Central Bank’s 2% Inflation Fetish

Throughout history banks have been at the epicenter of every financial crisis. That notoriety of failure led to the formation of Central Banks. In the wake of the 2008 financial crisis, global banks have repaired and strengthened their balance sheets, especially in the U.S. The majority of European banks have shored up their balance sheets but there are some banks where there is room for further improvement, especially in Italy. While the global financial system is more financially sound, Chinese banks are likely to experience their day of reckoning during the next global downturn.

The Federal Reserve was established on December 23, 1913 after Congress passed ‘The Federal Reserve Act’ to provide the nation with a safer, more flexible, and more stable monetary and financial system. The Federal Reserve Act was the response to a number of financial crises in the preceding 20 years that resulted in bank runs, bank failures, and economic contractions. The worst economic crisis began in 1893 and lasted until 1897 and was considered a Depression given its length and the depth of the contraction in the economy. The Panic of 1901 was the first Crash in the stock market and was triggered by a battle between E.H. Harriman, who owned the Union Pacific Railroad, and a group financed by J.P Morgan over the control of the Northern Pacific railroad. The Panic of 1907 began in mid October and led to a 50% decline in the New York Stock Exchange index within 3 weeks. A run on New York banks spread to banks throughout the country and ended when J.P. Morgan pledged his personal fortune, along with other prominent bankers, to shore up the banking system and provide liquidity to the financial system.

In the lead up to the Great Depression, the Federal Reserve expanded the money supply by 61% from 1921 to 1929. After the economy sunk into recession in 1930, the Federal Reserve allowed the money supply to contract by more than 30%, which led to bank runs and failures. As liquidity dried up, commodity prices plunged, the value of farms fell, and bank farm auctions soared. In an effort to stiff banks, neighbors would enter low bids for the property being auctioned so they could return the property to the family being foreclosed on. These auctions became known as Penny Auctions. Congress compounded the Fed’s monetary miscue by passing the Smoot-Hawley Tariff Act in June 1930 which added high tariffs to 20,000 imported products. World trade plummeted by 40% within 18 months of the passage of the Tariff Act, as our trading partners responded with their own higher tariffs. In 1932, Hoover pushed Congress to pass an increase in the top personal tax rate from 25% to 63% and the lowest tax rate to 4.0% from 1.1%. The Great Depression was the result of a number of policy mistakes.

In the run up to the Great Recession in 2008, the Federal Reserve maintained negative interest rates from 2001 through 2004, failed to supervise large banks after they increased their leverage from 12 to 1 in 2004 to 30 to 1 in 2007, allowed no-doc and liar loans to become the norm in 2005, 2006, and 2007, and publicly expressed confidence in May 2007 that the sub-prime problem would be contained. Congress encouraged the Housing of Urban Development (HUD) to push Fannie Mae and Freddie Mac to make mortgage loans to less qualified buyers so lower income families could participate in the American Dream. The 2004 HUD regulations established a set of sub-goals tied to the total number of mortgages purchased by each GSE. In 2007, both Fannie and Freddie were to allocate 47 percent of their respective purchase activity to low and moderate income housing, 18 percent to so-called special affordable housing, and 33 percent to so-called underserved areas. Mortgage originating firms like Countrywide Financial and large banks, like Pigs at the trough, created an assembly line of low quality mortgage pools rating firms Moody’s, S&P, and Fitch rubber stamped with a AAA blessing. This activity took place in plain sight of everyone, including the Federal Reserve which had a ring side seat.

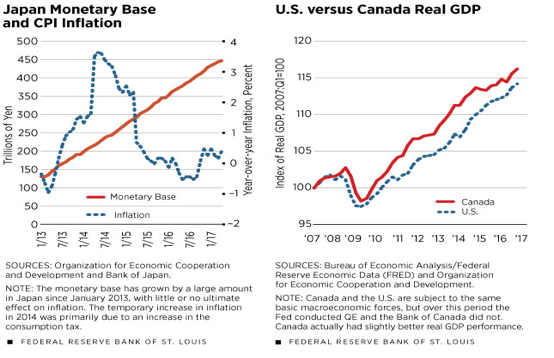

Financial crises are always preceded by excesses that appear reasonable and justifiable. The intervention by the Federal Reserve and its launch of the first Quantitative Easing (QE) program in 2008 clearly prevented another Great Depression. Maintaining QE for another six years so QE could boost asset values without discernible benefit in the real economy, as a number of Federal Reserve District bank analysis’s has indicated, is why the number of negative unintended consequences have increased. An analysis by Stephenson Williamson, an economist at the Federal Reserve of St. Louis, recently concluded “With respect to QE, there are good reasons to be skeptical that it works as advertised, and some economists have made a good case that QE is actually detrimental." In theory, QE is expected to boost economic growth and inflation. Williamson compared the U.S. and Japan which utilized QE to Canada, which only used low interest rates rather QE and low rates as was done in the U.S. and Japan. As noted by Williamson, "If QE were effective in stimulating aggregate economic activity, we should see a positive difference in economic performance in the U.S. relative to Canada since the financial crisis. There is little difference from 2007 to the fourth quarter of 2016 in real GDP performance in the two countries. Indeed, relative to the first quarter of 2007, real GDP in Canada in the fourth quarter of 2016 was 2 percent higher than real GDP in the U.S., reflecting higher cumulative growth, in spite of supposedly less accommodative monetary policy.”

The Bank of Japan has conducted the most aggressive QE program of any central bank but inflation has not responded as the accepted QE theory proposed. As Williamson concluded, "Thus, in these two natural experiments, there appears to be no evidence that QE works either to increase inflation, if we look at the Japanese case or to increase real GDP, if we compare Canada with the U.S."

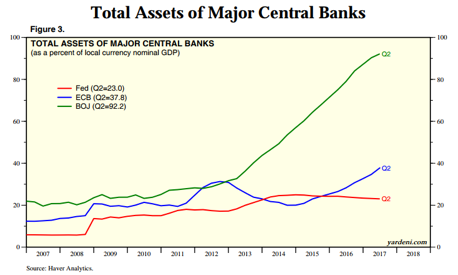

The Bank of England followed the Federal Reserve’s lead and launched the first of its three QE programs on March 5, 2009, followed by other Central Banks. Due to various political constraints, the European Central Bank didn’t launch its QE program until March 2015 but has been very aggressive in expanding its balance sheet. From December 2007 to May 2017, the Fed’s total assets increased from $882 billion to $4.473 trillion—a fivefold increase. Total Fed assets increased from 6.0% of U.S. GDP in the fourth quarter of 2007 to 23.0% of GDP in the second quarter of 2017. In June 2017 the Bank of Japan had a balance sheet that was 92.2% of GDP, Switzerland’s was 115% of GDP, the Swedish Riksbank’s was 19% of GDP, the Bank of England’s was 24% of GDP, and the European Central Bank’s was 37.8% of GDP.

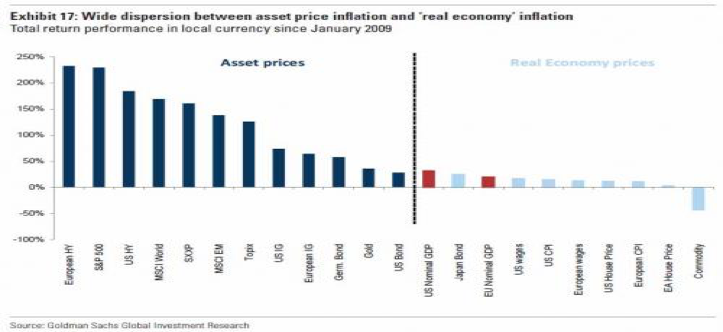

The disparity between the real economy and financial assets since January 2009 should be an embarrassment to central bankers and further proof that maintaining extraordinary monetary accommodation will not lead to faster economic growth or inflation. The definition of insanity is doing the same thing over and over again and expecting a different result. Janet Yellen deserves some credit for publically acknowledging that the failure of inflation to increase as economic theory proposes is a mystery.

The Federal Reserve didn’t formally adopt a 2% inflation target until January 2012. At that time, deflation concerns were rampant and the Fed believed that publically stating it would maintain an extraordinary accommodative monetary policy until inflation rose to 2% was necessary to allay deflation fears. Following its meeting in January 2012, the FOMC issued a statement regarding its longer-run goals and monetary policy strategy. “The FOMC noted in its statement that the Committee judges that inflation at the rate of 2 percent (as measured by the annual change in the price index for personal consumption expenditures, or PCE) is most consistent over the longer run with the Federal Reserve's statutory mandate. Communicating this inflation goal clearly helps keep longer-term inflation expectations firmly anchored, thereby fostering price stability and moderate long-term interest rates and enhancing the FOMC's ability to promote maximum employment.”

I think the Fed was correct in its assessment in 2012 but less so after 2014 when it became clear the U.S. and global economy was on a firmer footing. With the ECB enthusiastically joining the QE ranks in March 2015 and the BOJ’s QE program still on steroids, there are a growing number of imbalances that reflect excessive risk taking. The gap between the real economy and asset valuations is widening not just in the U.S. but around the world. Here are a few examples.

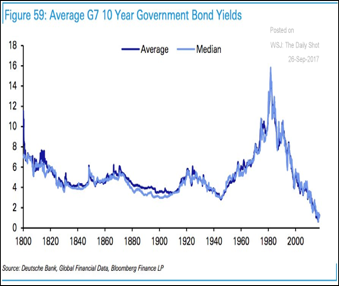

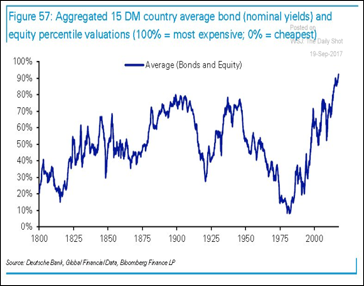

Bond yields in the seven largest developed G7 countries are the lowest since 1800.The valuation of bonds and equities in the 15 largest developed countries is the most expensive since 1800.

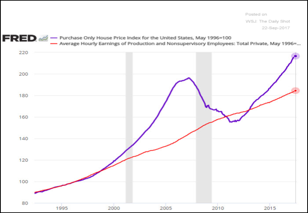

Home prices in the U.S. have just surpassed the peak in 2006. However, income growth has not kept pace with the increase in home values. The gap between the average hourly earnings of non supervisory workers and home prices is almost as wide as it was in 2006 during the housing bubble. As noted in the June issue of Macro Tides, home prices have been pushed higher by a lack of inventory in most markets. Real estate research firm Trulia looked at the market value of each home in the country and compared it to its pre-housing crash peak. Trulia’s study found that only 34.1% of homes nationally had surpassed their previous highs. The difference between Trulia’s study and the S&P/Case-Shiller Indexes is that they give more weight to expensive homes than the individual home pricing in Trulia’s study. This suggests the inventory of homes for sale will remain low as homeowners around the country wait for the price of their home to recover. The good news in this information is that the current bubble in home prices is concentrated in a smaller number of large cities, rather than more broadly across the country. Even in the markets that have exceeded their 2006 peak by a comfortable margin, some homeowners may be reluctant to put their home on the market since it would mean giving up a once in a generation low mortgage rate, especially if they refinanced in 2012.

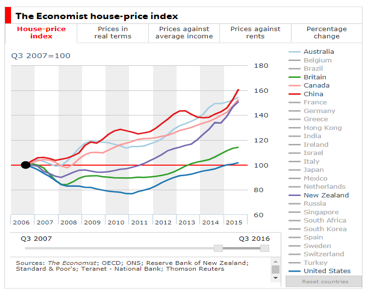

While the current value in home prices in the U.S. is not as threatening as it was in 2006, the same cannot be said for many cities around the world. Compared to the U.S., home prices are in the stratosphere in Canada, China, Hong Kong, New Zealand, and Australia, where they are up more than 150% above their peak in 2006. In Sydney Australia the average price of a home is 11 times media income. At the peak of the U.S. housing bubble in 2006, the ratio of the median home price to median income was 4.6 to 1.

