Passive Carnage Is Illogical

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe observe increased discussion about passive trends in indexing, whether a bubble has developed, and the future of active investing. There is always a desire to exploit predictable cyclical opportunities, yet it can be extremely difficult to forecast when active management should outperform. Below we discuss what is driving the passive rotation, as well as how strategies and products evolved to suit investors’ changing needs.

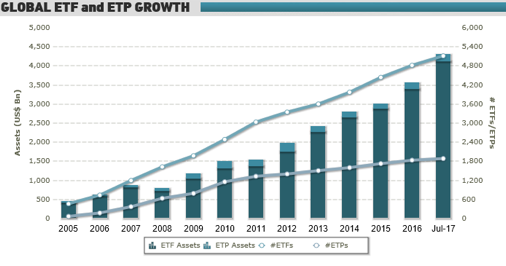

While ETF (exchange traded fund) flows since 2005 have been spectacular, mutual funds still hold $16.3 trillion or 83% of total U.S. listed fund assets. We don’t find arguments for a bubble very compelling, and will discuss why in greater detail below. Our belief in the theory of Rational Beliefs (vs. Rational Expectations) with relatively efficient markets supports that as long as a few good active managers exist with differing rational beliefs adapting over time, Passive Carnage Is Illogical.

Source: www.etfgi.com

Today there are over 2,025 U.S. ETF products with $2.8 trillion in assets. Growth in passive allocations has been impressive, but the ETF market has been dominated by iShares (Blackrock), Vanguard, and SPDRs (State Street) with about 70% market share of $4.1 trillion globally. This concentration is in part due to licensing of indices, which limits competition in primary benchmark indices like the S&P 500, MSCI EAFE, or the U.S. Aggregate Bond Index. This has driven higher acquisition valuations of index providers (i.e., Bloomberg-Barclays, FTSE-Russell), while Vanguard boldly partnered with CRSP to reduce licensing costs.

Source: ICI, 2017 Investment Company Factbook

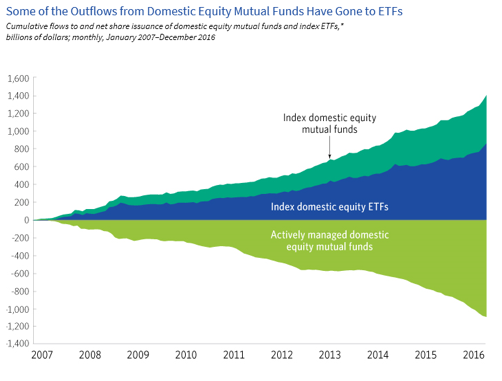

The chart above suggests passive investing is displacing active management, but it fails to tell the whole story. Mutual fund flows as a proxy for active management is misleading, while 25% of equity mutual funds are passively indexed (ref: ICI). Listed funds are only a portion of total market capitalization, ignoring separate accounts and security holdings of asset owners (pension, sovereign wealth and family office). Perceived decline in active management is likely exaggerated by narrow ICI fund flow measures.

Yet, there is no full accounting of flows into active portfolios of separately managed accounts (SMAs) or tactical ETF strategies, which expanded among wealth and financial advisors. Increased cost transparency, fiduciary governance, and competition are driving fee compression from ETFs to mutual funds.

Passive investing increasingly competes with active management. Competition between products and lack of growth or even outflows is causing investment companies to finally lower mutual fund fees and rationalize other costs. Retirement plan lawsuits and introduction of the Fiduciary Rule has increased visibility into complex mutual fund share classes, resulting in simplification and elimination of sales charges. Expense ratios are also beginning to decline. Adding an extra 25-50 bps to annual returns will improve manager success outperforming respective benchmarks, but also reduce profit margins.

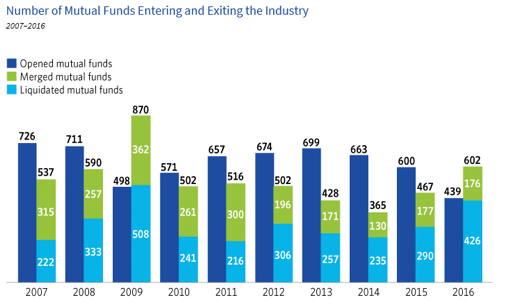

Source: ICI, 2017 Investment Company Factbook

The number of mutual funds declined for the first time since 2009. It was not surprising that mutual fund performance stumbled during the Financial Crisis, resulting in record fund closings and mergers (mostly stock funds, although credit-focused bond funds suffered too). 2016 may appear to be an anomaly, but the recent trend suggests a tipping point is apparent since 2014. Strong equity returns historically promoted new fund launches and positive fund flows, yet equity mutual fund flows were cumulatively negative since 2009. High fees and free market innovation (creative destruction) appear to finally urge active managers to begin rationalizing profit margins.

