating deductions. In this way, they sought to close the gap between statutory and effective tax rates to increase fairness and consistency. Although commissioned by President Obama, its final recommendations were rejected by his Administration. Yet, many recommendations of the final report were incorporated into tax reform proposals.

- A balanced budget law should seek to banish fiscal deficits, with an exception for recessions. Nearly all states have balanced budget requirements.

If imitation is the sincerest form of flattery, supply-side policies were replicated by many other countries since 1990, including former Soviet-bloc countries. They adopted incentive-based free market capitalism and flat tax rates upon rejecting failed economic planning and government control of Socialism. Political corruption and tax evasion diminished, as individual opportunity expanded and social mobility increased. Government cannot tax and spend a country into prosperity--it never worked and never will. Free market economies encouraged innovation and entrepreneurialism that have proven to most efficiently allocate resources over generations. There is no need to experiment---we understand well the mechanism for potential growth.

There is little comfort in the fact that our fiscal condition is not as bad as Europe or Japan. Our concern is that fiscal deficits and debt burdens do matter and bond vigilantes eventually will demand higher yields for Treasuries and other G-7 government bonds. Fiscal vulnerability to interest rate fluctuations rises as debt exceeds 70% of GDP with exceptionally low rates increasing convexity. It costs over three times as much to pay off debt if 10-year Treasuries rose from 2.3% to a half century average of 6%. We think bond yields could double within three years, pushing our annual interest burden closer to $1 trillion (5% of our debt).

Retirement Savings and Tax Reform

We observed a transformative shift in retirement from reliance on defined benefit and pensions to Individual Retirement Accounts (IRA) and defined contribution (DC plans: 401(k), 403(b), 457) over the last 25 years. Increasing self-reliance has opened up a wide gap in retirement security. Those that sacrificed consumption to save for retirement compounded growth in their nest eggs, while others with insufficient savings increase risk of greater dependency and social unrest.

- Incentivize retirement savings and improve access to prudent investment advice are needed---DC and IRA contribution limits should increase.

Consideration of reducing tax deferred contribution limits or Rothification5 (tax contributions) of retirement plans is a terrible and misguided idea, but we believe is unlikely to be included in tax reform. Deferring taxes on contributions and investment gains has incentivized savings behavior, bolstering retirement security. Most households are much better off with their self-directed retirement accounts, but we still need to increase participation and savings rates to meet the retirement challenge of self-reliance. Retirement innovation in the 1980s led the way globally to reduce dependence on pension systems that didn’t adapt to extending life expectancy and explosive liability growth. Social Security and Medicare suffer from a similar glitch.

In the waning months of the last Administration, the Labor Department introduced new rules that provided states and municipalities authority to set-up alternative retirement plans, such as California’s Secure Choice. The plans were to be exempt from the Employee Retirement Income Security Act (ERISA). This rule was based on a false premise that small business employees haven’t saved because they don’t have access to company retirement plans. Of course, an act of Congress was required to afford Secure Choice or similar programs the tax-deferred advantage conveyed to ERISA qualified DC plans and IRAs.

Well, according to the Bureau of Labor Statistics, only 55% of employees have access to a 401(k)-type plan and a third of those don’t participate. With regard to IRAs (traditional and Roth), only 14.2% of eligible taxpayers are contributing to IRAs, and only 55% of IRA contributors are saving the maximum allowed. Thus, few of the individuals targeted to benefit from this rule take advantage of existing IRAs available to all.

Finally, there are at least four alternatives for small businesses to offer retirement if 401(k) plans appear too expensive, namely SEP-IRA, SIMPLE IRA, Solo 401(k), and SIMPLE 401(k). All of them provide higher tax-deferred contribution limits, and most retirement plan providers, such as Vanguard, Schwab, Fidelity, and TIAA, offer options at negligible cost to employers. Retirement providers typically offer basic financial advice for free to help investors be more successful—it’s just good business if balances appreciate faster. If employers were required to offer retirement plans, then they would likely opt-out because these services are far better for employees than Secure Choice, so there is no government option to gather sufficient assets.

If that wasn’t enough, initial contributions with no deferred tax advantage were to be held in low-yield Treasury notes for three years, incurring higher fees than a bank account. Then the funds might shift to a pre-determined portfolio of stocks and bonds. Why should government manage services that competing businesses can run more effectively and efficiently?

