Global markets have been relatively calm this summer despite many uncertainties. Geopolitical risks have continued across the globe, and in some areas, looming monetary policy changes also appear likely. A key question for many investors is whether the sleepy summer period of low volatility will give way to a more turbulent autumn. Franklin Templeton’s senior investment leaders offer their perspective on the markets and discuss where they see opportunities and risks ahead.

Unwinding Quantitative Easing (QE)—Will it Unwind the Markets?

Q: Central banks have remained a focus of global markets. Can you give us an update on what different central banks around the world are telegraphing?

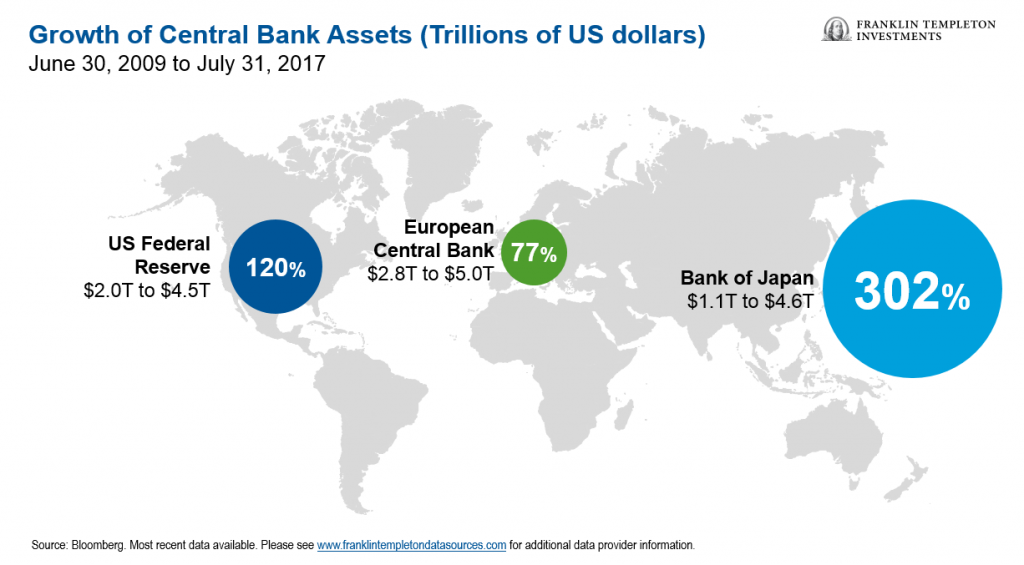

Michael Hasenstab: There has been a lot of focus on the speed and extent of interest-rate hikes out of the US Federal Reserve (Fed), but I think there hasn’t been enough focus on what happens when the central bank starts to unwind its balance sheet. I think the United States will be the first central bank to unwind, with Europe following suit at some point. Japan isn’t really in a position yet to be unwinding though, in my view. Even if the Bank of Japan stops QE, I believe it will still target the 10-year yield to keep it close to zero.

There is a concern that the Fed has never unwound such a large amount of assets before, and the likelihood that there are no disruptions is theoretically possible, but seems pretty unlikely in practice. We have to be ready for that. And, it’s not just what the Fed is doing in terms of its balance sheet that is important. We have a lot of deregulation happening, and there could be fiscal spending coming as well. It’s a pretty complicated US landscape.

Christopher Molumphy: To Michael’s point, central bankers have quite a task ahead of them. The Fed started with a balance sheet of less than $1 trillion, and now it’s up to $4.5 trillion, so it has some work to do to unwind it. I think the Fed has done a reasonably good job recently of trying to telegraph its intentions. But as Michael noted, it’s a big action in front of us, and there are a lot of things that could go wrong.

Ed Perks: I think another thing that’s relevant is the possible transition we could see at the Fed. Fed Chair Janet Yellen’s term is scheduled to end early in 2018, so I think the markets will increasingly be focused on the Fed’s potential path under new leadership if it seems likely she won’t continue on.

Christopher Molumphy: While Yellen isn’t totally out of the running for a second term, at this point, it seems likely that there could be a new Fed chair. When we think about monetary policy going forward, the impact of that transition is a question mark. As Ed pointed out, we are in the later innings of Yellen’s term, so we will need to see some transition communications sooner rather than later.

