It is a big week for economic data. The punditry will be analyzing the Trump tax proposal. Everyone will be drawing conclusions about how these factors may be linked with stock prices. Expect people to be asking:

Does economic strength equal stock market strength?

Last Week Recap

My expectation for last week was right on target. Attention rapidly turned to the Trump tax proposal. More on that in today’s Final Thoughts.

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short via Jill Mislinski. She notes the weekly gain of 0.68%. While the range was slightly higher than last week, it was still less than 1.5% on an intra-day basis.

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read the entire post for several more charts providing long-term perspective, including the size and frequency of drawdowns.

The Silver Bullet

As I indicated recently I am moving the Silver Bullet award to a standalone feature, rather than an item in WTWA. I hope that readers and past winners, listed here, will help me in giving special recognition to those who help to keep data honest. As always, nominations are welcome!

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The economic news remained quite positive.

The Good

-

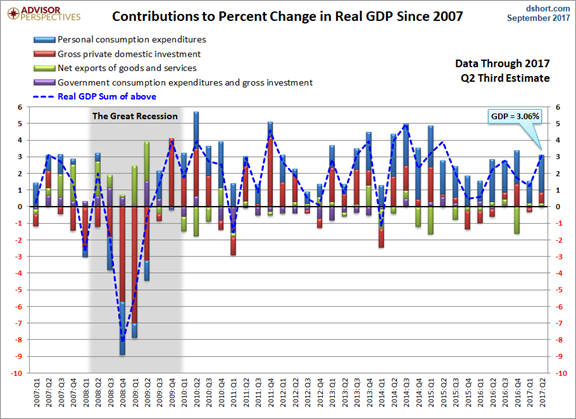

Q2 GDP registered a revised gain of 3.1%. This is backward looking, but an improved base for the rest of the year. The third quarter does not look as promising. Jill Mislinski’s “inside the GDP” story is a great look at the impact of individual GDP components.

-

North Korea and the US are in direct contact (BBC). The back-channel discussions will probably be more fruitful than the contact via tweets.

-

Serious mortgage delinquencies declined again. Fannie Mae (via Calculated Risk) notes that the level is at its lowest since November, 2007.

-

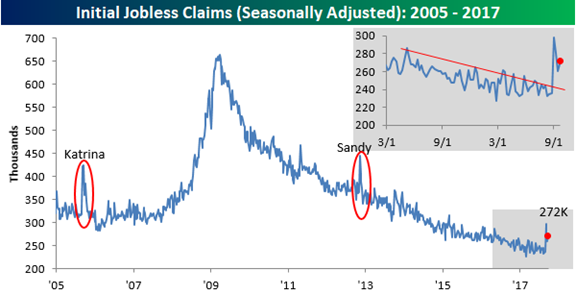

Jobless claims “defy nature” reports Bespoke. Their well-designed chart illustrates the point. New Deal Democrat’s “weather adjusted” calculation puts initial claims at 237K.

The Ugly

Puerto Rico after-effects. The needed infrastructure rebuild is massive. And do you know the largest element of the Puerto Rican economy? If you said “pharmaceuticals” you beat me. Plenty of drug production is affected.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

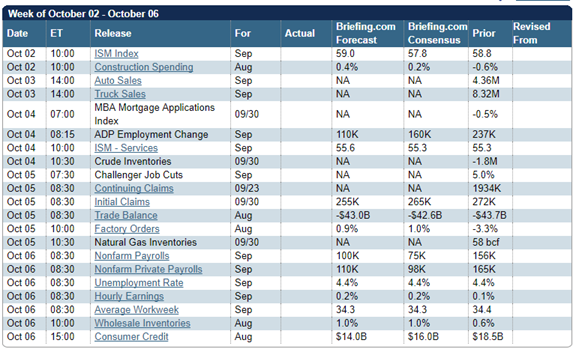

The Calendar

We have plenty of economic releases on the schedule, including the most important. The ISM indexes and auto sales are noteworthy, but the data on employment will take center stage. Fed participants will be in abundance. And of course, there might be an important tweet.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

The avalanche of economic data, right before earnings season, could refocus attention from politics to economic fundamentals. The two are related, of course. The state of the economy and employment is the backdrop for the debate on tax policy changes – not to mention political credit-claiming!

Expect the punditry to be asking:

Does economic strength imply stock market strength?

It is popular to note that the economy does not equal the stock market, that stock trading is not the same as GDP futures, etc. That said, the reasons for market strength or weakness are a continuing topic of interest. Here are some common claims about the extended market rally.

- It is crazy! Valuations are sky high according to CAPE and other measures.

- Asset prices are higher only because of the Fed – maybe with an assist from other central banks.

- A recession is imminent. (Some debunking from HORAN).

- It seems OK for the moment, but expect a major correction in the near future.

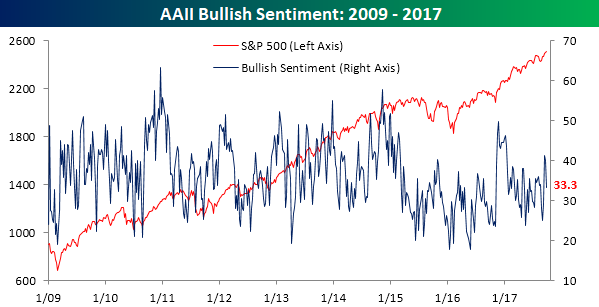

- Complacent investors are ill-prepared for a decline. Suzanne Woolley (Bloomberg) offers an alternative viewpoint. See also the sentiment chart above.

- Stock gains depend upon expectations of policy changes – Trump-designed or otherwise.

- Stock prices have followed the increase in earnings expectations. (Eddy Elfenbein sees a good earnings season ahead).

- Stock prices do not track the economy on a short-term basis, but long-term expectations are crucial. (Brian Gilmartin).

As usual, I’ll have more in the Final Thought, where I always emphasize my own conclusions.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

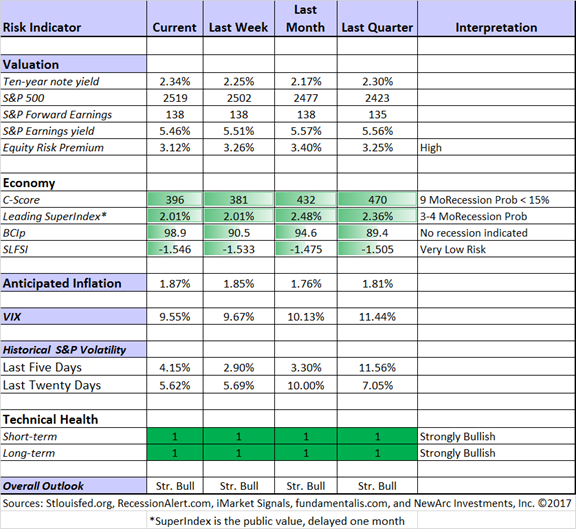

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

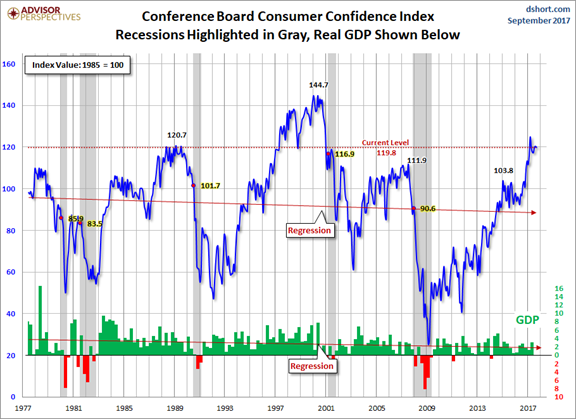

Georg Vrba: Business cycle indicator and market timing tools. It is a good time to show the chart with the business cycle indicator.

Doug Short: Regular updating of an array of indicators. Great charts and analysis.

Featured Guest Sources

New Deal Democrat explains his method for hurricane adjustments, focusing on industrial production. It is interesting, and worth a good look for those interested in the data!

…reasonable temporary workaround for industrial production unaffected by the recent hurricanes is to average the 4 regional Fed surveys, minus Dallas, plus the Chicago PMI.