The DoL’s auto-enrollment retirement alternative was obviously a terribly naive initiative, which could have caused more harm, than benefit to participants. This misguided effort was redundant given existing tax-deferred IRAs and 401(k) alternatives with competitive low cost investment options available to everyone. Why didn’t DoL instead lobby to increase IRA contribution limits for individuals without access to company plans? Like health care, small business need not be burdened by another misguided mandate. Fortunately, Congress rolled back this rule, although too many states already wasted taxpayers’ money on this boondoggle.

Estate and Wealth Taxes

The 16th Amendment ratified in 1913 provided that Congress may determine and begin collecting taxes only on income. That precludes the federal government from naivety accumulated wealth or assets, which was discussed during the 2017 election, without regard to whether it was Constitutional. It raises an interesting question with regard to estate taxes. Although the estate tax hits less than .23% of households, it hopes to prevent the accumulation of dynastic wealth that would threaten democracy. Visibility of high profile billionaires might suggest a concentration of dynastic wealth, but a brief look at Americans in the Forbes 500 suggests few on the list represent family dynasties.

There are two issues that arise in Constitutionality of the estate tax that don’t apply to a wealth tax. First of all, estate taxes were first implemented in 1913, before the 16th Amendment was adopted. Furthermore, the estate tax is not considered a recurring "direct" tax in the constitutional sense, but a duty or excise tax on the transfer of an estate, rather than a literal tax on the property itself. An analogy is a customs duty assessed on the imported property value, thus estate taxes must be an "event" tax that is imposed on your estate.

Warren Buffett penned a WSJ op-ed in 2012 suggesting that his 2010 effective individual tax rate was aberrantly 17.4%. Since his annual salary was just $100,000, most of his individual income comes from passive income, particularly Berkshire dividends taxed at 15%. Mr. Buffett also owned 31% of Berkshire Hathaway, whose federal corporate tax rate was 29% in 2010. He may characterize himself as a simple man, but his tax liability was dominated by his corporate holdings. His individual tax rate was misleading. His combined corporate tax rate was much higher than his Secretary paid. Mr. Buffett said, "Dynastic wealth, the enemy of a meritocracy, is on the rise. Equality of opportunity has been on the decline…A progressive and meaningful estate tax is needed to curb the movement of a democracy toward plutocracy." The idea that Mr. Buffett isn’t paying his fair share is disingenuous, and not as simple as some suggest in supporting a Buffett rule to justify income redistribution.

There is a desire to eliminate the estate tax, but many estates do have significant long-term capital gains in property and financial assets. This is particularly true as the next generation transfers wealth to their heirs. While a wealth tax is unconstitutional, there is a basis for taxing capital gains rather than wealth at transfer.

- Estate taxes should focus on settling-up unrealized capital gains at 15% rate vs. redistributing wealth.

A long-term capital gains rate of 15% seems reasonable. Inherited retirement accounts may be treated similarly. Inherited IRA or 401(k) accounts likely will have a low cost basis, but then after tax, the cost basis should be reset to fair value. These assets may include tax deferred earnings, but there is no record to separate investment gains from contributed earnings, but 15% tax is more equitable than 0% or 40%.

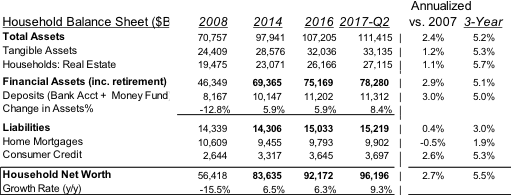

Source: Federal Reserve, Flow of Funds (Table B.101)

It is worth considering our national household balance sheet. Although the U.S. government is deeply in debt, household net worth has increased significantly since 2009, and exceeds $96.2 Trillion. Financial assets total $78.3 Trillion, including $11.2 Trillion in cash (or equivalent) earning less than 1%. Financial holdings increased 69% since 2008, including retirement assets. Financial assets play a greater role in estate planning and source of estate taxes. Losing the family farm to the taxman is just not that relevant anymore.

Tax Reform in the Bull’s Eye

Certain legislators will have greater influence over tax reform legislation. The Origination Clause requires: All Bills for raising Revenue shall originate in the House of Representatives. So, the House will draft and manage fiscal budget legislation, although the Senate has an opportunity to amend it. House Speaker Paul Ryan and Ways and Means Chairman Kevin Brady, along with Senate Finance Chairman Orrin Hatch will manage drafting tax reform. President Trump campaigned on his vision for tax reform, and the Executive Branch has published tax reform principles. While the President, as persuader-in-chief, plays an important role whipping votes, he is unlikely to veto or amend tax reform.