Several renowned managers have raised concerns that investors should fear a developing “passive bubble”. One even suggested that central planning of passive investing serfdom is lazy, un-American, or even Marxist, such as The Silent Road to Serfdom: Why Passive Investing Is Worse than Marxism by Bernstein. They suggest investors should increase exposure to active strategies. Anticipating bursting bubbles is difficult, but exceptional trends surely attract attention and may increase instability of markets.

A function of active management in a capitalist society intuitively seeks to efficiently allocate capital to the most compelling or attractive investment opportunities, but how does indexing actually impede such objectives---particularly free markets’ function of price discovery, except at an extreme (80-100%)? Social function is a higher standard than concern about price discovery (still good), liquidity (fine), volatility (low), and return correlation (falling). Concerns indexing may reinforce a “bubble machine” should be evaluated, but we don’t believe that passive trends can undermine fair and liquid price discovery of markets. Active management is key to efficient capital allocation and passive trends may be disruptive to business models, but free market forces remain resilient.

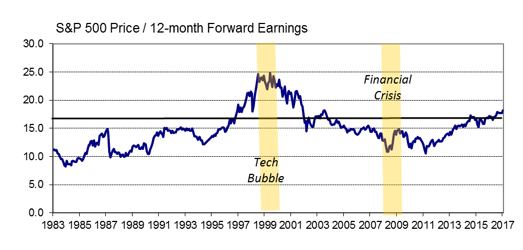

Equity valuations have increased as stocks rebounded from the Financial Crisis. The S&P 500 index has returned 346% rising toward 2500 since the 3/6/2009 intraday low of “666”. When strategists suggest the market is overvalued, investors know stocks had a remarkable run. They may not question uncommon or peculiar measures that look like a valuation ratio, but are problematic. Shareholders own a share of future cash flows, so appropriate measures must be relative to index-specific earnings, free cash flows, book value, or dividends. Considering the S&P 500 P/E below, valuation doesn’t look extended as earnings rose too. We are surprised one might infer that passive investing is dangerous to efficient markets.

Our S&P 500 valuation relative to interest rates still appears compelling as earnings grew in excess of GDP. Global equity valuations are not stretched in most other G-7 countries either, but lack of growth in Europe and Japan increase risk of a value trap. This is why we rely on multi-factor return forecasting in our asset allocation models. Unlike other equity declines, 2008’s recession was triggered by a credit crunch that caused earnings to collapse quickly, but then recovered. Focus on “peaking” charts of index total return or even S&P 500 earnings are inconsistent with history--earnings and stock prices have no upper bound, although earnings/price tends to mean revert. Price/GDP and Shiller’s CAPE (price vs. trailing 10-year earnings) are misleading “peaking” ratios with little value to forward looking investors, rather than justification for why passive investing is dangerous.

Our Global TAA equity valuation models across 15 countries suggest global equities are still inexpensive, as highlighted in Tailwinds and Creative Destruction (Q3/2017). We are more concerned about stretched bond valuations after years of explicit interest rate manipulation by the Federal Reserve and other central banks. Moral hazard has increased for individuals, businesses, and investors as emergency levels for interest rates must normalize and bloated balance sheet assets of bonds must run-off. We expect interest rates to rise at least another 2% across the yield curve as central banks begin unwinding bond holdings. We are more concerned about rising rates triggering a tipping point in global bonds, not equity ETFs.

There are two concerns we do have: (1) Index products underperform their benchmarks—absolutely. (2) ETFs are still susceptible to flash crashes (ref: May 2010, 2013 and 2015) or rapid and volatile price decline and recovery within a short time period, despite updated circuit breaker rules for exchanges. This may not affect long-term investors, but such volatility erodes market confidence. Index arbitrage that keeps index futures in lock-step hasn’t insulated ETFs from flash crashes. Traders know “fat-fingers” and rogue trading algorithms are part of our new reality, and ETFs are still as vulnerable as currencies and individual securities.

Exponential growth in ETFs also draws attention to concentrated overlap of common share ownership1, which may increase systemic market risk or induce specific risk in certain securities. If we desire efficient markets, divergent valuations resulting from increased indexing may seem to be a terrible thing, but if markets are relatively efficient in the long-run, does short-term mispricing cause harm or are they “spice of life”? Stocks added to indices may experience an anomaly of exceptional short-lived gains with increased demand for shares, unrelated to specific company news.

Even if assets of some ETF products might be limited, OTC derivatives can materially exceed nominal ETF exposure. Investment banks increasingly favor pricing off tradable securities, rather than indices. The dirty little secret is that these derivative products embed underlying ETF expense ratios, yet few buyers seem to be aware of this. While broad ETFs are relatively cheap, listed futures are less expensive to trade. However, more specialized exposures may depend on more expensive ETFs, such as sectors (i.e., industrials, financials, etc.), “smart” beta, or risk factors (i.e, value, momentum, credit, or size). Listed futures and options have exceeded trading volume in underlying securities of indices, such as the S&P 500, by 5X times or more historically. If we were worried about imbalances caused by ETF flows, we should be really concerned about derivatives based on ETFs. Any destabilizing threat of passive investing still seems a remote concern, but given leverage suggested above, it is worth monitoring across both equity and bond ETFs.

If indexed equity assets ever exceed 50% of market capitalization, active managers’ invisible hands might just stumble over each other to take advantage of market inefficiencies. In the meantime, liquidity seems to be enhanced as investors buy and sell ETFs daily. Until daily share volume declines, it is illogical for indexing to induce overvaluation or imbalances. Perma-bears seem to embrace coincidences that justify their opinion, but just don’t feed the bears!

Forces that cause certain stocks to become overvalued (or undervalued, by exclusion) increase dispersion of expected returns, thus expand opportunities to add value. We don’t believe that rotation from active to passive index and ETF strategies is likely to cause the equity market to become materially overvalued---that is simply illogical given active investors still dominate equity markets. Global multi-asset investors should quickly dispatch obvious market valuation disparities.

Three Big Disruptors: SMAs, Robos, and ETFs

It is not surprising FinTech investors are clamouring for companies providing portfolio aggregation data, risk analytics, performance attribution, thematic index construction and account management platforms. Nasdaq recently announced plans to acquire eVestment for $705 million reflecting the growing demand for SMA solutions. Simplistic focus on mutual fund and ETF flows may distract us from the critical trend of custom managed accounts and overstate the trend of active to passive investing.

Mutual fund holdings are also being displaced by portfolios of individual holdings, guided by SMA platform strategies. Some of these platforms are open and others are proprietary (single firm). These platforms provide model portfolios that fill style boxes, but often similar to existing mutual funds. Lower costs and access to tax optimization have encouraged advisors to increase allocations to SMA strategies. This is one of the most significant unappreciated trends in wealth management today.

ETF strategists also have leveraged SMA platforms to distribute their portfolio allocation advice---this is of particular interest to Strategic Frontier Management. Proliferation of indices, including alternative beta and risk factors, has enabled investors to broaden dimensions of strategic and tactical asset allocation with tracking ETFs. While the perception of ETFs is universally low cost, many specialized index trackers can be expensive and don’t have long track records to easily develop expectations for return, volatility, or correlation. Yet the strategists’ toolbox just got a lot larger and more capable for those with ability to utilize these indices in strategic and tactical allocations.

Growth of Robo-advised platforms has been another disruptor, which rely predominantly on indexed strategies. They also bolstered passive flows into ETFs and index funds, consistent with their low-cost focus. Growth in market share ignited a remarkable land rush for acquiring Robo-advisors in 2016. This year we observed greater activity in strategic partnerships.

We are concerned about the focus of bionic advice on technology, rather than being platforms hosting prudent advice. That sounds strange, but our analysis of their asset allocation methodologies suggest broadly a poor understanding of appropriate long-term expected return and risk measures, including volatility and correlation. Typical focus on 10-year horizons may seem sufficient, even responsive to evolving conditions, but can bias inputs due to monetary intervention and Financial Crisis related effects. Few seem to appreciate significance of rapidly evolving historical volatility, correlation, and return averages on optimal asset allocation at an inflection point in interest rates. Asset allocation committees rooted in recent history are prone to regency behavioral bias or “party effect”, as well as confirmation bias of group perceptions. These effects can undermine objective analysis of clearly the most important investment decision: Asset allocation.

Growth in ETFs may be assumed to be just a rotation into passive management, but the emergence of ETF strategists and highly specific nature of new ETFs suggest risk factor investing is coming of age. Alternative beta, smart beta, and thematic strategies wrapped as ETF products seek to add value by leveraging insights familiar to quantitative equity managers. These ETF products can be used to gain exposure, hedge risk, rebalance, or add value.

Many are concerned that the ETF industry is highly concentrated among three oligopolistic firms, but that is unlikely to change much given licensing primary benchmark indices remains limited to a small number of firms. Consumers should be concerned about concentration due to effects on pricing and potential systemic risk from a single firm. Yet, systemic risks of asset managers are very different than leverage concerns of “too big to fail” investment banks because fund shareholders hold fully collateralized (well, mostly except for leveraged ETFs) positions. Expense ratios remained higher for longer than without licensing barriers to entry, but price competition has now driven expense ratios lower in spite of manager concentration.

Active Management Cyclical, But Determinable?

We have long supported active management, but we believe that the portfolio decision to invest actively is a strategic allocation decision, not a determinable tactical decision. We would also suggest that forecasting when active management outperforms is a fools’ errand despite its cyclical nature---that is what we mean by determinable. Persistent large-cap dominance reminds us of another mega-cap period in 1998-2000. Are FAANGs the new .COMs? Our equity size (large-cap vs. small) model has over two decades of experience and we favor a small-cap tilt, but active vs. passive is a strategic decision and should not be driven by tactical views, such as a benefit from a small-cap tailwind.

Allocating to passive products are active decisions, just as which benchmark (or risk factor indices) is an active decision. Outperforming for the right reasons involves identifying managers with a well-defined and compelling philosophy implemented with consistency.

We offer the following key observations, in this regard:

· Periods favorable to active management vary by asset class (stocks vs. bonds), regions (countries still matter), investment styles (value-growth, large-small, credit), and tactical asset allocation (top-down) vs. security selection (bottom-up).

· Active headwinds of unequitized cash, small-cap equity bias, Emerging Market overweight, or credit tilt give an illusion that relative performance is more cyclical than related to unique investment styles.

· Equity selection tends to work when indices decline, but high cash exposures as equities rose were a headwind since the Financial Crisis. Consider that just 5% cash x 10% S&P 500 return = -0.5% drag at ~0% rates. Increasing active exposure because equites are expected decline is ill-advised.

· Active management decisions are strategic, and any suggestion is more compelling now is simply misleading. Since active returns are a fraction of total returns, significant portfolio re-allocation is required to materially exploit such opportunities.

· Performance attribution can reveal chronic tilts, which yielded outperformance for the wrong reasons and may not be repeatable. Persistent overweighting credit, longer bond duration, excess cash, or avoiding Japanese equities (1990s) produced excess return for the wrong reasons.

· Higher correlations between security returns tend to reduce opportunities to add value, whereas with falling correlations, we should expect potential excess return to increase. Unfortunately, we have found no explanatory factors that drive the cyclicality of correlations, other than they do tend to mean-revert. If correlations are exceptionally high, security correlations are more likely to fall.

· Manager selection skill might be as difficult as security selection, but also takes longer to prove value added given longer horizon of decisions---whereas portfolio managers are evaluated over a cycle, manager selectors are differentiated over several cycles. Furthermore, success in one category may not translate to other categories. This is a good reason to consider passive investing.

In the last decade, investors have become much more sophisticated and are increasingly aware of costs. ETFs based on primary core benchmarks are cheap, but after subtracting trading costs and management fees, they are guaranteed to underperform their respective indices without active enhancement or additional risk (ex: income from stock lending or option overwriting). So, if 30% of large-cap core equity mutual funds are passively managed, even if 50% of 70% active managers outperform, only 35% of all mutual funds would outperform their index. Thus, it should not be surprising that 100% - 35% = 65% of mutual funds underperform their benchmark. An active manager that just matches the benchmark must exceed the return of all passive strategies. Thus, if we can avoid really terrible or undisciplined managers, such as those with high cash levels or likely less viable after years of subpar performance, might we increase chances of selecting an outperforming manager?

