When President Donald Trump came into office, the financial markets were buoyed by the prospect of tax cuts and other business-friendly measures, and they expressed their high hopes in the form of higher share prices. While progress in many parts of Mr Trump’s agenda has been slow, his administration’s recent announcement of a “framework” for tax reform represents a potential step forward on a key plank of “Trumponomics”. There is clearly a renewed spirit among Republicans to get tax reform passed – particularly before mid-term Congressional elections in November 2018 – but there are several hurdles that must be crossed before making it to the finish line.

Corporate tax provisions

- Reduces the corporate tax rate to 20% from 35%

- Imposes a tax rate of 25% on income of pass-through businesses – sole proprietorships, partnerships and “S corporations”

- Eliminates the corporate alternative-minimum tax

- Immediate “expensing” of new equipment investment (ie, deducting the full cost of new investments) after 27 September 2017 for at least five years

- Partially limits the deduction for net interest expenses of “C corporations”, but does not specify the partial limitations

- Shifts to a territorial system of taxation of global American companies where only domestic income is taxed; this involves exempting foreign profits when repatriated to the US. Imposes a one-time tax on repatriated foreign earnings accumulated under the old system.

Individual tax provisions

- Doubles the standard deduction to $24,000 for married taxpayers and $12,000 for individuals; this is effectively a 0% tax rate for these filers

- Reduces the number of tax brackets to three (or four) from seven – 12%, 25%, 35%. The plan includes no details on income ranges for proposed tax brackets, and it may impose an additional top rate for highest-income taxpayers.

- Increases the Child Tax Credit and makes it available to more middle-income households; also makes the first $1,000 refundable

- Repeals the individual alternative-minimum tax

- Keeps the mortgage-interest and charitable-contribution deductions but eliminates many other itemized deductions

- Repeals the deductibility of state and local taxes

- Removes the estate tax

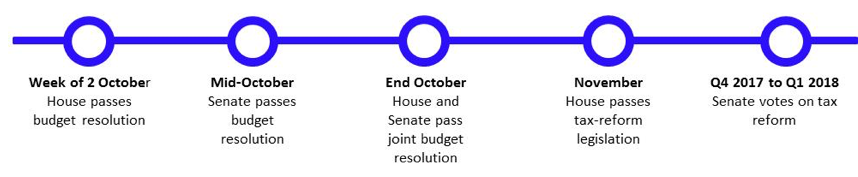

Timeline for reform

To move their new tax-reform proposal forward, Republicans in the US Congress are using the same special procedure that they used for health-care reform: budget reconciliation.

Under this approach, the Senate will need just 50 votes instead of the traditional 60-vote requirement. With 52 Republicans in the Senate, this will be a complicated process that will take negotiation on almost all fronts. As Senate Finance Chairman Orrin Hatch said: “It’s much harder than health care.”

The estimated timeline for this process is as follows:

Probability of passage

We estimate that as it stands today, the probability of tax reform occurring remains around 30%. But if President Trump and the Republicans meet with success as they proceed through the timeline outlined above, the probability of passage will rise. If the new budget resolution is passed, we believe there is a greater than 50% chance of tax reform by the first quarter of 2018.

Issues with the proposal

According to the Committee for a Responsible Federal Budget, the estimated loss in tax revenue from these reforms is $5.8 trillion over a 10-year period. However, there are offsets to these revenue losses, including eliminating state and local tax deductions. With these offsets, net tax cut costs are estimated at $2.2 trillion (about 1.5% of US gross domestic product).

Another key area of contention may arise from the repeal of the deductibility of state and local taxes. The largest state and local deductions are taken primarily in counties that are strongholds of the Democratic Party, creating further tension across party lines.

Investment implications

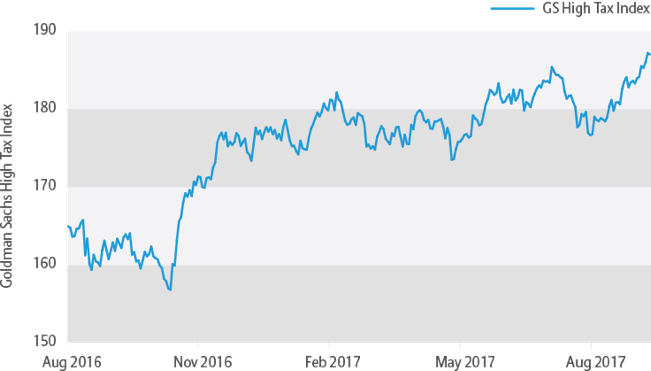

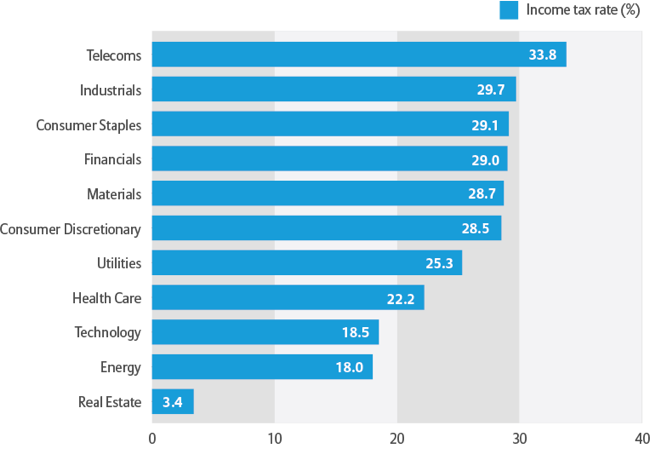

Assuming the new tax-reform proposal passes, sectors with the highest current tax rates are likely to benefit from the reduction of the corporate tax rate to 20%. The market has already priced in some of the benefit for the top 50 names (see Figure 1). The top beneficiaries would include telecoms, industrials and consumer staples (see Figure 2).

Figure 1: Markets Priced In Tax Reform after the Announcement

Price for basket of 50 stocks with highest tax rates in the S&P 500 Index

Source: Bloomberg as at 28 September 2017.

Figure 2: Telecoms and Industrials Could Benefit Most from Tax Reform

Corporate income-tax rates for 11 GICS sectors

Source: Bloomberg as at 28 September 2017.

In addition, from a style perspective, value stocks are a larger beneficiary of lower tax rates and have a lower portion of imported inputs when compared to growth stocks. Small and mid caps would benefit relative to large-cap stocks due to their higher domestic exposure.

An estimated $250 billion would return to the US in the form of repatriation dollars, and the sectors that would benefit most from this legislation include technology, health care and industrials. Based on the 2004 repatriation initiative, companies in these sectors would likely spend half the dollars on share buybacks, and spend the other half investing in growth programmes – such as research and development, capital expenditures, and mergers and acquisitions.

Repatriation could also potentially create pressure on US Treasuries, as foreign money, in the form of US Treasuries abroad, is brought back and sold. In this scenario, Treasury yields would be further pressured upwards. We believe this could also be a tailwind for the US dollar, and it could further compress US corporate bond spreads. Since the announcement of tax reform, we have already seen rising Treasury yields and a rising US dollar (see Figure 3) and increased spread compression.

Figure 3: US Dollar and Treasury Yields Moved Higher Post-Announcement

US dollar index and 10-year US Treasury yields, September 2016-September 2017

Source: Bloomberg as at 28 September 2017.

Impact on US consumers

While the windfall from tax cuts would appear to be generally supportive of the US consumer, there is a case to be made that the wealthiest Americans would benefit more than the average middle-class American family. Eliminating taxes such as the estate tax and the alternative minimum tax disproportionately creates windfalls for the richest Americans. Nonetheless, we believe the US consumer, who makes up more than 70% of US GDP, will benefit from increased spending power if tax reform passes.

Follow Us on Twitter

For more investment insights and market perspectives from our global research network, follow @AllianzGI_US on Twitter or visit us.allianzgi.com.

Important Information

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, us.allianzgi.com, 1 800 926 4456.

279352