The reconciliation budget process limits any increase in the scored fiscal deficit, although many assume it requires tax revenue neutral legislation---it does not. Use of more realistic dynamic scoring to quantify fiscal effectiveness will increase tax reform flexibility, albeit relying on material assumptions. We do have greater historical precedents and better financial models than a decade ago that indicate economic effects of tax law changes. If Congress also can reduce spending, it will provide greater flexibility in tax reform.

Administrative, compliance, and enforcement costs are about 10-15% of total tax revenue. Our progressive tax code requires the top 25% to pay 87% of individual tax revenue, while 50% of households pay trivial taxes (<5%) or receive tax credits in excess of liabilities. In 1981, the top 25% paid just under 50% of income taxes—so, as tax rates fell, the richest households now pay a much larger share of individual taxes. Tax revenues are more cyclical and volatile as a result.

Source: IRS

Over 70,000 pages of tax code complexity exposes more ways for tax avoidance that interfere with the efficient allocation of capital. Tax policy complexity may further be compounded by other objectives to promote specific behavior or social policy outcomes. Wide differences that exist between effective tax rates and statutory tax rates need to narrow, but the challenge for reform remains vested interests and the status quo.

The U.S. has maintained the highest combined (federal and state) corporate tax rate of 39.2%6, while other countries slashed tax rates. Small businesses tend to benefit less from decades of specific exemptions. Larger companies leverage scale for tax avoidance and deferral strategies, as with regulations that limits competition. General Electric paid an average tax rate of 2.3% over the decade ending 2010, including paying no taxes in 2002 or 2008-2010. Tax code and regulatory complexity limit free market competition and raise barriers to entry that weaken competitiveness.

Debate over tax policy is polarized over fairness issues between balancing liberty, free market competition, and rule of law versus social justice of income inequality. Consistent with the primary functions listed earlier, limited government should seek to maintain free and competitive markets, yet protect victims of misfortune or limited opportunity. Intervention, however well-intended, is too often misguided, overreaches, and undermines rights or liberty. Government control never created wealth, only destroyed, limited or redistributed it. Raising taxes never resolved fiscal deficits because higher taxes undermine competitiveness, reduce incentives, and increase inflation. Sharing the wealth should be a charitable response, not a government imposed requirement. Regulating the economy through the tax code often has adverse consequences.

However, there is no question that lower tax rates have proven to enhance potential growth, driving higher earnings and increased tax revenues. Changes in tax rates are not a zero-sum game given their impact on economic efficiency and growth. Higher tax rates never increased tax revenue or reduced fiscal deficits, but did slow economic and real income growth as inflation increased. Damage caused by Roosevelt raising corporate and individual taxes from 1934-1937 to pay for Depression-era programs is well chronicled. Yet, lowering tax rates with spending reform worked marvellously in the 1960s, initiated under Kennedy, and 1980s under Reagan. Spending reform is also needed with entitlement spending jumping to 13%, including health insurance mandates of Obamacare.

Source: OMB and BEA compiled by Deutsche Bank Research

If lower tax rates spur growth, why resist the better path forward that has proven to raise productivity and prosperity? Why insist that those shouldering the greatest burden must pay even more tax when there is no benefit raising tax rates? Simplifying tax filing and administration also should increase net tax revenue by reducing costs, while limiting special interest tax-breaks. Greater efficiency of simplifying tax collection benefits both taxpayers and government.

Concluding Thoughts

“We shall all consider ourselves unauthorized to saddle posterity with our debts, and morally bound to pay them ourselves.” ---Thomas Jefferson

Tax reform is coming into focus as politicians suggest they seek revenue neutral tax reform. Investors should understand how various tax reform elements impact potential economic growth and earnings expectations, as well as productivity and job growth. Better wage growth with an expanding workforce at lower tax rates yields increased net income and tax revenue. Improving potential growth to drive household and corporate earnings is the primary objective of tax reform. Simplification should reduce administrative, compliance, and enforcement costs. We believe a broader focus on fiscal reform increases policy options and effectiveness toward reform objectives.

Tax and regulatory reforms have repeatedly bolstered growth in tax revenues. Lower tax rates and tax code simplification will increase potential growth and earnings that drive greater tax revenue. Incentivizing foreign earnings repatriation with a 10-15% tax rate is a compelling way to increase research and domestic investment spending, while unshackling potential tax revenue. Economic benefits from tax reform are most effective when policy changes are permanent. While transition periods may be needed, we would caution against tax holidays or sunset provisions that can have unintended consequences and are difficult to extend. In the race for global competitive advantage, tax and regulatory policy changes have an constructive impact.

