Summary: The major US indices all recorded new all-time highs (ATH) this week. The very broad NYSE, covering 2800 stocks, also made a new ATH, suggesting the rally is supported by adequate breadth. Longer-term studies and the fundamental macro data continue to indicate that further upside into year-end is odds-on. Remarkably, a new survey shows that fund managers are the most underweight US equities in 10 years, despite the SPX rising 9 of the last 10 months by an impressive 17%.

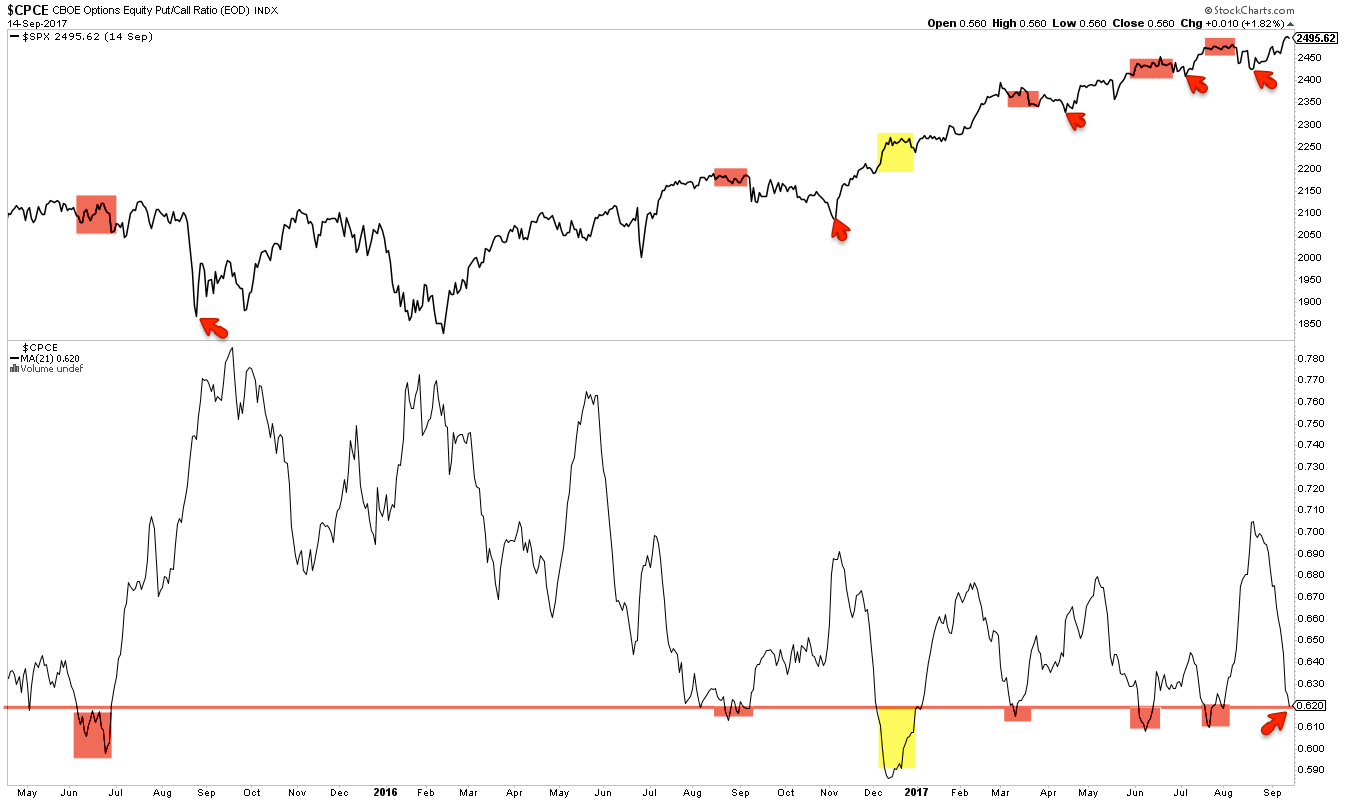

On a short-term basis, there are several reasons to be on alert for weakness over the next week or two. An important FOMC meeting is on deck for Wednesday.

US equities remain in a long term uptrend. SPX, DJIA, NYSE, COMPQ and NDX all made new all-time highs (ATH) this week.

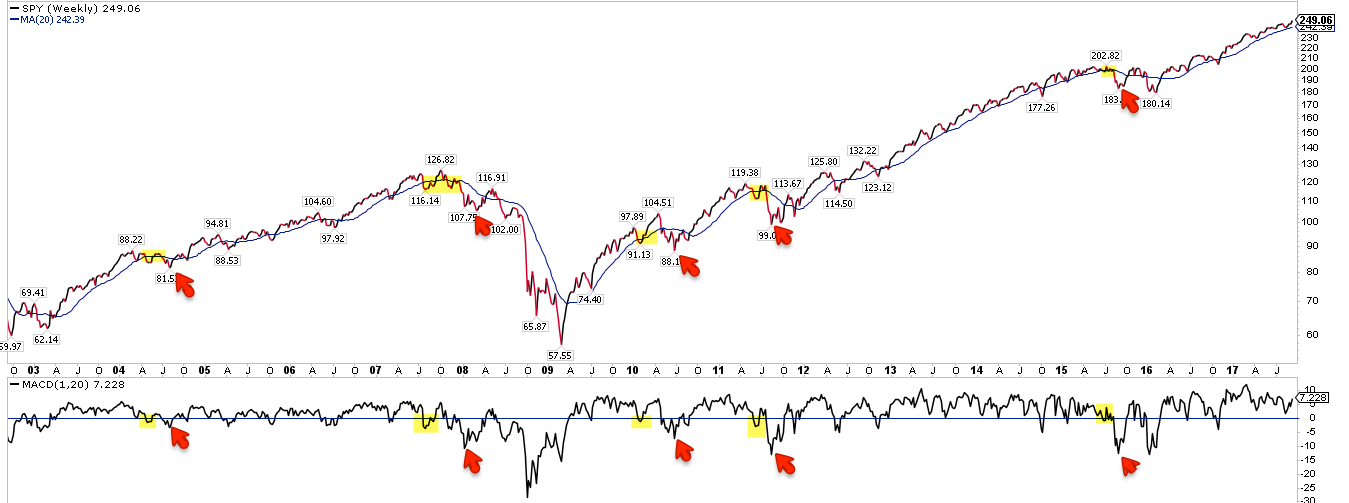

Long-term uptrends typically weaken before they reverse strongly. Note the bottom panel: the 20-wma will flatten in advance of a significant correction to price (yellow shading). This process has not started yet. That doesn't mean that an intermediate-term fall of 5-8% is unlikely; in fact, a correction by that amount is common in most years. But any such fall is likely to followed by a rebound to the prior highs before a more siginificant correction ensues.

Throughout 2017, we have presented the historical tendency for years with a strong trend, like this one, to rise further (see here, here, here and here). We can add to these the following data: when SPX rises 5 months in a row, as did through August, the index has closed higher after 6 or 12 months every time. The average maximum drawdown during the next year has been a very modest 4% (from @SJD10304).

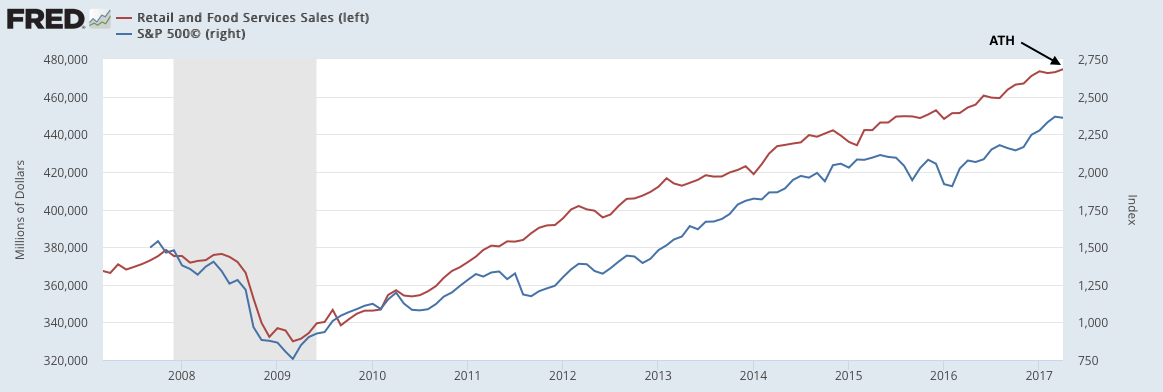

That conclusion is consistent with the fundamental data. Real retail sales reached a new ATH in July with growth approaching 2%. Employment has slowed in the past year, but an average of 175,000 new jobs are still being added each month and unemployment claims continue to fall. On balance, the risk of an imminent recession is minor. This is important as there have been 10 bear markets since the end of World War II but only 2 have occurred outside of an economic recession. A review of the most recent macro data can be found here.

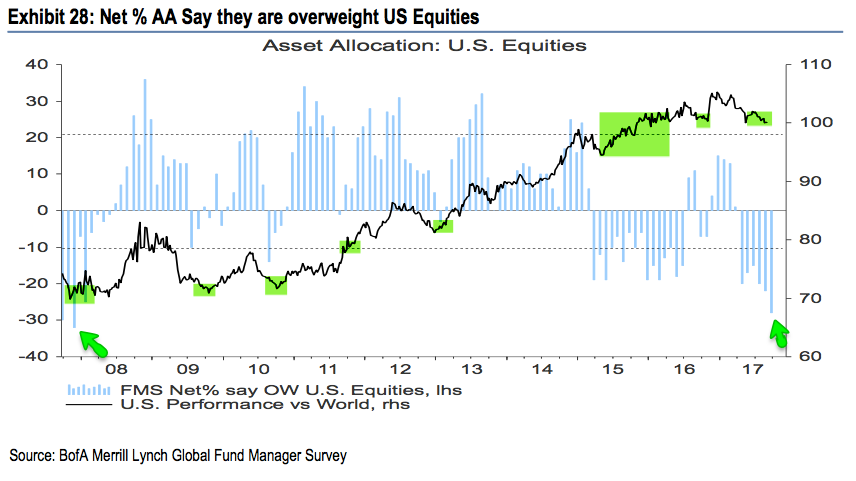

Continued gains in equities is also supported by longer-term measures of sentiment. Investment fund managers surveyed by BAML this month reported relatively high allocations to cash and modest allocations to equities. This combination is consistent with further upside in equity prices. For example, funds hold nearly 5% cash; prior to the 2008 bear market and significant corrections in 2010 and 2011, cash allocations were 3.5% or less. Read a new post on this here.