Michael Hasenstab: In my view, it might be a good thing to have someone from the market side at the Fed’s helm. But back to US monetary policy and the implications, I think it’s pretty simple. I believe interest rates need to go higher. The United States now has full employment, economic growth is at or above potential and the output gap has closed. Inflation has not come into the picture yet, but it’s probably just a matter of time as it’s a lagging indicator. All of these factors point to a 10-year US Treasury yield that should be higher than 2%.

Q: How should investors think about opportunities that are being created or potentially disappearing?

Chris Molumphy: We have a more intermediate- to longer-term investment horizon, so we try to stay long-term focused. With that, we are trying to take advantage of some of the shorter-term volatility where it creates potential buying opportunities. We have a reasonably constructive view on the economy globally and on the United States in particular. The US economy has been growing at about 2% annually, which isn’t a great rate of growth, but it’s decent from the perspective of a fixed-income investor. At least over the near term, we see a reasonably constructive corporate environment, and the consumer appears to be in decent shape, too. Our focus has been on asset classes such as corporate credit. We are still reasonably constructive on corporates, as well as mortgage-backed securities, but are staying diversified because we do not see a lot of cheap sectors in the fixed income markets right now. That said, we’re willing to take some reasonable level of risk because we think the fundamentals will remain fairly strong in the near-to-intermediate term.

Michael Hasenstab: If the Fed moves first and interest rates in the United States start to normalize, then higher US rates combined with stable rates in Japan or Europe should lead to a stronger US dollar, at least temporarily. And we think there are a lot of headwinds for the euro and yen beyond just interest rates. The situation will probably be a little different against emerging markets because many of those countries have a huge yield advantage over the United States. Some countries which have very low bond yields might be more vulnerable to a US rate hike. So I think we will see greater bifurcation in emerging-market currencies.