Our tax code is unfair in various dimensions because similarly situated taxpayers are not treated equally, such as within income brackets or between competing businesses across sectors. Targeted tax credits and income deductions leveraged for political advantage have increased complexity and reduced competition by targeting specific constituencies for exceptions. Once we simplify adjusted income by eliminating income deductions and credits, tax rates can align with current effective rates yielding a 33% top rate vs. a flat tax baseline of 14%. Other brackets can collapse to 25% and 12%, consistent with a recent House proposal.

Divergence between statutory and effective tax rates indicate the degree of tax policy unfairness, but those who benefit most exploiting tax exceptions won’t pay more just by raising tax rates. Simplifying tax reform can improve fairness of tax assessments. Broad-based tax reform also eliminates extreme loopholes that the Alternative Minimum Tax addresses, thus it can be retired. Government is accountable to maintain free and competitive markets, but this goal has been undermined by misguided or preferential tax laws and regulatory rules. Special interest and public policy tax exemptions foster capital allocation inefficiencies. Tax and fiscal reform principles articulated apply similarly for state and local levels.

America needs a credible fiscal plan to slow growth in spending, while increasing potential GDP and earnings growth with tax reform to unleash America’s full potential. The European sovereign debt crisis highlighted consequences of ignoring fiscal deficits and unsustainable growth in government programs. Risk of similar acrimony and social unrest that unfolded across Europe show how quickly public sentiment can make economic challenges politically more difficult.

Economic impact of policy changes due to shifts in the balance-of-power can lag for years. Changes in sentiment may have shorter-term halo effects, but regulatory changes were significant and economic effects are visible already. While innovation and technology transformed the world around us, these forces are also changing how government functions. Congressional leadership must adapt to an Executive Branch that works many issues in parallel.

Policymakers intuitively should seek out optimal decisions that most benefit a majority of their voters, thus taxpayers---for the common good of society. Our perspectives seek to identify the issues and decisions that increase fiscal efficiency---tax reform seeks to increase tax revenue, while spending reform seeks to minimize the cost of government. Fiscal reform can drive fiscal deficits into surpluses that begin to reduce our debt. Economic forecasting is hard and prone to error, but the final step is to translate policy changes into impact on economic variables and earnings.

Improving economic conditions and equity rally both indicated improving business and investor confidence following the election. Importance of regulatory reform at the agency level was overlooked by many, but material to improving confidence in likely higher potential growth. Now we must wait for tax reform before further upgrading our economic and earnings outlook. Any resemblance to the reform principles we outlined should increase real potential growth by 0.5-0.7% and add 1-2% to long-term U.S. earnings growth. Further improvement in the economy and equity returns hinge on scope and likelihood of tax reform.

Strategic Insights This publication is for general information only and is not intended to provide specific advice to any individual. Some information provided herein was obtained from third party sources deemed to be reliable. We make no representations or warranties with respect to the timeliness, accuracy, or completeness of this publication, and bear no liability for any loss arising from its use. All forward looking information and forecasts contained in this publication, unless otherwise noted, are the opinion of this author, and future market movements may differ from expectations. Index performance or any index related data is provided for illustrative purposes only and is not indicative of the performance of any portfolio. Any performance shown herein is no guarantee of future results. Investment returns will fluctuate, and the value of holdings may be worth more or less than original cost. © Strategic Frontier Management (www.StrategicCAPM.com). 2017. All rights reserved.

1 Dividend and capital gains, plus individual income tax rates increased, as well as Obamacare taxes added

2 Dodd-Frank financial reform, Basel II/III, MiFID II, and Affordable Care Act, plus agency rule making (EPA, Transportation, Energy)

3 Payroll taxes are split between you and your employer, so employees only observe half this amount, yet combined is a cost of being employed. After accumulating over a lifetime, why should Social Security ever be subject to means testing?

4 “The Economic Burden Caused by Tax Code Complexity”, by Arthur Laffer et al, estimated that administrative, filing, and compliance costs have increased since 1986 tax reform, exceeding $431 billion in 2010 or 30% of income tax revenues.

5 Rothification may provide near-term tax revenue by taxing contributions, but foregoes greater deferred tax revenues in the long run when IRAs are cashed out and income taxes are paid on both contributions and investment earnings.

6 Federal corporate tax rate of 35%, plus 4.2% state average. Japan recently cut its corporate tax rate from 39.5% to 38%.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits