With the FOMC decision behind us and a moderate data calendar, the financial world will be focused on Washington. Expect people to be asking:

Has the time come for tax reform?

Last Week Recap

My expectation for last week was partly correct. The focus was certainly on the Fed, but the market reacted quite calmly.

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short via Jill Mislinski. There was little change on the week, and little change during the week. The range was only 50 bps even during the Wednesday Fed announcement.

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read the entire post for several more charts providing long-term perspective, including the size and frequency of drawdowns.

Personal Note

My plans changed, so I was able to write today. I’ll get a weekend off soon!

The Silver Bullet

As I indicated recently I am moving the Silver Bullet award to a standalone feature, rather than an item in WTWA. I hope that readers and past winners, listed here, will help me in giving special recognition to those who help to keep data honest. As always, nominations are welcome!

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The economic news remained quite positive.

The Good

-

Fed decision led to little market reaction. I am scoring this as “good” because no one expected a statement that was friendly for stocks. The actual announcement was a bit more hawkish than most expected, but the market reaction was muted. Perhaps the Fed obsession will take a back seat and we can focus on earnings. Scott Grannis calls the decision “cautious and correct.” Eddy Elfenbein is a bit less sanguine.

-

Corporate earnings outlook is even better. FactSet reports that “a record number of S&P companies have issued positive revenue guidance for Q3”. Information Technology, Health Care, and Consumer Discretionary have been especially strong.

-

Leading indicators increased 0.4% up from 0.3% in July. (Conference Board).

-

Trucking continues to improve. Steven Hansen (GEI) explains why we should emphasize the CASS index and notes that the improvement remains “moderate.”

-

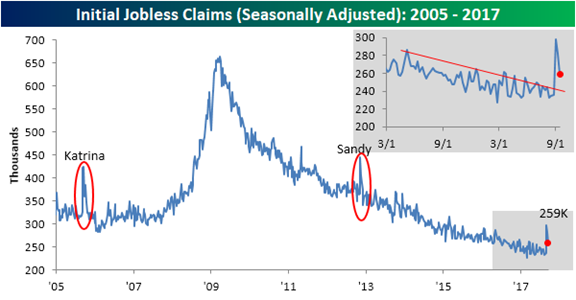

Jobless claims had a surprising decline in the face of hurricane effects. Will it continue? Bespoke has the story and one of their great charts.

-

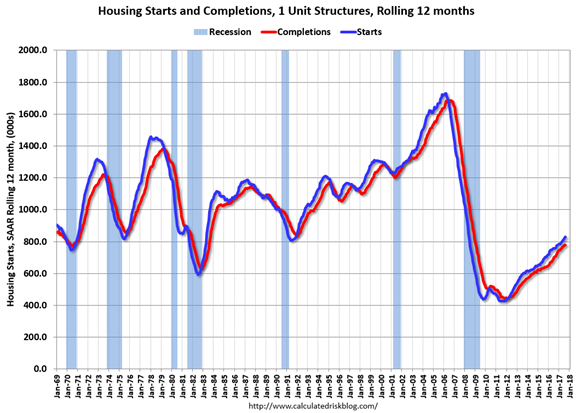

Housing starts and building permits beat expectations. Calculated Risk notes that the 0.8% decline compared to an upwardly revised July actually beat expectations. He has correctly forecast and monitored the shift from multi-family to single-family starts, concluding “now I expect a few years of increasing single family starts and completions. Permits beat expectations with a 1.3 million rate. Contra – New Deal Democrat notesthat we have not yet seen the hurricane effect.

Bespoke’s take on permits:

The Bad

-

Existing home sales declined 1.7% in August. Calculated Risk is not very concerned, citing low inventory. He does note that hurricane effects are still to come.

-

Escalation in the war of words with “Rocket Man,” “dotard,” and aggressive threats. A key to the story is the situation of South Korea. Brookings has a great background article by Kathy Moon, a Senior Fellow and Professor at Wellesley.

For the United States, a nuclear armed North Korea undercuts its security and traditional policy objectives, such as nonproliferation, and destabilizes the East Asia region. But for South Korea, it is an existential threat. Given the high tensions of late, Seoul fears being dragged into a war or, at the very least, falling victim to limited military exchanges between Washington and Pyongyang.

-

Rail traffic declined. This is especially true when using Steven Hansen’s“intuitive sectors” which remove coal and grain from the analysis.

-

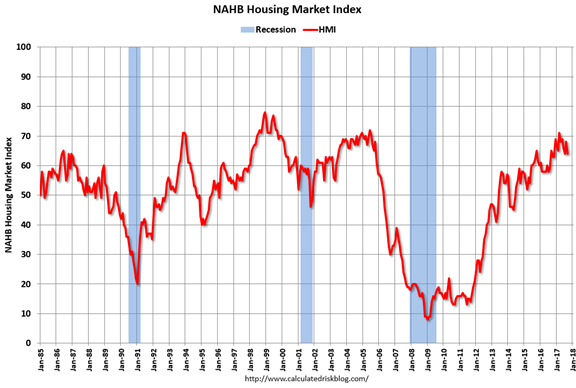

Builder confidence decreased to 64 from a revised 67 in August. Calculated Risk notes that this is “a solid reading.” Mortgage applications were also down 9.7% from the week before.

-

Mortgage delinquencies are 0.7% higher. This is especially true in the hurricane-affected areas. (Calculated Risk)

The Ugly

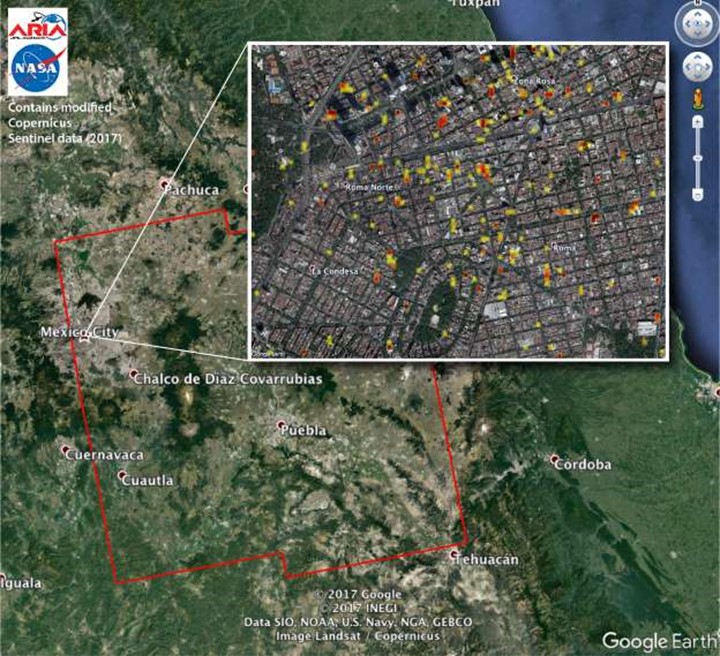

Earthquakes in Mexico, Hurricane Maria – Mother Nature keeps bringing new challenges. The cooperation of people in the affected areas, and the tireless work to find and help survivors, is an inspiration. Meanwhile, the advanced technology helps to find the important affected areas.

Noteworthy

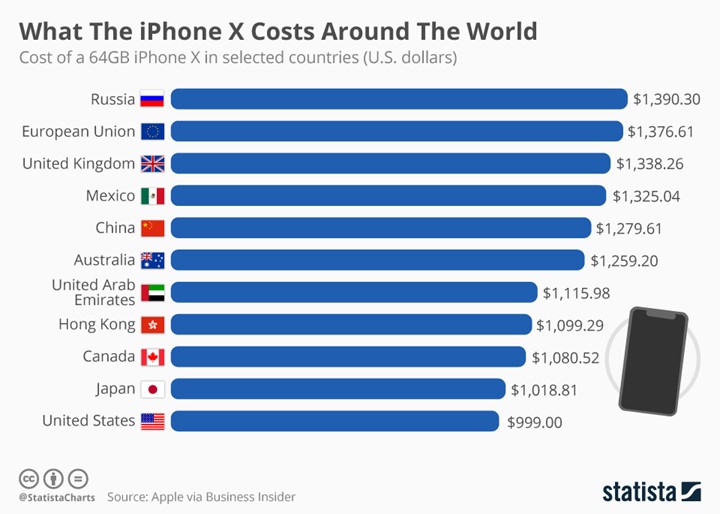

It is often a challenge to imagine ordinary life around the world, even if you are a frequent traveler. Sometimes the comparative price of a commonly purchased item is helpful. Statista looks at the iPhone X.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

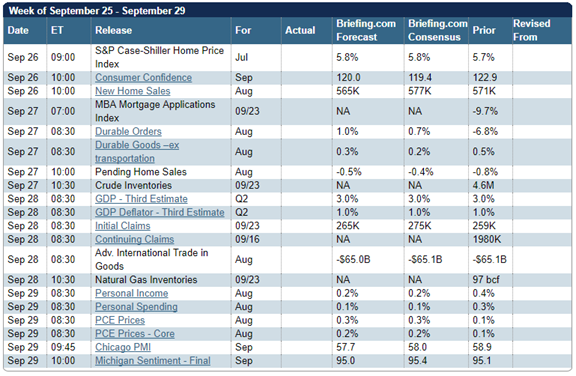

We have a normal economic calendar. Most important are personal income and spending. New home sales and the consumer confidence data will be interesting. There are plenty of Fed participants on the rubber chicken circuit. The GOP tax proposal will take center stage.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

Much of the attention to Congressional action this year has been a waiting game. The key market issues relate to trade, tax reform, and infrastructure spending. These are now coming to the fore. If the GOP is to pass legislation with a simple majority in the Senate, it must be done as part of the “reconciliation” process. That opportunity ends this week.

Breaking news suggests that the “Big Six” group of Republicans has reached agreement on a proposal. This will have everyone wondering:

Is it time for tax reform?

The expected proposal includes tax benefits for top-bracket individuals and large corporations. There are also some breaks for the middle class and elements of simplification. President Trump is expected to announce the outline on Wednesday.

The key viewpoints will be clearer after details are known, but here is the general outline:

- Support from those seeking tax relief for top brackets and business, which they view as economic stimulus;

- Opposition from the deficit hawks, who will not see this as revenue neutral;

- Opposition from some businesses, who will perceive a competitive disadvantage;

- Opposition from Democrats, who will argue that it tilts toward high-income taxpayers.

The time frame does not permit much time for specific coalitions to form. As usual, I’ll have more in the Final Thought, where I always emphasize my own conclusions.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

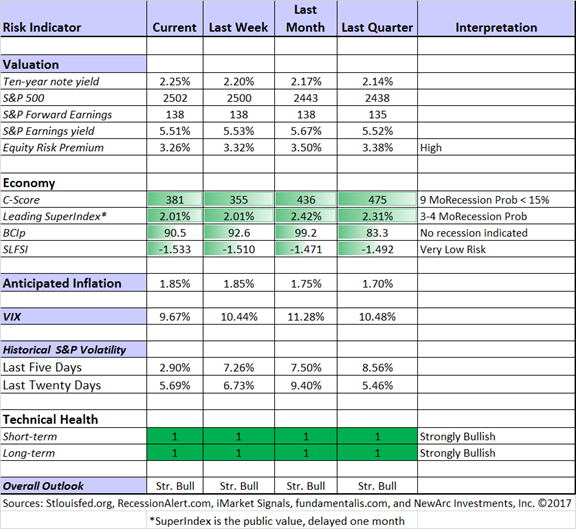

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

Notes on changes:

We have added a distinction between the technical appeal of the market on a short-term (two months or so) and a long-term basis. The mildly bearish interpretation for last week did not imply a full exit from trading. It was a warning that conditions are not as attractive. As you will see, this indicator can move fairly rapidly.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Georg Vrba: Business cycle indicator and market timing tools. It is a good time to show the chart with the business cycle indicator.

Doug Short: Regular updating of an array of indicators. Great charts and analysis.

Featured Guest Sources

Earnings expert Brian Gilmartin compares forward earnings estimates with the actual results. His conclusion will be surprising to many (but not to regular WTWA readers).

The forward estimate does a pretty good job of estimating SP 500 in what might be considered “normal” years. For instance, in late 2007, the forward estimate for 2008 was looking for roughly $100 in EPS, and the actual 2008 EPS was closer to $65. Another example might be 2015: in late 2014, the SP 500 forward estimate was looking for $122 in SP 500 EPS and the final was $118.78 thanks to the collapse in crude oil, the strength of the dollar and the China yuan devaluation that occurred in late summer, 2015.

Still those events only cost the SP 500 approximately $5 in EPS in 2015, which tells you what a tremendous shock the Financial Crisis was to SP 500 to cause a decline of roughly 35% from “estimated-to-actual” SP 500 EPS.

Brian’s work explains an inconsistency in the conventional wisdom about forward earnings. First, that analysts are too optimistic. Second that companies have a high “beat rate” because of low estimates.

At some point in the process of reducing estimates, the indication must be pretty good.

Dr. Ed Yardeni rebuts the latest scary story from Dr. Shiller. He describes several other valuation indicators that are regularly ignored. It is worth a read, if only to understand the varying perspectives. It is also quite consistent with Brian Gilmartin’s work.

Insight for Traders

We have not quit our discussion of trading ideas. The weekly Stock Exchange column is bigger and better than ever. We combine links to trading articles, topical themes, and ideas from our trading models. This week’s post showed how model-driven trades worked despite the popularly-cited worries. Blue Harbinger has taken the lead role on this post, using information from me and from the models. He is doing a great job.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility!

Best of the Week

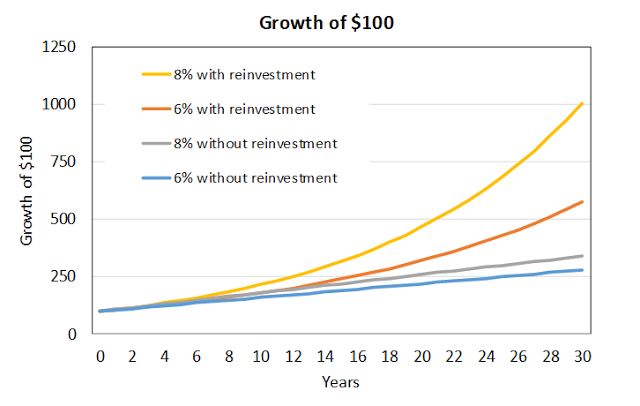

If I had to pick a single most important source for investors to read this week it would be Econompicdata’s look at compounding. This basic principle should be familiar to all investors, yet many forget the importance. The post concludes with practical advice, including minimizing taxes. Here is one of the charts.

Stock Ideas

Cardinal Health (CAH) is a dividend aristocrat trading near its all-time high yield. Simply Safe Dividends takes a closer look. I like this choice, but we have written short-term calls against the stock to enhance yield. We do this on solid choices where there is not explosive upside.

The Barron’s cover has an interesting Andrew Bary story on gene therapy, with explanations that will make sense to the average financial reader. The stocks are still very speculative, highly dependent on FDA decisions. Check out the story for a list of names.

Permian basin stocks? These are worth a look, especially if you think oil prices have bottomed. (Lee Jackson, 24/7 Wall St.).

Digital Realty Trust? (DLR) Simply Safe Dividends does a thorough review. Everything looks good except the valuation. That makes it worth watching in case there is a dip. (This is one we owned, but sold for valuation reasons).

Brian Gilmartin takes his normal careful look at Bed, Bath, & Beyond (BBBY). He raises some questions before their report and then writes a nice recap.

Bank stocks? WSJ’s MoneyBeat highlights the recent strength. My own take is that the regional banks (which we sold a few months ago) are still way too expensive, but some of the money center banks are closer to our buy range.

Personal Finance

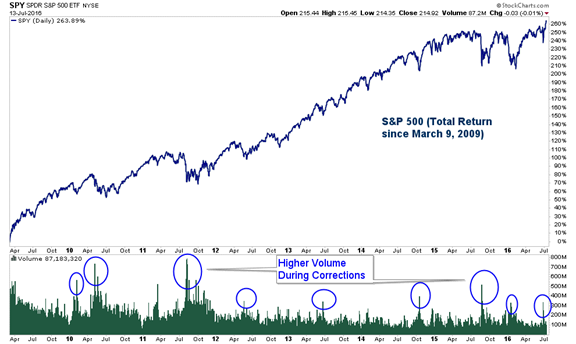

Seeking Alpha Senior Editor Gil Weinreich has an interesting topic every day. His own commentary adds insight and ties together key current articles. As usual this week he had several good posts, but I especially liked his “ignorance is bliss” column. He highlights Charlie Bilello’s lookat market history since 2009. Gil focuses on the implied definition of “evidence.” He agrees with Bilello that emotions should be put aside. That still leaves one to consider what sort of evidence to use.

He has a compendium of market worries in that time frame, including the repeated assertion that the “easy money has already been made.” Chart lovers will find plenty to study. Here he analyzes the popular claim that volume declines are bearish.

The Fear and Greed trader has a similar review as a backdrop for his current conclusions.

Watch out for….

Market timing. Another analysis of the futility of this approach. (For comparison, we are trying to help people with risk-timing. We reduce risk when necessary, even though it is probably not the market top).

REITs on the edge. Brad Thomas explains how to analyze a REIT at a “tipping point.”

REITs with “excessive” yield. Marc Gerstein suggests a method that screens out the most dangerous candidates – well worth a look. He provides his current list, while warning that it changes frequently.

ETFs? Simply Safe Dividends raises the question of whether it is better to buy your own portfolio or to choose an ETF. He concludes that the decision is often one of personal convenience. The main drawback?

The main drawbacks to owning ETFs over individual stocks are that you are stuck with whatever dividend yield they offer (which is often too low for investors needing income today), their income streams can be riskier because they own good and bad quality businesses, and they can lack reasonable diversification depending on how they are constructed.

All of these factors can be a bigger deal for dividend investors than simply comparing total return potential of different ETFs and hand-picked dividend portfolios.

Final Thoughts

Most people including the thought leaders in financial media, watch political events with a rooting interest. Having strong opinions is fine. Discussing them with friends and using them for voting are also fine.

Mixing your politics with your investing is a not fine. It is a serious mistake.

Thinking strictly in terms of your role as an investor, what do you want from Washington? Probably the following:

- Stronger economic growth

- Tax reform

- Better infrastructure

- Avoiding surprises and shocks

What is the best way to achieve these goals?

Compromise. Many years of gridlock have thwarted any progress on these fronts. You can monitor various measures of Congressional progress (or lack thereof) at the Bipartisan Policy Center. You will find plenty of data and charts – not just opinions.

The potential for compromise has increased dramatically in the past few weeks. There is no imminent threat to government funding. The ObamaCare repeal failure illustrates the need for bipartisan efforts on health care. It probably sets the pattern for tax and spending issues as well. This will be a very interesting week. There is real potential to form more lasting bipartisan alliances.

What worries me…

- An “accident” involving North Korea. Intentional action is mostly belligerent rhetoric.

- Strident positions that waste the chance for some meaningful compromise.

…and what doesn’t

- Market valuation. Growing earnings and a healthy economy have provided support for current stock prices. See Dr. Ed above, in the quant section.

- The Fed. As I expected, this has proven to be a benign and gentle policy shift.

© NewArc Investments, Inc.

Read more commentaries by NewArc Investments, Inc.