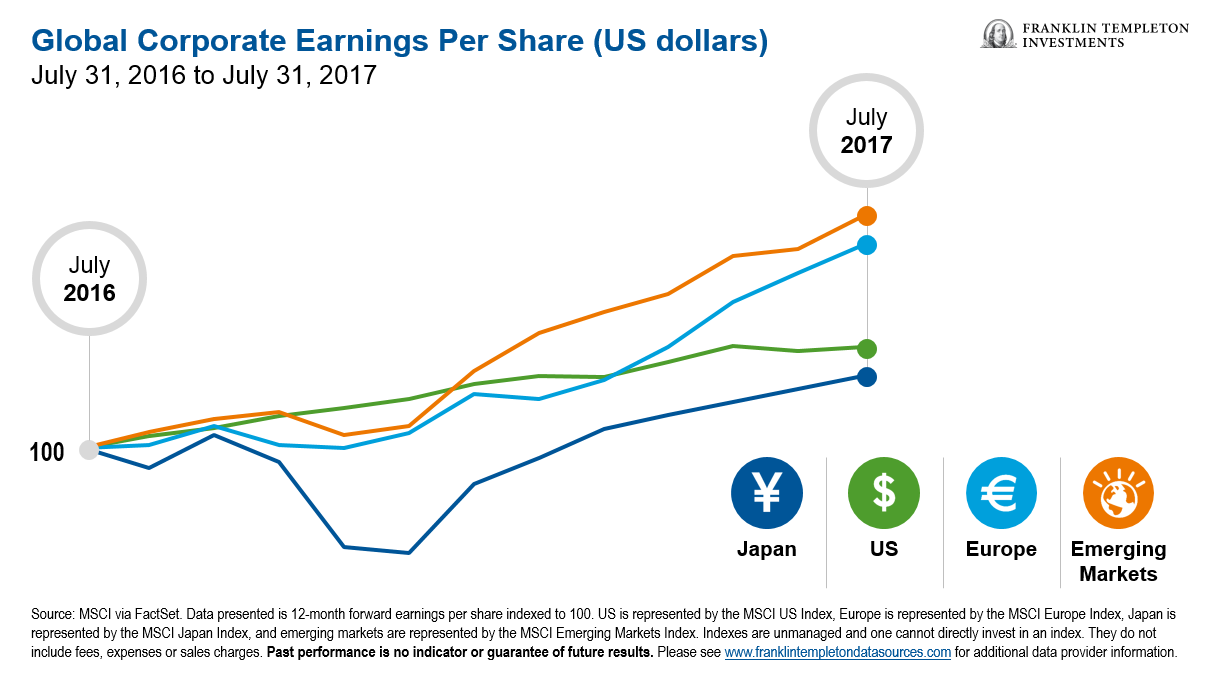

Stephen Dover: Corporate earnings have not only been strong but also coordinated around the world, which is the first time that’s happened in quite a while. Earnings continue to surprise on the upside, especially in emerging markets, and to some degree in Europe now, too. I think as long as interest rates rise on a measured basis, that’s probably priced into the market at this point. The environment is relatively benign, and markets are relatively calm, so the risk is that if there’s a shock, I think the markets are probably not really prepared.

Ultimately, as long as companies have earnings growth, the market should be able to keep moving higher. Europe has seen some economic turnaround and some positive political developments. European banks are doing better than many had thought they would. Financials in general still haven’t completely recovered from the 2007-2009 global financial crisis, providing additional upside potential. So we still see opportunities in that space, to some degree.

However, there are some big tail risks in Europe that probably are not priced into the market at this point. We also see a lot of opportunity in emerging markets where there is growth and positive political change—at least in select emerging markets such as in Latin America.

Market Stability or Volatility—How Should Investors Prepare?

Q: In spite of different risk factors, equity-market volatility remains near historic lows. How should investors think about risk in equity markets right now?

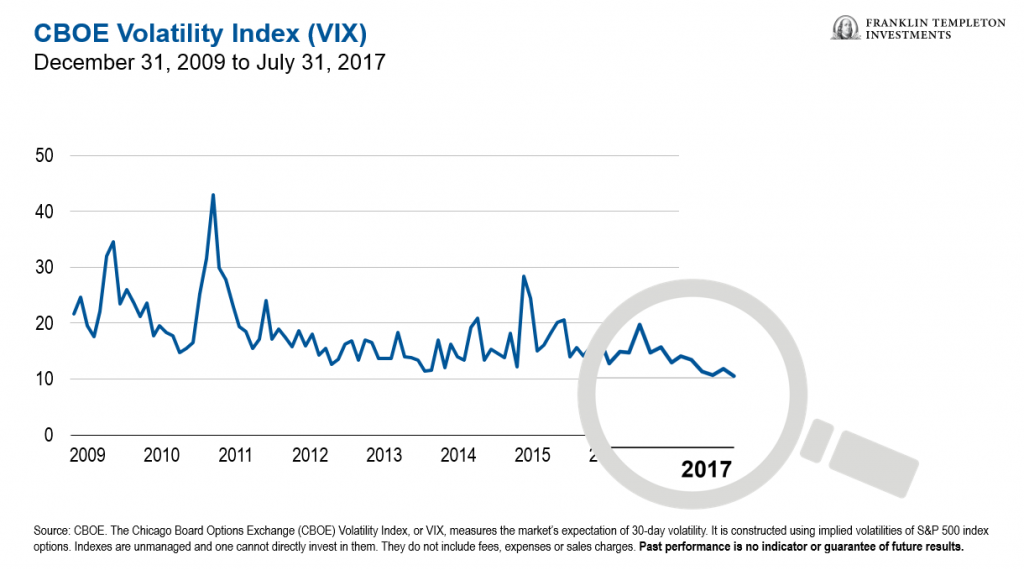

Ed Perks: I think it’s important to step back beyond just the last 12-15 months. If you take a longer perspective, just two years ago the markets saw substantially higher volatility. Broader global equity indexes experienced a sharp correction from the middle of 2015 to the early part of 2016. That said, I think this current period of low volatility has come with a lot of benefits. In the years since the global financial crisis, the purpose of the Fed’s monetary actions, and of global central-bank actions in general, was to bring down volatility in asset classes and more broadly in the economy, and we certainly received some benefits from that. We have seen the US and global economies continue to grow at a relatively modest pace. I think the low market volatility we have seen likely had some influence on the relatively strong business and consumer confidence that exists today. For investors, it has enabled more of a focus on fundamentals, which have been strong.

