TIPS Outperform Straight Treasurys Slightly in a Quiet 2017 Third Quarter

Membership required

Membership is now required to use this feature. To learn more:

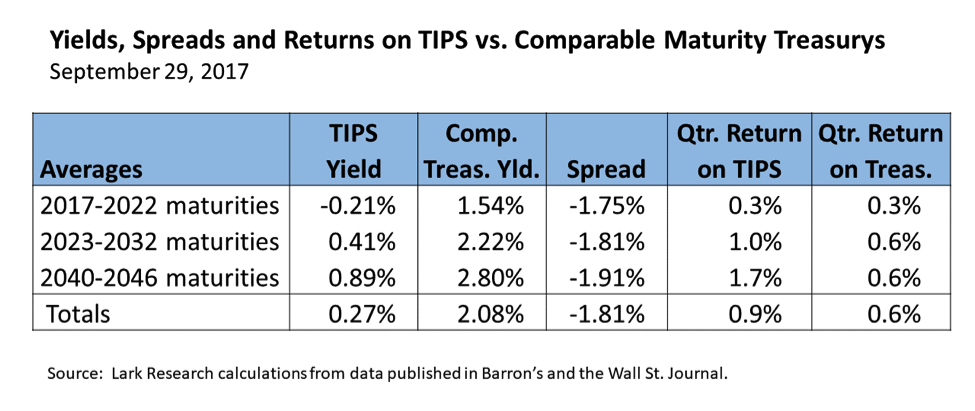

View Membership BenefitsIn what was a surprisingly quiet quarter for the Treasury market, TIPS outperformed straight Treasurys. According to my calculations, TIPS on average earned 0.9 percent in the 2017 third quarter compared to 0.6 percent for straight Treasurys. Investors bid the prices on short-term TIPS up so that short-term TIP yields fell back into negative territory, even though inflation (as measured by the CPI) eased during the quarter. On balance, TIP yields declined from 0.40 percent in the 2017 second quarter to 0.27 percent in the third quarter. Straight Treasury yields (on comparable maturities) increased slightly from 2.03 percent to 2.08 percent, mostly because of an increase at the short-end of the yield curve.

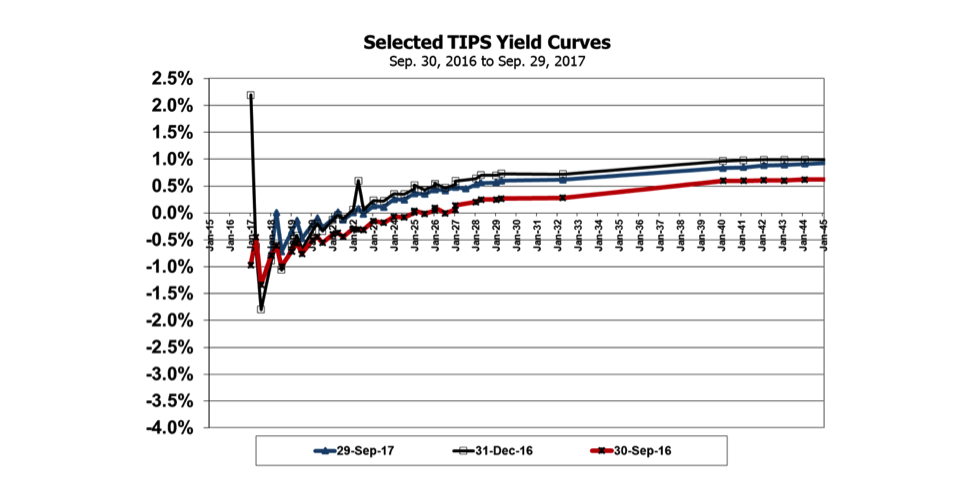

At quarter’s end, the TIPS yield curve was up modestly over the prior year, but it is little changed so far in 2017.

With the 13 basis point decline in TIPS yields and five basis point increase in straight Treasury yields, the TIPS spread increased by 18 basis points in the quarter, from 163 basis points to 181 basis points. That puts the TIPS/Treasury spread back above its 2009-2017 average of 171 basis points. On the surface, it seems that investors were willing to bid down TIPS yields, especially at the short end of the yield curve because they expect a comparable pick-up in inflation.

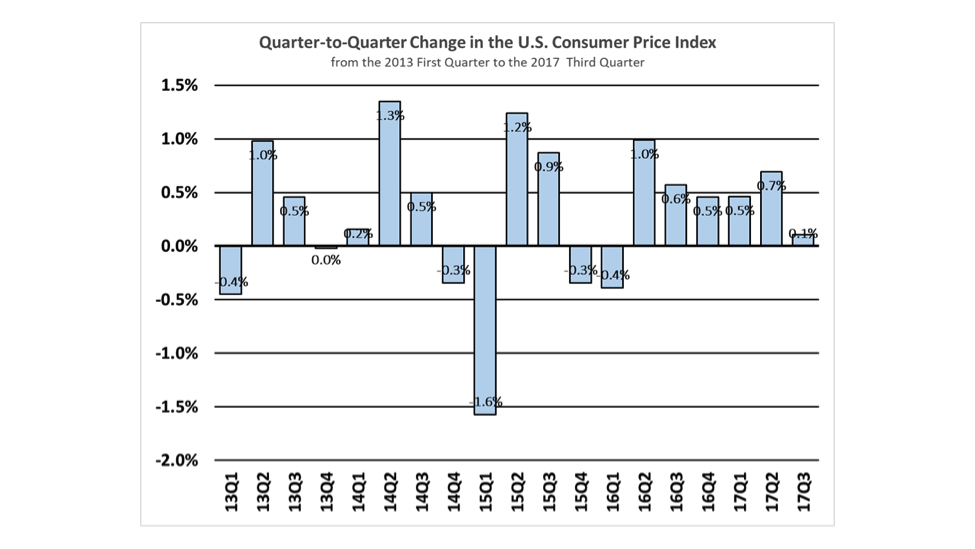

If that is correct, that view seems somewhat at odds with the trend in inflation, as measured by the CPI. On a quarter-to-quarter basis, CPI inflation slipped to 0.1 percent in the 2017 third quarter, the lowest gain in the past six quarters.

On a year-over year basis, the CPI was up 1.94 percent in August. That is better than a year ago, when the year-over-year change was running close to 1.00 percent, but down from the gains of 2.50 percent or better recorded in the opening months of 2017. Despite falling back since the beginning of the year, the year-over-year gain in headline CPI inflation has improved by about 30 basis points since June.

The consensus view of economists, as measured by the Philly Fed’s Survey of Professional Forecasters, anticipates that headline CPI inflation will average 1.7 percent in 2017. That’s up from 1.25 percent in 2016, but it appears to be much too conservative, given the average 2.2 percent increase recorded in the first half of the year. To bring the average down to 1.7 percent for the full year, the year-over-year change in headline CPI will have to fall well below 1.0 percent in the final months of 2017. Given the recent bump in oil prices that we have seen since the middle of June, the chances of that happening are probably quite low, in my view. I think it is much more likely that the change in headline CPI will average 2.0 percent or more for all of 2017. For 2018 and 2019, the Philly Fed forecasters expect the CPI to rise 2.2 percent and 2.3 percent, respectively.

In a recent speech, Fed Chair Janet Yellen said that the Fed should resume raising the Fed Funds target rate before inflation moves back to its two percent target, because monetary policy works with a lag. As long as there is no political interference and the pace of economic growth does not deteriorate, it seems likely that the FOMC will raise its Fed Funds target by a quarter point (25 basis points) in December, with probably two or three more increases in 2018.

Assuming a parallel shift in the yield curve across all maturities as short-term rates rise (which has not been the case so far), then real interest rates should rise faster than inflation. In that case, I expect that TIPS and straight Treasurys would face similar headwinds. Later, as inflation then begins to pick up, TIPS should begin to outperform straight Treasurys. If, on the other hand, inflation rises before interest rates, I expect that TIPS would outperform straight Treasurys and the TIPS/Treasury spread would increase.

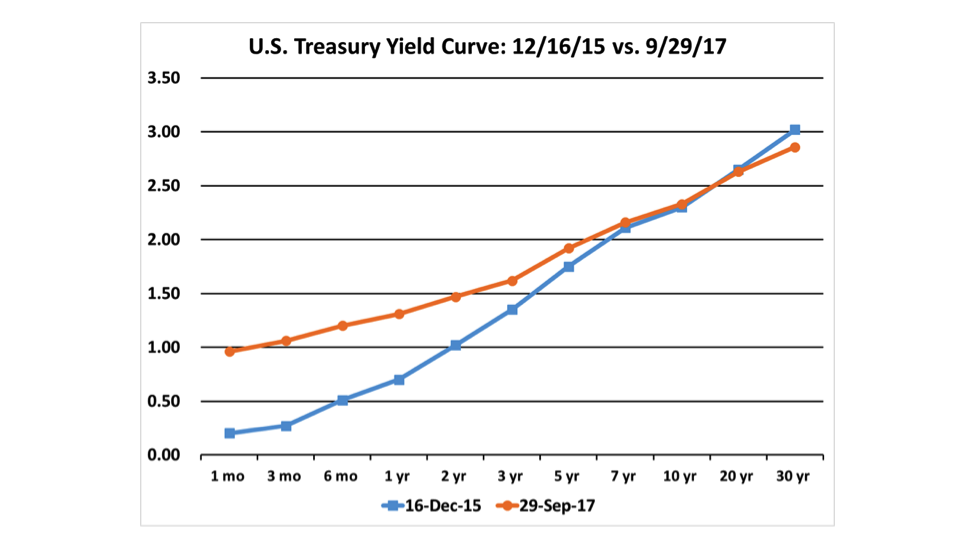

The behavior of long-term rates is obviously an important consideration. The Fed’s goal of normalizing short-term interest rates will be difficult to achieve, if yields on long-term Treasurys do not move up commensurately. Since the Fed began raising the Feds Fund target in December 2015, short-term rates are up by about 75 basis points, but long-term yields have not budged. (Yields on five-, seven- and 10-year notes are unchanged; while the yield on the 30-year Treasury bond was 16 basis points lower.)

The Fed’s balance sheet normalization plan will likely result in reduced demand for U.S. Treasury and agency securities. Under that plan, the Fed will allow its holdings of U.S. Treasury and agency securities to roll off at the pace of $10 billion per month, increasing to $50 billion per month in one year’s time. That’s $300 billion of roll-off in the first year, rising to $600 billion each year thereafter. This should provide support for longer-term Treasury yields going forward. In this way, the balance sheet normalization plan may help the Fed to achieve its goal of normalizing interest rates.

October 5, 2017

Stephen P. Percoco

Lark Research, Inc.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All