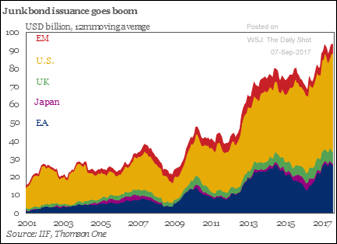

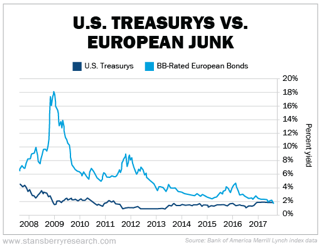

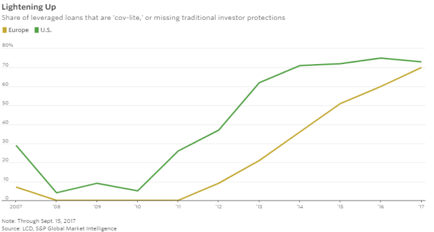

The reach for yield has become a global phenomenon as investors have bought an all-time record amount of junk bonds. The almost out of control demand for yield has pushed the yield on European junk bonds down so much they irrationally provide the same yield as U.S Treasury bonds. Covenant-lite loans offer less protection to institutional investors than traditionally structured credits. At the end of July, covenant-lite loans comprised 72.7% of the $943 billion U.S. leveraged loan market, according to LCD. The volume of leveraged loans in 2017 is up 52% in the U.S. and on pace to surpass the 2007 record of $534 billion, according to S&P Global Market. The share of covenant-lite loans in Europe is approaching the level in the U.S. although the size of the European market is smaller.

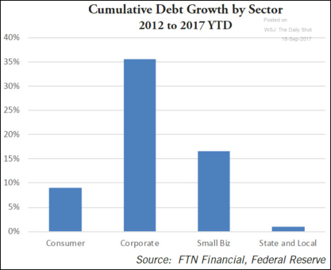

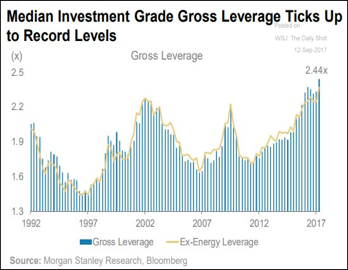

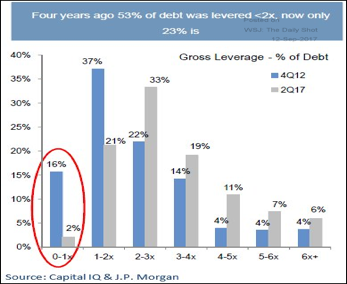

Since the end of 2012, U.S. real GDP had grown 10.7% through the second quarter of 2017. During the same period, corporate debt has grown by more than 35% according to the Federal Reserve, more than 3 times as fast as the economy. As U.S. companies have added more debt to their balance sheets, the amount of corporate leverage has increased from 1.7 in 2010 to 2.44 at the end of the second quarter in 2017. The leverage ratio is the highest on record and above the prior highs in 2008 and 2002. U.S companies are gorging themselves on debt since interest rates are so low. It is more worrisome that the quality of corporate debt has deteriorated. In 2012, 53% of corporate debt was leveraged less than 2 to 1. In 2017 only 23% of debt had a gross leverage ratio of less than 2 to 1. The percent of corporations with a leverage ratio above 4.0 has doubled from 12% in 2012 to 24% in 2017. In its second quarter report, the Bank for International Settlements highlighted the growth of covenant-lite loans in the U.S. and said they could harm the economy during the next downturn or from a rise in interest rates. According to the minutes of the September 2016 FOMC meeting, some members of the Federal Open Market Committee worried that some corporations were using ultralow rates to do more than their usual borrowing. “A few participants expressed concern that the protracted period of very low interest rates might be encouraging excessive borrowing and increased leverage in the nonfinancial corporate sector.” The increase in corporate leverage, deterioration in quality, and surge in covenant-lite loans since September 2016 suggests that more than a few FOMC members should be concerned that low interest rates are encouraging excessive borrowing.

