Introduction

Countless articles have been written in the past 10 years predicting (or warning) of China’s imminent financial demise, with the number of articles accelerating in recent years amid China’s debt build-up in the post Global Financial Crisis period. Investing on the basis of a “China collapse” view of the world would likely have resulted in more risk-averse portfolios in the emerging debt space and, hence, lower returns in recent years. Our investment process, which is heavily skewed toward finding underpriced securities (bottom-up) rather than making global macro calls, or even country calls, for the most part exempts us from having to take a view on topics such as if and when China is going to collapse. That being said, China’s presence in our asset class is increasing and, as alpha-focused investors, we are aware of our direct and indirect China exposures and the relative value of China exposures. This paper provides our readers with a glimpse into how we view China’s sovereign, quasi-sovereign, rates, and FX exposures.

China’s Increasing Presence in the Asset Class

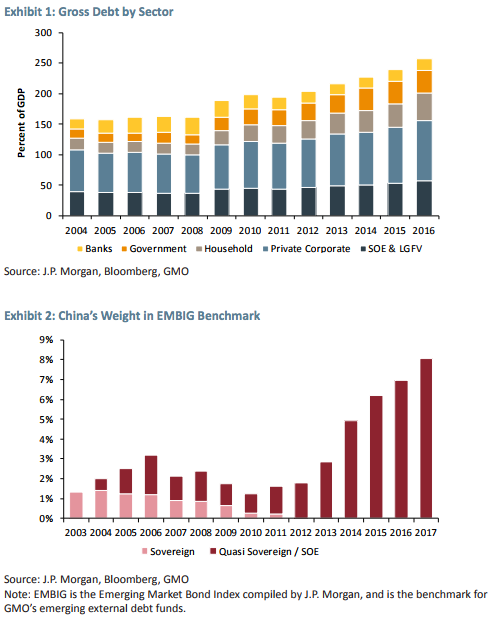

China’s well-documented debt build-up has had a significant impact on the emerging debt asset class. Since the Global Financial Crisis in 2008, China has done the world a big favor by boosting growth through a debt-financed investment spending binge. The aggregate debt-to-GDP ratio of “China Inc.” (corporates, households, governments, and banks) has doubled and now stands at about 258% of GDP.2 During this period, China contributed over half (57%) of the world’s nominal growth in GDP, measured in US dollars.3 In doing so, it sucked in commodities from all corners of the earth.

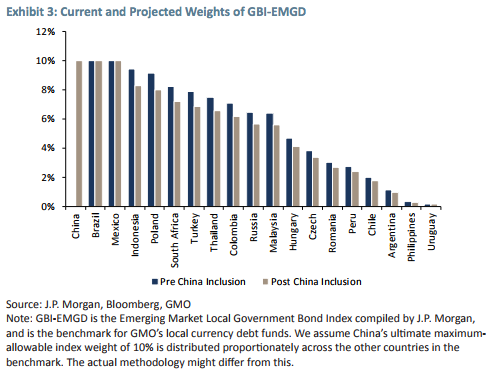

As seen in Exhibit 1, more than half of the 100% of GDP in incremental debt has been incurred by the corporate and state-owned enterprise (SOE) sector. The rest was split between government and households to levels that are, by international standards, not very alarming. The increase in SOE and corporate debt has had a dramatic impact on certain emerging debt benchmarks. Exhibit 2 shows China’s weight in the EMBIG benchmark of dollar-denominated sovereign and quasi-sovereign debt. Two things are notable. First, in the past five years China has gone from relative insignificance in this benchmark (with a weighting akin to countries like Lebanon, Kazakhstan, Panama, and Lithuania) to a weighting of more than 8% as of June 2017, second only to Mexico. Second, the entire China component of the benchmark is comprised of quasi-sovereign issuers that are, by the criteria of index inclusion, 100% owned by the Chinese government (more on this later).

