The U.S. Federal Reserve has announced the October start of the slow reversal in the unprecedented expansion of its balance sheet following the 2008 Global Financial Crisis. Chairwoman Janet Yellen declared the Fed’s asset purchases, commonly known as “quantitative easing” (QE), successful in “stimulating a faster recovery than we otherwise would have had.”

That’s debatable. QE no doubt kept the economy from falling off a cliff after the crisis broke. But critics point out that the 1.6% average yearly growth since the recovery began is historically sluggish. And after expanding its balance sheet to $4.5 trillion from less than $900 billion, the liquidity generated has reflated asset prices to levels that fundamentals may be hard pressed to justify, leaving markets vulnerable to destabilizing pullbacks.

Fed officials—not to mention their peers at other major central banks—seem increasingly sensitive to that danger. Signs are growing that they are factoring to a greater degree the potential impact of their policies on financial market stability. In any case, QE’s unwind should in time reduce its market distortions and allow for risk to be priced more appropriately.

QE and ground-level interest rates have no doubt helped push unemployment to less than longer-run targeted levels. As joblessness fell, the Fed gained sufficient confidence to halt its buying binge in 2014 and start raising its key interest rate in late 2015. Following that first post-crisis hike, the Federal Open Markets Committee (FOMC), the Fed’s monetary policy panel, raised the Federal funds rate another 25 basis points last December and so far this year lifted it two more times, each by the same amount. Although policy makers kept it at 1% to 1.25% at their Sept. 20 meeting, they signaled in their “dot plot” assessments of future rate levels that another quarter-point hike is likely this year. The rate futures market is aligning with that expectation, pricing in a 71% probability of a quarter-point hike this December.

That’s still very accommodative by historical standards. If economic growth hasn’t taken off to the degree expected by the Fed in recent years, neither have the predictions of Fed critics that inflation would come roaring back. To the contrary, the Fed’s preferred Personal Consumption Expenditures Index, excluding food and energy, hasn’t hit the 2% target in more than five years, and sagged to 1.4% in July from 1.9% in January (Chart 1). That has made Yellen’s repeated characterization of weak inflation reports as “transitory” feel stretched, especially as some Fed officials publically question whether low inflation is a cyclical or structural challenge. But a consensus-beating headline August Consumer Price Index (CPI) of 1.9% annual growth no doubt bolstered FOMC members to vote unanimously on the latest rate decision and balance sheet reduction plan, which lets $10 billion a month roll off over the fourth quarter, rising each subsequent quarter until it reaches $50 billion per month after a year.

CHART 1: CORE PCE COMING UP SHORT 9/30/2011 - 7/31/2017

Source: FactSet

The FX Barometer

As the rate decision and balance sheet unwind were well flagged in advance, markets took the announcements in stride, including the guidance on another hike in December. The S&P 500 Index and Dow Jones Industrial Average both hit record closing highs, and U.S. government bond prices fell, with the yield on the 10-year Treasury rising three basis points to 2.27%. The dollar also strengthened sharply against its major counterparts.

The greenback’s move may signal an important shift in how global markets are viewing major central bank monetary policy. Driving the change is the now much-discussed synchronization of accelerating global growth, which is reflected in the World Trade Organization’s Sept. 21 forecast upgrade of its 2017 global merchandise trade volume growth to 3.6% this year from 2.4% previously. That’s a significant improvement from the plodding 1.3% increase logged in 2016. The International Monetary Fund expects 3.5% global growth this year and 3.6% in 2018, up meaningfully from 3.2% in 2016. Major central banks outside Japan’s are girding to reduce accommodation or tighten policy. The Bank of Canada, like the Fed, has already started.

But things lately haven’t been as clear cut for the Fed. “Until recently, the Fed made moderating noises due to some moderating data over the summer,” Thornburg CEO and portfolio manager Jason Brady says. But he notes that while some data have come in weaker, other data have come in a bit stronger. In addition to the August CPI, Producer Price Inded (PPI), Institute of Supply Management (ISM) Manufacturing, home price index reports as well as the Leading Economic Index all showed improvement. Corporate earnings have also been encouraging: third quarter S&P 500 estimated earnings growth stands at 4.5%, with eight sectors expected to report earnings expansion in the period, led by the energy sector, according to Factset. And broad after-tax corporate earnings as tracked by the Bureau of Economic Analysis in its National Income and Product Accounts rebounded in the second quarter, resuming the recovery started in late 2015. (Chart 2).