Concluding Thoughts

We believe concern about rotation into passive investing and growth of ETFS is not a harbinger of market dysfunction, failing price discovery, reduced liquidity, or a new equity valuation bubble. Passive investing has a potential to cause distortions, but can it materially affect price discovery or market liquidity? It is mathematically illogical that passive flows in market capitalization proportions have much effect on econometric relationships. Breadth and liquidity of low cost ETFs have reduced total management costs and expanded the universe of tactical decisions to include many risk factors. We have noted our excitement about alternative beta and risk factors as new dimensions of strategic and tactical asset allocation.

Indexing tax efficiency (low turnover), fiduciary regulation, due diligence challenges, and chronic active fund underperformance are the most obvious reasons for rotation away from active management. Regulation, high management fees, transaction costs, cash drag, large-cap headwinds, persistent biases (credit, duration, country/sector avoidance, etc.), monetary intervention, and other policy risks probably have had a greater impact on markets than passive trends. Some portfolio management issues identified can be avoided with more discipline or risk management controls, but rotation from mutual funds to ETFs should continue.

Management fees and transaction costs are declining or being restructured. ETF expense ratios have been falling toward 0%, leaving Blackrock, Vanguard, Schwab, and State Street managing most ETF assets for a few basis points. Active management fees are also beginning to decline due to competition between managers, as well as because of lower passive costs. Wealth management also is experiencing margin pressure from increased competition, particularly disruptors such as Robo-advice platforms. In response, financial advisors are trading clients’ mutual fund holdings for lower cost SMAs and ETF-based tactical strategies, which provide greater opportunity for tax optimization. Wealth managers providing integrated financial planning or tax accounting are probably more insulated to increasing advisory cost pressures. While new regulation has increased operating costs, innovation has reduced trading and investment management costs, while increasing advisor efficiency.

Commodity funds, including gold, are the one area we have observed market dysfunction with financialization demand. European central banks have held on to excess reserves, even as the ECB has increased its holdings. Bank of China also accumulated over 500 tonnes of gold since 2003. Barrick Gold has reported all-in sustaining cost of $772/ounce, so what supports gold at $1300 vs. our fair estimate of $1000? The lesson here is that narrow ETFs can have an adverse or destabilizing impact on market prices if ETF demand exceeds underlying demand of securities.

The global economy has finally awakened from its slumber like Rip van Winkle. We should expect growth to be more resilient and inflation more volatile, as differences between countries, sectors, and risk factors increase in importance. International diversification improved even as Jack Bogle condemned owning international stocks, suggesting that U.S. multinationals generate more than 50% of S&P 500 revenues, so additional international complexity is not needed. We choose not limit our investment universe and observe that countries still matter in global returns.

Investors should be reminded of the still remarkable benefits of international country and currency diversification. After the U.S. dollar appreciated from 2012-2016 and Emerging Market darlings struggled in 2016, it is not surprising some investors might be sympathetic to dumping their international exposure. No sooner than investors thought the S&P 500 looked invincible, the U.S. dollar moderated in 2017 and currency headwinds turned into international tailwinds.

Strategic Insights This publication is for general information only and is not intended to provide specific advice to any individual. Some information provided herein was obtained from third party sources deemed to be reliable. We make no representations or warranties with respect to the timeliness, accuracy, or completeness of this publication, and bear no liability for any loss arising from its use. All forward looking information and forecasts contained in this publication, unless otherwise noted, are the opinion of this author, and future market movements may differ from expectations. Index performance or any index related data is provided for illustrative purposes only and is not indicative of the performance of any portfolio. Any performance shown herein is no guarantee of future results. Investment returns will fluctuate, and the value of holdings may be worth more or less than original cost. © Strategic Frontier Management (www.StrategicCAPM.com). 2017. All rights reserved.

1 Some may draw an analogy to the 2007 Quant Quake, assumed to be a consequence of overlapping holdings, when indeed it was minimizing of common (BARRA) risk factors being liquidated by a run on quantitative equity funds, exacerbated by hedge fund redemptions and proprietary trading exploitation. Insider trading trip wires would have raised red flags if indeed it was security overlap. Credit market illiquidity following Bear Stearns default limited access to redeeming credit hedge funds--- asset owners and fund-of-funds concentrated redemptions on quantitative equity hedge funds with greater liquidity.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All