Robo advice is the newest disruptor in the financial industry and many advisors are not sure how to interpret this new investment advice solution. Some are writing it off as a solution for lower asset customers, some are concerned about the competitive threat, while others are embracing the technology for use in their own business. Regardless of perspective, the technology, introduced by start-ups like Betterment and Wealthfront, is achieving widespread adoption at financial service providers as either stand-alone solutions or in conjunction with more traditional advisory services.

Starting early in the evolution of these investment products, BackEnd Benchmarking opened and funded accounts at the most prominent robo advisors in order to collect unbiased data. There has been no data previously available to advisors on the performance or portfolios of robo advisors, which is why BackEnd Benchmarking created The Robo Report detailing this and more in-depth analysis that can be found at TheRoboReport.com.

The largest legacy players in the financial industry are embracing this technology and are exposing their many customers and the general public to robo advice options. The result will be significant growth in the market for digital investing solutions across the entire industry. The questions are, how will this affect traditional advisory businesses and what is the best response strategy.

Firms are taking note of the large volume of assets flowing into these platforms. They may also want to note that the assets are flowing disproportionately to the largest most established players. Vanguard’s Personal Advisory Service product recently announced $83 billion in AUM, which represents staggering growth of around $5 billion a month. The level of asset inflows is attracting competition, but for the time being, Vanguard’s product is an unrivaled success. The next two most successful robos, judged by assets under management, are Schwab and Betterment, with $14.9 billion and $10 billion, respectively. Assets are concentrating in the top few providers, while legacy players with deep pockets and large existing customer bases continue to enter the market.

We believe there are three major takeaways from this trend:

· First, independent robos are facing rapidly increasing competition from established financial institutions introducing robo products. This will likely lead to consolidation within independent robos. We believe only a few of the largest independent robos will achieve sufficient economies of scale to survive as independent companies in the long term.

· Second, investors will become more familiar with the solutions as more firms offer and promote them. A robo advice solution is increasingly becoming another standard offering at the major players in the advice market.

· Third, this will add to the larger trend of pricing pressure on financial advice providers. We do not believe robo advice will replace traditional advice, but traditional advisors must be prepared to defend their value propositions in the face of low-cost automated alternatives.

Currently, the robo advice industry is experiencing rapid introduction of new offerings. Here is a short list of just some of the new offerings: TIAA-CREF and Merrill Lynch both launched products early in the year. Zacks and T-Rowe price unveiled robos this spring. Morgan Stanley and Wells Fargo have said they hope to launch a robo advice solution later this year. Ally Financial integrated last year’s purchase of TradeKing, rebranding their product to Ally. Goldman Sachs is also rumored to be working on a robo advice solution.

The advice market is also seeing robo technology being implemented in more traditional firms. Some advisors are concerned about competition from within their own firms. Merrill Lynch and Morgan Stanley advisors are questioning whether or not robo technology will be a tool to help them provide better service to more clients, or if robo solutions will be competing with them for clients.

Firms have an eye on helping their advisors be more efficient, provide better service, and expand their markets. For example, some investors do not want or feel they need a dedicated live advisor and prefer a bare bones low cost solution. Equally important, many advisors have investment minimums and cannot profitably service clients below a certain asset threshold. Robo advice technology can help both clients and advisors by providing solutions that expand an advisor’s traditional client base.

This opportunity is not limited to large institutions that have the capacity to build, or acquire through M&A, a robo solution. Smaller firms can join robo platforms that allow the technology to be white labeled specifically to their firm. Depending on the solution, they can also maintain control over asset allocation and investment selections. Betterment and Schwab both have institutional offerings that lower the barrier to entry for firms. Another early player in the marketplace, Jemstep, has no direct to consumer robo, but instead allows firms to leverage their technology to quickly implement a robo solution.

There is good news for smaller advisors who are considering adding a robo solution. It appears many consumers like robo solutions, but they may not be ready to give up on traditional live advice. Many of the earliest robos focused on platforms that eliminated person-to-person advice, but now the trend is adding in options to connect to live advisors. Betterment recently added an option for access to live advisors following Schwab announcing the addition of a hybrid product late last year. Meanwhile, Vanguard’s popularity may be, in part, due to their hands-on approach, which always involves live planners.

Existing robo advisors are trying to differentiate their platforms mostly on services and not performance. Very few robo advisors publish returns and almost no advisors are employing active management strategies. They are focusing on other ways to add value. Smart tax investing, rebalancing, and financial planning features are more commonly touted than a portfolio that will beat the market.

Most robo advisors seem to, or explicitly, state their investment selection process is based in modern portfolio theory. This would lead one to believe that the portfolios would be similar across providers in the types and weights of assets held. This is not the case. Some portfolios have international equity allocations as low as 20% of total equities, while others have international holdings that make up more than half of the equity portion of the portfolio. Within fixed income, some portfolios hold all municipal bonds while others hold none, some rely heavily on corporates, while others rely heavily on treasuries. The same risk profile at one robo may produce a surprisingly different portfolio at another.

