1

1

Note: This is the first in a three-part series of blog posts on principles of the low-return imperative

My way or the highway, the old saying goes.

In the institutional investment community, my way includes the highway might be more appropriate.

In certain cases, up to 17% of the total assets in an institutional investor’s portfolio are invested in infrastructure today, according to data from the Ontario Municipal Employees Retirement System (OMERS) 2016 Annual Report.2

What’s behind all this? What might institutional investors have uncovered that could be helpful in potentially generating an additional source of market returns—the first principle of our low-return imperative?

The low-return imperative: A quick review

It's no secret that we believe future market returns are likely to be low—and many analysts agree with us.3 In fact, we view low returns as the single greatest challenge facing investors today. To combat this, we've taken to beating the drum on what we define as the low-return imperative—the idea that when expected future market returns are likely to be lower than the required rate of return, we believe an investor cannot afford to ignore any investment strategy that may offer incremental return, take on risks they do not expect to get paid for or disregard implementation efficiency.

This is where infrastructure comes into play. We see it as a shining example of the low-return imperative’s first principle: it’s an asset class that cannot be ignored in the search for additional returns. To understand why, it’s helpful to first take a step back and define what it means.

What is infrastructure?

Infrastructure is a fundamental building block to the functioning of modern society and can include energy, transportation and communication networks and systems. Within the broad infrastructure investment universe, there exists what we call pure play infrastructure. Pure play infrastructure assets typically provide essential services, operate in monopoly-like competitive positions and enjoy sustainable cash flows producing reliable income streams. By way of example, we consider an airport to be a pure play infrastructure asset, as opposed to an airline. Another example would be a toll road, as opposed to a construction company that builds the toll road.

Today, infrastructure is recognized by the institutional investment community as a stand-alone asset class. To wit, many pension plans around the world have been attracted to the infrastructure asset class since the early 1990s. But why?

The case for infrastructure investment

We believe that the reasons for infrastructure to be included in a multi-asset portfolio are threefold.

The first reason is access to a global growth opportunity. Upgrading the world’s infrastructure will be a dominant theme over the next 20 years. In fact, it’s estimated that a staggering $49 trillion will be spent on infrastructure by the year 2030.4 In addition, given the fiscally challenged positions of many governments and municipalities, it’s likely that there will increasingly be a reliance on private capital to finance infrastructure spending needs.

In addition, U.S. President Donald Trump has outlined a plan to generate $1 trillion in infrastructure spending through incentives for private investors to build and modernize American infrastructure. If this comes to fruition, this policy initiative, over time, will likely benefit the listed infrastructure asset class by creating more opportunities for the private sector to build, own and operate critical infrastructure assets.

It’s also important to note this trend has already been developing globally over the last 10-15 years. Case-in-point: The market capitalization within the broad universe of publicly traded infrastructure companies was approximately $400 billion in 2005.5 Today, that same universe has a market cap of between $2 and $3 trillion.

This growth in the investable opportunity set has, and will likely continue to be, driven by the following factors:

- Privatization: Where governments sell ownership stakes to private enterprise. Examples of infrastructure that have been privatized include airports, toll roads, seaports and electricity transmission and distribution assets.

- Organic growth: Where the owners of infrastructure assets expand and grow their existing businesses. Examples include energy infrastructure companies expanding pipelines and toll road operators extending highways to facilitate increased user demand.

Given the massive scope of infrastructure financing requirements globally, infrastructure investment opportunities will likely continue to expand to meet demand for developing and modernizing critical infrastructure.

The second reason to consider investing in infrastructure is the enhanced yield potential relative to equities and bonds. Infrastructure companies historically provide a relatively high dividend yield, but importantly, they also exhibit predictable and resilient cash flows. The resiliency of cash flows attached to pure play infrastructure assets can be attributed to the following: essential nature of the service provided, structural growth, high barriers to entry and strong pricing power.

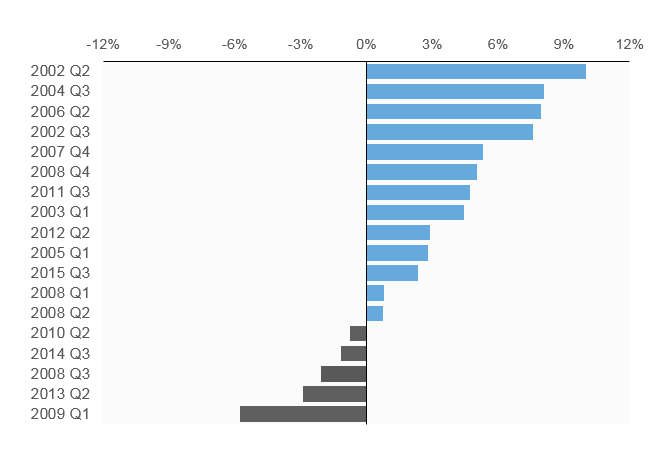

The third reason is portfolio diversification and downside protection. As a defensive alternative to equities, exposure to infrastructure can help manage total portfolio volatility, given its forecasted low correlations to stocks, bonds and real estate. Since 2001, infrastructure securities have outperformed global equities during 13 of the 18 quarters where the Russell Global Index experienced a negative quarterly return.[6] On average, the S&P Global Infrastructure Index has outperformed global equities by 2.8% per quarter during negative quarters. And dollar for dollar, we believe downside protection may be worth more than upside growth.

Chart: Outperformance of S&P Global Infrastructure Index vs. Russell Global Index during quarters of negative equity market performance

6 Source: S&P Global Infrastructure Index, Russell Global Index, as of June 30, 2017

Maximizing the benefits of infrastructure

We believe a well-defined and repeatable investment process is required to create an infrastructure portfolio to help achieve desired investment outcomes, and to deliver on the infrastructure investment value proposition. The following three considerations may be helpful to consider when investing in the infrastructure asset class:

Pure play: The unique characteristics of pure play infrastructure are what ultimately drive the portfolio diversification and enhanced yield (or income) associated with the infrastructure asset class. Caution is warranted when expanding the investable universe beyond pure play infrastructure companies (i.e. construction, airlines, telecommunications carriers), as this may expose investors to industries and businesses that are more cyclical in nature and whose revenues or earnings are much more dependent on the business cycle. In times of recession or economic downturns, these companies are more likely to suffer, therefore mitigating the portfolio benefits of the infrastructure asset class.

Global: Infrastructure is a global asset class, with an opportunity set potentially as large as $49 trillion. Over half of the world’s infrastructure investment needs are outside of North America.7 By constraining portfolios to North American infrastructure (which tend to be biased towards the utilities and energy sectors), individuals may be forgoing investment opportunities in key areas such as toll roads, airports, seaports and cell towers.

Actively managed multi-manager portfolio: This may help mitigate single manager risk, in addition to providing access to the rich source of potential active management opportunities that infrastructure allows, including balanced sector exposures, alpha generation potential and prudent risk management. While it is possible to gain passive exposure to infrastructure, there may be significant opportunity costs, including lower returns and greater risks, attached to forgoing active management in favor of passive implementation approaches. In contrast, actively managed portfolios tend to have more balanced sector exposures, emphasize pure play infrastructure investments and may be well positioned to exploit market inefficiencies such as business fundamentals, relative valuation and merger and acquisition activity. Active managers in this sector can also provide access to an expanded investment universe through out-of-benchmark exposures.

In short, we believe that infrastructure exposure can be a key part of a multi-asset portfolio. Infrastructure can provide an opportunity to help achieve desired investment outcomes while effectively managing overall risk at the total portfolio level. In today’s world of low returns, the game is on to unearth additional sources of return. Infrastructure may be worth the dig.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

Investing involves risk and principal loss is possible.

Past performance does not guarantee future performance.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

This material is not an offer, solicitation or recommendation to purchase any security. Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Please remember that all investments carry some level of risk. Although steps can be taken to help reduce risk it cannot be completely removed. They do no not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Investments that are allocated across multiple types of securities may be exposed to a variety of risks based on the asset classes, investment styles, market sectors, and size of companies preferred by the investment managers. Investors should consider how the combined risks impact their total investment portfolio and understand that different risks can lead to varying financial consequences, including loss of principal. Please see a prospectus for further details.

Indexes are unmanaged and cannot be invested in directly.

The S&P Global Infrastructure Index provides liquid and tradable exposure to 75 companies from around the world that represent the listed infrastructure universe. To create diversified exposure across the global listed infrastructure market, the index has balanced weights across three distinct infrastructure clusters: Utilities, Transportation, and Energy.

The Russell Global Index measures the performance of the global equity market based on all investable equity securities. The index includes approximately 10,000 securities in 63 countries and covers 98% of the investable global market. All securities in the Russell Global Index are classified according to size, region, country, and sector, as a result the Index can be segmented into more than 300 distinct benchmarks.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments' management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

Copyright © Russell Investments Group LLC 2017. All rights reserved.

UNI-11137

1 Source: McKinsey Global Institute June 2016 “Bridging global infrastructure gaps”. The estimate of total demand is lower than the $57 trillion projection in previous research. It has been adjusted based on a shorter projection period of 15 years (versus 18 years), water numbers have been reduced by 40%, base

year prices have been revised from 2010 to 2015 and GDP growth forecasts have been revised downwards.

2 Source: www.omers.com

3 Source: Federal Reserve Bank of Philadelphia, Survey of Professional Forecasters and Russell Investments. Data as of January, 2017.

4 Source: McKinsey Global Institute, June 2016. “Bridging global infrastructure gaps”.

5 Source: S&P Global Infrastructure Index

6 Source: S&P Global Infrastructure Index, Russell Global Index, as of June 30, 2017

7 Source: Global Infrastructure Outlook, July 2017 https://outlook.gihub.org/