CHART 2: U.S. EARNINGS BACK ON TRACK 4/1/2012 - 4/1/2017

Source: U.S. Bureau of Economic Analysis, St. Louis Federal Reserve

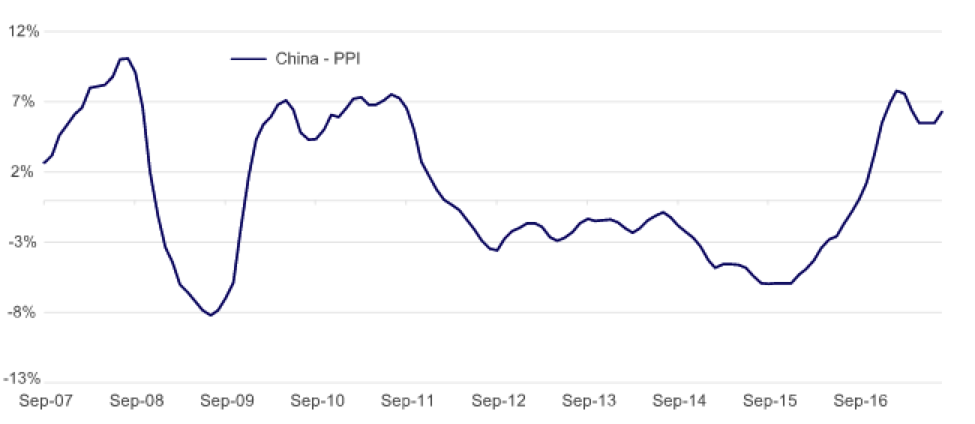

Economic growth and earnings in Europe and emerging markets are also accelerating. Significantly, the rebalancing in China’s economy, the world’s second largest, appears to be well underway. CLSA points out that consumption drove two-thirds of China’s 6.9% year-on-year real economic growth in the first half, while capital formation finally took a back seat, contributing the remaining third. China’s economic transition will improve the quality and sustainability, albeit at a lower level, of its still strong growth. Beijing’s supply-side reform agenda continues apace, cutting excess capacity in heavy industries and the pollution they generate. It’s worth recalling that China’s PPI inflation turned positive one year ago, and after lapping it with a recent dip, has remained squarely in positive territory (Chart 3).

CHART 3: CHINA PPI PUSHING HIGHER 9/28/2007 - 8/31/2017

Source: FactSet

In a way, this year has represented something of a role-reversal in market sentiment toward the outlook for benchmark rates in the U.S. and the rest of the world. As the Fed started reducing its stimulus in 2014 with the end of QE purchases and began hiking the Fed funds rate a year later, the dollar took off. It gained nearly 30% from June 2014 through the end of 2016, when the U.S. “reflation” trade was in full swing after the Republicans’ November electoral sweep of the White House and Congress. Outside the U.S., the mood wasn’t nearly so optimistic, and it appeared that the Fed would be the only big central bank able to raise rates.

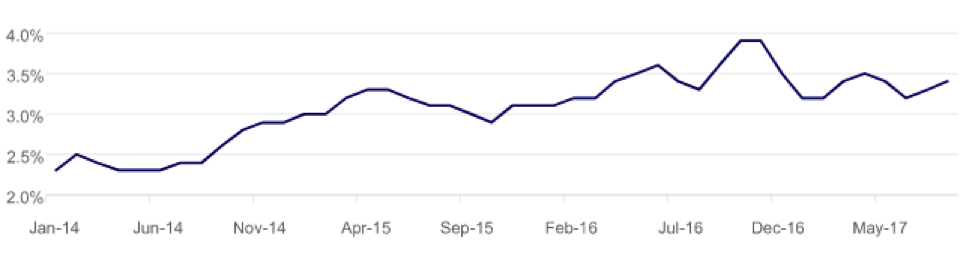

But as 2017 got underway, it quickly became apparent that if deregulation in the U.S. is feasible, infrastructure spending and health care and tax reforms would be more difficult than anticipated. As inflation began falling again, so did the wage growth that had been building since 2014, despite 4.4% unemployment (Chart 4).

CHART 4: THE WAGES OF WEAK INFLATION: WAGE GROWTH (MEDIAN ANNUAL PERCENT CHANGES) 1/1/2014 - 8/1/2017

Source: Bureau of Labor Statistics, Federal Reserve Bank of Atlanta

A Mystery and a Terminal Rate Cut

Amid the upswing in growth overseas and the subdued inflation data at home, comments from Fed doves called into question not just the future pace of rate hikes, but even suggested that the forecast for the terminal rate, the neutral rate level consistent with full employment, capacity utilization and stable prices, might also have to be revised lower. Fed Governor Lael Brainard recently said low “underlying” inflation may be due to non-transitory factors, so Fed rate hikes should come even more slowly than they have. After the latest FOMC meeting, Yellen said the inflation shortfall this year may not be largely driven by cyclical factors and so “is more of a mystery.” Perhaps the FOMC’s most significant revision was the longer-run downgrade of the Fed funds rate to 2.75% from 3% in June.