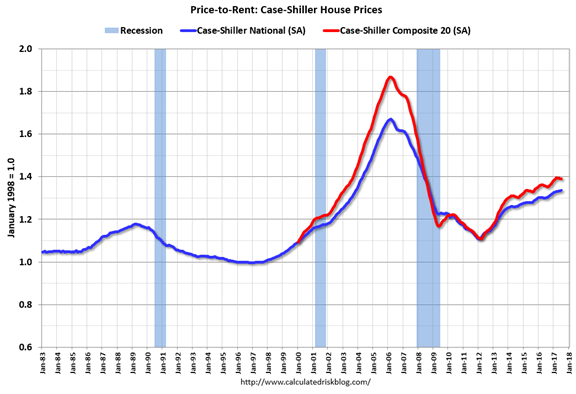

Calculated Risk provides an interesting take on the home price to rent ratio. Bill shows how much lower current values are than before the Great Recession.

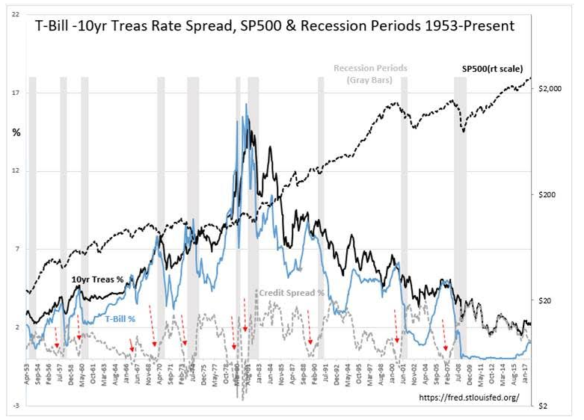

“Davidson” (via Todd Sullivan) has a nice analysis of rate spreads and the prognosis for equities.

From current T-Bill/10yr Treasury rate spread levels, historicaly it has taken 2yrs-3yrs before the 0.20% level has been reached. I suspect it will take a similar time frame before we see 0.20% again. Till then, it is reasonable to expect we are likely to experience an expanding economy and higher equity prices.

Be bullish! The rate spread tells you to be so.

Insight for Traders

We have not quit our discussion of trading ideas. The weekly Stock Exchange column is bigger and better than ever. We combine links to trading articles, topical themes, and ideas from our trading models. This week’s post analyzed the difference between patience and complacency. Blue Harbinger has taken the lead role on this post, using information from me and from the models. He is doing a great job.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be the unusual, helpful, and honest post from “BeatlesRockerTom.” Since no one has a perfect record, his recap of a trade gone wrong includes lessons for everyone. He explains the behavioral finance reasons why people choose inaction—anchoring, sunk costs, and failing to see opportunity costs. He then analyzes his reasons for selling his own loser and moving on. You will learn and enjoy reading this refreshingly honest story.

By contrast, I often see investors holding on to losing positions, hoping they will just get back to even. If the stock does in fact rebound to their purchase point, that is probably the wrong time to sell!

Stock Ideas

Chuck Carnevale does a thoughtful and objective analysis of Apple, Inc. (AAPL). You will learn from the analysis. He concludes:

The company has become enormously large, which is always an impediment to fast growth.

Consequently, in 2012, Apple initiated its first dividend as the company had morphed from a pure growth stock into a high-quality dividend growth stock. Therefore, I believe investors should recognize how Apple has changed as an investment and think of investing in the company accordingly. An important part of achieving investment success is managing realistic expectations. Apple still has investment merit, but I believe the stock today is more about quality, income, and perhaps, moderate growth.

What to expect from the “new” General Electric (GE). Here is what to watch for after the change in leadership.

Blue Harbinger takes profits on Caterpillar and highlights five “better” income options. I own two of them and trade in and out of a third, so I like the approach.

What about Charles Schwab (SCHW). Here are six reasons to buy.

David Fish updates the dividend champions for October.

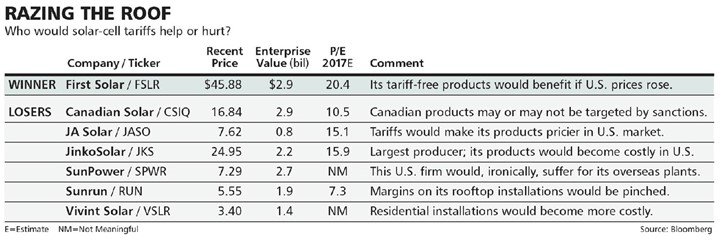

Solar cell tariffs can shake up the industry. Barron’s cover story analyzes the possible effects of Trump Administration policy. Read the entire post to evaluate the logic behind the winners and losers.

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich has an interesting topic every day. His own commentary adds insight and ties together key current articles. As usual this week he had several good posts, but I especially liked his objective and thoughtful discussion about managing your personal balance sheet. As always, he includes good links throughout the week, including today’s choice as best investment advice (above).

Abnormal Returns continues the Wednesday series on Personal Finance. My favorite this week discusses the Investor Policy Statement and how the process of preparing one can help your investing. Tadas now includes a wide range of links on various topics. There is something interesting every day. Readers who have enjoyed the personal finance section should explore some of the other topics as well.

Watch out for….

The fourteen mistakes that can wreck your retirement plans. (24/7 WallSt). Hints: Maximize employer matching and consider allocation decisions.

Poorly designed and biased analyses from those on a mission. Victor Niederhoffer questions the TBills beat stocks argument.

Final Thoughts

This week I want to cover two topics: a follow up on tax reform and more perspective on the stock/economy relationship. But first, a small commercial moment. My principal motivation in writing is helping my growing audience, small by comparison with those selling fear. Many will find this to be enough. Others might benefit from some personal consultation. If you are not completely happy with your current investment plan, I have some free resources that might help. Send an email to main at newarc dot com and we will send information on Understanding Risk, The Top Investor Pitfalls (a good test of whether you can/should fly solo), and How to Get Back into the Market (gradually and carefully).

I personally speak with each potential client, matching needs with programs. It is not buy and hold. Not one size fits all. Not an attempt at all weather, ignoring the biggest risks. It is best to be personal, flexible, and adaptive. That is our approach.

Trump Tax Reform Proposals

Everyone is taking this plan seriously. Every firm has a research team that will instantly tell you the effect of the proposals on you, the general public, income inequality, and anything else. Each media source has a story ready to run, just as they do for obituaries on old folks. This is not analysis; it is jumping the gun. Since the election the major Trump discussion has focused on the effects of his policies. People rushed to buy “Trump Stocks” and attributed stock moves to the “Trump Rally.” Few noted the low probability for adopting these policies.

The current proposal is more of the same – dead on arrival. Even trying to squeeze it in via the convoluted “reconciliation” method instead of the “regular order” there is no winning coalition. (If this sentence did not make sense to you, that is exactly my point. The top sources are discussing the wrong topic).

I am an expert at translating political events into stock ideas, but this administration has provided little so far. I have been looking for “Trump Stocks,” those that will benefit from changes he can actually control. I have found one – a company that works on pipelines. It is a nice winner, but there will eventually be more.

The Economy and Stocks

The most hated rally has its foundation in a misconception about stock valuation – that it is absolute and accurately reflected by history. Actually the intrinsic value of stocks is relative to other available assets and is dramatically affected by inflation.

If you start with a wrong-headed idea that stocks have only been fairly valued (briefly) at one point in the last thirty years, you must continually find new reasons to explain why your theory is not working. The imaginative candidates have included fake data, the Fed, earnings manipulation, and many others.

Alternatively, there is a simple explanation:

Economic strength –à better corporate earnings à higher stock prices. Stocks may not reflect the economy in the short run, but they certainly do in the long run!

What worries me…

- Aggressive and unilateral moves on trade restrictions. The average person does not understand how much this has benefited the world economy, and that of the U.S.

- Strident positions that might waste the chance for some meaningful compromise on tax reform.

…and what doesn’t

- North Korea is declining as an item for worry. There is some distinction between posturing and policy. It still deserves careful monitoring.

- The length of the rally. A strange debate has emerged. Some believe that the rally must be ready to expire because the length is greater than average. Others want to “re-date” the starting point, reducing the overall length. This debate is irrelevant if you realize that business cycles and stock rallies have no specified length. The gradual recovery from a deep decline (in both) should help us understand why there is no “expiration date” on this bull market.

© NewArc Investments, Inc.

Read more commentaries by NewArc Investments, Inc.