We have seen a powerful recovery in asset prices in the wake of the global financial crisis (GFC). We cannot forget, however, that more than $15 trillion in asset values evaporated in 2008–2009, wiping out gains earned in the bull markets of the 1990s and early 2000s. During the GFC, clients were horrified and did not know what to do. Of course, in hindsight, the right thing to do was to ride out the storm; some investors sold out and regret it to this day. History has shown that markets are cyclical, so another bear market will occur again, it is just a matter of time. When times are good, as they have been for the past eight years, our skills as advisors can get dull because we haven’t had to deal with panicky, stressed-out clients. But we need to stay on top of our game. Knowing that markets can grow suddenly violent, financial advisors must be able to diagnose irrational behaviors and advise their clients accordingly. That means incorporating behavioral finance into our practices.

Behavioral Finance

The way investors think and feel affects their investment behaviors. Some investor behaviors are unconsciously influenced by past experiences and personal beliefs to the extent that even intelligent investors may deviate from logic and reason. These influences, or behavioral biases, can affect the way risk is perceived. In Pompian (2006), I introduced a way to categorize biases. The broadest category is cognitive and emotional. Cognitive biases involve how people think and emotional biases involve how people feel. Cognitive errors result from memory and information-processing errors—that is, faulty reasoning. Emotional biases lead to reasoning influenced by feelings. This distinction is critical.

Cognitive biases can be broken down into belief-perseverance and information-processing biases. Belief-perseverance biases affect people who have a hard time modifying their beliefs even when faced with information to the contrary. It is a very human reaction to feel uncomfortable when new information contradicts information you hold to be true. For example, for decades many people have been under the false impression that eating sugar produces hyperactivity in children. Twenty years ago, several studies examined the effects of sugar on children’s behavior and concluded that sugar in the diet does not affect children’s behavior (Wolraich et al. 1995). But many people continue to believe that it does; this is an example of belief perseverance. Related biases include cognitive dissonance, conservatism, confirmation, representativeness, illusion of control, and hindsight.

Information-processing biases affect people who make thinking errors when processing information. The simplest example is anchoring, where people tend to estimate something based on an initial default number. If I asked you to estimate the population of Canada and remarked that I did not know whether it was higher or lower than 30 million, you would probably “anchor” your estimate to that number and adjust from there rather than make an independent estimate. Information-processing biases include anchoring and adjustment, mental accounting, framing, availability, self-attribution, outcome, and recency.

Emotional biases are based on feelings rather than facts. Emotions can overpower our thinking during times of stress. All of us likely have made irrational decisions during our lives. Emotional biases include loss aversion, overconfidence, self-control, status quo, endowment, regret aversion, and affinity.

The distinction between cognitive and emotional biases is critical when assessing risk tolerance. Advisors often need to adapt to client behaviors caused by emotional biases because it is hard to change the way people feel. With cognitive biases, however, advisors have an opportunity to modify or change clients’ thinking and moderate clients’ behaviors.

Figure 1 shows a simple framework for applying behavioral finance in practice that I have used in my advisory practice over the past 20 years to solve vexing challenges of client relationship management.

Defining Risk

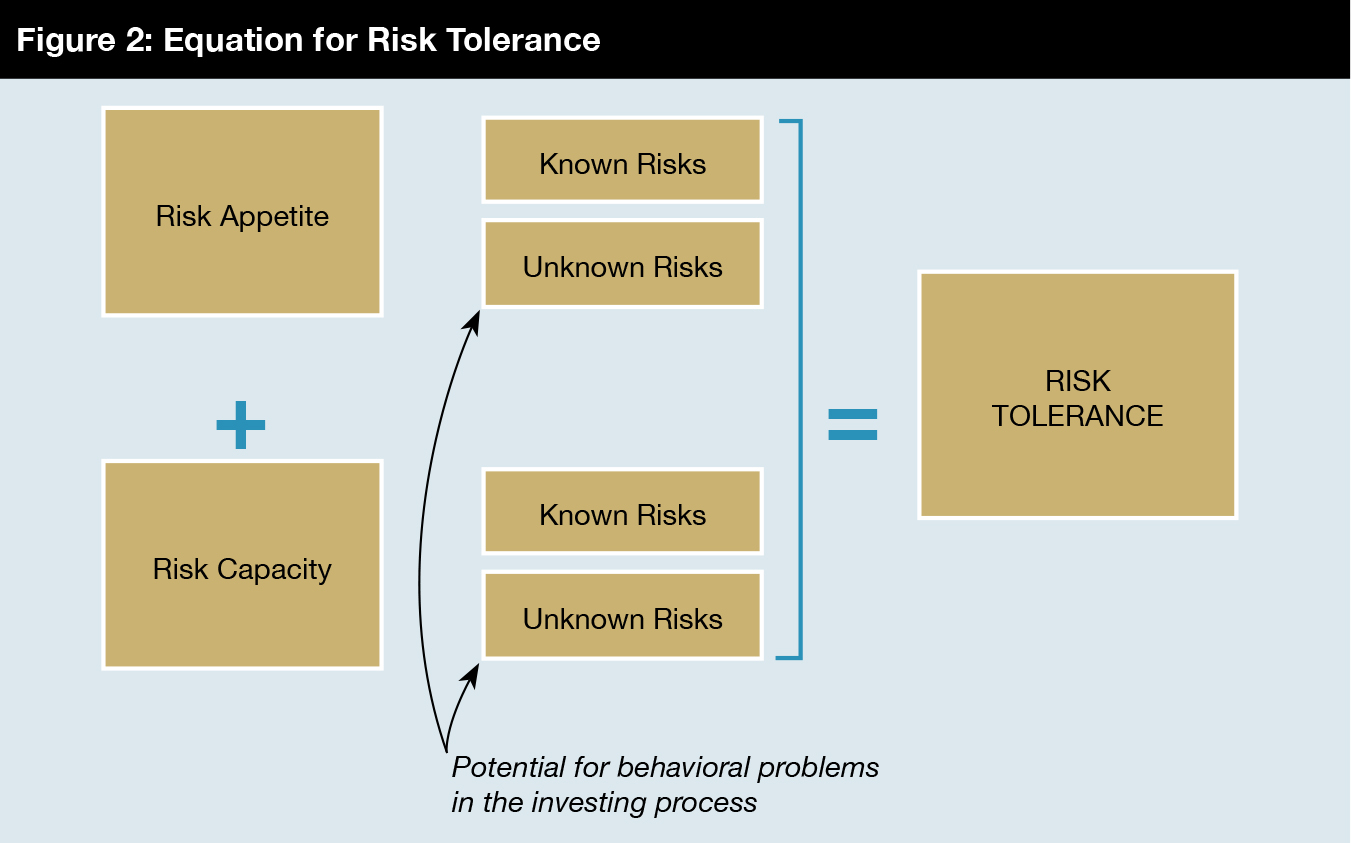

There are lots of aspects to risk. Risk appetite generally is the willingness to take risk, and risk capacity is the ability to take risk. We further define risk appetite and risk capacity in terms of known and unknown risks, because when clients can understand and measure the risks they are taking, they can accept the results. But problems arise when the risks fall outside the bounds of what they expect or understand.

Risk appetite is the amount of risk that one is willing to take in pursuit of reward. Risk appetite varies per expected return; it may be expressed qualitatively and/or quantitatively. Investors with a high risk appetite focus on the potential for significant gains and are willing to accept a higher possibility or severity of loss. Conversely, investors with a low risk appetite are risk-averse and focus on stability and preservation of capital.

The level of both risk appetite and risk capacity varies by individual; obviously, investors should not define their risk appetite without considering their risk capacity, but sometimes they do. In the end, risk capacity is the amount of risk a person can actually bear. On the one hand, an investor may have a high risk appetite but lack the capacity to handle the potential volatility or impact. Or risk capacity may be high but the investor may have a lower risk appetite. Advisors can get a handle on these issues with their clients relatively easily for known risks. Unknown risk, which is not so easily measured, is often associated with irrational investor behavior.

Known and Unknown Risk

Donald Rumsfeld, U.S. secretary of defense under President George W. Bush, famously described known and unknown risk: “There are known knowns. These are things we know that we know. There are known unknowns. That is to say, there are things that we know we do not know. But there are also unknown unknowns. There are things we don’t know we don’t know.”1

Clients may tell advisors that they have certain risk appetites and risk capacities. But do the advisor and the client agree on what is meant by risk? How much known risk and how much unknown risk can the client handle? Known risk is what we might call “normal risk”—risk we can comprehend easily and quantify using historical data from observations of financial markets. But what about unknown “abnormal” risk, the kind that occurs once every 10 or 20 years and falls outside expectations? We can think of normal risk as one or two standard deviations from the normal. We can think of unknown risk as three or more standard deviations from the normal. Although severe bear markets and crashes occur from time to time, 2008–2009 can be categorized as an unknown or abnormal risk. At that time, portfolio return fell outside the expected range of most models based on a normal distribution of returns.

When a decision is made about how much risk to take (risk appetite) or a measurement is taken of how much loss can be tolerated without jeopardizing financial goals (risk capacity), unknown risk can cause investors to behave irrationally. People must consider their likely reaction to known risk and especially unknown risk to get a complete picture of their risk tolerance. Figure 2 combines these concepts to graphically represent an equation for risk tolerance.

Risk Tolerance and Behavioral Finance

Consider the concept of behavioral investor types (BITs). BITs can be identified using my Behavioral Alpha® (BA) process. BA is a multi-step diagnostic process that classifies clients as one of four investor types. Bias identification, which is done near the end of the process, is based on the client’s risk tolerance.

BITs were designed to help advisors make rapid yet insightful assessments before recommending an investment plan. By ascertaining investor type at the outset of a relationship, an advisor can mitigate client behavioral surprises that might dispose a client to change the portfolio because of market turmoil. If an advisor can limit traumatic episodes by delivering smoother (or closer-to-expected) investment results by tailoring an investment plan to the client’s behavioral makeup, a stronger client relationship is the result. Here each BIT is characterized by a certain risk tolerance level and a primary type of bias—either cognitive (driven by faulty reasoning) or emotional (driven by impulses and/or feelings).

Advisors should keep in mind that the least risk-tolerant investors and the most risk-tolerant investors are driven by emotional biases, whereas the two types between these extremes are driven by cognitive biases (Pompian 2012). Emotional clients, however, tend to be more difficult to work with. Advisors who can recognize the type of client they are dealing with before making investment recommendations will be much better prepared to deal with irrational behavior when it arises.

Guidelines for Practitioners

As discussed, the least risk-tolerant BIT clients and the most risk-tolerant BIT clients are emotionally biased in their behavior. In the middle of the risk scale are BITs that are affected mainly by cognitive biases. This dynamic should make intuitive sense. Emotion drives the behavior of clients who have a high need for security (i.e., a low risk tolerance); they get emotional about losing money and are uneasy during times of stress or change. Similarly, highly aggressive investors are also emotionally driven people who typically suffer from a high level of overconfidence and mistakenly believe they can control the outcomes of their investments. Between these extremes are the investors who suffer mainly from cognitive biases, and education and information about their biases can help them make better investment decisions. With aggressive clients, the best approach is to deal with their biases head-on and discuss how their investment decisions will affect family members, legacy, and standard of living.

Clients who are emotional about their investing need to be advised differently from those who make mainly cognitive errors. When advising emotionally driven investors, advisors need to focus on how an investment program can affect important emotional issues such as financial security, retirement, and the impact on future generations—rather than focusing on portfolio details such as standard deviations and Sharpe ratios. A quantitative approach is more effective with clients who are less emotional and tend to make cognitive errors. The goal is to build better long-term relationships with clients, and BITs were designed to help in this effort. The four BITs are conservative, moderate, growth, and aggressive; brief descriptions of the types, their common biases, and thoughts about how to advise each type of client are included.

Continue reading this article now.

Download this article PLUS two additional articles from IMCA’s Investments & Wealth Monitor now.

Michael M. Pompian, CFA®, CAIA®, CFP®, is chief executive officer and chief investment officer of Sunpointe Investments. He earned an MBA in finance from Tulane University and a BS in management from the University of New Hampshire. Contact him at [email protected].

© IMCA