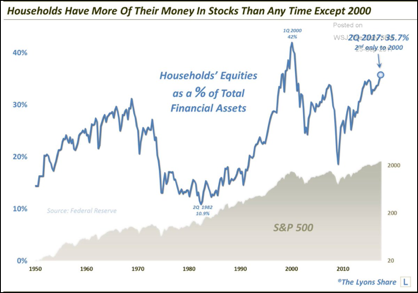

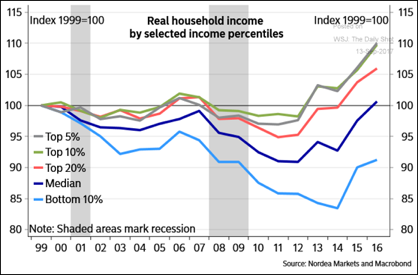

A significant portion of the newly assumed debt by corporations has been used to buy back $3.6 trillion of their stock, which has certainly helped the S&P 500 to continue making new highs. Equities as a percent of household financial assets is at the highest level since 1950, other than during the dot.com bubble. The Federal Reserve used their Quantitative Easing programs to boost the value of stocks, homes, and bonds. The Fed believed the wealth affect would result in an increase in consumer spending that would elevate growth so a self sustaining recovery would take hold. The Fed’s QE programs have increased the value of stocks, homes, and bonds. At the end of the second quarter, household net worth was a record $96.2 trillion, up 1.8% from $94.5 trillion as of March 31, 2017. Since the end of the recession in June 2009, household net worth has increased from $56.1 trillion or 71.5%, but real GDP has only increased 18.3%. This indicates that the expected wealth affect was far weaker than what the Fed forecast, which may explain in part why the Fed’s annual GDP forecasts were for years too optimistic. The primary reason why the economy didn’t benefit more from the increase in asset values is that income growth has been so weak during this recovery. Median incomes have only surpassed their high in 2007 and 2000 in recent months, while those in the top 5% breached the prior high in late 2012 and the top 10% in mid 2014. The bottom 10% are still more than 8% below were their income was in 2000 more than 16 years ago.

Monetary policy increased income inequality which is why the economy never reached a sustainable growth path. Consumer spending comprises almost 70% of GDP and the simple reality is that the majority of American workers didn’t receive the post World War II average increase in annual wages of 3.3%. Instead, income growth averaged 2.2%, which means wage growth in the average Post WWII recovery was 50% higher than in the 2009 recovery, despite the Fed’s QE programs. There is a good chance that the Fed’s monetary policy contributed to this sub-par growth in wages. Companies were so incentivized by low interest rates they not only used cash flow to buy back stock, but borrowed a lot of money to finance stock repurchases, rather than increase wages.

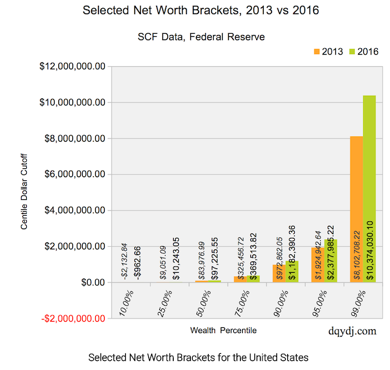

Since the Fed’s Quantitative Easing boosted asset values far more than incomes, it also widened the already large gap in net worth between those in the top 25% and bottom 25%. Although every group experienced improvement between the Federal Reserve’s Surveys of Consumer Finances in 2013 and 2016, the gains were heavily weighted to those in the top 25%. These results are not surprising since a 10% increase in a home valued at $200,000 increases the owners net worth by $20,000 while the owner of a $1,000,000 home experiences a $100,000 bump in net worth. Since many of those in the bottom 25% of wage earners don’t even have savings for a portfolio of stocks and bonds, the increase in stock and bond prices haven’t benefited them. The Fed’s focus should not be on asset values but on income growth. Savings are driven by excess income over expenses. If wage growth is insufficient to cover expenses, there is little or no savings available to buy a home, or income to buy a more expensive home, and certainly no savings to fund an investment portfolio.

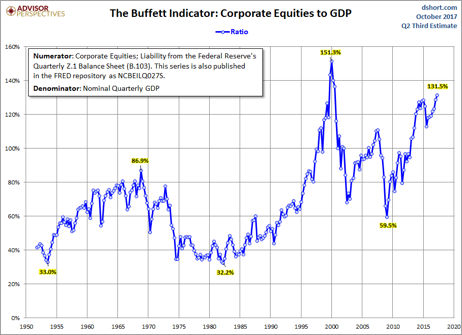

Whether one uses Tobin’s Q-Ratio, Shillers CAPE Ratio, Crestmont Research’s P/E Ratio, or the Buffett Indicator, the message is the same. (Chart compliments of Advisor Perspectives and dshort.com) The stock market is at the second most expensive level since 1900, exceeded only by the tech mania bubble in 2000. Strategists are often quick to point out that interest rates are at historic lows. What’s interesting about this argument is that it overlooks the fact that the yield on the 10-year Treasury bond was under 2.5% from October 1938 until October 1950, and didn’t exceed 3.0% until April 1956. In the early 1950’s, these various valuations show that the stock market was valued at less than half its current level.