So after its strong run on expectations for continued monetary tightening, the dollar this year hit considerable headwinds as the outlook for Fed tightening dimmed (Chart 5). “The market has been discounting further Fed moves while beginning to price in other central bank moves,” Thornburg portfolio manager Jeff Klingelhofer says. “Over the period of weakness for the dollar we’ve seen the story for the U.S. move from higher inflation as a result of rising wage pressure, to wage pressure abating and inflation moving down significantly. While economic growth is okay, it isn’t great, and the market is re-pricing how much additional tightening the Fed can do.”

CHART 5: U.S. DOLLAR INDEX'S HILLS AND DALES 9/22/2014 - 9/22/2017

Source: FactSet

Klingelhofer notes the market isn’t just taking back some of the dollar gains from the previous two years, it’s also reflecting rates broadly: the ten-year U.S. Treasury yield tumbled from a March 2017 peak of 2.6% to around 2.25% in late September (Chart 6).

CHART 6: 10-YEAR TREASURY YIELDING TO AN UNCERTAIN OUTLOOK 12/30/2016 - 9/22/2017

Source: FactSet

So why would Yellen, her FOMC colleagues and interest rate futures markets tag the December meeting as “live” for another rate increase? As the Trump administration needs to appoint a new chair or re-appoint Yellen along with filling four other vacancies on its board next year, the FOMC “is about to have a very different composition,” Brady points out. “It might be that the current body wants to get the rate to a level that they view as more neutral before they turn over the reins.”

Waiting on Long and Variable Lags

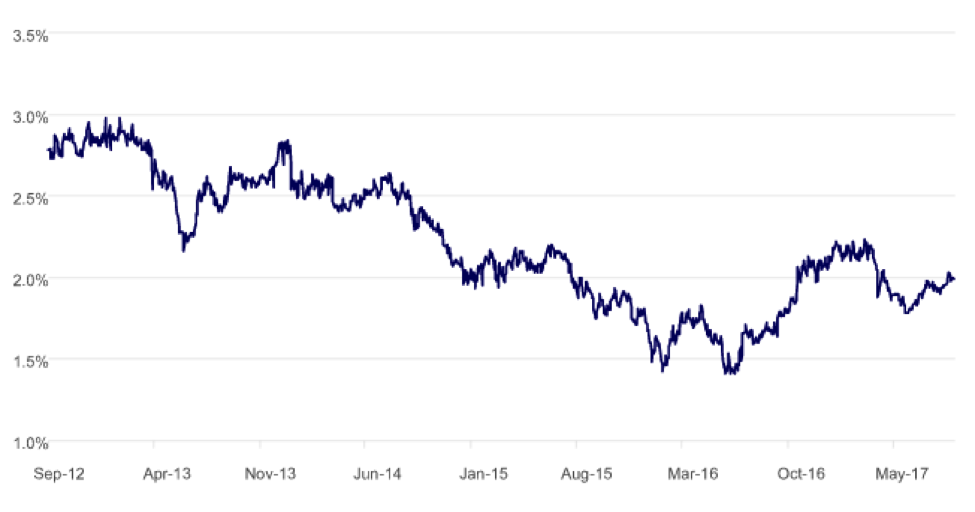

Federal Reserve Bank of New York chief William Dudley recently provided another reason, pointing out that “monetary policy is still accommodative and that financial conditions have eased,” despite the three rate hikes since December. Moreover, “the long and variable lags between monetary policy adjustments and their impact on the economy imply that the FOMC may need to remove accommodation even when inflation is below its goal. In particular, if the unemployment rate were already below its longer-run natural rate, as may be the case currently, the impact on wage growth and price inflation would still likely take some time to become evident,” he noted. That’s particularly the case as inflation expectations are currently “well-anchored at or slightly below our 2% objective,” Dudley added. Five-year forward average inflation expectations have indeed been running at 2% or lower since May, but have been trending higher since June (Chart 7).

CHART 7: 5-YEAR FORWARD INFLATION EXPECTATIONS RATE 9/21/2012 - 9/21/2017

Source: Federal Reserve Bank of St. Louis, FactSet

Dudley’s point about the lag between unemployment running below its long-run natural rate and its impact on wages and inflation is fair. It should color the growing talk about the “death of the Phillips Curve,” which posits that low unemployment should lead to wage growth and inflation, while high unemployment should lead to wage deflation and lower inflation.

If the double-digit unemployment and inflation of the 1970s stagflation didn’t bury the Phillips Curve, it might be premature this time around to speculate that the deflationary impact of technology disruption evident in e-commerce, artificial intelligence, robotics, the “sharing economy” or even of globalization, as companies move capital across borders to take advantage of cheaper foreign labor pools, will together finish it off. Historically, innovation has destroyed some jobs and created others. As for globalization, imports as a share of U.S. GDP and personal consumption are relatively small. Moreover, synchronized global growth also implies rising global inflation—the International Monetary Fund (IMF) expects average CPI in advanced economies to double to 1.8% this year from 0.8% last year, and among emerging markets accelerate to 4.5% from 4.3% in 2016. Accelerating global inflation is also driving the growing degree of synchronized monetary policy.

Perhaps the lag Dudley mentions needs to play out before wage growth revives. Or perhaps unemployment isn’t yet below its long-run natural rate. BCA Research notes that the empirical evidence from past economic cycles supports the view “that U.S. wage growth has tended to accelerate once the unemployment rate falls into the range of 4% to 5%.” But if the labor force participation rate continues to crawl higher, 4.4% unemployment may still hold a while before the output gap closes. “Once the output gap is fully closed, any further decline in slack will cause bottlenecks to emerge, pushing wage and prices higher,” BCA points out.

It’s also worth noting that while Fed policy makers kept their long-run 4.6% unemployment forecast, they penciled in three more hikes in 2018, and shaved their unemployment projection for next year one-tenth of a point from their June forecast to 4.1%. If joblessness hits that level or falls below 4%, a subsequent, fast-steepening Phillips Curve would look very much alive.

The labor participation rate appears to have troughed in September 2015 at 62.4%, and has since inched higher to 62.9%. While still low by historical standards, given the retirement of the baby boomers and the outlook for immigration, where the natural labor force participation rate lies isn’t clear. But if unemployment does continue to fall, at some point wages will have to resume rising. Inflation could well follow.

It’s nice to see the Fed and most other major central banks recognize the acceleration in global growth and prepare to unwind their rate and asset purchase interventions, which have distorted markets in one way or another. “Central banks around the world are factoring in the stronger growth and some of the negative consequences of accommodative policy,” Klingelhofer says. “At a minimum, they are looking to water down the punch in the punchbowl.”

Read more Global Perspectives from Thornburg >>

Important Information

Before investing, carefully consider the Fund’s investment goals, risks, charges, and expenses. For a prospectus or summary prospectus containing this and other information, contact your financial advisor or visit our literature center. Read them carefully before investing.

The performance data quoted represents past performance; it does not guarantee future results.

The views expressed are subject to change and do not necessarily reflect the views of Thornburg Investment Management, Inc. This information should not be relied upon as a recommendation or investment advice and is not intended to predict the performance of any investment or market.

Any securities, sectors, or countries mentioned are for illustration purposes only. Holdings are subject to change. Under no circumstances does the information contained within represent a recommendation to buy or sell any security.

Investments carry risks, including possible loss of principal. Portfolios investing in bonds have the same interest rate, inflation, and credit risks that are associated with the underlying bonds. The value of bonds will fluctuate relative to changes in interest rates, decreasing when interest rates rise. This effect is more pronounced for longer-term bonds. Unlike bonds, bond funds have ongoing fees and expenses. Investments in lower rated and unrated bonds may be more sensitive to default, downgrades, and market volatility; these investments may also be less liquid than higher rated bonds. Investments in derivatives are subject to the risks associated with the securities or other assets underlying the pool of securities, including illiquidity and difficulty in valuation. Investments in equity securities are subject to additional risks, such as greater market fluctuations. Additional risks may be associated with investments outside the United States, especially in emerging markets, including currency fluctuations, illiquidity, volatility, and political and economic risks. Investments in the Fund are not FDIC insured, nor are they bank deposits or guaranteed by a bank or any other entity.

Please see our glossary for a definition of terms.

Thornburg mutual funds are distributed by Thornburg Securities Corporation.

Thornburg Investment Management, Inc. mutual funds are sold through investment professionals including investment advisors, brokerage firms, bank trust departments, trust companies and certain other financial intermediaries. Thornburg Securities Corporation (TSC) does not act as broker of record for investors.

Read more commentaries by Thornburg Investment Management