However, this period of relatively low—I wouldn’t say unprecedented, but I would say relatively low—volatility is unlikely to persist. From my perspective, the unknowns would be the more significant risks that might lie out there. During the last several years, we have seen a tremendous amount of assets move into passive strategies. So, to what extent will we see algorithmic, indiscriminate selling of equities, of assets in general as volatility moves higher? That’s something that we are a bit concerned about and something I think investors need to think about.

Stephen Dover: To Ed’s point, passive funds are in essence momentum players—buying “high” on appreciating stocks that get progressively larger weightings in an index while selling “low” on those that depreciate and get progressively smaller in the index, regardless of the stocks’ future upside potential. The possibility of indiscriminate selling is one of the things we are looking at from a research point of view. We are looking at how much a company is owned by indexes, or by passive investors, because that money could move out very quickly and affect the company.

The Elephant in the Investment Room

Q: How are exogenous political risks influencing your investment thesis?

Chris Molumphy: I think the markets have done a reasonably good job looking through some of these non-fundamental bouts of volatility—political, geopolitical and otherwise—and have held up reasonably well. But to your question, exogenous risks make things a bit more difficult. At the same time, if you can stick to your main investment thesis, the fundamentals and a longer-term horizon, you can use these events as opportunities. Bouts of market volatility can create buying opportunities. What we try to do is determine whether near-term risks are going to impact longer-term fundamentals. More often than not, they tend to be more transitory in nature.

Michael Hasenstab: The shift in many emerging markets to more orthodox policy has been an area of opportunity for us. In the United States and in Europe, there is a much more charged political environment and, in some cases, the abandonment of orthodox policy. In places like Mexico, for example, policymakers stuck to their guns and hiked interest rates to protect their currency (despite speculative attacks), followed through with fiscal reform and liberalized the energy sector. We have seen a very sharp snapback in the peso.

Meanwhile, Brazil has been targeting corruption in a more forceful manner than ever there. I think that is going to lead to some positive political changes. And Argentina has done a 180 degree about-face under President Mauricio Macri to re-embrace market principles and get the economy started again. India’s Prime Minister Narendra Modi has embarked upon a very rigorous reform of the tax system and has set in place inflation targeting with the central bank. So there have been a lot of positive fundamental changes in emerging markets that I think will pay dividends for years to come.

In Europe, we are a little more cautious medium term. With growth improving, there is unlikely to be a major flashpoint in the short term, in my view. However, we are seeing nationalism grow at levels that it hasn’t for decades. The desire for Europe to come together seems to be changing and there’s more national identity as opposed to European identity. Longer term, I think that’s going to be a big challenge for the eurozone.

Stephen Dover: A lot of what goes on in politics doesn’t necessarily affect corporate earnings that much—at least in the short term. Overall, I think the political environment hasn’t had a huge impact on the equity market because it hasn’t actually affected earnings streams.

Like Michael, I am pretty enthusiastic about emerging markets that seem to be more progressive than the developed markets are. In Brazil, as Michael mentioned, an unpopular government is making dramatic changes. These changes are low-hanging fruit in the sense that they are likely to have a very positive economic impact and, ultimately, I think, on the earnings stream for many companies in Brazil.

Ed Perks: At the risk of oversimplifying it, I think diversification is the best rule to follow when you are thinking about a broader portfolio. Do markets see a rise in correlation across asset classes? That’s something I think investors have to be very mindful of. As investors ourselves, ultimately, we need to access as broad and strong a set of building blocks for our portfolios as possible. Generally, with many markets at different levels of valuation in terms of attractiveness, we increasingly want to be very specific with the exposures we might be getting in particular asset classes.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. High yields reflect the higher credit risk associated with these lower-rated securities and, in some cases, the lower market prices for these instruments. Interest rate movements may affect the share price and yield. Treasuries, if held to maturity, offer a fixed rate of return and fixed principal value; their interest payments and principal are guaranteed.

Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Such investments could experience significant price volatility in any given year.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments