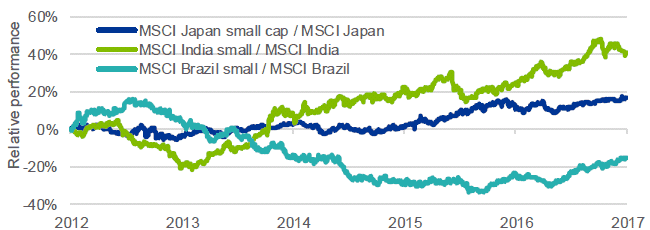

Over the past year, small capitalization indexes have outperformed their large capitalization counterparts. Although the reasons for this rally are varied, attractive return on assets of emerging market (EM) small-cap constituents and specific domestic drivers have supported this trend. We look at Brazil, Japan, and India as particular observations of this trend that should be monitored going forward.

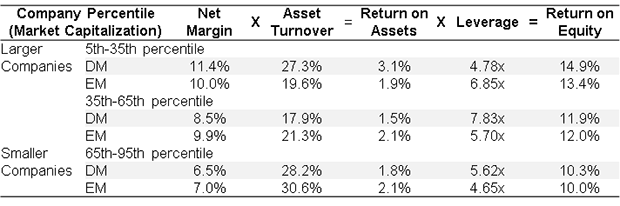

Many small-cap indexes have outperformed their large-cap peers across the globe over the past year. Although the exact reasons for this trend may vary, this global theme has been amplified in select countries. Within emerging markets (EM), particularly companies in the MSCI Brazil and India indexes, small-caps have benefited from structural reforms and improving local economies. Additionally, a historical breakdown of EM companies globally shows why this outperformance may have occurred: small cap EM companies are generally more efficient than their developed market (DM) peers, as measured by their return on assets.

Relative performance of small cap over large cap for Japan, India, and Brazil

EM small caps are generally more efficient than DM small cap peers

India

The country has benefited from the general uptick in global growth and lower oil prices, but the domestic story has been particularly constructive. Indian small-cap companies have benefited as they tend to be more locally driven in nature with high exposure to consumer discretionary. Sector composition differences amongst small and large/mid showcase this point. On the economic front, exports have increased along with regional trade even as trade deficit widened on pickup in gold and capital goods imports. Risks include implementation of the Goods and Services Tax (GST).

Brazil

Brazilian equities and the real have bounced back sharply this year. Legislative reforms have helped improve the economy, including passing a government spending cap, labor reforms, and phasing out the inflationary policies of the previous Lula-administration regulations. These developments have stabilized the economy and led the real to appreciate against the U.S. dollar over the last two years. Brazil has also rebalanced the external side of its economy, helping to reduce the sensitivity to global factors like commodity price swings and global liquidity conditions.

Japan

Economic growth has accelerated amid a rebound in global trade and strong domestic demand at home. Japanese small cap company revenues tend to be more domestically oriented relative to large cap companies, and the structural reform agenda, monetary policy, and economic outlook are all supportive. Domestic demand is supported by wage growth near 15-year highs, however it’s still slow enough not to erode corporate margins. Risks include potential yen strength, however this should affect small cap companies less than large cap companies, and a general slowing in global growth.

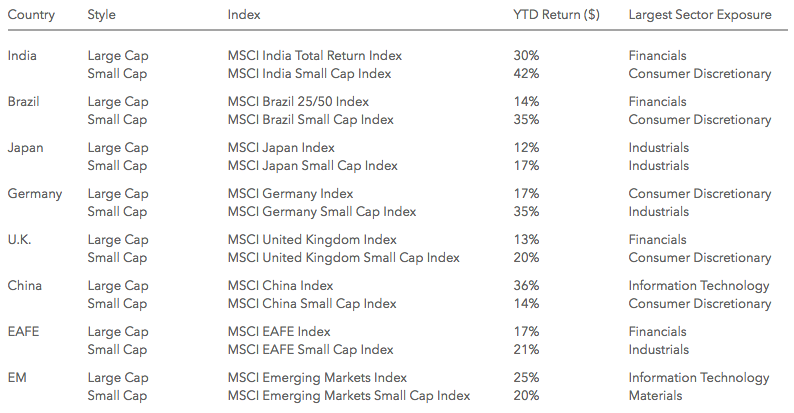

Regional small and large cap returns

Summary

Small cap returns are notable for both the size and broad performance across regions. Strong fundamentals and local reforms in select countries may further support small cap outperformance. Potential small cap opportunities in select countries are accessible through iShares country fund suite.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

Small-capitalization companies may be less stable and more susceptible to adverse developments, and their securities may be more volatile and less liquid than larger capitalization companies.

Certain sectors and markets perform exceptionally well based on current market conditions and iShares Funds can benefit from that performance. Achieving such exceptional returns involves the risk of volatility and investors should not expect that such results will be repeated.

This material represents an assessment of the market environment as of the date indicated; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any issuer or security in particular.

The strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective.

The information presented does not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy or investment decision.

This document contains general information only and does not take into account an individual's financial circumstances. This information should not be relied upon as a primary basis for an investment decision. Rather, an assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a financial advisor before making an investment decision.

The Funds are distributed by BlackRock Investments, LLC (together with its affiliates, "BlackRock").

The iShares Funds are not sponsored, endorsed, issued, sold or promoted by Barclays, Bloomberg Finance L.P., BlackRock Index Services, LLC, Cohen & Steers Capital Management, Inc., European Public Real Estate Association ("EPRA®"), FTSE International Limited ("FTSE"), India Index Services & Products Limited, Interactive Data, JPMorgan Chase & Co., Japan Exchange Group, MSCI Inc., Markit Indices Limited, Morningstar, Inc., The NASDAQ OMX Group, Inc., National Association of Real Estate Investment Trusts ("NAREIT"), New York Stock Exchange, Inc., Russell or S&P Dow Jones Indices LLC. None of these companies make any representation regarding the advisability of investing in the Funds. With the exception of BlackRock Index Services, LLC, who is an affiliate, BlackRock Investments, LLC is not affiliated with the companies listed above.

Neither FTSE nor NAREIT makes any warranty regarding the FTSE NAREIT Equity REITS Index, FTSE NAREIT All Residential Capped Index or FTSE NAREIT All Mortgage Capped Index; all rights vest in NAREIT. Neither FTSE nor NAREIT makes any warranty regarding the FTSE EPRA/NAREIT Developed Real Estate ex-U.S. Index, FTSE EPRA/NAREIT Developed Europe Index or FTSE EPRA/NAREIT Global REIT Index; all rights vest in FTSE, NAREIT and EPRA."FTSE®" is a trademark of London Stock Exchange Group companies and is used by FTSE under license.

©2017 BlackRock, Inc. All rights reserved. BLACKROCK, BLACKROCK SOLUTIONS, BUILD ON BLACKROCK, ALADDIN, iSHARES, iBONDS, FACTORSELECT, iTHINKING, iSHARES CONNECT, FUND FRENZY, LIFEPATH, SO WHAT DO I DO WITH MY MONEY, INVESTING FOR A NEW WORLD, BUILT FOR THESE TIMES, the iShares Core Graphic, CoRI and the CoRI logo are registered and unregistered trademarks of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

251968

Read more commentaries by iShares