As financial asset values become more stretched than they already are, they will increasingly pose a risk to financial stability when economic growth slows. In addition, the Federal Reserve has expressed the importance of getting the federal funds rate up to a level so it can be the primary tool of monetary policy again. The Fed does not want to implement Quantitative Easing in the future, unless it is clearly warranted. The Dot Plot after the FOMC meeting in September projects a peak in the federal funds rate of 2.75% in 2019. The longer the Fed waits to get the federal funds rate up to that level the more likely it won’t get there. Understandably the Fed is concerned that if it increases the funds rate too quickly it could jeopardize the recovery. Conversely, if the Fed is too gradual, there is a risk that inflation may begin to run above their 2.0% target necessitating the need for a less than gradual process. The decision facing the members of the FOMC is when do the risks to financial stability, the cyclical peak in the federal funds rates that is too low to enable the federal funds rate to again become a viable policy tool, and the potential for wage push inflation begin to outweigh the FOMC’s obsession to get inflation up toward 2%.

In a speech at the National Association for Business Economics on September 26, Janet Yellen made two comments that frame the Fed’s dilemma. “How should policy be formulated in the face of such significant uncertainties? In my view, it strengthens the case for a gradual pace of adjustments.” She followed this statement with the following comment. “It would be imprudent to keep monetary policy on hold until inflation is back to 2%.” On September 25, William Dudley, president of the New York Fed said, “I expect inflation will rise and stabilize around 2% over the medium term.” In a speech on September 25, Charles Evans, president of the Chicago Fed, stated, “I think we need to see clear signs of building wage and price pressures before taking the next step in removing accommodation.” The Fed is between a rock and a hard place but has no one to blame but the academic driven mindset of FOMC members for proceeding too slowly in 2015 and 2016, when they increased the federal funds rate just once each year.

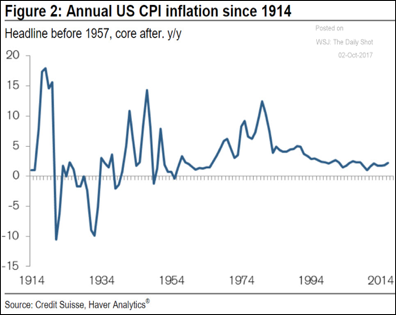

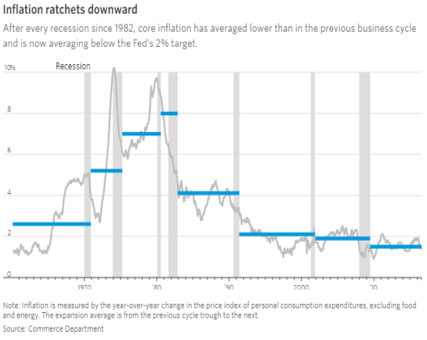

The annual increase in the Fed’s preferred inflation measure – the Personal Consumption Expenditures Index - (PCE) has been trending lower since peaking in 1981 more than 36 years ago. It has ratcheted lower after each recession and has spent most of the time since the mid 1990’s below the Fed’s target of 2%. Low PCE inflation is not a new development or problem. Interest rates have been trending lower since their peak in 1981. This raises an interesting question. Is it possible that low interest rates have contributed to low inflation? Money is a commodity like anything else and the lower cost of money (which low interest rates represent) contributes to lower inflation just as lower prices for goods and services lower inflation. An increase in the cost of money would thus lead to more inflation. This may seem counter intuitive, especially to the academics on the FOMC, but it makes sense.

The European Central Bank (ECB) meets on October 26 and is expected to announce a change in its EQ program after Mario Draghi said in the press conference after ECB’s September 7 meeting, “Probably the bulk of these decisions will be taken in October.” In Draghi’s press conference statement he reiterated the ECB’s fixation on meeting its inflation target of 2%. “Regarding non-standard monetary policy measures, we confirm that our net asset purchases, at the current monthly pace of €60 billion, are intended to run until the end of December 2017, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. The economic expansion, which accelerated more than expected in the first half of 2017, continues to be solid and broad-based across countries and sectors. At the same time, the recent volatility in the exchange rate represents a source of uncertainty which requires monitoring with regard to its possible implications for the medium-term outlook for price stability. Measures of underlying inflation have ticked up slightly in recent months but, overall, remain at subdued levels. Therefore, a very substantial degree of monetary accommodation is still needed for underlying inflation pressures to gradually build up and support headline inflation developments in the medium term.” Despite all the evidence to the contrary, Mario Draghi still believes that the only reason EU inflation hasn’t reached its 2% target is that the ECB hasn’t done enough QE, even though the ECB’s balance sheet is already 37.8% of Europe’s GDP.