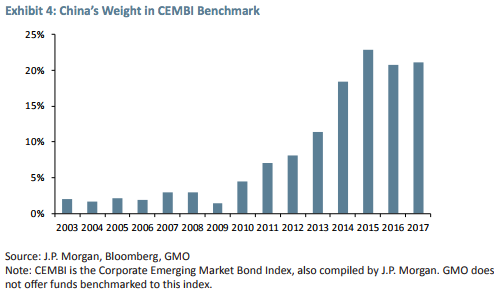

In terms of local debt markets, China is currently unrepresented (please see “The What-Why-WhenHow Guide to Emerging Country Debt: 2017 Edition” for more detailed discussion), but this is likely to change in the next 12 to 18 months. The authorities are taking aggressive steps to open the onshore debt markets to foreign investors, which is a necessary condition to meet liquidity and transparency requirements for inclusion in, for example, J.P. Morgan’s GBI-EMGD local debt benchmark.4 China’s domestic government bond market is the third largest in the world, at about $1.8 trillion, which dwarfs the entire market capitalization of the GBI-EMGD, at $1.2 trillion. It follows, then, that China’s weighting will eventually be at the 10% cap. Exhibit 3 shows the current weightings of the benchmark and our estimate of the pro-forma weightings after China is fully incorporated into the index.5 Weightings of Brazil and Mexico, which are also at the cap, are unlikely to change, but several countries could see their weights drop by a percentage point or more.

Possible future inclusion in the local debt benchmark is consistent with China’s growing role in the world economy. China’s impact on trade flows and supply chains has skyrocketed since it joined the World Trade Organization in 2001. Recent steps have paved the way for a more important role in global capital markets.6 China has become the largest bilateral lender to many emerging countries, and this status is likely to grow as a result of the Belt and Road Initiative, and various multinational development banks in which China is taking a leadership role. The CNY has gained inclusion in the SDR basket of currencies, and gained inclusion of its onshore equity markets to the MSCI indices. China’s future inclusion in the local debt benchmark is likely to affect the benchmark more than China’s domestic capital markets. Assuming a 10% cap on China’s weighting, this would correspond to about $120 billion equivalent of Chinese bonds being included in the benchmark. While this would be 10% of the benchmark, it would represent only about 7% of China’s domestic government bond market of $1.8 trillion. This is unlikely to have much impact on China’s own financial markets, but it is consistent with the creeping importance of China in the world. This is also why China is lobbying to be included in the much larger Bloomberg Barclay’s Aggregate Index (formerly Lehman Aggregate) and the Citibank World Government Bond Index. These are potentially more impactful for China. Whereas the GBI-EMGD has only an estimated $200 billion in benchmarked assets under management, the other two larger benchmarks have an estimated $4 trillion in AUM.

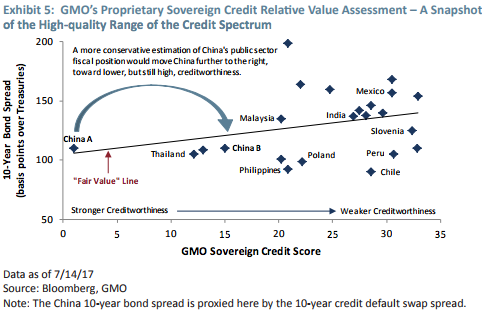

Finally, Exhibit 4 shows the staggering increase in the Chinese weighting in the CEMBI index of emerging corporate bonds, which has gone from relative obscurity in 2009 to more than 20% currently. The next largest country is Brazil, at 12.7%. This chart is meant to be illustrative of China’s rising influence. It is doubtful that dedicated corporate EMD managers would benchmark themselves to this version of the CEMBI. The CEMBI Diversified, for example, shaves China’s weighting all the way to 8.7%, effectively distributing the balance across the other 41 countries represented in that index.

Valuation Considerations – External Debt

Many of our readers will be familiar with our sovereign credit risk assessment process, which scores countries on their relative strength across three risk vectors – Economic Structure, Fiscal Sustainability, and External Liquidity. Our analysis, which is based on statistical estimation techniques applied to economic data that is as accurate as we can ascertain, scores China as the strongest sovereign credit among the roughly 80 of our investable emerging market countries, as seen in Exhibit 5. The exhibit plots GMO’s Sovereign Credit Score, which is on a scale of 1 (best) to 100 (worst) against 10-year external sovereign bond spreads. The chart is “cut off ” at a score of 35 to focus on the investment-grade end of the credit spectrum. Fair value is determined by the regression line through the data. Countries whose 10-year bond spread falls below the fair value line (e.g., Philippines, Poland, and Chile) look expensive in relative terms, while those above the line (e.g., Mexico, and Malaysia) look cheap.

Why does China anchor the high-grade end of our credit spectrum? China’s score on Economic Structure is strong, owing to its track record of high and stable GDP growth, rising GDP per capita, and strong competitiveness, among other attributes. China is one of the few countries in our investment universe that has a reasonable chance of moving from middle income to high income in the next 20 years, following in the footsteps of other regional economies like South Korea, Taiwan, and Singapore. External Liquidity is also very strong, by our measures, due to consistent surpluses in the current account of the balance of payments, massive foreign exchange reserves, and relatively low external indebtedness at both the sovereign and overall country level.

If there is a weakness in China’s creditworthiness, as we see it, it is in Fiscal Sustainability. The outsized state role in the economy makes it difficult to assess China’s fiscal policy. What we know is that fiscal deficits have been running in the 2-3% of GDP range for several years, and the narrowly defined government debt-to-GDP ratio is around 40%. These numbers place China squarely in investmentgrade territory, where we think it belongs. However, more conservative approaches to China’s public finance analysis attempt to quantify the fiscal impulse coming from debt-financed local government spending, state policy banks, and SOEs. On this basis, China’s fiscal deficit could be as high as 10% of GDP and the debt-to-GDP ratio could be double the 40% figure. Were this to be the true reflection of China’s fiscal stance, it would look more like a speculative-grade country on this one measure. Our model allows us to easily stress test our assumptions, and when we plug in these higher fiscal deficit numbers, China’s score moves from 1 to about 15 (China A to China B in Exhibit 5). China sovereign credit risk goes from being slightly cheap to about fair, as the slope of the fair value line at the investment-grade end of the spectrum is fairly flat.

On this basis, and the fact that EMBIG currently trades at a spread of around 300 bps to Treasuries, there is little compelling reason to own China from a top-down perspective. Given that currently the benchmark is comprised entirely of quasi-sovereign names, might there be opportunities in this space for security selection? Our quasi-sovereign research process, like our sovereign research process, is a multi-pillar assessment that takes account of the company’s stand-alone creditworthiness, the sovereign’s ability to support the company in a time of stress, and the sovereign’s willingness to support the company based on its strategic importance and other factors. Using these inputs, we statistically estimate a risk-neutral “fair value” spread over the sovereign that we should demand for owning the given SOE.

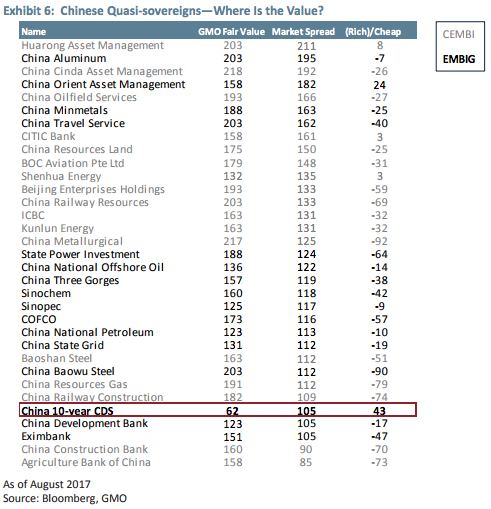

In Exhibit 6, we show our valuation estimates for our universe of Chinese quasi-sovereigns (in-EMBIG and beyond).7 Two things stand out. First, some of the quasi-sovereigns trade at spreads very close to or lower than the China sovereign credit default swap (CDS) spread. We do not think this makes sense. We fundamentally believe that companies, whether or not they are strongly supported by the government, should offer substantially higher spreads than their respective sovereigns. They are less liquid, offer poor recourse for creditors in the event of default, and have additional (idiosyncratic) default risk above that of their sovereign. They don’t offer much risk diversification, because a sovereign default usually triggers a default of all the associated corporates.8 Second, of the SOEs that offer a spread higher than that of China sovereign CDS, relatively few meet our model’s valuation hurdle, where the actual spread is higher than the GMO fair value spread. None in the sample of 32 offers a spread that is meaningfully higher than our assessment of fair value.

From an investment process perspective, we note that our model is global in nature. Therefore China, where quasi-sovereigns in general are tighter to the sovereign than elsewhere, will tend to screen rich. Digging in deeper, we also find structural deficiencies in bond documentation across Chinese issues.9 Separately, we can imagine that, owing to the broad inclusion of such issues across global and regional investment-grade bond benchmarks, there may be an outsized demand for such issues relative to supply. This latter effect seems particularly pronounced in Chinese investment-grade issues relative to other EMBIG investment-grade quasis.

Based on the preceding analysis, our direct exposure to China in our external debt portfolios is significantly underweight.

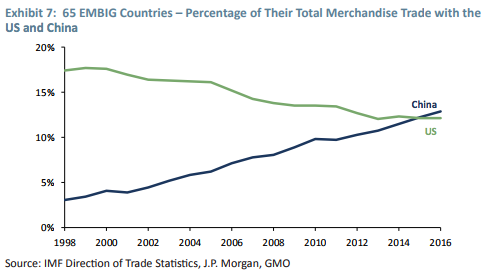

However, we are also mindful of our indirect exposure to China, owing to the country’s growing importance in the global economy. China’s impact on emerging countries mostly flows through the trade channel, as opposed to the United States, which still affects emerging countries through both the financial and trade channels. Exhibit 7 demonstrates the growing importance of China’s trade relations with the emerging world. For the aggregated countries of EMBIG, we contrast the falling share of total bilateral merchandise trade between them and the United States and the growing share between them and China. Recently, China overtook the United States in terms of the value of trade with the EMBIG subset of 65 emerging countries. We can imagine this continuing in light of the tilt toward economic nationalism in the United States, countered with President Xi Jinping’s stated unwavering commitment to globalization.

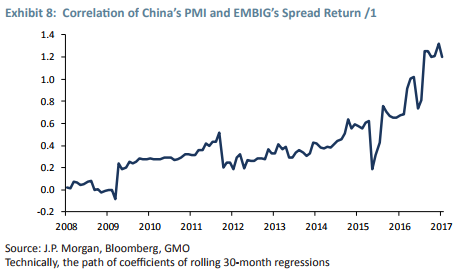

Given this secular shift in trade flows, it might not be surprising that China’s economic performance has come to have a growing influence on emerging country financial assets. In Exhibit 8, we show the correlation10 of China’s Purchasing Manager’s Index (PMI) with EMBIG’s spread return (total return excluding the component attributable to changes in U.S. treasury yields). Note the rising correlation, interrupted by a few events that were unrelated to China. This chart is consistent with our intuition that a portfolio of emerging country bonds has an increasing correlation with China’s economic performance. To date, this correlation has been largely beneficial to returns, since China’s economy has continued to grow at a rapid pace. However it also underscores the negative impact that a hard landing scenario in China could have on the market.

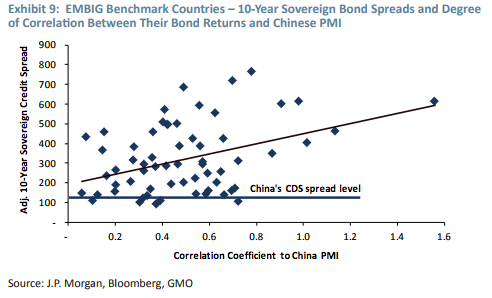

We dug a little deeper into the data, and asked if there was any pattern to the types of countries that display a higher correlation to China’s PMI. We found two observations that were consistent with our intuition and supported by the data. The first was that there is a significant relationship between such correlation to China’s PMI and a country’s commodity dependence, measured by the ratio of commodity exports to total exports.11 The second was that countries with a higher correlation with China would also tend to have higher-yielding bonds. This is shown in Exhibit 9. One conclusion we can draw is that there may be numerous ways to get indirect China exposure with a much higher yield than direct Chinese sovereign and quasi-sovereign obligations.

Valuation Considerations – Local Currency Debt

Traditionally, our local debt portfolios have had zero exposure to local Chinese rates, but they have had exposure to the RMB as an off-benchmark position. Our investment process considers three “exposures” present in a local currency sovereign bond: sovereign default exposure, local interest rate (duration) exposure, and currency exposure. Sovereign default exposure is covered jointly with our external debt process and has already been discussed.

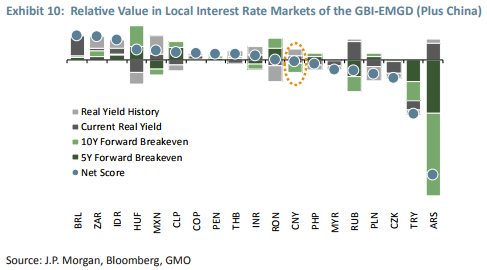

Our local interest rate relative value model considers measures of term structure, rewarding countries with relatively steep yield curves, as well as real yield differentials relative to other countries and relative to the country’s own history. Countries with high real yields are favored by the model’s specifications, but this factor is moderated by comparing the current real yield to its own history. Exhibit 10 shows how China would stack up against the other 18 countries in the GBI-EMGD. The chart is somewhat skewed, owing to Argentina’s recent inclusion, but China’s local rates market results in a net score that is slightly negative, suggesting a slight underweight for our portfolios. China scores poorly on 5-year and 10-year breakeven rates, indicative of a flat yield curve and market expectations of persistent low rates. China scores better on the level of real yields currently and relative to its history.

Turning to currency valuation, we view the CNY as a heavily managed currency, and therefore it does not fit into our standard relative value model, which considers measures of momentum, and economic cycle (such as interest rate differentials) across countries. The future path of the CNY will depend on some combination of economic fundamentals and “other considerations,” which could include Communist Party priorities for economic stability and growth, Trump administration trade policies, and Chinese policy desires to gain more global financial influence.12

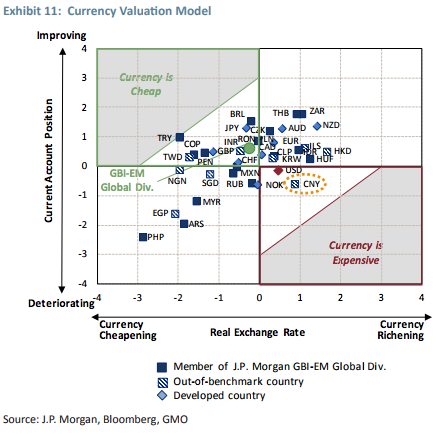

Our current long-term valuation model for currencies is shown in Exhibit 11. The model analyzes trends in real effective exchange rates and the balance of payments, and via a z-score analysis measures how far away current values are from their longer-term averages. Note the “bunching” of currencies in the middle zone of this chart, where it is difficult to have strong conviction on the richness or cheapness of any of the currencies covered. However, the CNY is currently among the richest currencies on this model, and this partially explains our current underweight (short) position in the renminbi. Note also the weighted average score of the current local debt benchmark, marked by the green dot in the exhibit. It is on the cheap (attractive) side of neutral as we currently estimate it, and introduction of the CNY at a 10% weight would almost surely reduce the aggregate attractiveness of benchmark currencies, making relative value selection within the benchmark currencies even more important.

Regarding our indirect exposure to CNY and Chinese local rates markets, we’d expect much less than is the case in external debt. Emerging local rates markets are more likely to be influenced by domestic macroeconomic policy factors, and G-3 monetary policy, than China’s domestic policy factors. Work that we’ve done on correlations suggest that, based on historical data, Chinese rates have low correlation with other global rate markets, but the rates markets with higher correlation with China tend to be low volatility, “safe haven” markets such as Thailand, United States, Israel, and Singapore, among others.

Not surprisingly,13 however, indirect exposure of China in our currency selection process is somewhat more pronounced. Exhibit 12 shows correlations (betas) of the currencies in the GBI-EMGD benchmark to the CNY, looking back three years. Several currencies have shown strong correlation with the CNY, including the ZAR, COP, RUB, MYR, TRY, and MXN. With the possible exception of MYR where FX policy has tended to mirror that of China, we’re not sure what fundamental justification exists for these currencies to be so highly correlated with the CNY. We think the correlations have more to do with overall risk sentiment in the market than any fundamental economic rationale. Thus, since the CNY is a heavily managed currency, it is relatively stable most of the time, but when the CNY is volatile, the global risk environment for emerging markets has pivoted to “risk off.” The currencies that are most highly correlated with the CNY have some combination of the following characteristics: 1) high yield; 2) a high volatility; and 3) highly liquid and therefore convenient for risk hedging. In Exhibit 12, we focus on the second factor – volatility – but if we were to plot currency implied yields, the result would be similar.

Thus, we come to a similar conclusion as we did with external debt. Namely, we have potentially significant indirect exposure to China in our local debt portfolios, owing to China’s rising systemic relevance in the global economy and financial markets. When China enters the GBI-EMGD, which may be considered in 2018, its relevance will only increase. This should present us with choices for security selection alpha via direct exposure to China’s debt markets, or via more attractively priced securities elsewhere in the opportunity set.

Carl Ross. Dr. Ross is engaged in research for GMO’s Emerging Country Debt team. Prior to joining GMO in 2014, he was a managing director at Oppenheimer & Co. Inc. where he covered emerging debt markets. Previously, he was the Senior Managing Director and Head of Emerging Markets Fixed Income Research at Bear Stearns & Co. Dr. Ross earned his BA in Economics from Mount Allison University as well as his M.A. and PhD in Economics from Georgetown University.

Disclaimer: The views expressed are the views of Carl Ross through the period ending September 2017, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2017 by GMO LLC. All rights reserved.

© GMO

Read more commentaries by GMO