Although most robo advisors focus on value-added service and not performance, we believe performance and risk management are important. For the most part, performance is impossible for potential customers to evaluate on their own. We provide a look inside portfolios at each robo advisor, alongside analysis to help advisors and investors make informed decisions.

Highlights from our Q2 2017 Report:

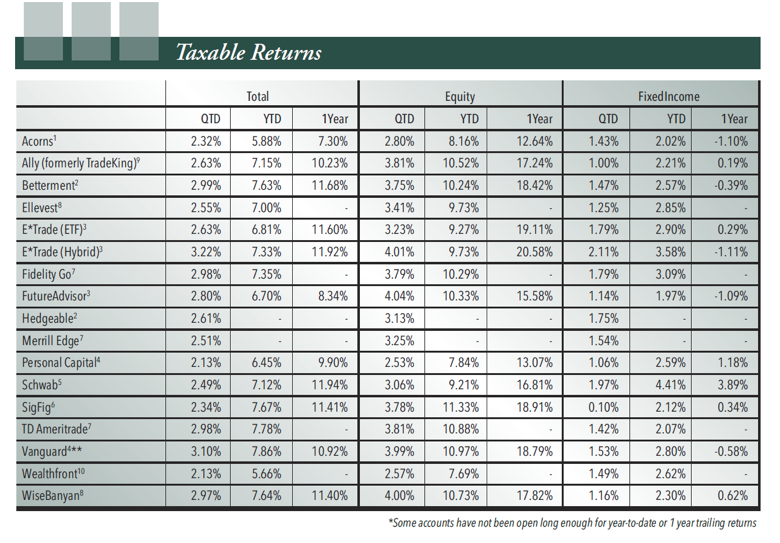

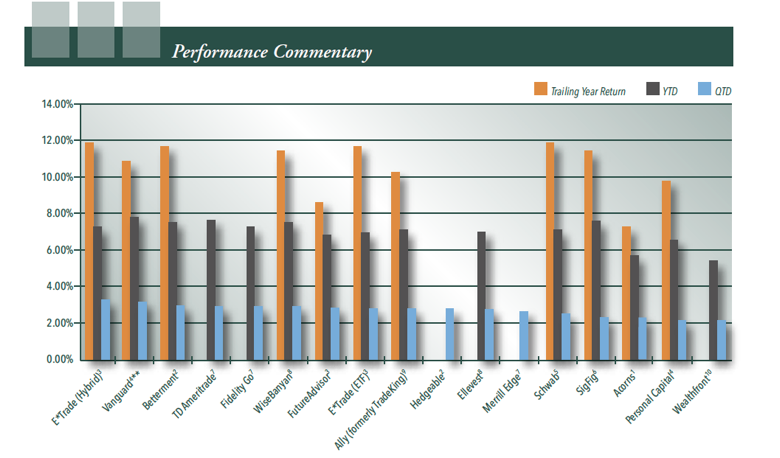

Figure 1 shows the performance results of the portfolios. Performance is broken down by equity, fixed income, and total performance over three different time periods. Here advisors can easily compare how different robo advisory services are performing. All returns are net of fees. A full set of disclosures, including specifics on net of fee return calculations for the different portfolios can be found in the full report at theroboreport.com. All results are as of 06/30/2017.

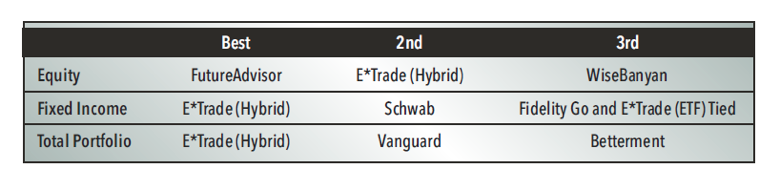

Figure 2 highlights the best performance in equity, fixed income, and the total portfolio for the quarter. Quarterly results can vary significantly, and as time passes it will be easier to use our data to identify long-term trends and see how the different portfolios perform in a bear market. The returns for the quarter ranged between 3.22% and 2.13% in our taxable accounts and 3.88% and 2.71% in our IRA accounts.

Figure 3 shows performance across the taxable portfolios. Performance is net of fees. Portfolios missing the year-to-date or trailing-year return have not been open long enough to have these data points. All results are as of 06/30/2017.

There are many robo options available to advisors and their clients. While not a good fit for everyone, we are confident that robo advice is here to stay. Investors need to select the correct balance of services, fees, risk, and performance to choose the best advisory solution. Meanwhile, advisors need to focus on their own value proposition and what value they can add that an automated solution will have difficulty replicating.

We believe transparency is paramount to advisors and investors making an informed decision. More details of performance, specific portfolios and allocations can be found in our new report for free at The Robo Report.

© The Robo Report

Read more commentaries by BackEnd Benchmarking