During the press conference Draghi was asked about potential bubbles in markets as the result of ultra-loose monetary policy by the ECB and other central banks. Draghi acknowledged that valuations are stretched in a number of markets but doesn’t see any bubbles. “Now on the potential financial stability risks stemming from monetary policies that are very accommodating for a long time, it certainly is a danger, but do we see that now? No, we don't see systemic danger coming from bubbles. If you look at the various markets – the stock market, the bond market – the prime commercial real estate is the only area where you actually see stretched valuations. But even in the residential real estate you see situations where prices have been going up pretty fast in some large cities, in some countries, but not on average and not in other cities in the same countries or in other countries at the same speed.”

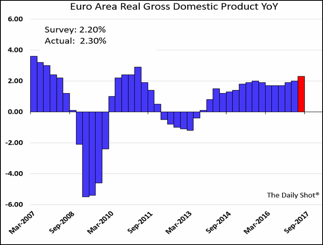

If it were up to Mario Draghi, the ECB wouldn’t pare its QE program or increase their policy rate from minus -.40% until inflation was near 2% and rising. There are 23 members on the ECB’s Governing Council and I believe they will announce at their October 26 meeting that the ECB will reduce its monthly bond purchases from $60 billion beginning in January 2018. As Draghi noted, the Eurozone economy improved more than expected in the first half of 2017. Although retail sales slipped in September, recent gauges of consumer and business sentiment are at multi-year highs, suggesting GDP growth is likely to remain good. The headwind from the stronger Euro has eased a bit with the Euro falling almost 3% since it peaked on September 8, the day after Draghi’s press conference. As I discussed at length in the September issue of Macro Tides, the Euro peaked in May 2014 the day after Mario said, “The strengthening of the exchange rate in the context of low inflation is cause for serious concern in the view of the Governing Council.” His assessment after the September 2017 meeting was very similar. “The recent volatility in the exchange rate represents a source of uncertainty which requires monitoring with regard to its possible implications for the medium-term outlook for price stability.” Just as in May 2014, the Euro reversed lower the day after Draghi’s comments on September 7 as currency traders got his message.

As I noted in the September commentary, “The positioning in the Euro futures market shows a multi-year high in Euro long positions, so a decline in the Euro could force longs to sell triggering even more selling pressure.” It may seem counterintuitive for the Euro to decline even as the ECB announces its cutting in QE program. I would note that the Dollar declined by more than 12% from its high in January 2017, even though the Federal Reserve increased the federal funds in March and June. Conventional wisdom says higher interest rates translate to a stronger currency, but that didn’t pan out for the Dollar in 2017.

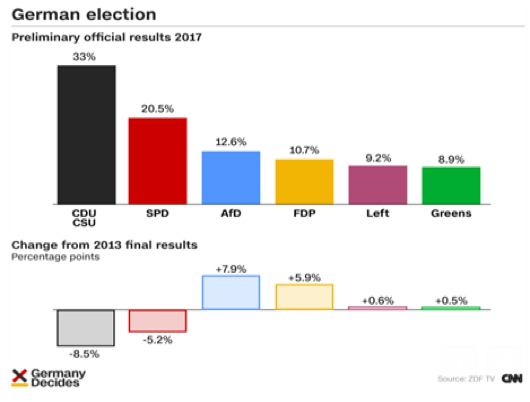

The results of the German election on September 24 could also pose a headwind for Mario Draghi. The Alternative for Germany party, or AfD came in third place, claiming 12.6% of the seats up from just 4.7% in 2013. The AfD, founded only four years ago, became the first far-right party to enter the Bundestag since 1961. In a debate on September 7, AfD candidate Alice Weidel said the ECB’s “illegitimate policy of cheap money” is responsible for rising real-estate prices that are hurting average German voters. Weidel added that her four-year-old party was the only one to channel German anger with the ECB. “This is the reason why the AfD exists,” she said. Prior to the election, Angela Merkel’s Christian Democratic Union (CDU) and the Social Democrats (SPD) of Martin Schulz ruled out any cooperation with the AfD. Of course, that was before they lost so much ground in the election.

There has been opposition to the ECB’s QE program within Germany as conservatives see it as a stealth bailout of indebted south European governments. Germans are especially irked by the massive cash injections, arguing that German taxpayers have to bear the risk for others and have tried to stop the ECB’s QE program in the courts. On August 15, 2017, Germany's constitutional court called into question the European Central Bank's asset purchases, saying they might overstep the central bank's powers, referring the case instead to the European Court of Justice. While it is unlikely the European Court of Justice will shut the ECB’s QE program down, the legal efforts reflect the negative sentiment within Germany which the AfD will only amplify. It is going to be more difficult for Mario Draghi to get a majority on the Governing Council to continue to support ‘a very substantial degree of monetary accommodation.’

The seeds for the next financial crisis have been sown by the Federal Reserve and other Central Banks with their fixation on getting core inflation up to 2%. As long as core inflation remains below 2%, Central Bankers can justify maintaining a level of monetary accommodation that is not justified given economic fundamentals, asset valuations, corporate leverage, and the global reach for yield inspired by extraordinary low interest rates. The negative unintended consequences of delaying the normalization of monetary policy since 2014 are going to contribute to the upcoming financial crisis. To be clear, the next financial crisis is not on our doorstep and may not begin for some time. The onset may be delayed if inflation remains under 2% and Central Banks continue to use low inflation as an excuse to postpone normalization. One thing is clear. The risks posed by the negative unintended consequences from central bank’s monetary experiment are likely to increase, if the Federal Reserve and other Central Banks maintain their 2% inflation fetish.

A Game of Chicken between Central Banks and Bond Investors

As discussed last month, the interests of the Central Banks and international bond investors are no longer aligned. “When the Fed and ECB wanted to repress interest rates they could enlist the help of market participants to ride their coattails since investors would profit from the collaboration. Unwinding negative real interest rates and curtailing bond purchases will cause interest rates to rise and create losses for bond holders. Rather than being coconspirators, market participants will be combatants with the central banks and more importantly with each other.” This is a significant change which has yet to manifest itself. The question isn’t if it will but when it will occur. No matter how gradual the Federal Reserve and the ECB progress toward less monetary accommodation, at some point international bond investors are going to realize that the odds the Fed and ECB will be able to unwind accommodation without a hiccup are lower than they are comfortable with. This will lead global bond investors to reduce exposure to Treasury bonds and European sovereign bonds. What is likely to start as a trickle could turn into a torrent as global bond yields break out above prior interest rate highs.

From the low in the 30-year Treasury bond yield of 2.10% in July 2016, the yield rose to 3.20%, an increase of 1.10%. A 50% retracement targeted 2.65% which was reached on September 7 and has been followed by a sharp rise to 2.933% on October 6. This suggests that an important low in yields was achieved on September 7. As I discussed in the October 2 Macro Tides Weekly Technical Review, “The yield on the 30-year Treasury bond has closed above the black down trend line connecting the May and June high for 4 consecutive days, adding further confirmation that the low in yields on September 7 was an intermediate low. I expect the yield to rise to 2.91% - 2.94% (blue horizontal trend line) before the 30-year yield becomes overbought and a rally in bond prices develops.” Although the yield may fall to 2.80% in the short term, a test of 3.0% - 3.04% is likely. A breakout above 3.05% is likely to be followed with a test of the March high near 3.20%. A close above 3.21% is where the trickle could turn into a torrent.

The initial move higher was 1.10% on the 30-year Treasury bond from the low of 2.10% to 3.20%. An equal move from the September 7 low of 2.65% suggests the 30-year Treasury yield has the potential to soar to 3.75% during the next twelve months.

The yield on the 10-year German Bund has made a series of higher lows since falling to .154% on April 18, .227% on June 15, and the recent low of .312% on August 9. In addition, the yield has also made higher highs with a high on December 12, 2016 at .465%, two highs of .484% on January 16, 2017 and March 10, and a spike high on July 14 of .604%. The pattern of higher lows and higher highs indicates that the trend in the 10-year German Bund is up. Last week it tested the highs at .484% before finishing the week at .465%. A close above .61% is likely to lead to more selling and a higher yield on the 10-year Bund. On June 2015, the German Bund yield closed at .922%. This peak was followed a decline to minus -.189% after the ECB dropped its policy rate to minus -.40%. The high of .922% thus becomes the target once the German 10-year Bund closes above .61%. As the yield rises on the 10-year German Bund, it will pull yields throughout Europe higher. Higher yields in Europe will pull Treasury bond yields up as well, since yields in the global bond market are linked like Siamese twins.

Jim Welsh

760-710-1956

[email protected]

@JimWelshMacro

Read more commentaries by Macro Tides